CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

8-19

Ex. 8–28

a. Year 3: $4,118.5 per month ($49,422 ÷ 12)

b. Year 3: 6.2 months ($25,668 ÷ $4,118.5)

c. At the end of Year 1, Amicus Therapeutics had 5.4 months of cash and cash

equivalents remaining to use in operations. During Year 2, Amicus issued $45

million of additional stock, which increased its ratio of cash to monthly cash

expenses to 25.4 months. In addition, negative cash flows from operations

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

8-20

Prob. 8–1A

Strengths: a, b, e, and f

Weaknesses:

c. Employees should not be allowed to use the petty cash fund to cash personal

d. Requiring cash register clerks to make up any cash shortages from their own

funds gives the clerks an incentive to shortchange customers. That is, the clerks

will want to make sure that they don’t have a shortage at the end of the day. In

g. The mail clerk should prepare an initial listing of cash remittances before

forwarding the cash receipts to the cashier. This establishes initial accountability

PROBLEMS

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

8-21

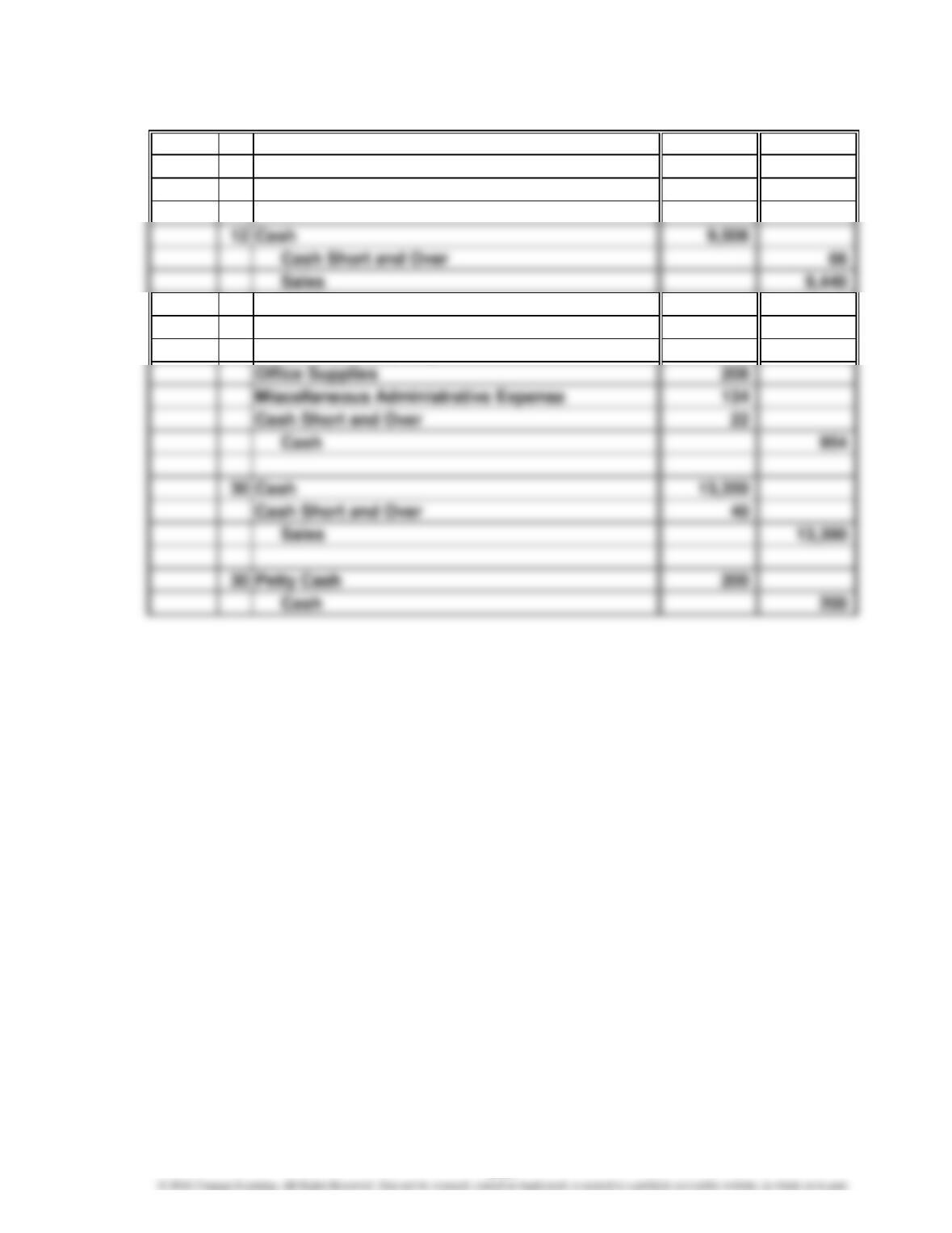

Prob. 8–2A

1 Petty Cash 750

Cash 750

12 Cash 12,465

Cash Short and Over 25

Sales 12,440

2016

Oct.

