CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN)

BUDGETING

DISCUSSION QUESTIONS

1. The three major objectives of budgeting are (1) to establish specific goals for future

operations, (2) to execute plans to achieve the goals, and (3) to periodically compare

actual results with the goals.

4. Conflicting goals can cause employees or department managers to act in their own self-

interests to the detriment of the organization’s objectives.

5. A static budget is most appropriate in situations where costs are not variable to an underlying

activity level. As a result, it is reasonable to plan spending on the basis of a fixed quantity of

resources for the year. This will occur in some administrative functions, such as human

resources, accounting, or public relations.

8. Purchases of direct materials should be closely coordinated with the production budget so

that inventory levels can be maintained within reasonable limits.

9. a. The cash budget contributes to effective cash planning. This involves advance planning

so that a cash shortage does not arise and excess cash is not permitted to remain “idle.”

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

BASIC EXERCISES

BE 22–1 (FIN MAN); BE 8–1 (MAN)

Variable cost:

Direct labor (2,350 hours × $30* per hour) ………………………………………

$70,500

Fixed cost:

BE 22–2 (FIN MAN); BE 8–2 (MAN)

Pasadena Candle Inc.

Production Budget

For the Month Ending January 31

Expected units to be sold

800,000

Total units to be produced in January

785,000

BE 22–3 (FIN MAN); BE 8–3 (MAN)

Pasadena Candle Inc.

Direct Materials Purchases Budget

For the Month Ending January 31

Pounds of wax required for production:

Candles [(785,000 × 10 oz.) ÷ 16 oz.]

490,625

503,125

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

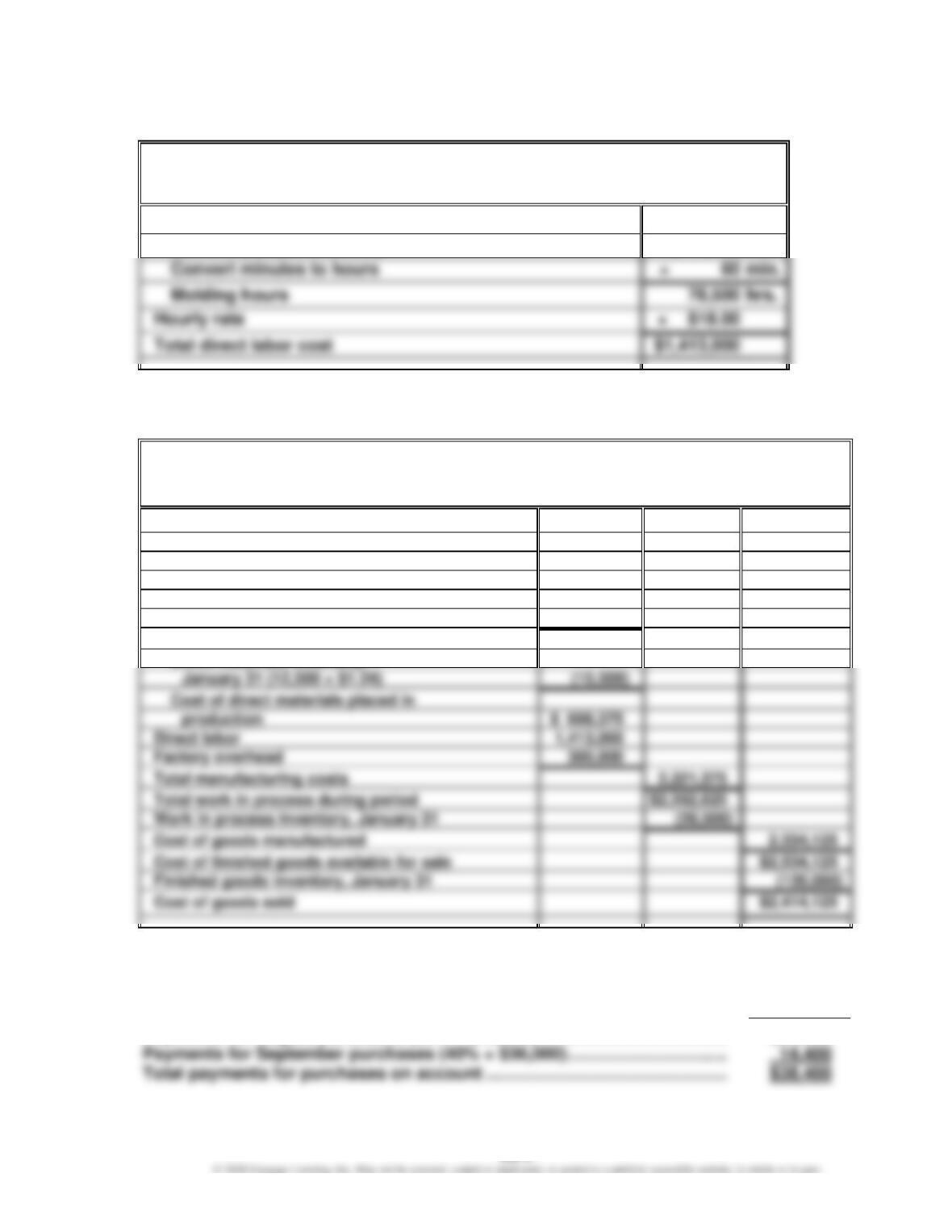

BE 22–4 (FIN MAN); BE 8–4 (MAN)

Pasadena Candle Inc.

Direct Labor Cost Budget

For the Month Ending January 31

Hours required for assembly:

Candles (785,000 × 6 min.)

4,710,000

min.

Molding hours

hrs.

BE 22–5 (FIN MAN); BE 8–5 (MAN)

Pasadena Candle Inc.

Cost of Goods Sold Budget

For the Month Ending January 31

Finished goods inventory, January 1

$ 200,000

Work in process inventory, January 1

$ 41,250

Direct materials:

Direct materials inventory, January 1

(16,000 × $1.24)

$ 19,840

Direct materials purchases

604,035

Cost of direct materials available for use

$ 623,875

Direct materials inventory,

January 31 (12,500 × $1.24)

Cost of direct materials placed in

$ 608,375

Direct labor

Factory overhead

300,000

Total manufacturing costs

Total work in process during period

$2,362,625

Work in process inventory, January 31

Cost of goods manufactured

Cost of finished goods available for sale

$2,534,125

Finished goods inventory, January 31

BE 22–6 (FIN MAN); BE 8–6 (MAN)

September

Payments for August purchases (60% × $40,000) …………………………………

$24,000

Payments for September purchases (40% × $36,000) …………………………...

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

EXERCISES

Ex. 22–1 (FIN MAN); Ex. 8–1 (MAN)

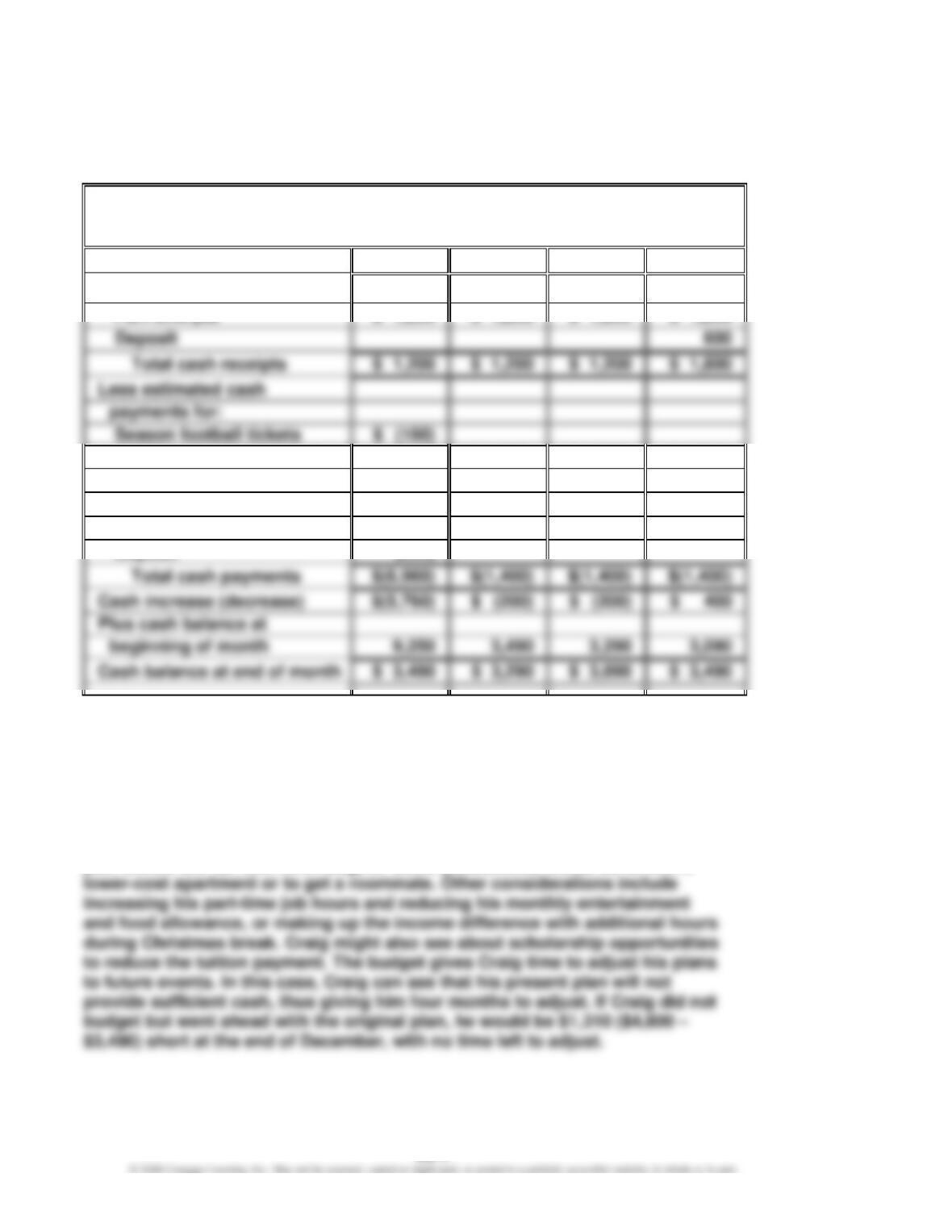

a.

