Chapter 08—Inventories and the Cost of Goods Sold

Financial and Managerial Accounting, 18e 8-1

8 INVENTORIES AND THE COST OF GOODS SOLD

Chapter Summary

The chapter is a detailed introduction to the cost flow assumptions used to value

inventories and measure the cost of goods sold.

Application of specific identification, average cost, FIFO and LIFO is first examined

within the context of a perpetual inventory system. The impact of the cost flow assumption

employed on income taxes is discussed in detail. The need for a physical inventory to assess

inventory shrinkage is also reviewed as are the accounting procedures necessary to record

inventory shrinkage. A brief presentation of lower-of-cost-or-market write-downs concludes the

discussion of perpetual systems.

Application of the cost flow assumptions within a periodic system is next explained. We

also demonstrate that restatement of ending inventory by the periodic method results in the

maximum tax advantage from the LIFO flow assumption.

The chapter covers a number of additional issues surrounding inventory accounting.

These include: the financial statement effects of inventory errors; the retail and gross profit

methods for estimating ending inventory; and, an analysis of the inventory turnover ratio.

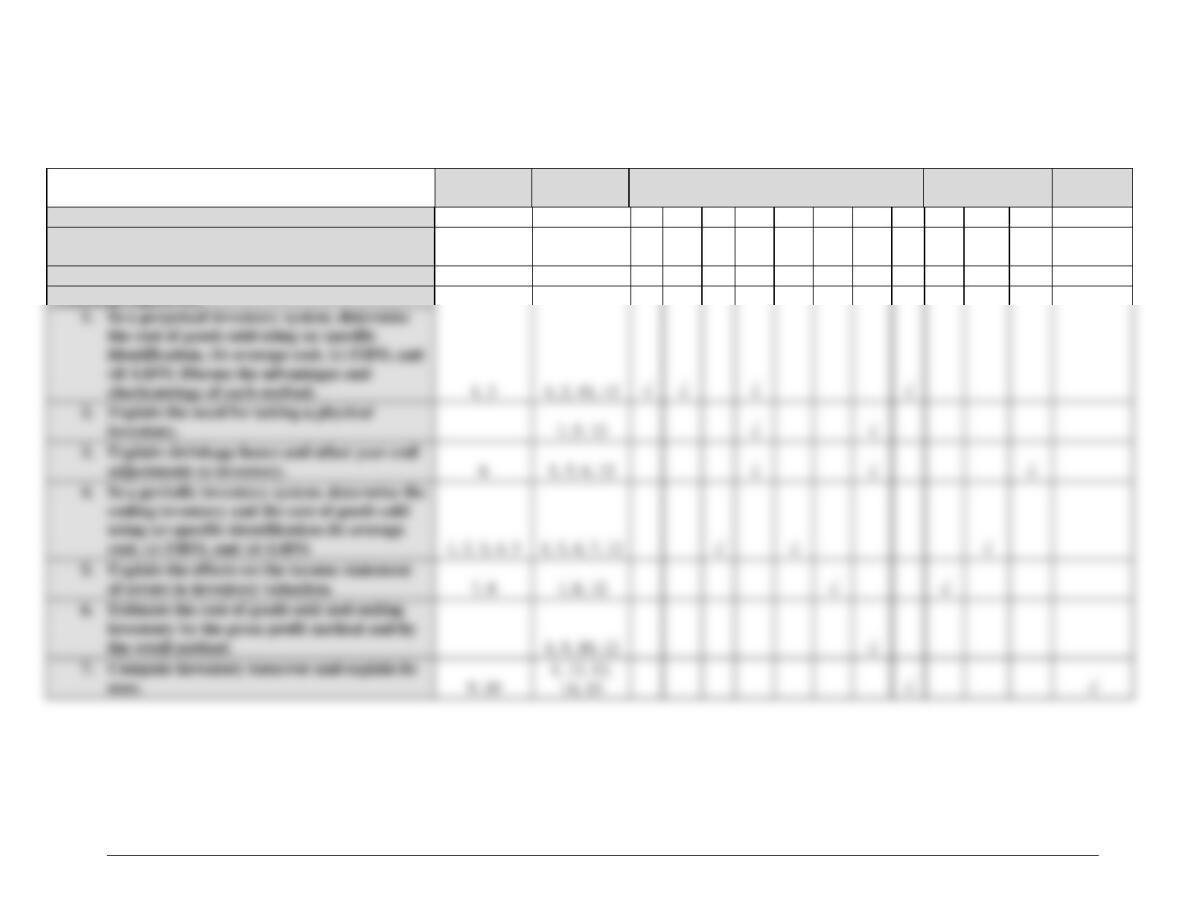

Learning Objectives

1. In a perpetual inventory system, determine the cost of goods sold using (a) specific

identification, (b) average cost, (c) FIFO, and (d) LIFO. Discuss the advantages and