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

8-22

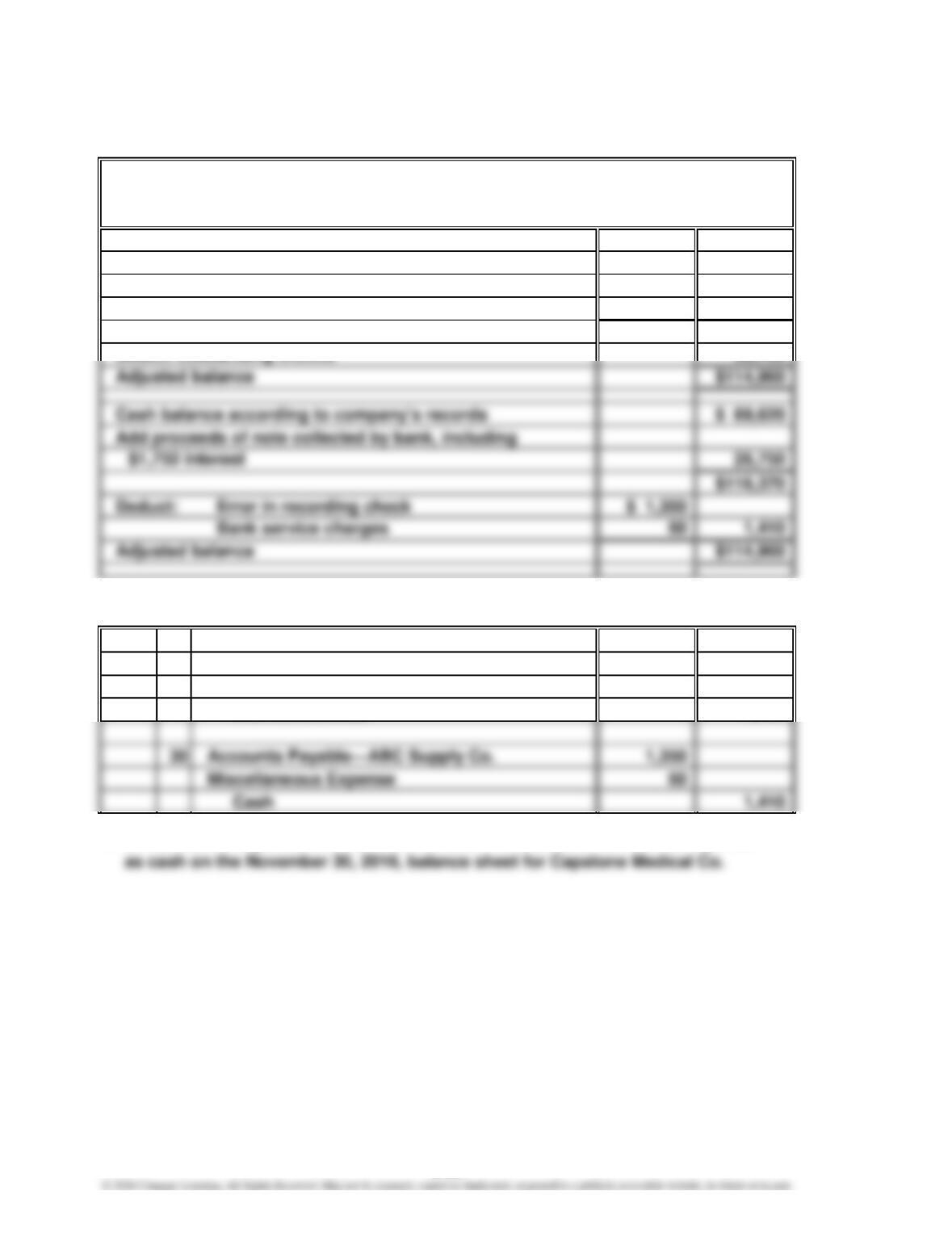

Prob. 8–3A

1.

Cash balance according to bank statement $128,660

Add:

Deposit of November 30, not recorded by bank $18,550

Bank error in charging check as $940 instead

of $490 450 19,000

$147,660

Deduct outstanding checks 32,700

Deduct:

2.

2016

Nov. 30 Cash 26,750

Notes Receivable

25,000

Interest Revenue

1,750

3. $114,960; the adjusted balance from the bank reconciliation should be reported

CAPSTONE MEDICAL CO.