Craig Kovar

Cash Budget

For the Four Months Ending December 31

September

October

November

December

Estimated cash receipts from:

Season football tickets

Additional entertainment

(250)

$ (250)

$ (250)

$ (250)

Tuition

(4,800)

Rent

(600)

(600)

(600)

(600)

Food

(550)

(550)

(550)

(550)

(600)

$ (200)

$ (200)

3,090

b. The four-month budgets do not change with any identified activity level; thus,

they are static budgets.

c. While Craig’s budget might first appear satisfactory, Craig must earn enough

cash in order to pay for the spring semester tuition. His present budget shows

that he will be $1,310 short of the tuition amount ($4,800 – $3,490) by the time

he needs to pay his spring tuition. Thus, Craig will likely need to adjust the

plan before the fall term even begins. Some possibilities would be to rent a

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Ex. 22–2 (FIN MAN); Ex. 8–2 (MAN)

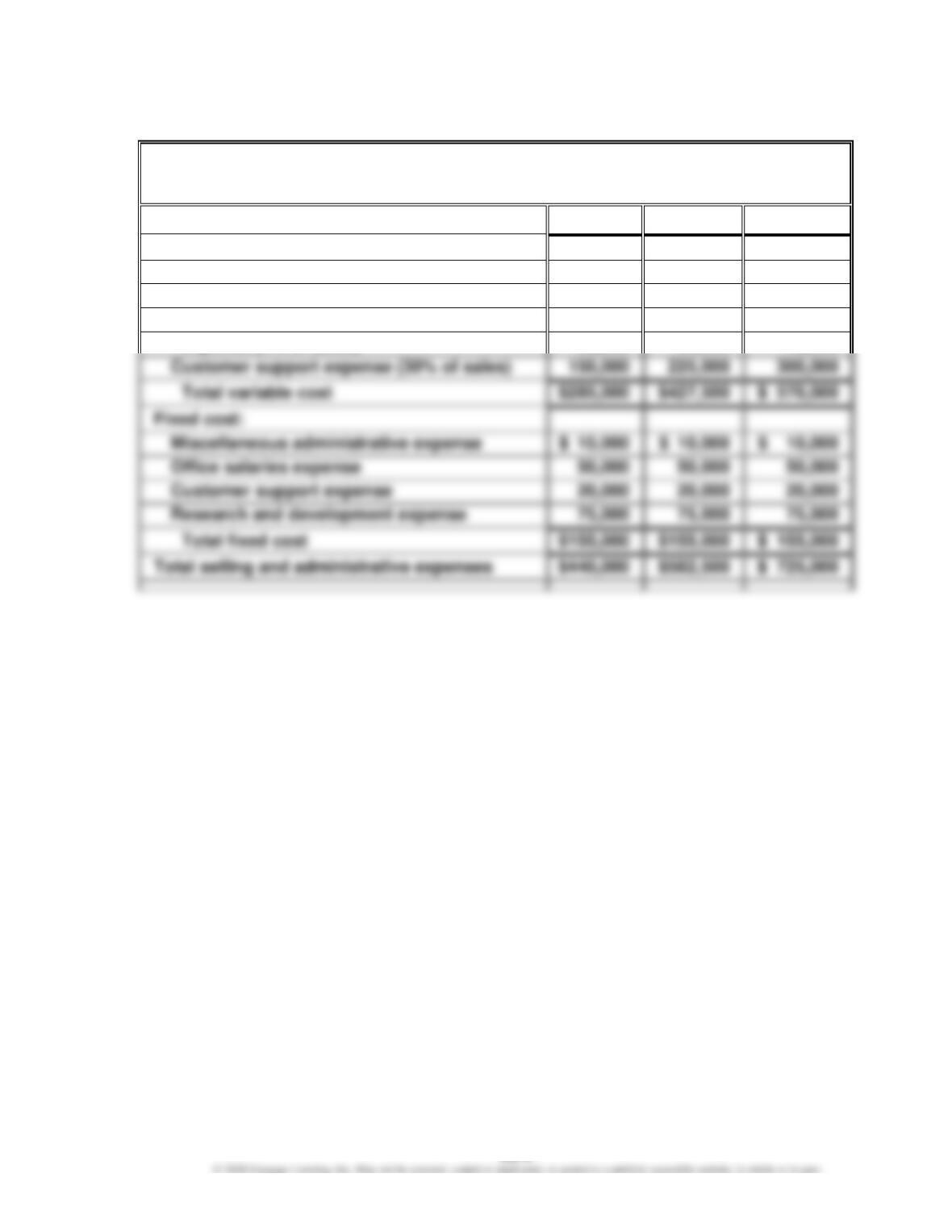

Digital Solutions Inc.

Flexible Selling and Administrative Expenses Budget

For the Month Ending October 31

Total sales

$500,000

$750,000

$1,000,000

Variable cost:

Sales commissions (8% of sales)

$ 40,000

$ 60,000

$ 80,000

Advertising expense (15% of sales)

75,000

112,500

150,000

Miscellaneous administrative

expense (4% of sales)

20,000

30,000

40,000

Customer support expense (30% of sales)

$ 570,000

Fixed cost:

Miscellaneous administrative expense

$ 10,000

Office salaries expense

Customer support expense

20,000

20,000

20,000

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Ex. 22–3 (FIN MAN); Ex. 8–3 (MAN)

a.

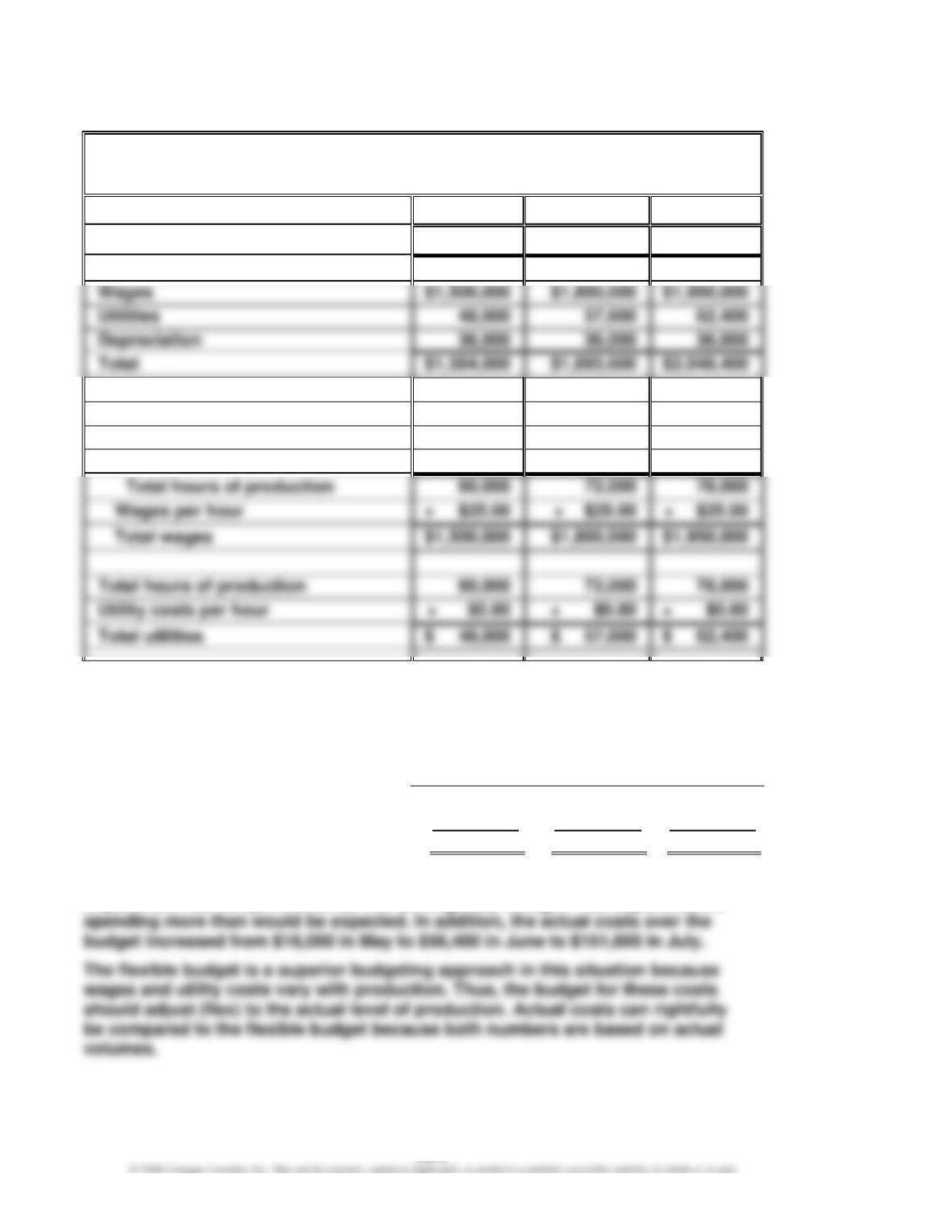

Hagerstown Company

Machining Department Budget

For the Three Months Ending July 31

May

June

July

Units of production

40,000

48,000

52,000

Supporting calculations:

Units of production

40,000

48,000

52,000

Hours per unit

× 1.50

× 1.50

× 1.50

Wages per hour

× $25.00

Total hours of production

Utility costs per hour

Depreciation is a fixed cost, so it does not “flex” with changes in production.

Because it is the only fixed cost, the variable and fixed costs are not classified in

the budget.

b.

May

June

July

Total flexible budget …………………………..

$ 1,584,000

$ 1,893,600

$ 2,048,400

Actual cost …………………………………………..

