CHAPTER 8

SOLUTIONS TO PROBLEMS—SET C

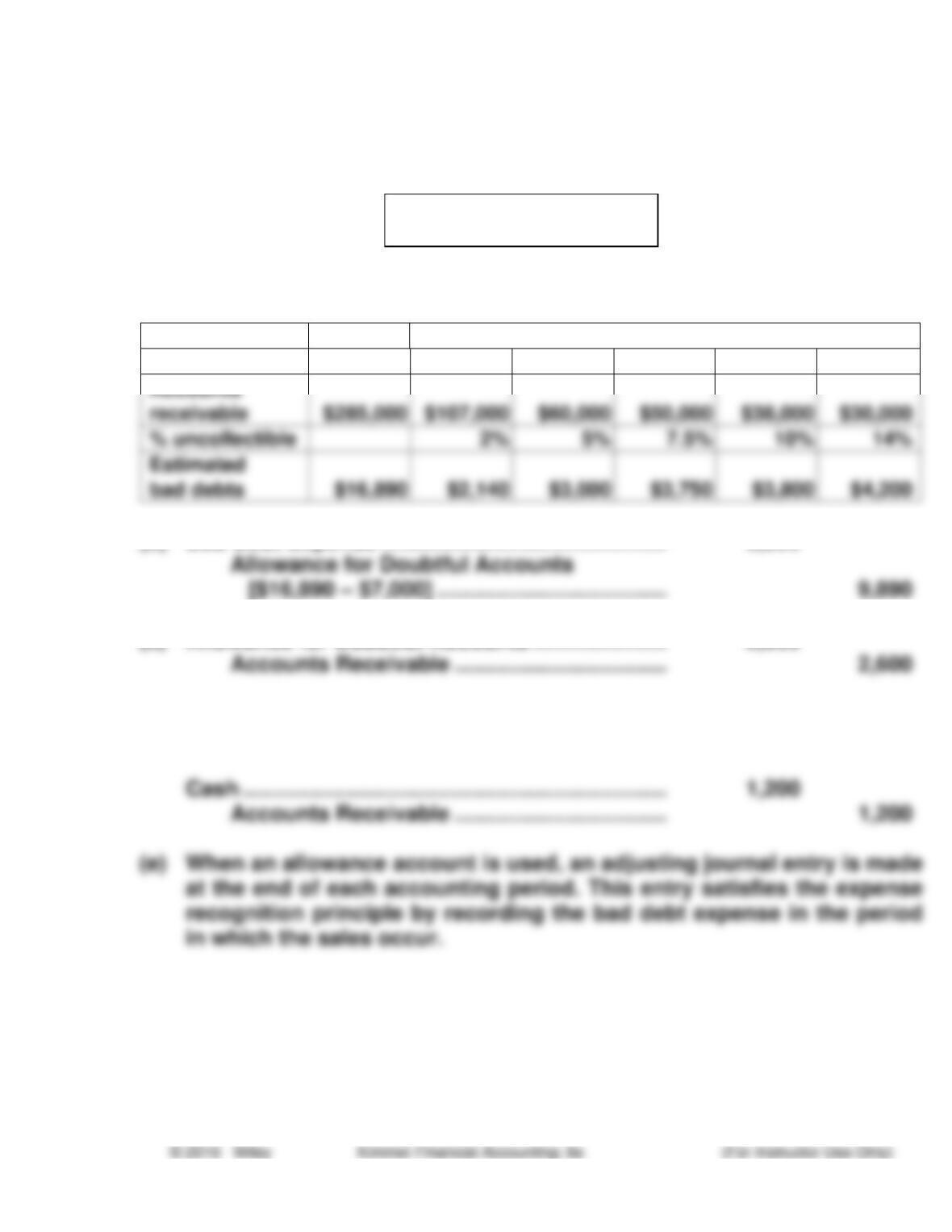

(a) Total estimated bad debts

Number of Days Outstanding

Total

0–30

31–60

61–90

91–120

Over 120

receivable

% uncollectible

bad debts

(b) Bad Debt Expense ……………………………………….. 9,890

(c) Allowance for Doubtful Accounts …………………. 2,600

(d) Accounts Receivable ……………………………………. 1,200

Allowance for Doubtful Accounts …………… 1,200

PROBLEM 8-1C

PROBLEM 8-2C

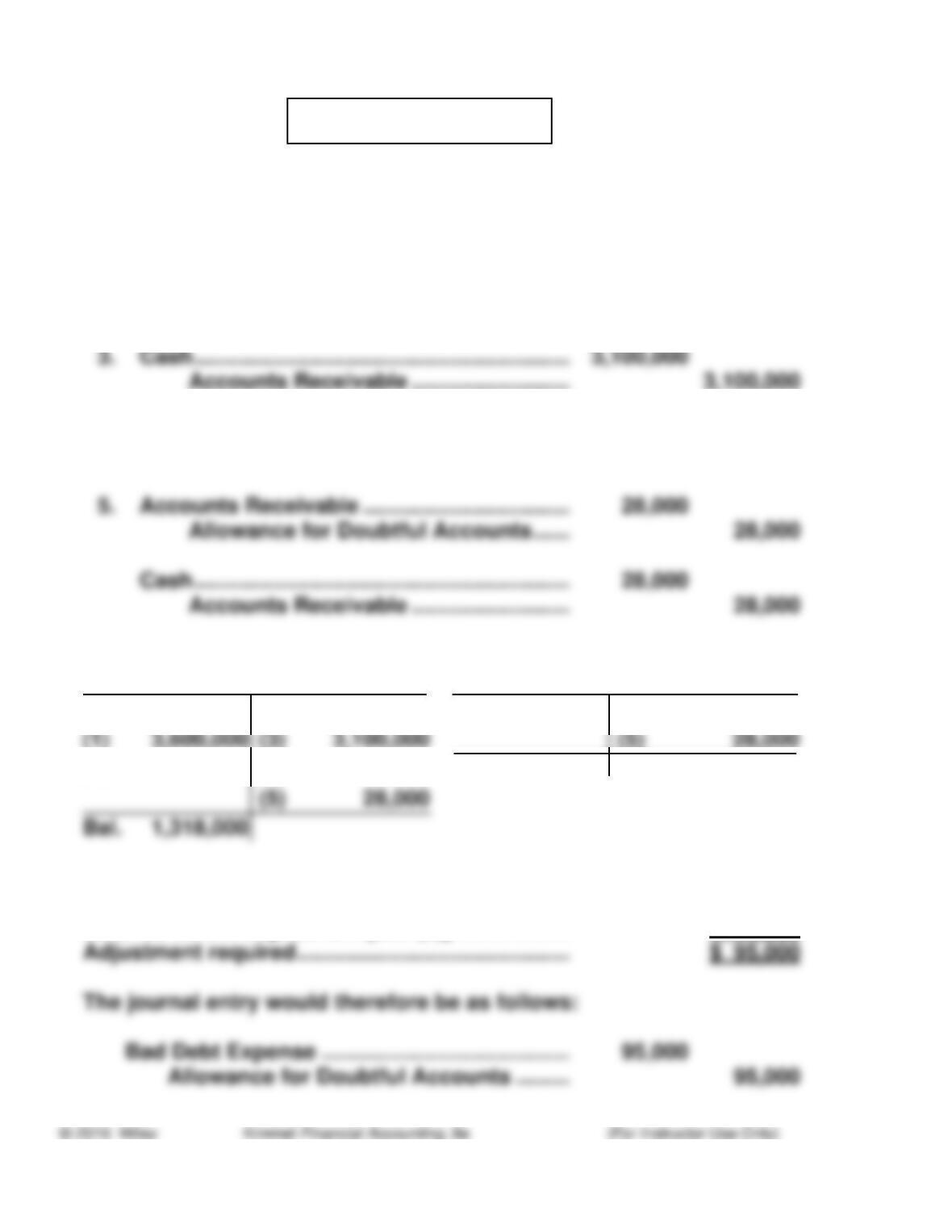

(a) 1. Accounts Receivable …………………………... 3,600,000

Sales Revenue ………………………………. 3,600,000

2. Sales Returns and Allowances ……………… 50,000

Accounts Receivable …………………….. 50,000

4. Allowance for Doubtful Accounts ………….. 92,000

Accounts Receivable …………………….. 92,000

(b) Accounts Receivable Allowance for Doubtful Accounts

Bal. 960,000 (2) 50,000 (4) 92,000 Bal. 78,000

(5) 28,000 (4) 92,000 Bal. 14,000

(c) Balance needed ……………………………………………. $109,000

Balance before adjustment [see (b)] ………………. 14,000

PROBLEM 8-2C (Continued)

(d)