shortcomings of each method.

2. Explain the need for taking a physical inventory.

3. Record shrinkage losses and other year-end adjustments to inventory.

4. In a periodic inventory system, determine the ending inventory and the cost of goods sold

using (a) specific identification, (b) average cost, (c) FIFO, and (d) LIFO.

5. Explain the effects on the income statement of errors in inventory valuation.

6. Estimate the cost of goods sold and ending inventory by the gross profit method and by the

retail method.

7. Compute inventory turnover and explain its uses.

Chapter 08—Inventories and the Cost of Goods Sold

8-2 Instructor’s Resource Manual

Brief Topical Outline

A. Inventory defined

B. The flow of inventory costs

1. Which unit did we sell?

2. Data for an illustration

3. Specific identification

4. Cost flow assumptions

5. Average-cost method

6. First-in, first-out method

7. Last-in, first-out method

8. Evaluation of the methods

a. Specific identification

b. Average cost

c. First-in, first-out

d. Last-in, first-out

9. Do inventory methods really affect performance?

10. The principle of consistency

11. Just-in–time (JIT) inventory system—see Case in Point (page 354)

C. Taking a physical inventory—see Pathways Connection (page 364) and Your Turn

(page 365)

1. Recording shrinkage losses

2. LCM and other write-downs of inventory

a. The lower-of-cost-or-market (LCM) rule

3. The year-end cutoff of transactions

a. Matching revenue and the cost of goods sold

b. Goods in transit—see Your Turn (page 357)

4. Periodic inventory systems

a. Applying flow assumptions in a periodic system

b. Specific identification

c. Average cost

d. FIFO

e. LIFO—see International Case in Point (page 359)

f. Receiving the maximum tax benefit from the LIFO method

g. Pricing the year-end inventory by computer

5. International financial reporting standards

6. Importance of an accurate valuation of inventory—see Ethics, Fraud, &

Corporate Governance (page 365)

a. Effects of an error in valuing ending inventory

b. Inventory errors affect two years

c. Effects of errors in inventory valuation: a summary

7. Techniques for estimating the cost of goods sold and the ending inventory

8. The gross profit method

9. The retail method

10. “Textbook” inventory systems can be modified . . . and they often are

D. Concluding remarks

Chapter 08—Inventories and the Cost of Goods Sold

Financial and Managerial Accounting, 18e 8-3

Topical Coverage and Suggested Assignments

Class

Meetings on

Chapter

Topical

Outline

Coverage

Discussion

Questions*

Brief

Exercises*

Exercises*

Problems*

Critical

Thinking

Cases*

1

A

1, 2, 3

1, 3

2, 3

2, 3

1

2

B

5, 7, 9, 10

5, 7

7, 9, 10

5, 6, 7

3

C – D

15

10

12, 13, 14

3

*Homework assignment (to be completed prior to class)

Comments and Observations

Teaching Objectives for Chapter 8

Our specific teaching objectives in this chapter are to:

1. Explain why it is necessary for a company with an inventory to either use specific

identification or adopt a “flow assumption.”

2. Illustrate the “flow of costs” into the cost of goods sold account using each costing method

(specific identification, average cost, FIFO, and LIFO).

3. Discuss the factors to be considered in the selection of an appropriate cost method.

4. Illustrate the recording of shrinkage losses and other year-end adjustments to inventory

(excepting that in objective 6, below).

5. Illustrate the valuation of ending inventory using periodic costing procedures.

6. Explain why companies using perpetual LIFO might adjust the valuation of inventory at

year-end to the amount indicated by periodic LIFO costing procedures.