(1,600,000)

(1,950,000)

(2,200,000)

Excess of actual cost over budget …………

$ (16,000)

$ (56,400)

$ (151,600)

The excess of actual cost over the flexible budget suggests that the Machining

Department has not performed as well as originally thought. The department is

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

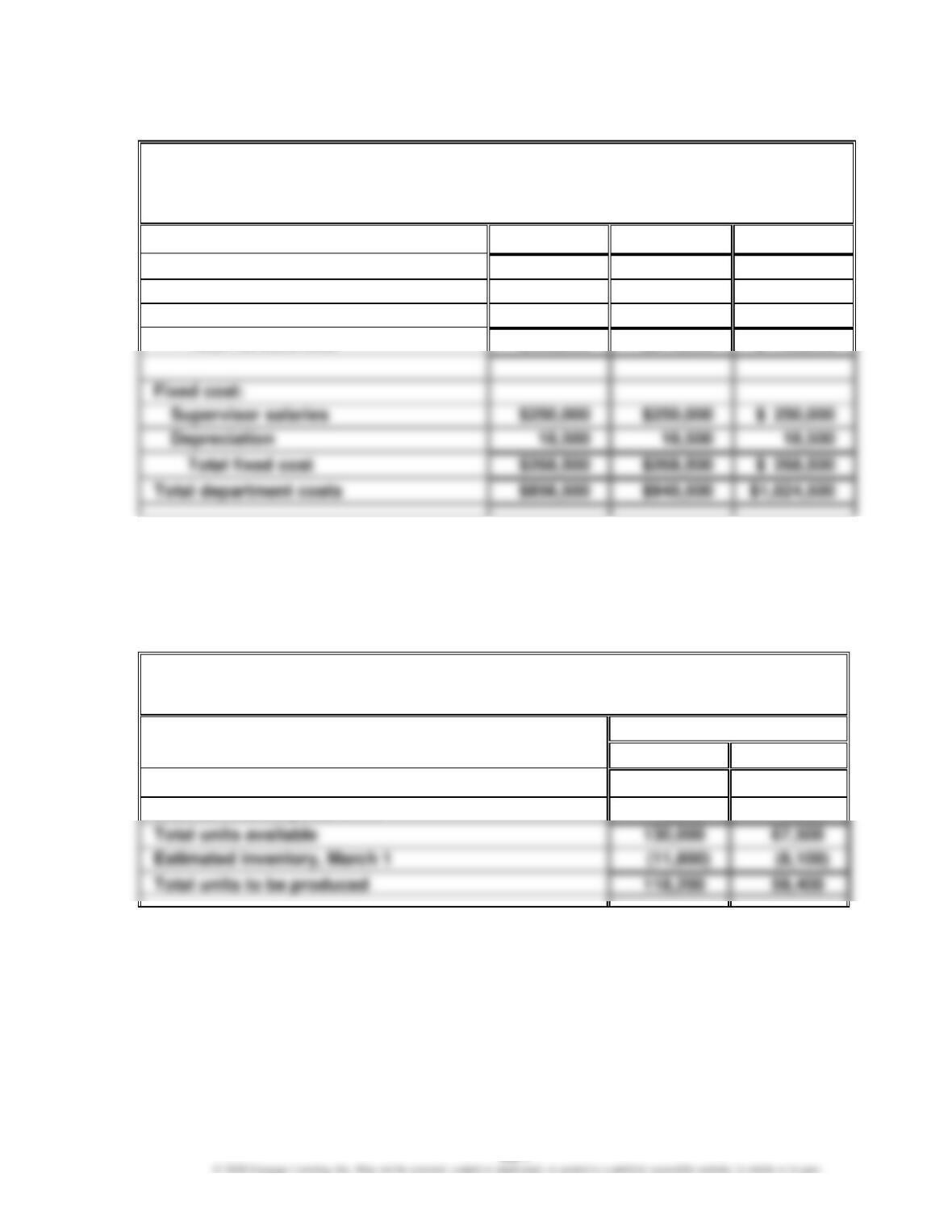

Ex. 22–4 (FIN MAN); Ex. 8–4 (MAN)

Steelcase Inc.

Assembly Department Budget

For the Month Ending February 28

(assumed data)

Units of production

70,000

80,000

90,000

Variable cost:

Direct labor

$588,0001

$672,0002

$ 756,0003

Total variable cost

$588,000

$672,000

$ 756,000

Supervisor salaries

$250,000

$ 250,000

18,500

1 70,000 × 18/60 min. × $28

2 80,000 × 18/60 min. × $28

3 90,000 × 18/60 min. × $28

Ex. 22-5 (FIN MAN); Ex. 8-5 (MAN)

Healthy Measures Inc.

Production Budget

For the Month Ending March 31

Units

Bath Scale

Gym Scale

Expected units to be sold

115,000

60,000

Desired inventory, March 31

15,000

7,500

Total units available

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

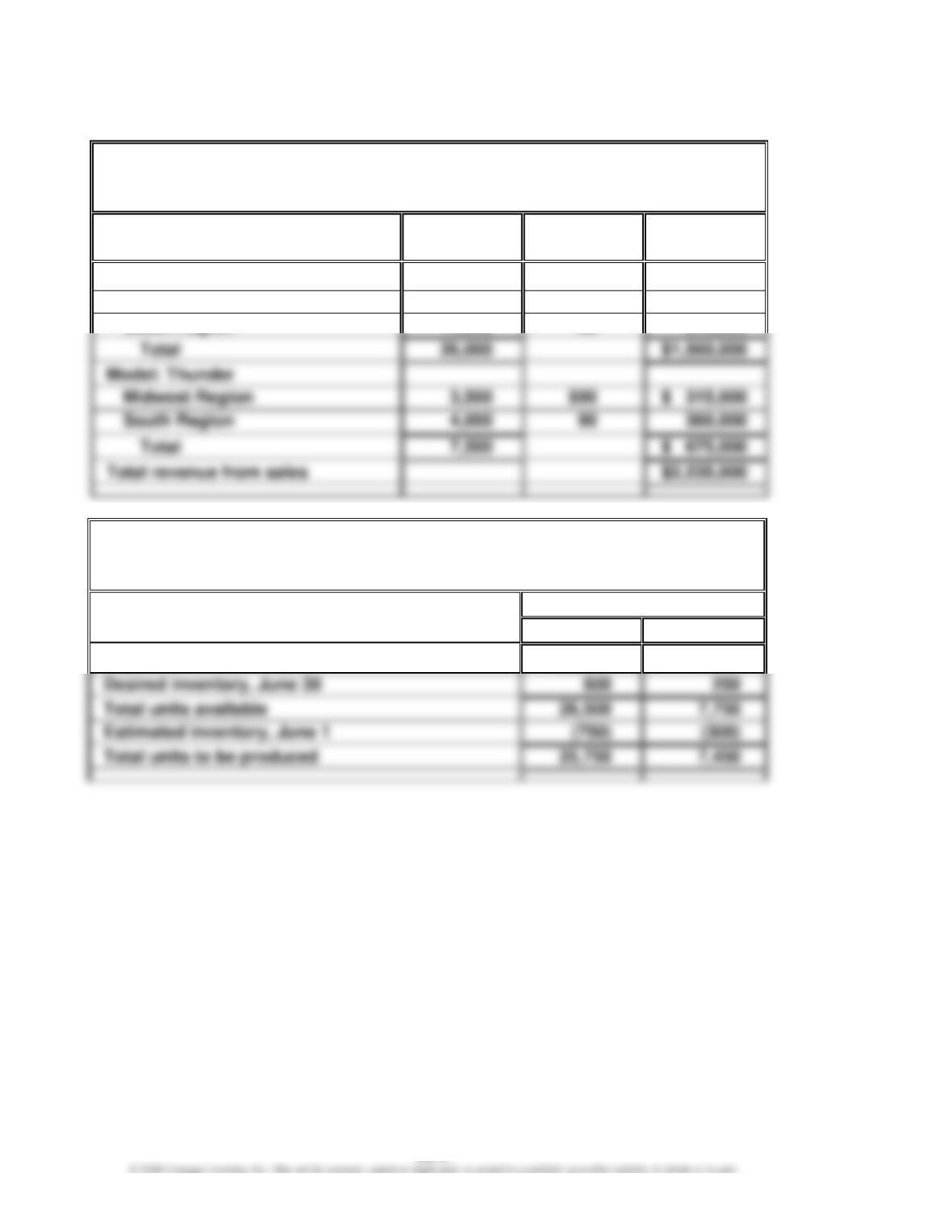

Ex. 22–6 (FIN MAN); Ex. 8–6 (MAN)

a.

Sonic Inc.

Sales Budget

For the Month Ending June 30

Product and Area

Unit Sales

Volume

Unit Selling

Price

Total Sales

Model: Rumble

Midwest Region

12,000

$60

$ 720,000

South Region

14,000

26,000

$ 675,000

b.

Sonic Inc.

