Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

EXERCISE 8-10

The outstanding checks are as follows:

No.

Amount

255

$ 620

EXERCISE 8-11

(a) CRANE VIDEO COMPANY

Bank Reconciliation

July 31

Cash balance per bank statement .................................... $7,263

Add: Deposits in transit .................................................. 1,300

8,563

8,000

Less: Bank service charge ............................................... 28

(b) July 31 Cash ................................................................... 716

EXERCISE 8-12

(a) MINTON COMPANY

Bank Reconciliation

September 30

Cash balance per bank statement .......................... $16,422

Add: Deposits in transit ......................................... 5,450

21,872

Adjusted cash balance per books .......................... $19,489

(b) Sept. 30 Cash ....................................................... 2,530

Notes Receivable ........................... 2,500

Interest Revenue ............................ 30

EXERCISE 8-13

(a) Deposits in transit:

Deposits per books in July ..................................... $15,750

EXERCISE 8-13 (Continued)

(b) Outstanding checks:

Checks per books in July ............................... $17,200

(c) Deposits in transit:

Deposits per bank statement in

September .................................................... $26,700

(d) Outstanding checks:

Checks clearing bank in September .............. $25,000

Add: Outstanding checks, September 30 ... 2,100

EXERCISE 8-14

(a) Cash and cash equivalents should be reported at $88,500.

Cash in bank .................................................... $42,000

Cash on hand .................................................. 12,000

(b) “Cash in plant expansion fund” should be reported as part of long-term

investments (a noncurrent asset). “Receivables from customers” should be

SOLUTIONS TO PROBLEMS

PROBLEM 8-1A

Principles

Application to Cash Disbursements

Establishment of responsibility.

Only the treasurer and assistant treasurer are

authorized to sign checks.

Documentation procedures.

Checks are prenumbered. Following payment,

invoices are stamped PAID.

Physical controls.

Blank checks are kept in a safe in the treasurer’s

office. Only the treasurer and assistant treasurer

have access to the safe. Checks are imprinted by

a machine in indelible ink.

PROBLEM 8-2A

(a) July 1 Petty Cash .............................................. 200.00

Cash ................................................ 200.00

15 Freight-Out ............................................. 92.00

Postage Expense ................................... 42.40

Entertainment Expense ......................... 46.60

Miscellaneous Expense ......................... 11.20

Cash Over and Short ............................. 3.80

Cash ................................................ 196.00

Aug. 15 Freight-Out ............................................. 77.60

Entertainment Expense ......................... 43.00

Postage Expense ................................... 33.00

Miscellaneous Expense ......................... 37.00

Cash Over and Short ...................... 3.60

Cash ................................................ 187.00

(b)

Petty Cash

Date

Explanation

Ref.

Debit

Credit

Balance

July 1

Aug. 16

CP

CP

200

100

200

300

PROBLEM 8-2A (Continued)

(c) The internal control features of a petty cash fund include:

(1) A custodian is responsible for the fund.

PROBLEM 8-3A

(a) REBER COMPANY

Bank Reconciliation

May 31, 2017

Cash balance per bank statement ................... $6,404.60

Add: Deposit in transit ................................... $2,416.15

Bank error—Stiner check ...................... 800.00 3,216.15

9,620.75

Less: Outstanding checks .............................. 576.25

Adjusted cash balance per bank ..................... $9,044.50

(b) May 31 Cash .............................................................. 3,060