Bank Reconciliation

November 30, 2016

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

8-23

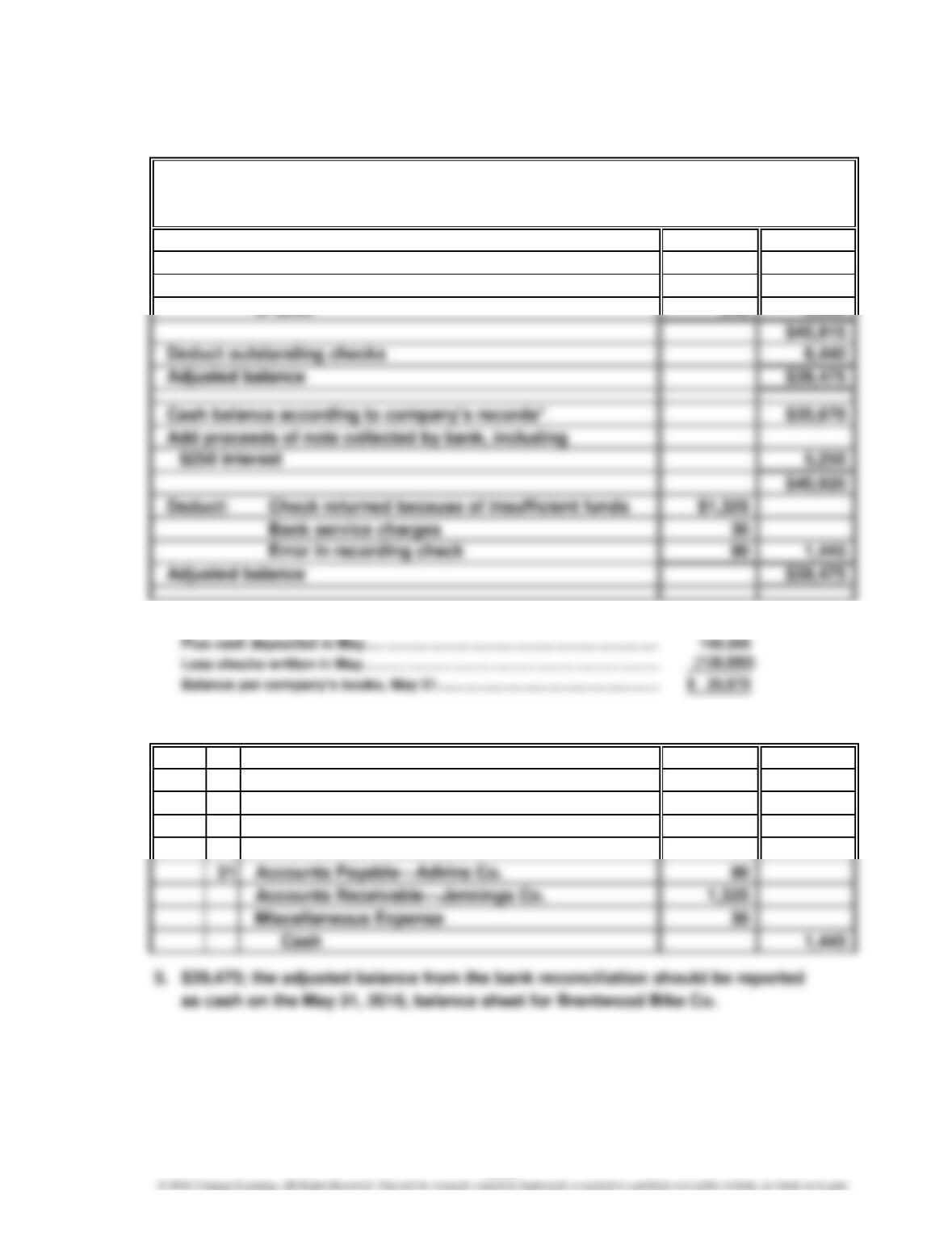

Prob. 8–4A

1.

Cash balance according to bank statement $43,525

Add: Deposit of May 31, not recorded by bank $1,850

Bank error in charging check as $930 instead

of $390 540 2,390

*

Cash balance, May 1…………………………………………………………………

$34,250

Plus cash deposited in May………………………………………………………

Less checks written in May…………………………………………………………

Balance per company’s books, May 31…………………………………………

2.

2016

May 31 Cash 5,250

Notes Receivable

5,000

Interest Revenue

250

BRENTWOOD BIKE CO.