Production Budget

For the Month Ending June 30

Units

Rumble

Thunder

Expected units to be sold

26,000

7,500

26,500

25,750

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

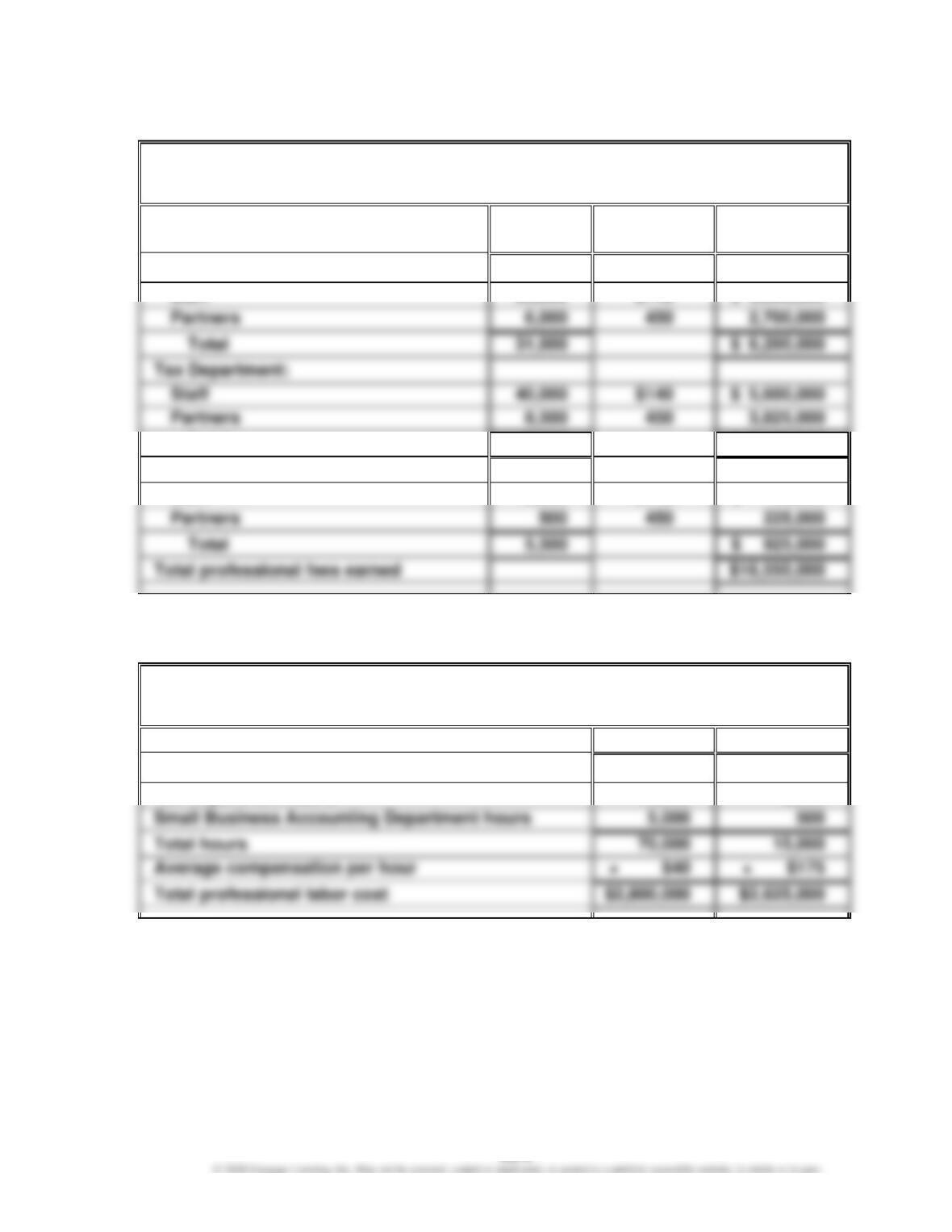

Ex. 22–7 (FIN MAN); Ex. 8–7 (MAN)

Lundquist & Fretwell, CPAs

Professional Fees Earned Budget

For the Year Ending May 31, 20Y8

Billable

Hours

Hourly

Rate

Total

Revenue

Audit Department:

Staff

$140

Partners

6,000

Total

31,000

$ 6,200,000

40,000

$ 5,600,000

Partners

8,500

Total

48,500

$ 9,425,000

Small Business Accounting Department:

Staff

5,000

$140

$ 700,000

Partners

Total

Ex. 22–8 (FIN MAN); Ex. 8–8 (MAN)

Lundquist & Fretwell, CPAs

Professional Labor Cost Budget

For the Year Ending December 31, 20Y8

Staff

Partners

Audit Department hours

25,000

6,000

Tax Department hours

40,000

8,500

Small Business Accounting Department hours

Total hours

70,000

Average compensation per hour

× $40

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

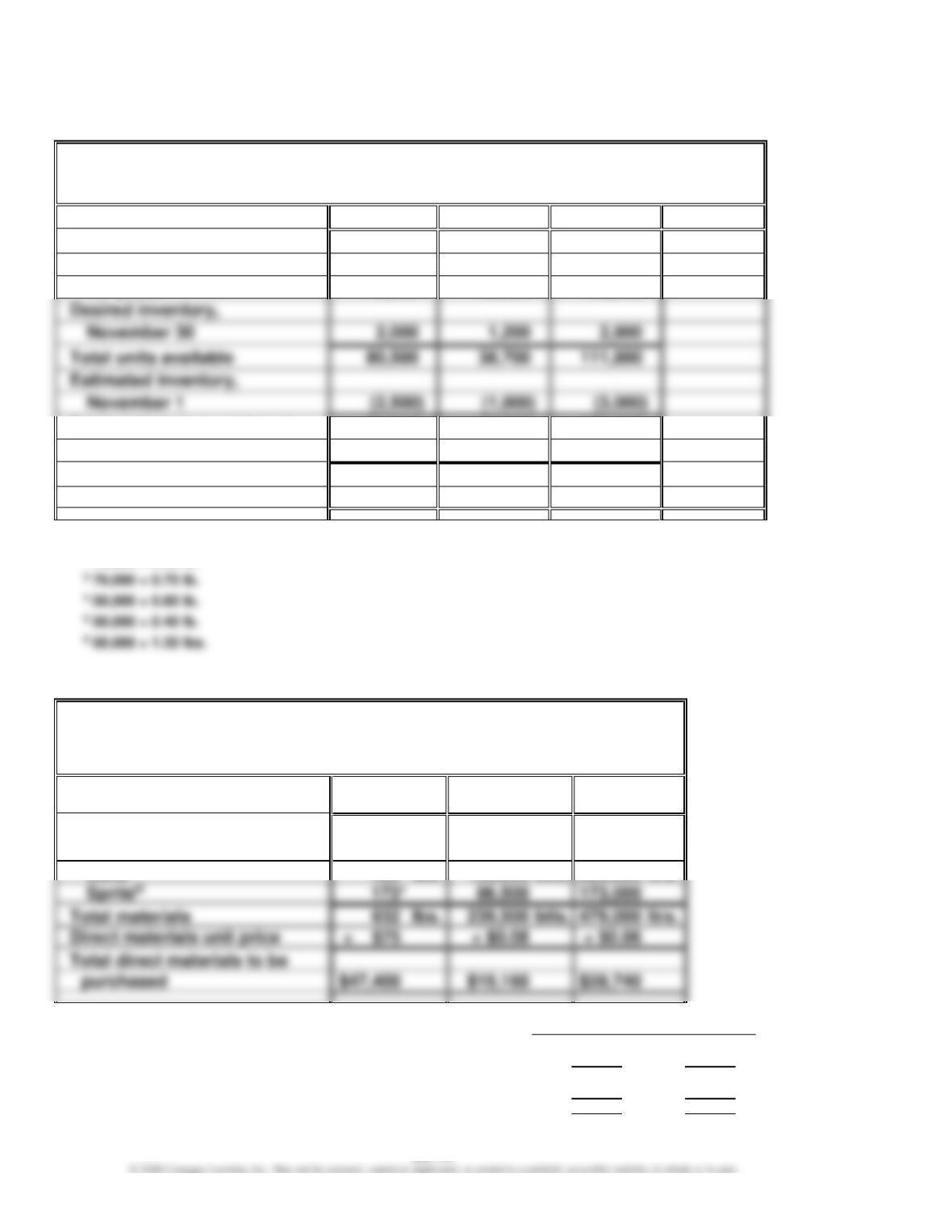

Ex. 22–9 (FIN MAN); Ex. 8–9 (MAN)

Tobin’s Frozen Pizza Inc.

Direct Materials Purchases Budget

For the Month Ending November 30

Dough

Tomato

Cheese

Total

Units required for production:

12″ pizza

38,5001

17,5002

49,0003

16″ pizza

40,0004

20,0005

60,0006

Desired inventory,

November 30

Total units available

80,500

38,700

111,800

Estimated inventory,

November 1

Total units to be purchased

78,000

37,700

108,800

Unit price

× $0.50

× $0.60

× $0.85

Total direct materials to

be purchased

$39,000

$22,620

$92,480

$154,100

1 70,000 × 0.55 lb.

2 70,000 × 0.25 lb.

Ex. 22–10 (FIN MAN); Ex. 8–10 (MAN)

Coca-Cola Enterprises—Wakefield Plant

Direct Materials Purchases Budget

For the Month Ending May 31

(assumed data)

Concentrate

2-Liter

Bottles

Carbonated

Water

Materials required for

production:

Coke®

Sprite®

* Production in liters (bottles × 2 liters/bottle) ………………………….

306,000

173,000

Divide by 100 ……………………………………………………………………….

÷ 100

÷ 100

3,060

1,730

Multiply by concentrate pounds per 100 liters ……………………….

× 0.15

× 0.10

Concentrate pounds required for production ………………………..