Miscellaneous Expense ............................... 20

Notes Receivable ................................. 3,000

Interest Revenue .................................. 80

31 Accounts Receivable—Sue Allison ............ 680

Cash ...................................................... 680

31 Sales Revenue ............................................. 50

Cash ...................................................... 50

PROBLEM 8-4A

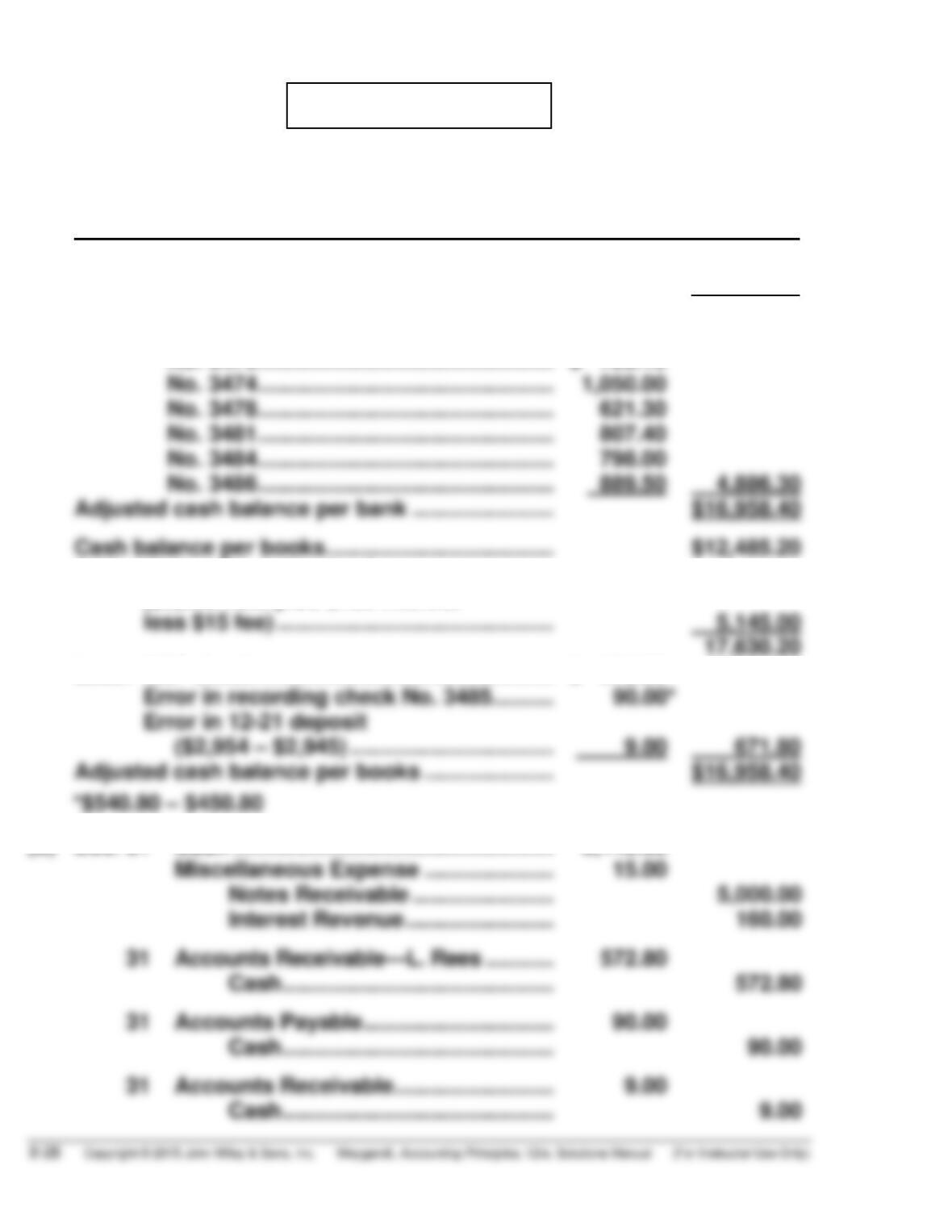

(a) LANGER COMPANY

Bank Reconciliation

December 31, 2017

Cash balance per bank statement ..................... $20,154.30

Add: Deposits in transit ................................... 1,690.40

21,844.70

Less: Outstanding checks

No. 3470 ................................................ $ 720.10

No. 3474 ................................................ 1,050.00

Cash balance per books ..................................... $12,485.20

Add: Note collected by bank

($5,000 note plus $160 interest

Less: NSF check ................................................ $ 572.80

Error in recording check No. 3485 .......... 90.00*

Error in 12-21 deposit

(b) Dec. 31 Cash .................................................... 5,145.00

Miscellaneous Expense ..................... 15.00

31 Accounts Receivable—L. Rees ........... 572.80

Cash ............................................ 572.80

PROBLEM 8-5A

(a) RODRIGUEZ COMPANY

Bank Reconciliation

July 31, 2017

Cash balance per bank statement .......................... $24,514

Add: Deposits in transit (1) ................................... 10,400

34,914

Less: Outstanding checks (2) ................................ $ 8,460

Bank error ($255 – $155) .............................. 100 8,560

Adjusted cash balance per bank ............................ $26,354

(1) July receipts per books ....................... $81,400

July deposits per bank ........................ $79,000

Less: Deposits in transit,

(2) Disbursements per books

in July................................................ $77,150

Less: Book error ................................. 90

Total disbursements to

PROBLEM 8-5A (Continued)

(b) July 31 Cash ............................................................... 4,470

Notes Receivable ................................... 4,400