Bank Reconciliation

May 31, 2016

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

8-24

Prob. 8–5A

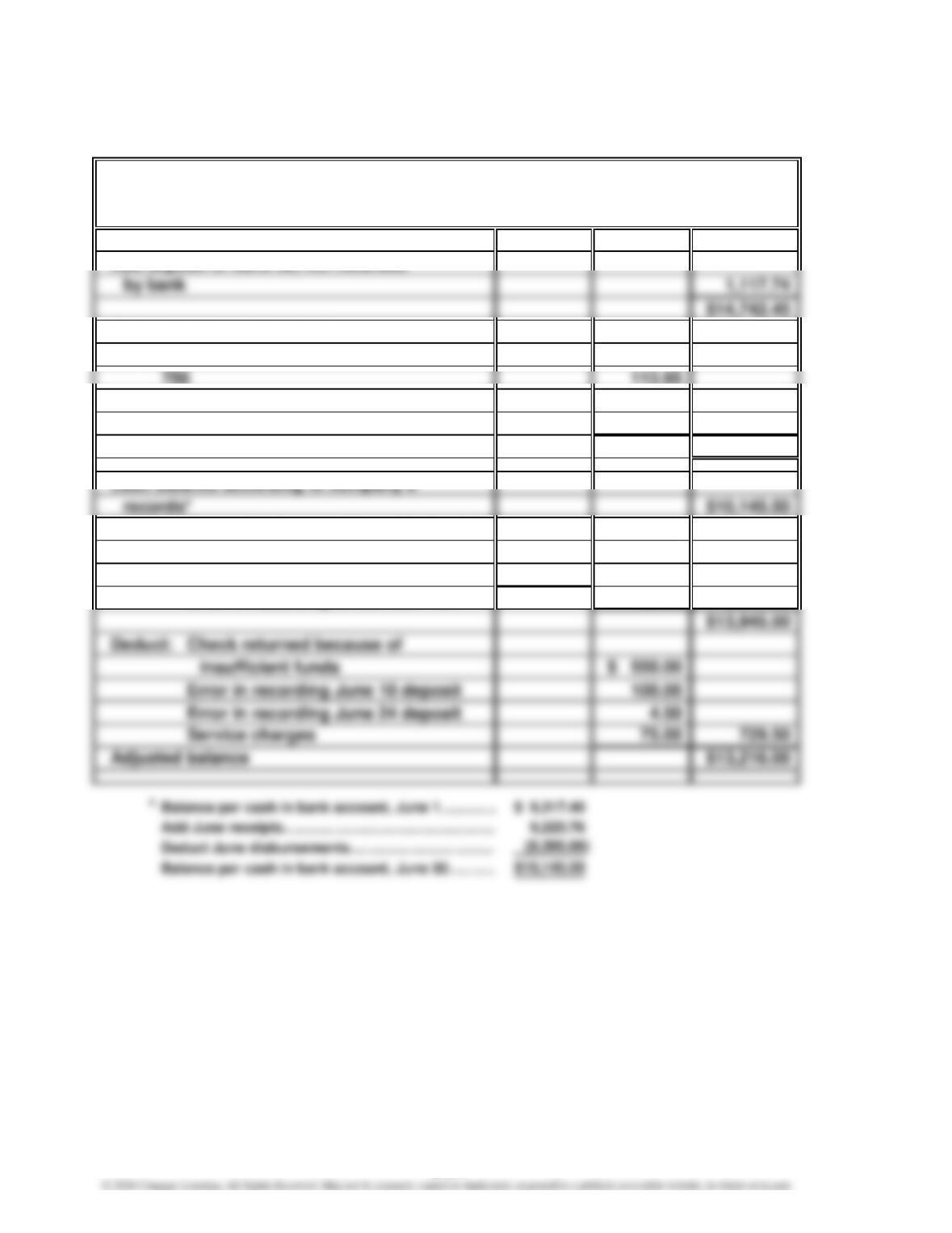

1.

Cash balance according to bank statement $13,624.71

Add deposit of June 30, not recorded

Deduct outstanding checks:

No. 738 $251.40

758 259.60

759 901.50 1,526.45

Adjusted balance $13,216.00

Add: Proceeds of note collected by bank:

Principal $3,500.00

Interest 210.00 $3,710.00

Error in recording Check No. 743 90.00 3,800.00

BEELER FURNITURE COMPANY

Bank Reconciliation

June 30, 2016

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

8-25

Prob. 8–5A (Concluded)

2.

2016

June 30 Cash 3,800.00

Notes Receivable

3,500.00

Interest Revenue

210.00

Accounts Payable

3.

4. The error of $540 ($930 – $390) in the canceled check should be added to the

$13,216.00

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

8-26

Prob. 8–1B

Weaknesses:

c. An independent person (for example, a supervisor) should count the cash in

each cashier’s cash register, unlock the record, and compare the amount of cash

with the amount on the record to determine cash shortages or overages.

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

8-27

Prob. 8–2B

1 Petty Cash 1,000

Cash 1,000

30 Store Supplies 375

Merchandise Inventory 215

2016

June

8-28

1.

Cash balance according to bank statement $33,650

Add deposit of July 31, not recorded by bank

9,150

$42,800

of $1,810 630 18,495

Adjusted balance $24,305

2.

2016

July 31 Cash 6,635

Notes Receivable

5,750

Interest Revenue

345

Accounts Payable—Holland Co.