459

173

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

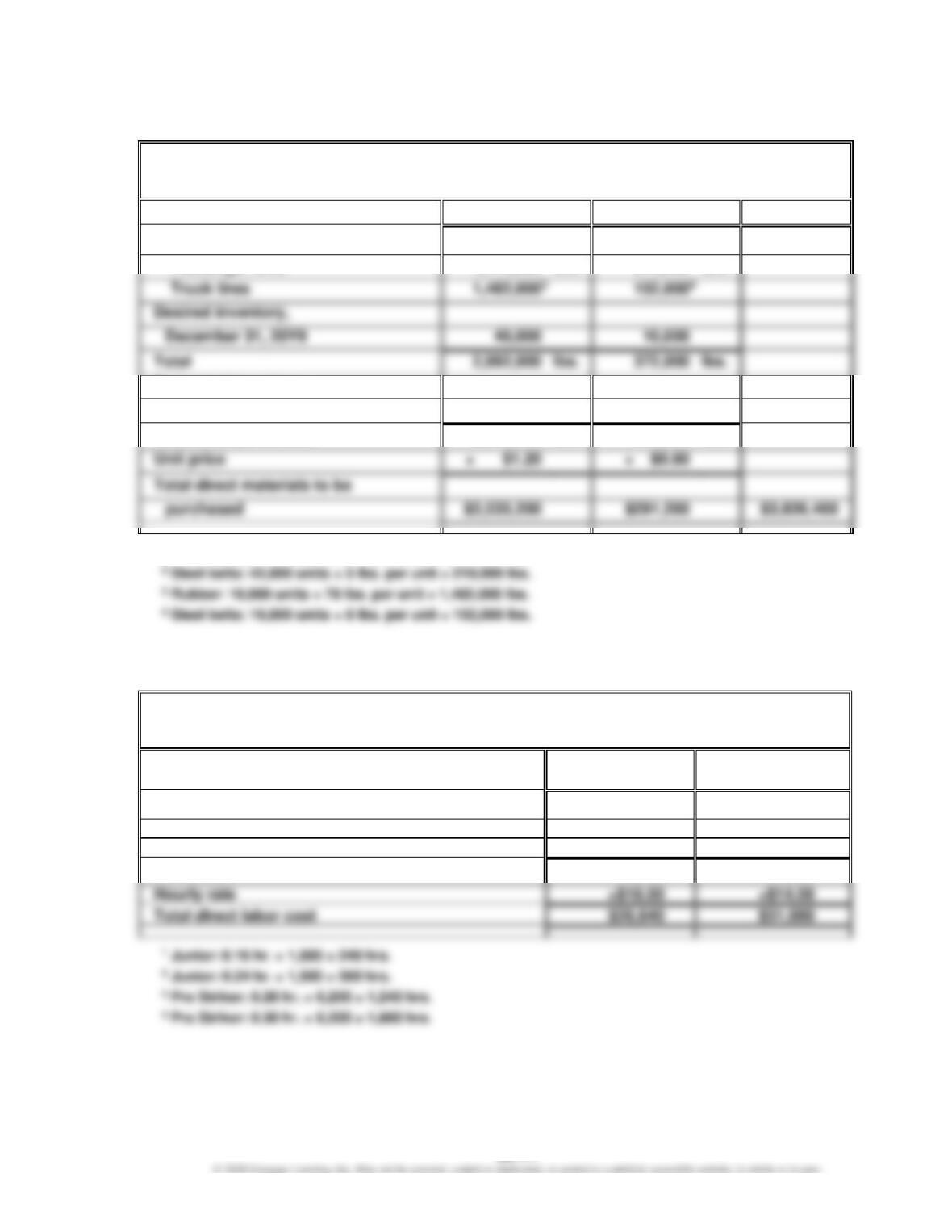

Ex. 22–11 (FIN MAN); Ex. 8–11 (MAN)

Safety Grip Company

Direct Materials Purchases Budget

For the Year Ending December 31, 20Y9

Rubber

Steel Belts

Total

Pounds required for production:

Passenger tires

1,470,000

lbs.1

210,000

lbs.2

1,482,0003

152,0004

Desired inventory,

2,992,000

lbs.

372,000

lbs.

Estimated inventory,

January 1, 20Y9

(46,000)

(8,000)

Total units purchased

2,946,000

lbs.

364,000

lbs.

Total direct materials to be

1 Rubber: 42,000 units × 35 lbs. per unit = 1,470,000 lbs.

Ex. 22–12 (FIN MAN); Ex. 8–12 (MAN)

Ace Racket Company

Direct Labor Cost Budget

For the Month Ending July 31

Forming

Department

Assembly

Department

Hours required for production:

Junior

2401

3602

Pro Striker

1,2403

1,8604

Total

1,480

2,220

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Ex. 22–13 (FIN MAN); Ex. 8–13 (MAN)

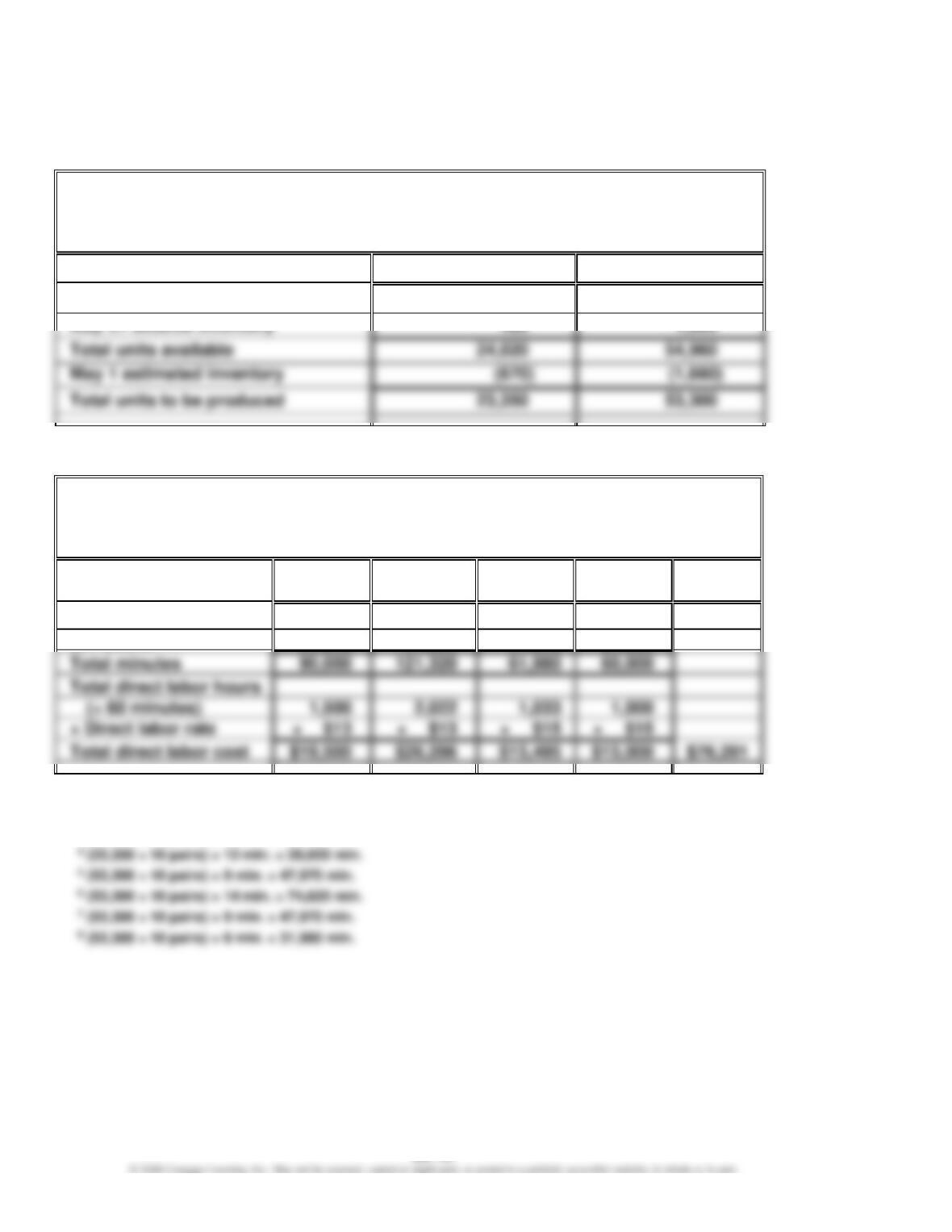

a.

Levi Strauss & Co.

Production Budget

For the Month Ending May 31

(assumed data)

Dockers®

501 Jeans®

Expected units to be sold

23,600

53,100

b.

Levi Strauss & Co.

Direct Labor Cost Budget

For the Month Ending May 31

(assumed data)

Inseam

Outer-

seam

Pockets

Zipper

Total

Dockers®

42,0301

46,7002

14,0103

28,0204

501 Jeans®

47,9705

74,6206

47,9707

31,9808

1 (23,350 ÷ 10 pairs) × 18 min. = 42,030 min.

2 (23,350 ÷ 10 pairs) × 20 min. = 46,700 min.

3 (23,350 ÷ 10 pairs) × 6 min. = 14,010 min.

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

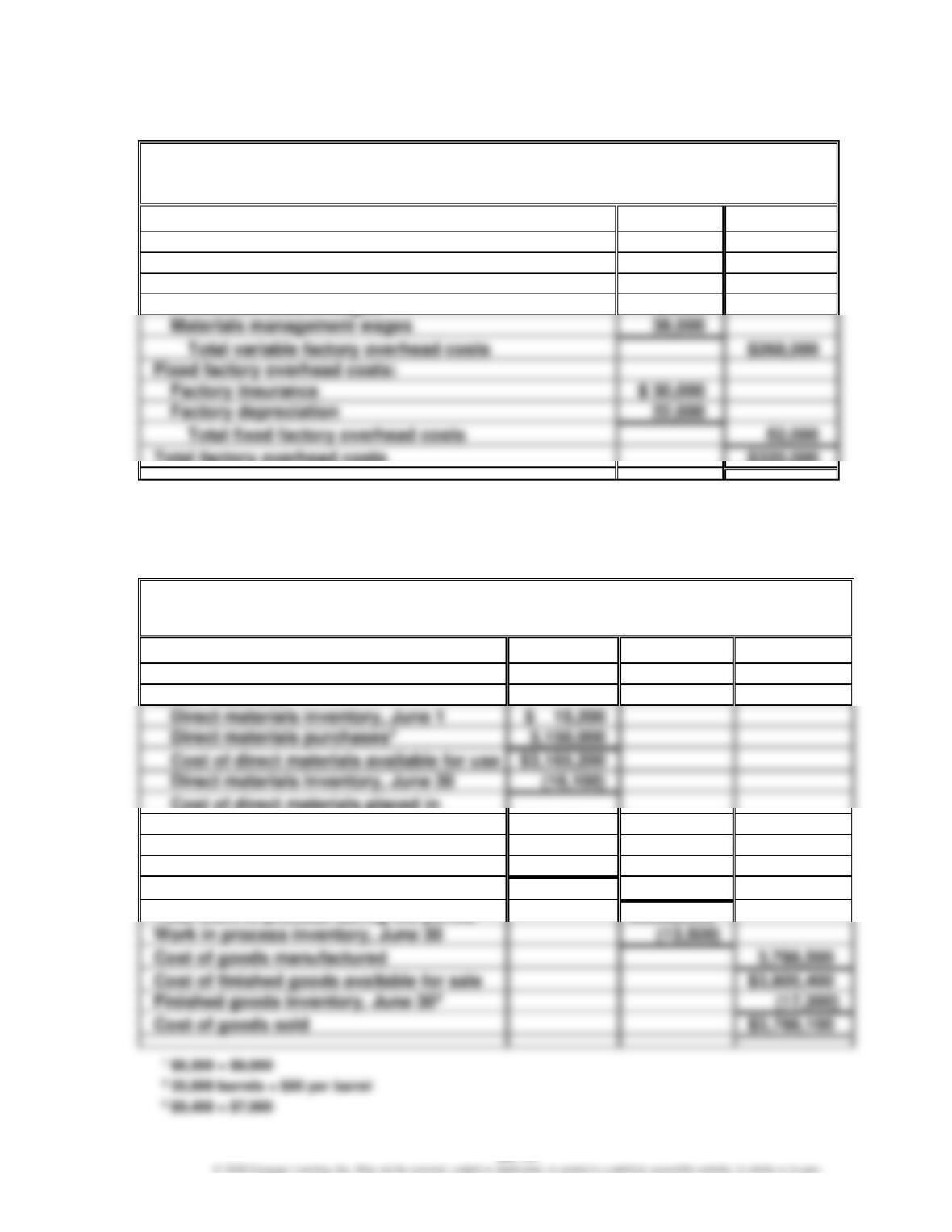

Ex. 22–14 (FIN MAN); Ex. 8–14 (MAN)

Sweet Tooth Candy Company

Factory Overhead Cost Budget

For the Month Ending August 31

Variable factory overhead costs:

Manufacturing supplies

$ 14,000

Power and light

48,000

Production supervisor wages

135,000

Production control wages

32,000

Materials management wages

39,000

$268,000

Fixed factory overhead costs:

Factory insurance

$ 30,000

Factory depreciation

22,000

Total factory overhead costs

$320,000

Note: Advertising expenses, sales commissions, and executive officer salaries are selling

and administrative expenses.