7. Illustrate the gross profit and retail methods of estimating the cost of goods sold and ending

inventory.

8. Discuss the purpose of computing a company’s inventory turnover rate.

General Comments

As in the previous edition, we emphasize the perpetual inventory system primarily

because this is the method now in predominant use. Teaching with an emphasis on perpetual

inventory systems has a number of benefits in the classroom.

Of greatest importance, a perpetual system shifts the focal point of cost assignment from

ending inventory to the cost of goods sold. As a result, the names of the flow assumptions finally

“mean what they say.” For example, “first-in, first-out” means that the first costs are used in the

Chapter 08—Inventories and the Cost of Goods Sold

8-4 Instructor’s Resource Manual

cost assignment process; “last-in, first-out” means that the last costs are used. Under a periodic

system, the reverse is true.

Not only do students more quickly grasp the concepts underlying the flow assumptions

when we assume a perpetual inventory system, but they also quickly grasp the effects of using

different assumptions during a period of rising prices. This enables us to emphasize the effects of

different methods upon earnings, income tax considerations, and even the implications of LIFO

reserves.

We use Exercise 2 to illustrate the basic cost-flow assumptions and follow it with a

discussion of Exercise 11 to demonstrate the effects of using alternative methods. Exercise 12

presents a more challenging analysis of the same points. We also discuss in class such topics as

“just-in–time” systems, inventory shrinkage, and the factors management should consider in

determining the optimal size of a company’s inventory. These discussions portray inventory as

physical goods moving in and out of the business, rather than merely as a dollar amount. We find

that these discussions contribute to students’ interest and also to their understanding of the

importance of inventories to accountants, managers, and investors.

Supplemental Exercises

Group Exercise

In the mid-2000s, two former executive leaders of the Bristol-Myers Squibb Company

were criminally charged in a case of financial reporting fraud that centered around inventory

manipulations. Research this case and report your findings. How did the managers perpetrate the

fraud? How were both internal and external stakeholders impacted?

Internet Exercise

Visit Walmart’s website and access their most recent annual report. Locate the summary

of significant accounting policies and find the inventory method(s) used by Walmart.

Chapter 08—Inventories and the Cost of Goods Sold

Financial and Managerial Accounting, 18e 8-5

CHAPTER 8 NAME #

10-MINUTE QUIZ A SECTION

Indicate the best answer for each question in the space provided.

1. The primary purpose of an inventory flow assumption is to:

a Increase inventory turnover.

b Increase gross profit.

c Determine which unit costs are assigned to inventory and which are assigned to the cost of

goods sold.

d Minimize taxable income during periods of rising prices.

2. During a period of steadily rising prices, which of the following inventory valuation methods is

likely to result in the lowest cost of goods sold?

a LIFO.

b FIFO.

c The retail method.

d The gross profit method.

3. The primary reason for the popularity of the LIFO flow assumption is that this method:

a Is most appropriate when each item in inventory is unique.

b Tends to minimize taxable income.

c Causes inventory to be reported at or near its current replacement cost.

d Reduces the amount of money “tied up” in inventory.

4. In a periodic inventory system, the cost of goods sold is determined by:

a Multiplying net sales for the period by a cost ratio.

b Journal entries made at the time of each sales transaction.

c Physically counting the quantities of merchandise sold each day, and determining the cost of

these items at year-end.

d Subtracting the cost assigned to the ending inventory from the cost of goods available for sale

during the period.

5. Salerno Co. has an inventory turnover rate of 7 and an accounts receivable turnover rate of 5.

Assuming 365 days in a year, the period of time required for Salerno to convert its inventory into

cash through normal business operations is approximately:

a 21 days.

b 52 days.

c 4 months.

d 2.5 months.

Chapter 08—Inventories and the Cost of Goods Sold

8-6 Instructor’s Resource Manual

CHAPTER 8 NAME #

10-MINUTE QUIZ B SECTION

Ace Systems, Inc. uses a perpetual inventory system. The company’s beginning inventory of a particular

product and its purchases during the month of January were as follows:

Quantity Unit Cost Total Cost

Beginning inventory (Jan. 1) ………………………… 10 $27.50 $275

Purchase (Jan. 15) ……………………………………….. 15 $28.00 $420

Purchase (Jan. 23) ……………………………………….. _5 $29.00 $145

Total ……………………………………………………… 30 $840

On January 28, Ace Systems sells 18 units of this product. The other 12 units remain in inventory at

January 31.