3. $24,305; the adjusted balance from the bank reconciliation should be reported

STONE SYSTEMS

Bank Reconciliation

July 31, 2016

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

8-29

Prob. 8–4B

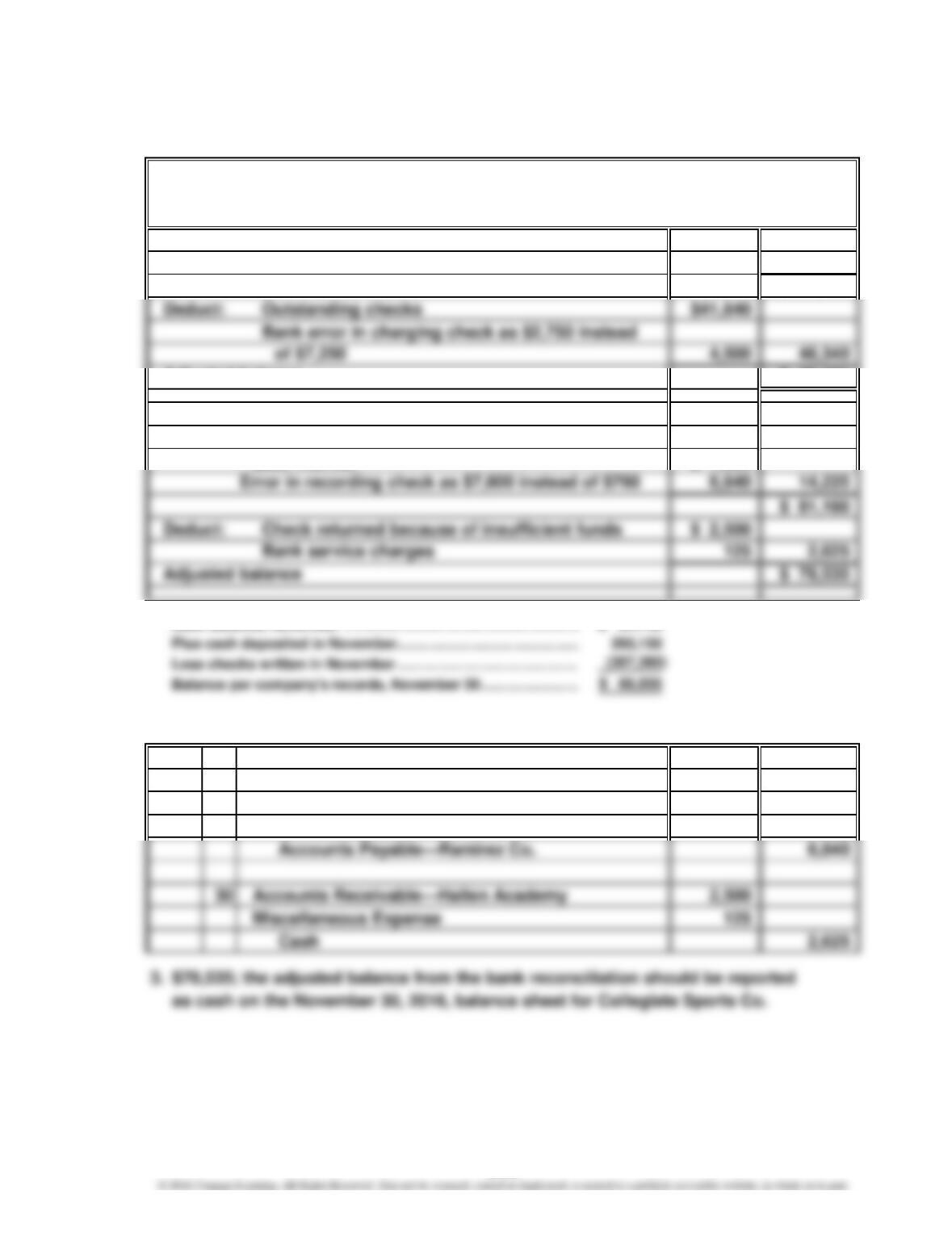

1.

Cash balance according to bank statement $112,675

Add deposit of November 30, not recorded by bank

12,200

$124,875

Deduct:

Adjusted balance $ 78,535

Cash balance according to company’s records* $ 66,935

Add:

Proceeds of note collected by bank, including

$385 interest $7,385

Deduct:

*

Cash balance, November 1……………………………………………

$81,145

Plus cash deposited in November…………………………………

Less checks written in November…………………………………

2.

2016

Nov. 30 Cash 14,225

Notes Receivable

7,000

Interest Revenue

385

COLLEGIATE SPORTS CO.

Bank Reconciliation

November 30, 2016

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

8-30

Prob. 8–5B

1.

Cash balance according to bank statement $11,601.41

Add deposit of July 31, not recorded by bank

1,177.87

$12,779.28

Deduct outstanding checks:

633 310.08 1,285.28

Adjusted balance $11,494.00

Cash balance according to company’s records*

$7,664.00

Add proceeds of note collected by bank:

Principal

$4,000.00

Interest

160.00

Add error in recording July 23 deposit

18.00

*

Balance per cash in bank account, July 1…………

$9,578.00

Add July receipts…………………………………………

6,465.42

Deduct July disbursements……………………………

Balance per cash in bank account, July 31…………

SUNSHINE INTERIORS

Bank Reconciliation

July 31, 2016

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

8-31

Prob. 8–5B (Concluded)

2.