Ex. 22–15 (FIN MAN); Ex. 8–15 (MAN)

Delaware Chemical Company

Cost of Goods Sold Budget

For the Month Ending June 30

Finished goods inventory, June 11

$ 16,900

Work in process inventory, June 1

$ 12,900

Direct materials:

Direct materials inventory, June 1

Cost of direct materials available for use

$3,165,200

Direct materials inventory, June 30

Cost of direct materials placed in

production

$3,149,100

Direct labor

240,000

Factory overhead

400,000

Total manufacturing costs

3,789,100

Total work in process during the period

Work in process inventory, June 30

(13,500)

Cost of goods manufactured

3,788,500

Cost of finished goods available for sale

Cost of goods sold

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

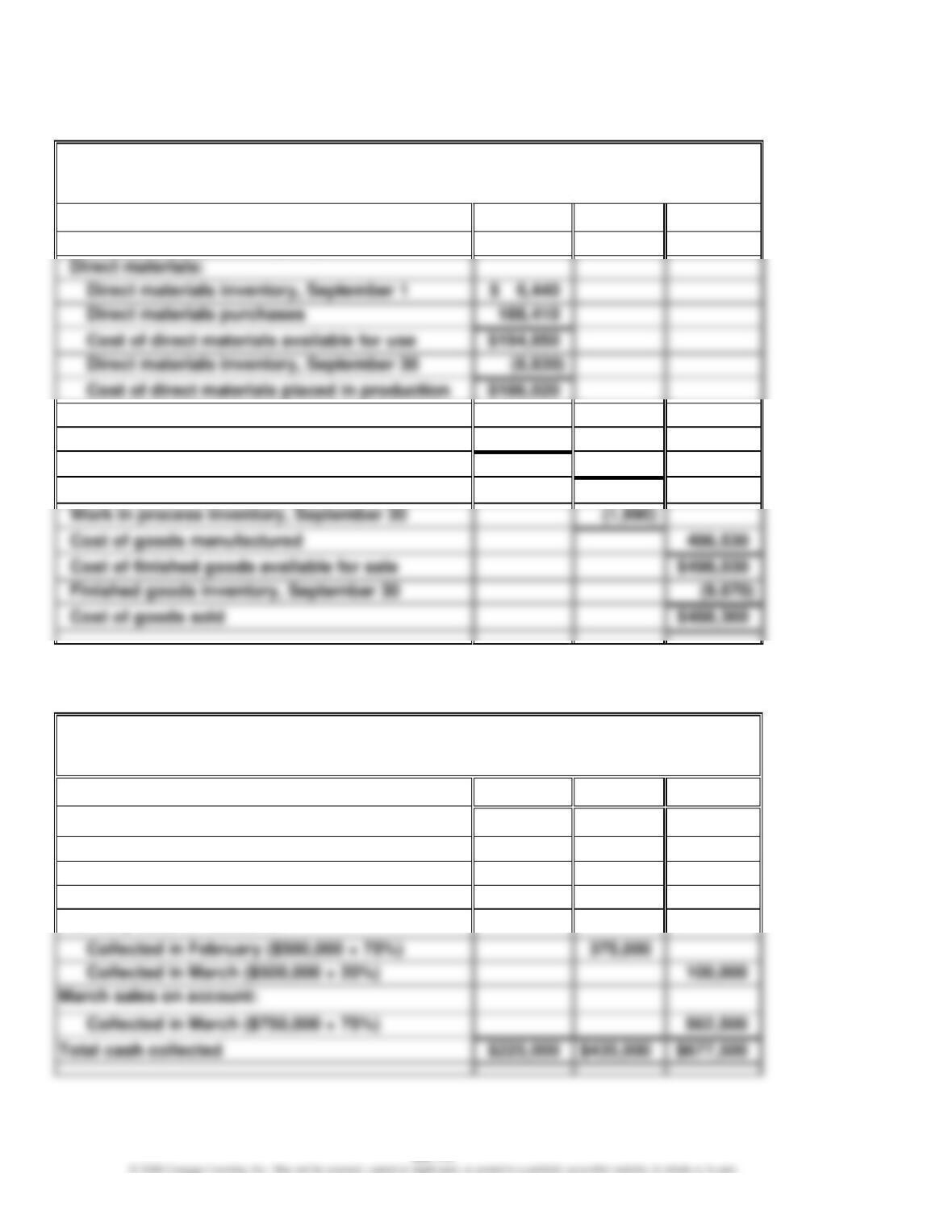

Ex. 22–16 (FIN MAN); Ex. 8–16 (MAN)

MingWare Ceramics Inc.

Cost of Goods Sold Budget

For the Month Ending September 30

Finished goods inventory, September 1

$ 11,500

Work in process inventory, September 1

$ 3,400

Direct materials:

Direct materials inventory, September 1

Direct materials purchases

188,410

Cost of direct materials available for use

Cost of direct materials placed in production

Direct labor

193,600

Factory overhead

105,500

Total manufacturing costs

485,120

Total work in process during the period

$488,520

Cost of goods manufactured

Finished goods inventory, September 30

Ex. 22–17 (FIN MAN); Ex. 8–17 (MAN)

Pet Supplies Inc.

Schedule of Collections from Sales

For the Three Months Ending March 31

January

February

March

January sales on account:

Collected in January ($300,000 × 75%)

$225,000

Collected in February ($300,000 × 20%)

$ 60,000

Collected in March ($300,000 × 5%)

$ 15,000

February sales on account:

Collected in March ($500,000 × 20%)

Collected in March ($750,000 × 75%)

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

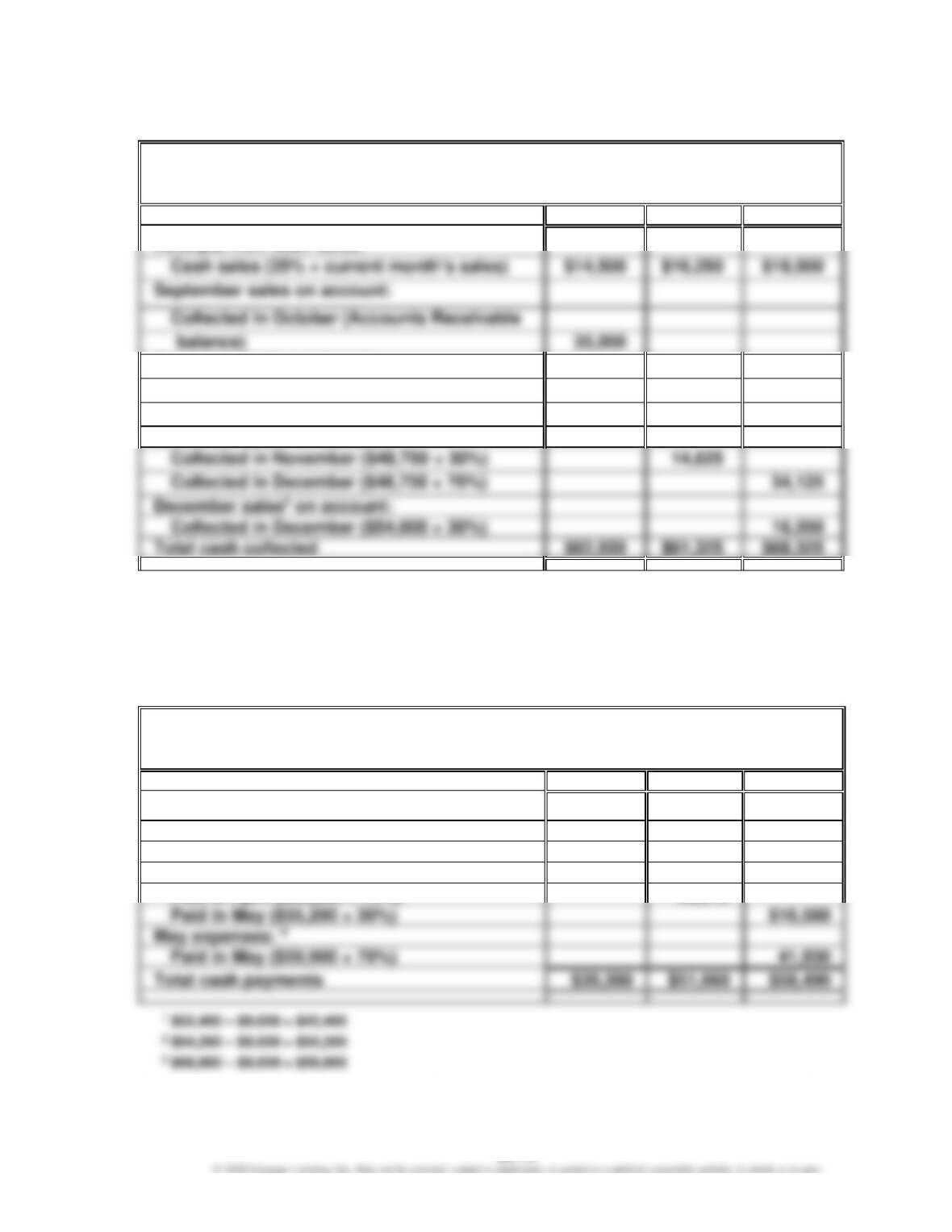

Ex. 22–18 (FIN MAN); Ex. 8–18 (MAN)

OfficeMart Inc.

