Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-1

CHAPTER 8

Variable Costing and the Costs of Quality and

Sustainability

ANSWERS TO REVIEW QUESTIONS

8-1 Under absorption costing, fixed manufacturing-overhead costs are assigned to units

8-2 Timing is the key in distinguishing between absorption and variable costing. All

manufacturing costs will ultimately be expensed under either absorption costing or

8-3 The term direct costing is a misnomer. Variable costing is a better term for this

product-costing method. Under variable costing, the variable costs of direct material,

8-4 When inventory increases, the income reported under absorption costing will be

greater than the income reported under variable costing. This difference results from

8-5 Many managers prefer variable costing over absorption costing because income

statements prepared under variable costing more closely reflect operations. For

8-2

8-6 Some managerial accountants believe that absorption costing may provide an

8-7 Variable and absorption costing will not result in significantly different income

measures in a JIT setting. Under JIT inventory and production management,

8-8 Many managers prefer absorption-costing data for cost-based pricing decisions.

They argue that fixed manufacturing overhead is a necessary cost of production. To

8-9 Proponents of variable costing argue that a product’s variable cost provides a better

8-10 Variable costing is consistent with cost-volume-profit analysis because it properly

reflects the cost behavior of variable and fixed costs. Only variable manufacturing

8-11 An asset is a thing of value owned by the organization with future service potential.

By accounting convention, assets are valued at their cost. Since fixed costs

comprise part of the cost of production, advocates of absorption costing argue that

inventory (an asset) should be valued at its full (absorption) cost of production.

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-3

8-12 Four types of product quality costs are as follows:

8-13 Observable quality costs can be measured and reported, often on the basis of

information in the accounting records. For example, the cost of inspectors’ salaries

8-14 A product’s quality of design is how well it is conceived or designed for its intended

8-15 A product’s grade is the extent of its capability in performing its intended purpose,

viewed in relation to other products with the same functional use. An example in the

8-16 “An ounce of prevention is worth a pound of cure” can be interpreted in terms of

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-4

8-18 Private environmental costs are environmental costs borne by a company or

individual.

Social environmental costs are environmental costs borne by the public at large.

8-19 End–of-pipe strategies: Under this approach, a company produces a pollutant and

cleans it up before discharging it into the environment.

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-5

SOLUTIONS TO EXERCISES

EXERCISE 8-20 (15 MINUTES)

1. a. Inventory decreases by 3,000 units, so operating income is greater under variable

2. a. Inventory remains unchanged, so there is no difference in reported income under