2016

July 31 Cash 4,241.00

Interest Revenue

Sales

18.00

Accounts Payable

63.00

Cash

4. The error of $1,620 ($1,800 – $180) in the canceled check should be added to the

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

8-32

CP 8–1

Acceptable business and professional conduct requires Joel Kimmel to notify the

CP 8–2

Several control procedures could be implemented to prevent or detect the theft of

cash from fictitious returns.

One procedure would be to establish a policy of “no cash refunds.” That is, returns

could only be exchanged for other merchandise. However, such a policy might not

be popular with customers, and Turpin Meadows Electronics might lose sales from

customers who would shop at other stores with a more liberal return policy.

CP 8–3

Several possible procedures for preventing or detecting the theft of grocery items by

failing to scan their prices include the following:

a. Most scanning systems are designed so that an audible beep is heard each time

an item is rung up on the cash register. This is intended to alert the cashier that

the item has been properly rung up. Thus, observing whether a cashier is ringing

CASES & PROJECTS

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

CP 8–3 (Concluded)

c. Although this detection procedure would probably not be used in a grocery

store, it is used by Sam’s Clubs to detect this activity. Specifically, an employee

CP 8–4

Jo is clearly behaving in an unprofessional manner in intentionally shortchanging

her customers.

At this point, Doris is in a difficult position. She is apparently adhering to Fuller’s

Organic Markets’ policy of making up shortages out of her own pocket, but she is

obviously upset about it. If Doris accepts Jo’s advice, she will be engaging in

unprofessional behavior. Doris is also faced with the dilemma of whether she should

report Jo’s behavior. If Doris continues to work for Fuller’s Organic Markets, her

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

CP 8–5

1. There are several methods that could be used to determine how much the

cashier has stolen. The method described below is based on preparing a

Balance according to bank statement $10,575

Add undeposited cash receipts on hand 1,500

2670

3679

3690

225

750

800 5,150

Adjusted balance $ 6,925

Note to Instructors: The amount stolen by the cashier could also be computed directly

from the cashier-prepared bank reconciliation as follows:

Outstanding checks omitted from the bank

reconciliation prepared by the cashier:

No.

2670………………………………………………………

$1,050

3679………………………………………………………

3690………………………………………………………

Unrecorded note plus interest incorrectly recorded on

the bank reconciliation prepared by the cashier……………

2,400

Addition error in the total of the outstanding checks in

the bank reconciliation prepared by the cashier*……………

5151

PARKER COMPANY

Bank Reconciliation

July 31, 2016

5148

5149

8-35

CP 8–5 (Concluded)

2. The cashier attempted to conceal the theft by preparing an incorrect bank

reconciliation. Specifically, the cashier (1) omitted outstanding checks on

3. a. Two major weaknesses in internal controls that allowed the cashier to

steal the undeposited cash receipts are as follows:

●First, large amounts of undeposited cash receipts were kept on hand

during the month. For example, cash receipts for July 30 and 31 had

yet to be deposited as of July 31. The large amount of undeposited

b. Two recommendations that would improve internal controls so that similar

types of thefts of undeposited cash receipts could be prevented are as

follows:

●All cash receipts should be deposited daily. This would reduce the

risk of significant cash losses. In addition, any missing cash would be

more easily detected.

CHAPTER 8 Sarbanes-Oxley, Internal Control, and Cash

CP 8–6

Note to Instructors: The purpose of this activity is to familiarize students with the

internal controls used by specific businesses. For example, when you order food

at a McDonald’s drive-through lane, your order is processed as follows:

2. The order is simultaneously shown on a computer screen in the food

preparation area.

4. You drive farther to where your order is delivered by an employee other than

the cashier.

CP 8–7

1. Year 3: $497.8 per month ($5,974 ÷ 12)

2. Year 3: 5.6 months ($2,807 ÷ $497.8)

3. At the end of Year 1, TearLab had less than a month (0.3) of cash remaining.

During Year 2, the monthly cash expenses increased from $341.5 to $378.3. At the

end of Year 2, less than eight months (7.2) of cash remained. In Year 3, TearLab