Schedule of Cash Collections from Sales

For the Three Months Ending December 31

October

November

December

Cash sales (25% × current month’s sales)

Collected in October (Accounts Receivable

October sales1 on account:

Collected in October ($43,500 × 30%)

13,050

Collected in November ($43,500 × 70%)

30,450

November sales2 on account:

Collected in November ($48,750 × 30%)

Collected in December ($48,750 × 70%)

34,125

1 $58,000 × 75% = $43,500

2 $65,000 × 75% = $48,750

3 $72,000 × 75% = $54,000

Ex. 22–19 (FIN MAN); Ex. 8–19 (MAN)

Horizon Financial Inc.

Schedule of Cash Payments for Selling and Administrative Expenses

For the Three Months Ending May 31

March

April

May

March expenses: 1

Paid in March ($43,400 × 70%)

$30,380

Paid in April ($43,400 × 30%)

$13,020

April expenses: 2

Paid in May ($55,200 × 30%)

$16,560

May expenses: 3

Paid in May ($59,900 × 70%)

$30,380

$51,660

$58,490

Note: Insurance, property taxes, and depreciation are expenses that do not result in cash

payments in March, April, or May.

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

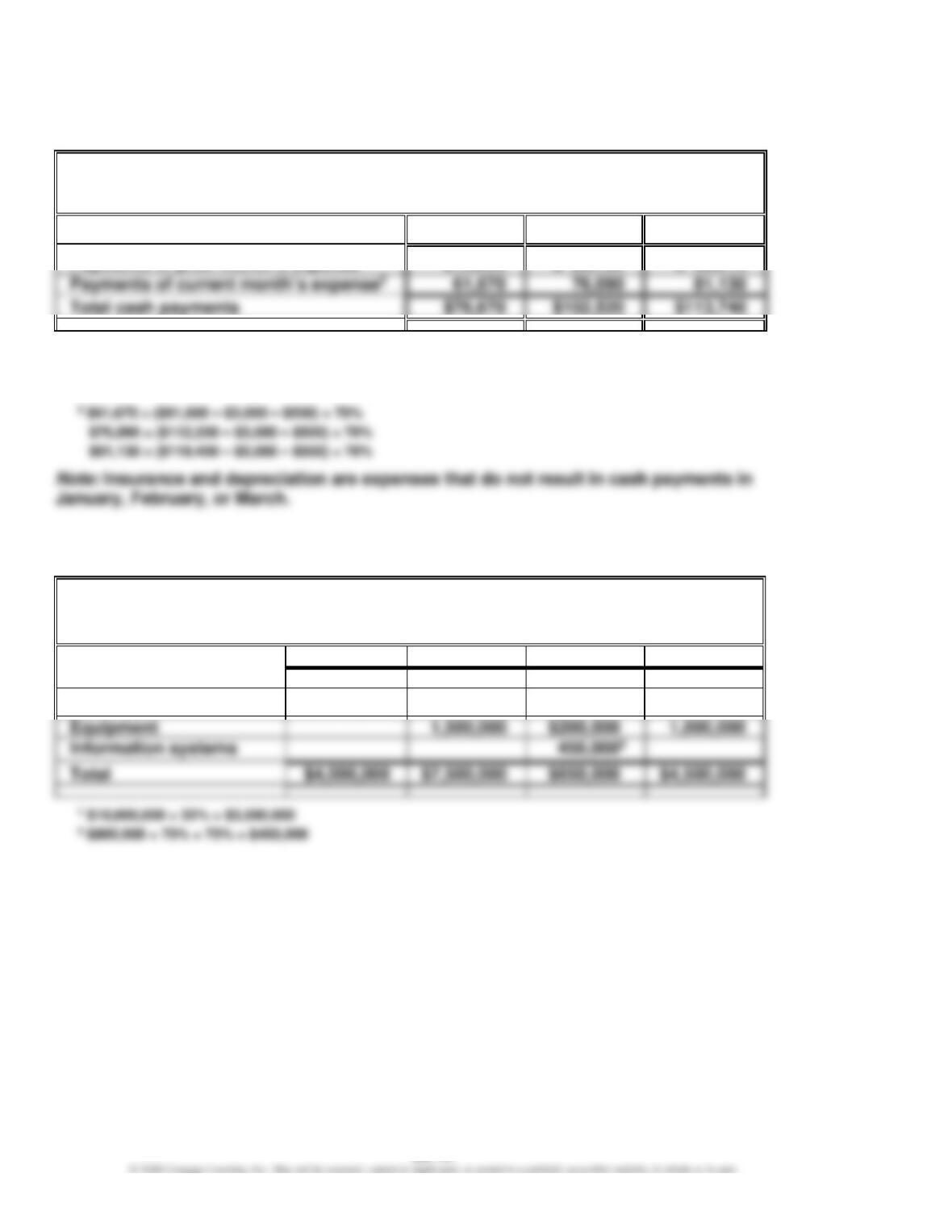

Ex. 22–20 (FIN MAN); Ex. 8–20 (MAN)

EastGate Physical Therapy Inc.

Schedule of Cash Payments for Operations

For the Three Months Ending March 31

January

February

March

1 $15,000, given as Accrued Expenses Payable, January 1

$26,430 = ($91,600 – $3,000 – $500) × 30%

$32,610 = ($112,200 – $3,000 – $500) × 30%

Ex. 22–21 (FIN MAN); Ex. 8–21 (MAN)

Omicron Inc.

Capital Expenditures Budget

For the Four Years Ending December 31, 20Y6–20Y9

20Y6

20Y7

20Y8

20Y9

Building

$4,000,000

$6,000,000

$3,500,0001

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

PROBLEMS

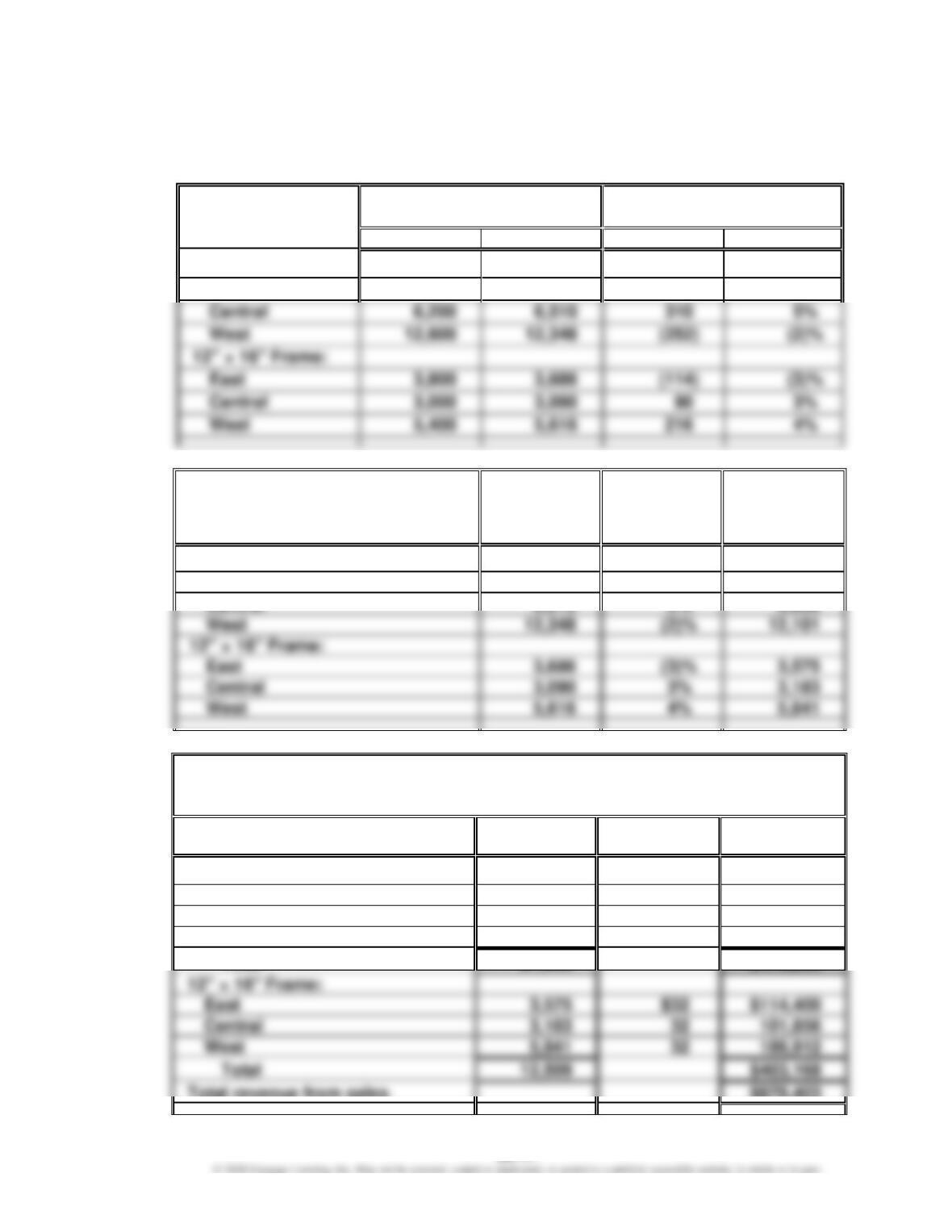

Prob. 22–1A (FIN MAN); Prob. 8–1A (MAN)

1.

Unit Sales, Year Ended 20Y8

Increase (Decrease)

Actual Over Budget

Budget

Actual Sales

Amount

Percent

8″ × 10″ Frame:

East

8,500

8,755

255

3%

Central

6,200

6,510

310

5%

West

12″ × 16″ Frame:

East

3,800

3,686

Central

3,000

3,090

3%

West

5,400

5,616

216

4%

2.