Interest Revenue ................................... 70

PROBLEM 8-6A

Matt has created a situation that leaves many opportunities for undetected

theft. Here is a list of some of the deficiencies in internal control. You may

find others.

1. Documentation procedures. The tickets were unnumbered. By numbering

the tickets, the students could have been held more accountable for the

tickets. See number 3 below.

2. Physical controls and establishment of responsibility. The tickets were left

in an unlocked box on his desk. Instead, Matt should have assigned

control of the tickets to one individual, in a locked box which that student

alone had control over.

4. Documentation procedures. There was no control over unsold tickets.

This deficiency made it possible for students to sell the tickets, keep

the cash, and tell Matt that they had disposed of the unsold tickets.

Instead, students should have been required to return the unsold

tickets to the student maintaining control over tickets, and the cash to

Matt. In each case, the students should have been issued a receipt for

the cash they turned in and the tickets they returned.

PROBLEM 8-6A (Continued)

7. Segregation of duties. Jeff Kenney counted the funds, made out the

deposit slip, and took the funds to the bank. This made it possible for

Jeff Kenney to take some of the money and deposit the rest since there

was no external check on his work. Matt should have counted the funds,

with someone observing him. Then he could have made out the deposit

slip and had Jeff Kenney deposit the funds.

COMPREHENSIVE PROBLEM SOLUTION

(a)

Dec. 7

Cash .............................................................

Accounts Receivable ..........................

3,600

3,600

12

Inventory ......................................................

Accounts Payable ...............................

12,000

12,000

19

Salaries and Wages Expense .....................

Cash .....................................................

2,200

2,200

22

Accounts Payable .......................................

Cash ($12,000 X .99) ............................

Inventory ..............................................

12,000

11,880

120

COMPREHENSIVE PROBLEM SOLUTION (Continued)