$3,600,000 –$50,000

($882,000*+ $1,209,000**)÷2=$3,550,000

$1,045,500 = 3.4 times

PROBLEM 8-3C

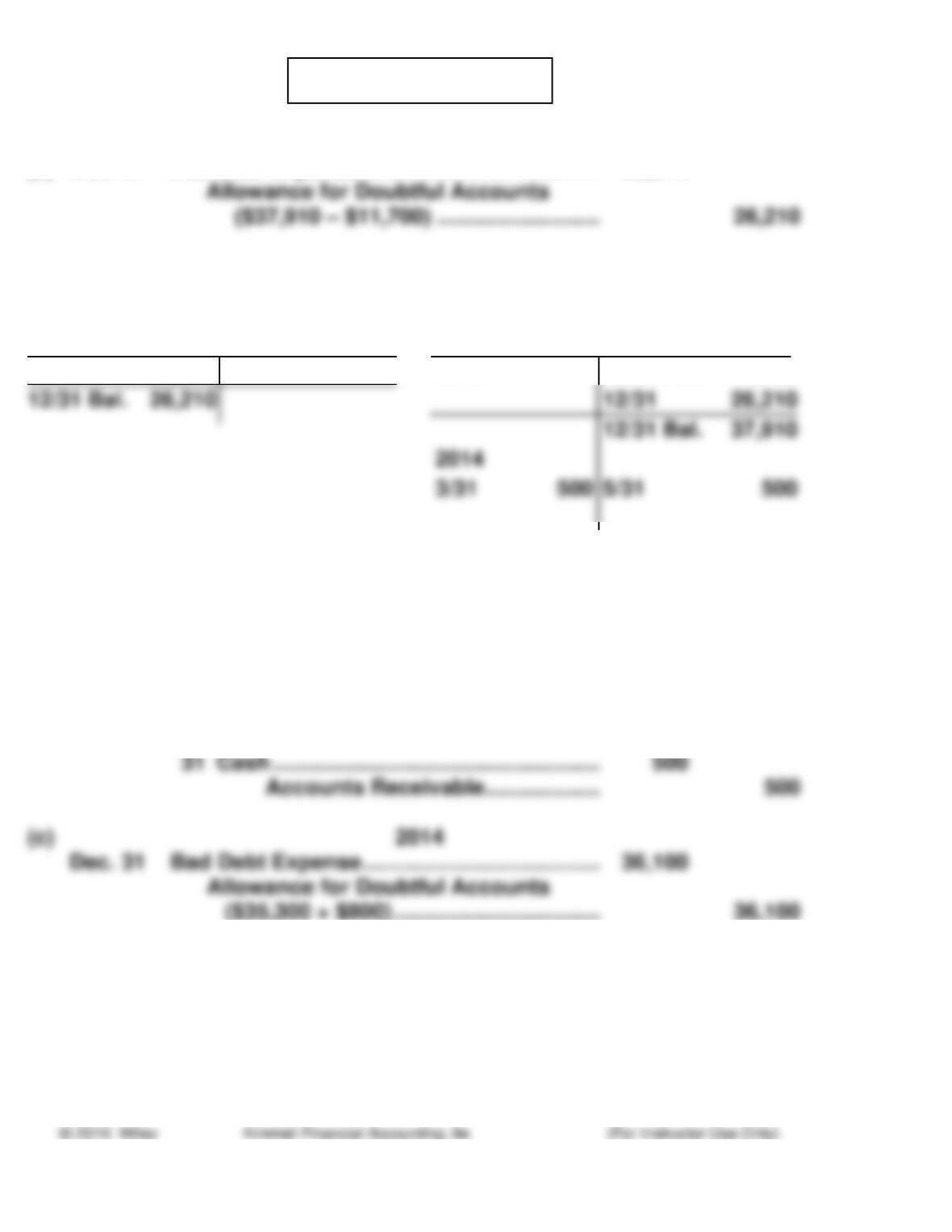

(a) Dec. 31 Bad Debt Expense ………………………………… 26,210

(a) & (b)

Bad Debt Expense Allowance for Doubtful Accounts

12/31 26,210 2013 12/31 Bal. 11,700

(b) 2014

(1) Mar. 31 Allowance for Doubtful Accounts …… 500

Accounts Receivable ………………. 500

(2) May 31 Accounts Receivable ……………………… 500

Allowance for Doubtful

Accounts …………………………….. 500

PROBLEM 8-4C

(a) $15,000.

(b) $12,300 [($400,000 X 4%) – $3,700].

PROBLEM 8-5C

(a) The allowance method is being used by Seidl. Since the balance in

the allowance for doubtful accounts is given, it must be using this

method because the account would not exist if it were using the direct

write-off method.

(b) Dec. 31 Bad Debt Expense ($26,000 – $4,800) ……. 21,200

Allowance for Doubtful Accounts ……. 21,200

PROBLEM 8-6C

Jan. 5 Accounts Receivable—Flint Company ………. 10,000

Sales Revenue ……………………………………. 10,000

20 Notes Receivable ……………………………………… 10,000

Accounts Receivable—Flint Company … 10,000

May 25 Notes Receivable ……………………………………… 9,000

Accounts Receivable—Aberd Inc ………… 9,000