20Y8

Actual

Units

Percentage

Increase

(Decrease)

20Y9

Budgeted

Units

(rounded)

8″ × 10″ Frame:

East

8,755

3%

9,018

West

5,616

4%

5,841

3.

Raphael Frame Company

Sales Budget

For the Year Ending December 31, 20Y9

Product and Area

Unit Sales

Volume

Unit Selling

Price

Total Sales

8″ × 10″ Frame:

East

9,018

$17

$153,306

Central

6,836

17

116,212

West

12,101

17

205,717

27,955

$114,400

West

5,841

32

186,912

Total revenue from sales

$878,403

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

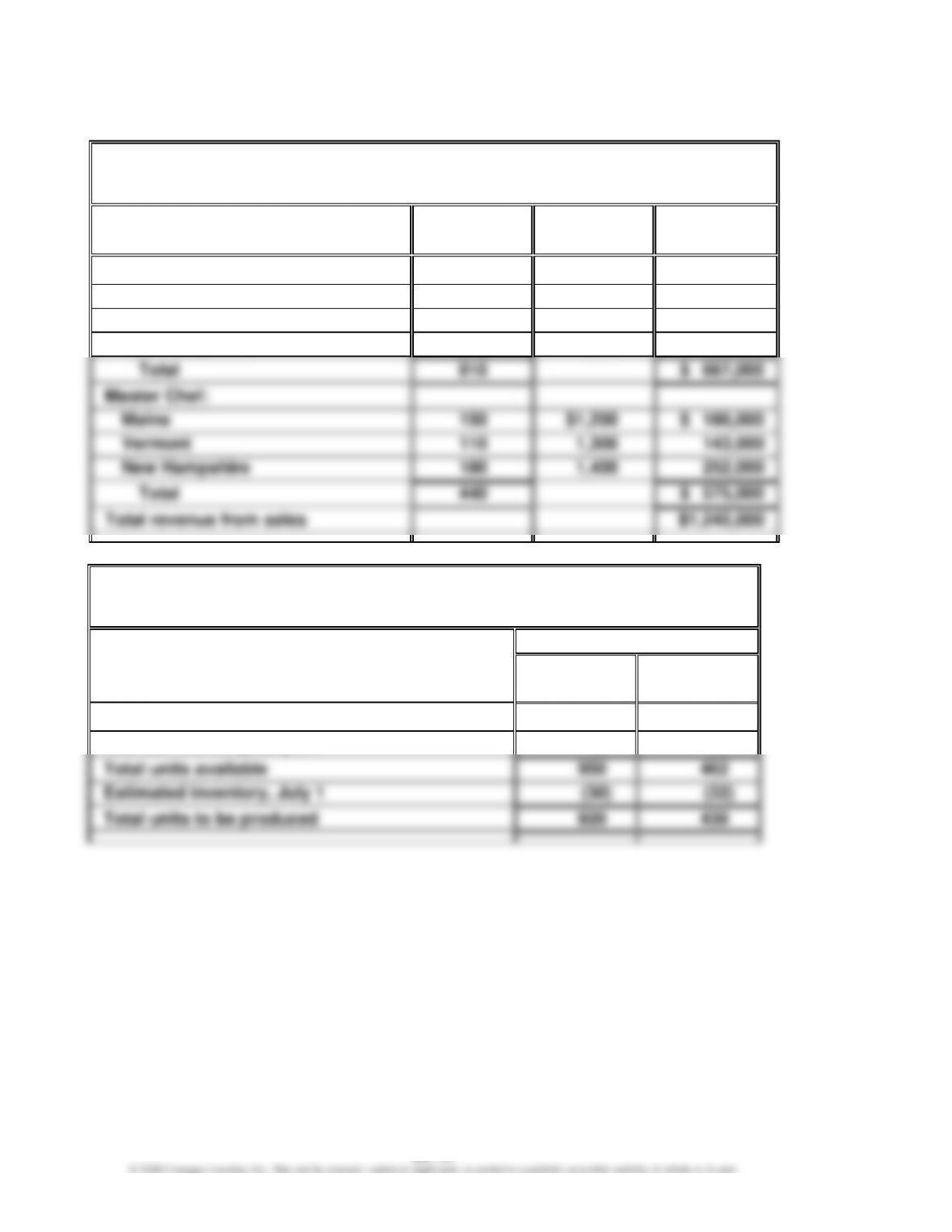

Prob. 22–2A (FIN MAN); Prob. 8–2A (MAN)

1.

Gourmet Grill Company

Sales Budget

For the Month Ending July 31

Product and Area

Unit Sales

Volume

Unit Selling

Price

Total Sales

Backyard Chef:

Maine

310

$ 700

$ 217,000

Vermont

240

750

180,000

New Hampshire

360

750

270,000

Master Chef:

Maine

150

$ 180,000

Vermont

110

143,000

440

$ 575,000

2.

Gourmet Grill Company

Production Budget

For the Month Ending July 31

Units

Backyard

Chef

Master

Chef

Expected units to be sold

910

440

Desired inventory, July 31

40

22

Total units available

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

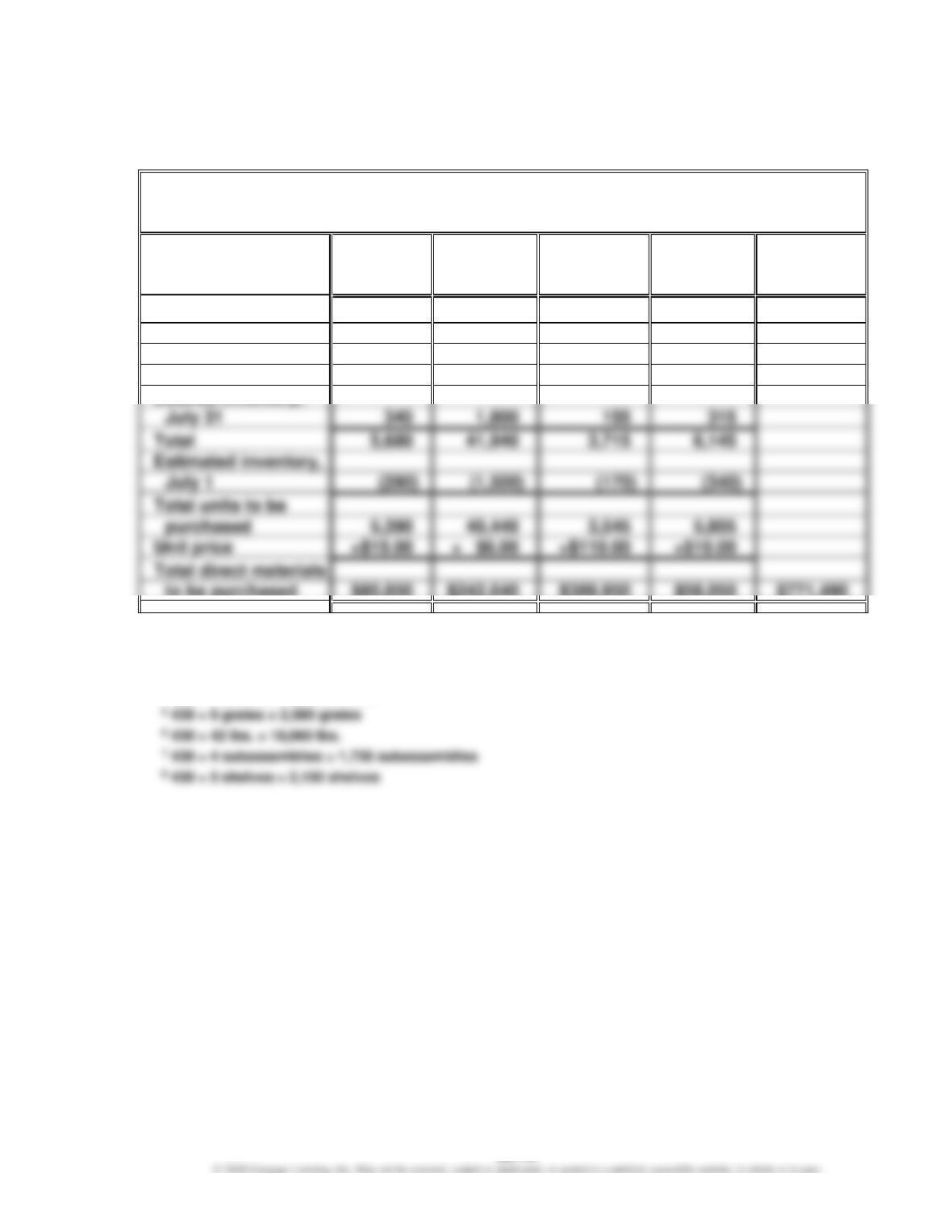

Prob. 22–2A (FIN MAN); Prob. 8–2A (MAN) (Continued)

3.

Gourmet Grill Company

Direct Materials Purchases Budget

For the Month Ending July 31

Grates

(units)

Stainless

Steel

(lbs.)

Burner Sub-

assemblies

(units)

Shelves

(units)

Total

Required units for

production:

Backyard Chef

2,7601

22,0802

1,8403

3,6804

Master Chef

2,5805

18,0606

1,7207

2,1508

July 31

Estimated inventory,

purchased

Unit price

×$15.00

×$110.00

×$10.00

to be purchased

$80,850

$242,640

$389,950

$58,050

$771,490

1 920 × 3 grates = 2,760 grates

2 920 × 24 lbs. = 22,080 lbs.

3 920 × 2 subassemblies = 1,840 subassemblies

4 920 × 4 shelves = 3,680 shelves

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–2A (FIN MAN); Prob. 8–2A (MAN) (Concluded)

4.

Gourmet Grill Company

Direct Labor Cost Budget

For the Month Ending July 31

Stamping

Department

Forming

Department

Assembly

Department

Total

Hours required for production:

Backyard Chef 1

460

552

920

1 This line is calculated as 920 Backyard Chef units from the production budget multiplied

by the hours per unit in each department estimated for the Backyard Chef.

460 = 920 × 0.5; 552 = 920 × 0.6; 920 = 920 × 1.0