1. Refer to above data. Assuming that Ace Systems uses the average cost flow assumption, the cost

of goods sold to be recorded at January 28 is:

a $504.

b $336.

c $499.

d Some other amount.

2. Refer to above data. Assuming that Ace Systems uses the LIFO flow assumption, the cost of goods

sold on January 28 is:

a $331.

b $509.

c $499.

d Some other amount.

3. Refer to above data. Assuming that Ace Systems uses the FIFO flow assumption, the cost of goods

sold on January 28 is:

a $509.

b $341.

c $499.

d Some other amount.

4. Refer to above data. Assuming that Ace Systems uses the LIFO flow assumption, the 12 units of this

product in inventory at January 31 have a total cost of:

a $499.

b $331.

c $509.

d Some other amount.

5. Refer to above data. Assuming that Ace Systems uses the FIFO flow assumption, the 12 units of this

product in inventory at January 31 have a total cost of:

a $341

b $509.

c $499.

d Some other amount.

Chapter 08—Inventories and the Cost of Goods Sold

Financial and Managerial Accounting, 18e 8-7

CHAPTER 8 NAME #

10-MINUTE QUIZ C SECTION

Canfield uses a perpetual inventory system. The company’s beginning inventory of a particular product

and its purchases during the month of January were as follows:

Quantity Unit Cost Total Cost

Beginning inventory (Jan. 1) ………………………………………….. 50 $6 $300

Purchase (Jan. 10) …………………………………………………………. 25 $7 $175

Purchase (Jan. 22) …………………………………………………………. 25 $8 $200

Total ………………………………………………………………….. 100 _$675

On January 25, Canfield sells 55 units of this product. The other 45 units remain in inventory at January

31.

a Determine the cost of goods sold using each of the following flow assumptions:

(1) LIFO $_____________

(2) FIFO $_____________

(3) Average cost $_____________

b Determine the cost of the 45 units in inventory at January 31 using each of the following flow

assumptions:

(1) LIFO $_____________

(2) FIFO $_____________

(3) Average cost $_____________

Chapter 08—Inventories and the Cost of Goods Sold

8-8 Instructor’s Resource Manual

CHAPTER 8 NAME #

10-MINUTE QUIZ D SECTION

Sherman Electric uses a periodic inventory system. The beginning inventory of a particular product, and

the purchases during the current year, were as follows:

Jan. 1 Beginning inventory ………………………… 60 units @ $105 = $ 6,300

Mar. 8 Purchase …………………………………………. 30 units @ $115 = 3,450

Aug. 11 Purchase …………………………………………. 90 units @ $125 = 11,250

Oct. 23 Purchase ………………………………………… _20 units @ $135 = _2,700

Total available for sale……………………………………… 200 units $23,700

At December 31, the ending inventory of this product consisted of 65 units.

Using periodic costing procedures, determine (1) cost of the year-end inventory and, (2) cost of goods

sold relating to this product under each of the following flow assumptions:

(1) Inventory at Dec. 31 (2) Cost of Goods Sold

a Average cost $_______________ $_______________

b First-in, first–out $_______________ $_______________

c Last-in, first-out $_______________ $_______________

Chapter 08—Inventories and the Cost of Goods Sold

Financial and Managerial Accounting, 18e 8-9

SOLUTIONS TO CHAPTER 8 10–MINUTE QUIZZES

QUIZ A

1 C

QUIZ B

QUIZ C

a Cost of goods sold

Learning Objective: 1

QUIZ D

Chapter 08—Inventories and the Cost of Goods Sold

8-10 Instructor’s Resource Manual

Assignment Guide to Chapter 8

Brief

Exercises

Exercises

Problems

Cases

Net

Item Number

1 – 10

1-15

1

2

3

4

5

6

7

8

1

2

3

4

Time estimate (in minutes)

< 10

15

3

5

30

20

20

25

20

25

20

30

20

15

n/a

Difficulty rating

E

E

M

S

M

M

S

M

M

S

S

M

M

S

Learning Objectives:

1, 2

1, 2, 11, 12