3. a. Inventory increases by 1,200 units, so operating income is greater under

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-6

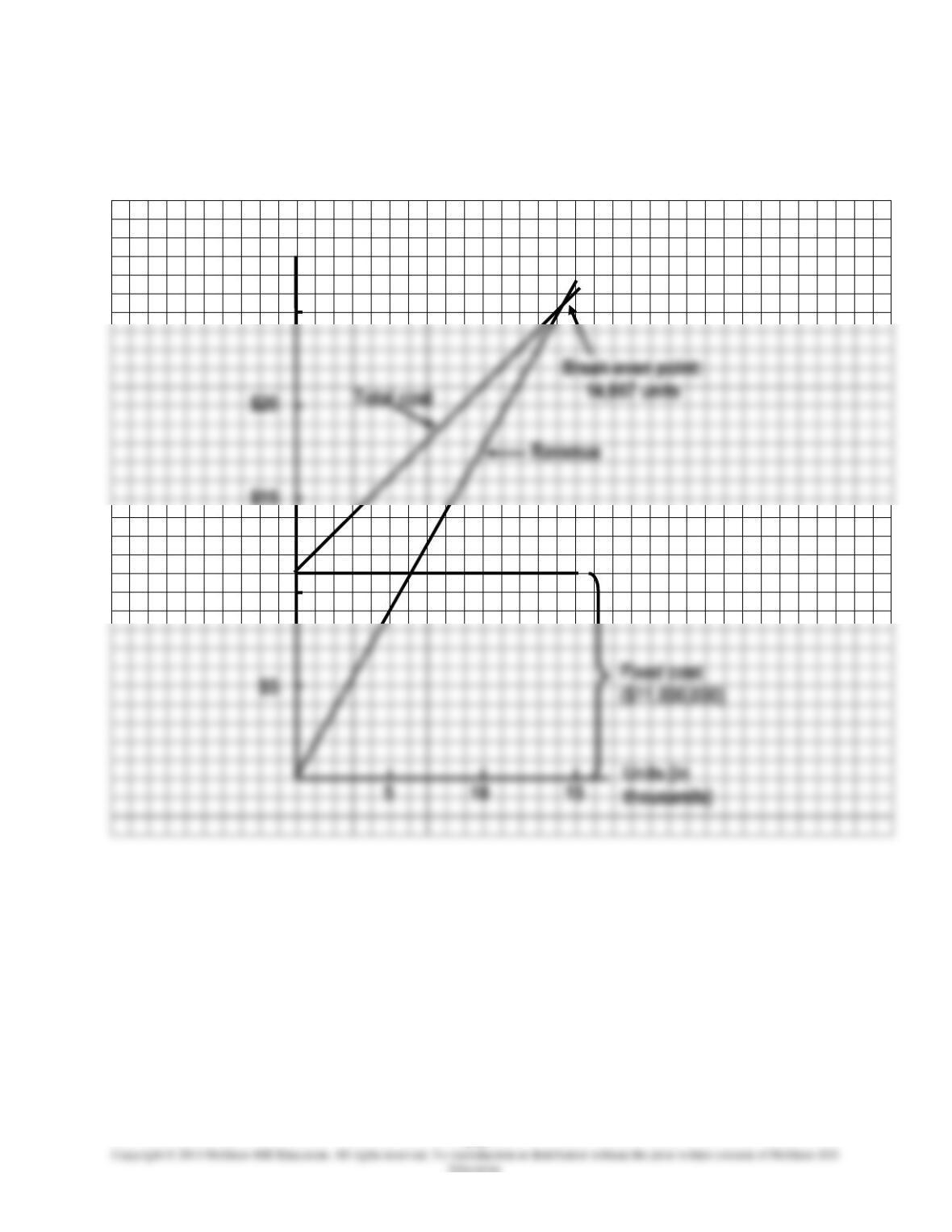

EXERCISE 8-21 (20 MINUTES)

1. Cost-volume profit graph:

Dollars (in millions)

$25

$10

•

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-7

EXERCISE 8-21 (CONTINUED)

2. Calculation of break-even point:

Break-even point

=

margin oncontributi unit

cost fixed

14,667 units (rounded)

3. Variable costing is more compatible with the cost-volume-profit chart, because it

maintains the distinction between fixed and variable costs as does CVP analysis.

EXERCISE 8-22 (15 MINUTES)

Inventory calculations (units):

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-8

EXERCISE 8-22 (CONTINUED)

1.

Variable costing:

Inventoriable costs under variable costing:

Direct material used …………………………………………………………………….

$300,000

Direct labor incurred ……………………………………………………………………

Variable manufacturing overhead ………………………………………………..

Total …………………………………………………………………………………………..

$550,000

Cost per unit produced = $550,000/20,000 units = $27.50 per unit

$ 27,500

2. Absorption costing:

Predetermined fixed-overhead rate

=

production planned

overhead ingmanufactur fixed

=

units 000,20

000,210$

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-9

EXERCISE 8-23 (15 MINUTES)

1. a. Inventory increases by 3,000 units, so operating income is greater under

2. a. Inventory decreases by 5,000 units, so operating income is greater under variable

3. a. Inventory remains unchanged, so there is no difference in reported income under

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-10

EXERCISE 8-24 (10 MINUTES)

1.

Inventoriable costs under absorption costing:

Direct material used …………………………………………………………………….

$272,000

Direct labor …………………………………………………………………………………

Variable manufacturing overhead ………………………………………………..

Fixed manufacturing overhead …………………………………………………….

Total …………………………………………………………………………………………..

$560,000

2.

Inventoriable costs under variable costing:

Direct material used …………………………………………………………………….

$272,000

Direct labor …………………………………………………………………………………

Variable manufacturing overhead ………………………………………………..

Total …………………………………………………………………………………………..

$460,000

EXERCISE 8-25 (30 MINUTES)

The specifics of the answer will vary, depending on the company and product selected.

However, the relative merits of absorption and variable costing as the basis for pricing

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-11

EXERCISE 8-26 (25 MINUTES)

Inventory calculations (units):

Finished-goods inventory, January 1 ……………………………………………

Add: Units produced …………………………………………………………………..

Less: Units sold ………………………………………………………………………….

Finished-goods inventory, December 31 ………………………………………

1.

Variable costing:

Inventoriable costs under variable costing:

Direct material used …………………………………………………………………….

$ 80,000

Variable manufacturing overhead ………………………………………………..

Total …………………………………………………………………………………………..