Aug. 18 Cash ($4,000 + $160) …………………………………. 4,160

Notes Receivable ……………………………….. 4,000

Interest Revenue

($4,000 X 8% X 6/12) …………………………. 160

PROBLEM 8-7C

(a)

Transaction

Accounts

Receivable

Turnover

(6X)

Average

Collection

Period

(61 days)

2.

Collected amounts owed by

customers.

I

D

3.

method)

Wrote off an account receivable

4.

Recorded sales returns and credited

the customers’ accounts.

I

D

5.

Recorded bad debt expense for the

year using the allowance method.

I

D

(b) There are three reasons why companies sell their receivables:

• Large companies encourage sales of their products by providing

financing to their customers. These companies do not want to manage

PROBLEM 8-8C

(a) Oct. 7 Accounts Receivable ………………………. 4,600

Sales Revenue …………………………... 4,600

12 Cash ($600 – $18) ……………………………. 582

Service Charge Expense

(b)

Notes Receivable Interest Receivable

10/1 Bal. 18,800 10/15 6,000 10/31 49

PROBLEM 8-8C (Continued)

BROCKMAN COMPANY

Balance Sheet (Partial)

October 31, 201X

(c) Current assets

Notes receivable …………………………………………….. $ 9,800

PROBLEM 8-9C

Intel AMD

Accounts receivable

turnover

$35,127

($1,712a+ $2,273b)÷2

$5,403

($320c+$745d)÷ 2