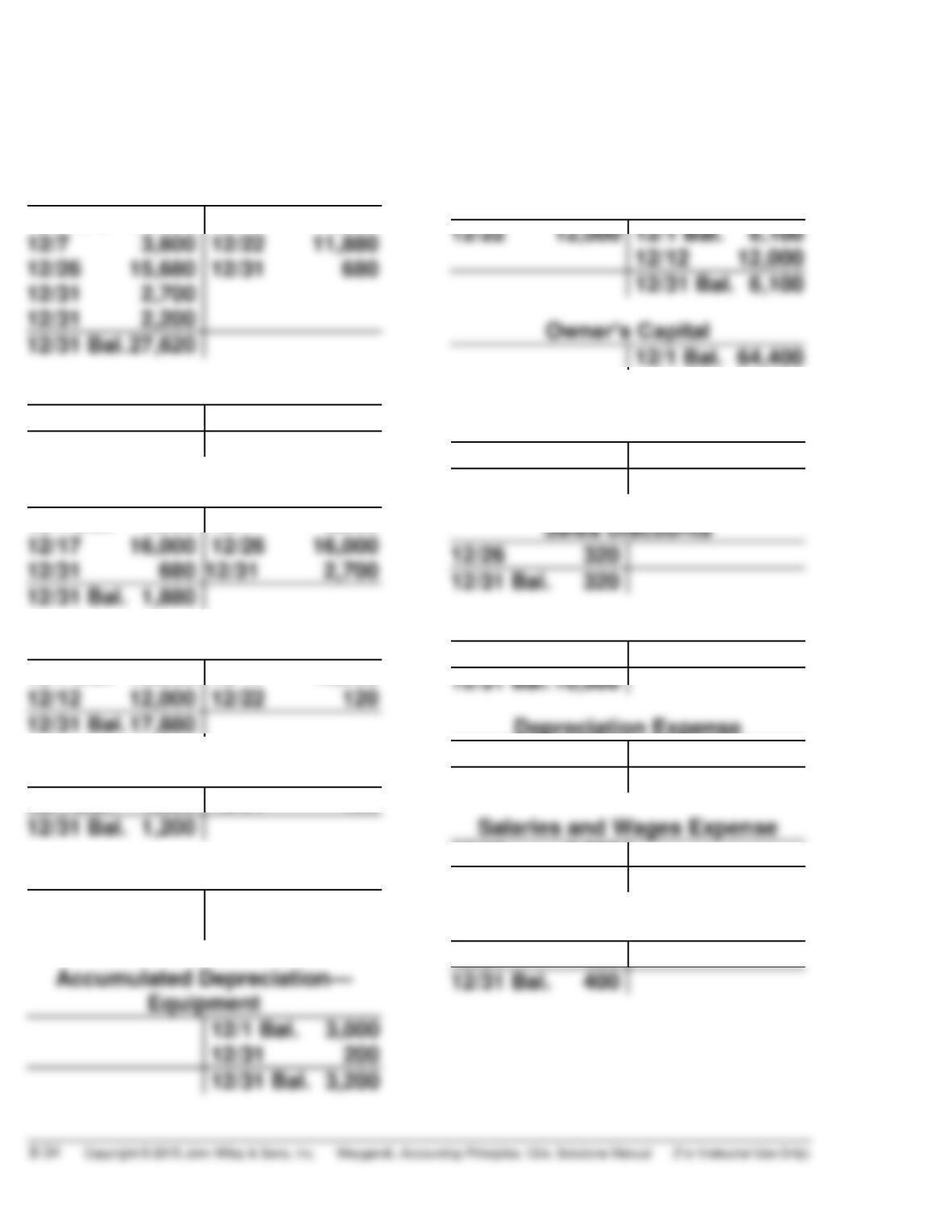

(b) & (e) General Ledger

Cash

12/1 Bal. 18,200

12/7 3,600

12/26 15,680

12/19 2,200

12/22 11,880

12/31 680

Notes Receivable

12/1 Bal. 2,200

12/31 2,200

12/31 Bal. – 0 –

Accounts Receivable

12/1 Bal. 7,500

12/7 3,600

Inventory

12/1 Bal. 16,000

12/12 12,000

12/17 10,000

12/22 120

12/31 Bal. 17,880

Prepaid Insurance

Accumulated Depreciation—

Equipment

12/1 Bal. 3,000

Accounts Payable

12/22 12,000

12/1 Bal. 6,100

12/12 12,000

12/1 Bal. 64,400

Sales Revenue

12/17 16,000

12/31 Bal. 16,000

Cost of Goods Sold

12/17 10,000

12/31 Bal. 10,000

Depreciation Expense

12/31 200

12/31 Bal. 200

Insurance Expense

12/31 400

12/31 Bal. 400

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(c) FULLERTON COMPANY

Bank Reconciliation

December 31, 2017

Cash balance per bank statement .......................... $26,130

Add: Deposits in transit .......................................... 2,700

28,830

Less: Outstanding checks ...................................... 1,210

Adjusted cash balance per bank ............................ $27,620

(d) Dec. 31 Cash .......................................................... 2,200

Notes Receivable ............................... 2,200

31 Accounts Receivable—L. Bryan .............. 680

Cash .................................................... 680