$144,000

Cost per unit produced = $144,000/10,000 units = $14.40 per unit

$ 14,400

2. Absorption costing:

Predetermined fixed-overhead rate

=

production planned

overhead ingmanufactur fixed

=

units 000,10

000,50$

= $5.00 per unit

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-12

Since units of inventory increased during the year, operating income reported under

absorption costing will be $5,000 higher than that reported under variable costing.

EXERCISE 8-27 (10 MINUTES)

1.

Inventoriable costs under variable costing:

Direct material used …………………………………………………………………….

$203,000

Direct labor …………………………………………………………………………………

Variable manufacturing overhead ………………………………………………..

Total …………………………………………………………………………………………..

$308,000

2.

Inventoriable costs under absorption costing:

Direct material used …………………………………………………………………….

$203,000

Direct labor …………………………………………………………………………………

Variable manufacturing overhead ………………………………………………..

Fixed manufacturing overhead …………………………………………………….

Total …………………………………………………………………………………………..

$364,000

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-13

EXERCISE 8-28 (10 MINUTES)

Observable quality costs in the airline industry:

• Cost of repairing damaged luggage.

• Cost of providing lodging for passengers stranded when a flight is cancelled due to

• Cost of cleaning a passenger’s clothing when a flight attendant spills food or

Hidden quality costs in the airline industry:

• Cost of lost flight bookings when passengers judge in-flight service to be

substandard.

• Cost of lost flight bookings when potential passengers are unable to get through to

• Cost of lost flight bookings when passengers react to cancelled or late flights.

EXERCISE 8-29 (5 MINUTES)

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-14

EXERCISE 8-30 (20 MINUTES)

CERRITOS CIRCUITRY

QUALITY-COST REPORT

Costs

For

May

Percentage

of

Total

Prevention costs:

Training of quality-control inspectors …………………………………

$ 31,500

__22.2

Total ……………………………………………………………………………

$ 31,500

__22.2

Appraisal costs:

Tests of instruments ………………………………………………………….

Inspection of purchased electrical components ………………….

18,000

Total ……………………………………………………………………………

$ 63,000

__44.4

Internal failure costs:

Costs of rework …………………………………………………………………

$ 13,500

Costs of defective parts that cannot be salvaged ………………..

9,150

___6.5

Total ……………………………………………………………………………

$ 22,650

__16.0

External failure costs:

Replacement of instruments already sold …………………………..

$ 24,750

__17.4

Total ……………………………………………………………………………

$ 24,750

__17.4

EXERCISE 8-31 (45 MINUTES)

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-15

SOLUTIONS TO PROBLEMS

PROBLEM 8-32 (45 MINUTES)

1. a. Absorption-costing operating income statements:

Year 1

Year 2

Year 3

Sales revenue (at $25 per case) …………………………..

$2,000,000

$1,500,000

$2,250,000

Gross margin ……………………………………………………….

Less: Selling and administrative expenses:

Variable (at $ .50 per case) …………………………..

Fixed ……………………………………………………….

Operating income ……………………………………………………….

Less: Cost of goods sold (at

*The absorption cost per case is $21, calculated as follows:

production Planned

overheadingmanufactur fixed Budgeted

+

case per cost

ingmanufactur variable

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-16

PROBLEM 8-32 (CONTINUED)

b. Variable-costing operating income statements:

Year 1

Year 2

Year 3

Sales revenue (at $25 per case) ……………………………………………………

$2,000,000

$1,500,000

$2,250,000

Less: Variable expenses:

Variable selling and administrative

Contribution margin ……………………………………………………….

$ 680,000

$ 510,000

$ 765,000

Less: Fixed expenses:

Fixed manufacturing overhead …………………………..

Fixed selling and administrative

Operating income ……………………………………………………….

Variable manufacturing costs (at

2. Reconciliation:

Year

Reported Operating

Income

Difference

in

Reported

Operating

Income

Change in

Inventory

(in units)

Predetermined

Fixed

Overhead

Rate*

Difference In

Fixed Overhead

Expensed Under

Absorption and

Variable Costing

Absorption

Costing

Variable

Costing

1

$242,500

$242,500

-0-

-0-

$5

0

2

$100,000

20,000

3

PROBLEM 8-32 (CONTINUED)

3. a. In year 4, the difference in reported operating income will be $50,000, calculated

as follows:

Change in

inventory

(in units)

Predetermined

fixed overhead

rate

b. Over the four-year period, the total of all reported operating income will be the

same under absorption and variable costing. This result will occur because

8-18

PROBLEM 8-33 (45 MINUTES)

1. Sales during the year were:

Beginning inventory ……………………………………………………………………

0

units

Production ………………………………………………………………………………….

units

Ending inventory ………………………………………………………………………..

) units

Sales ………………………………………………………………………………………….

units

Since inventory increased during the year, reported operating income is higher

under absorption costing.

Difference in

reported

operating income

=

inventory

in change

unit per

overhead fixed

Reported operating income under variable costing ………………………

Fixed overhead …………………………………………………………………………..

Total contribution margin ……………………………………………………………

8-19

PROBLEM 8-33 (CONTINUED)

Contribution margin

per unit

=

units in sales

margin oncontributi total

=

=

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-20

PROBLEM 8-33 (CONTINUED)

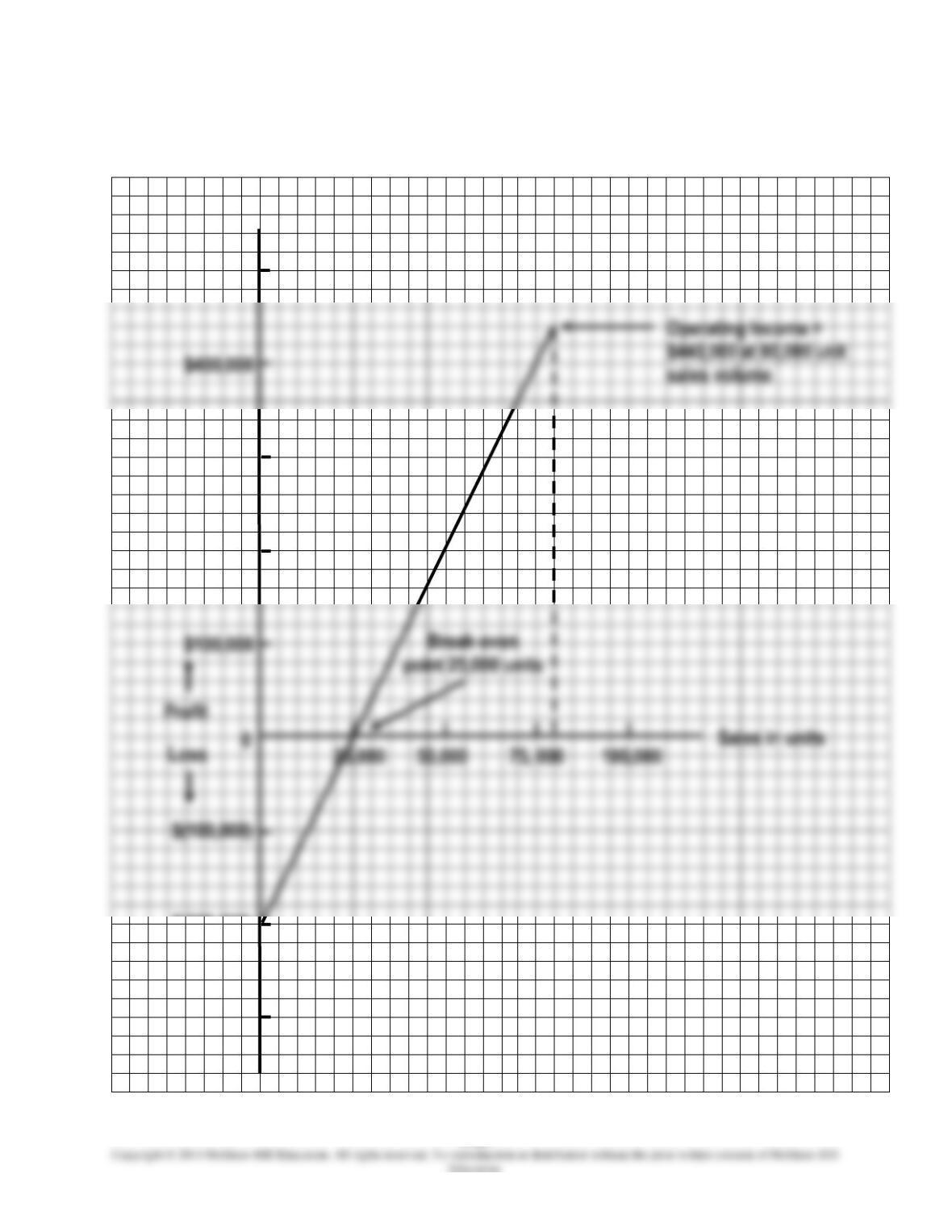

2. Profit-volume graph:

$(100,000)

Dollars

$500,000

$300,000

$200,000

$(200,000)

$(300,000)