Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

8-1

CHAPTER 8

CASH, FRAUD AND INTERNAL CONTROLS

Related Assignment Materials

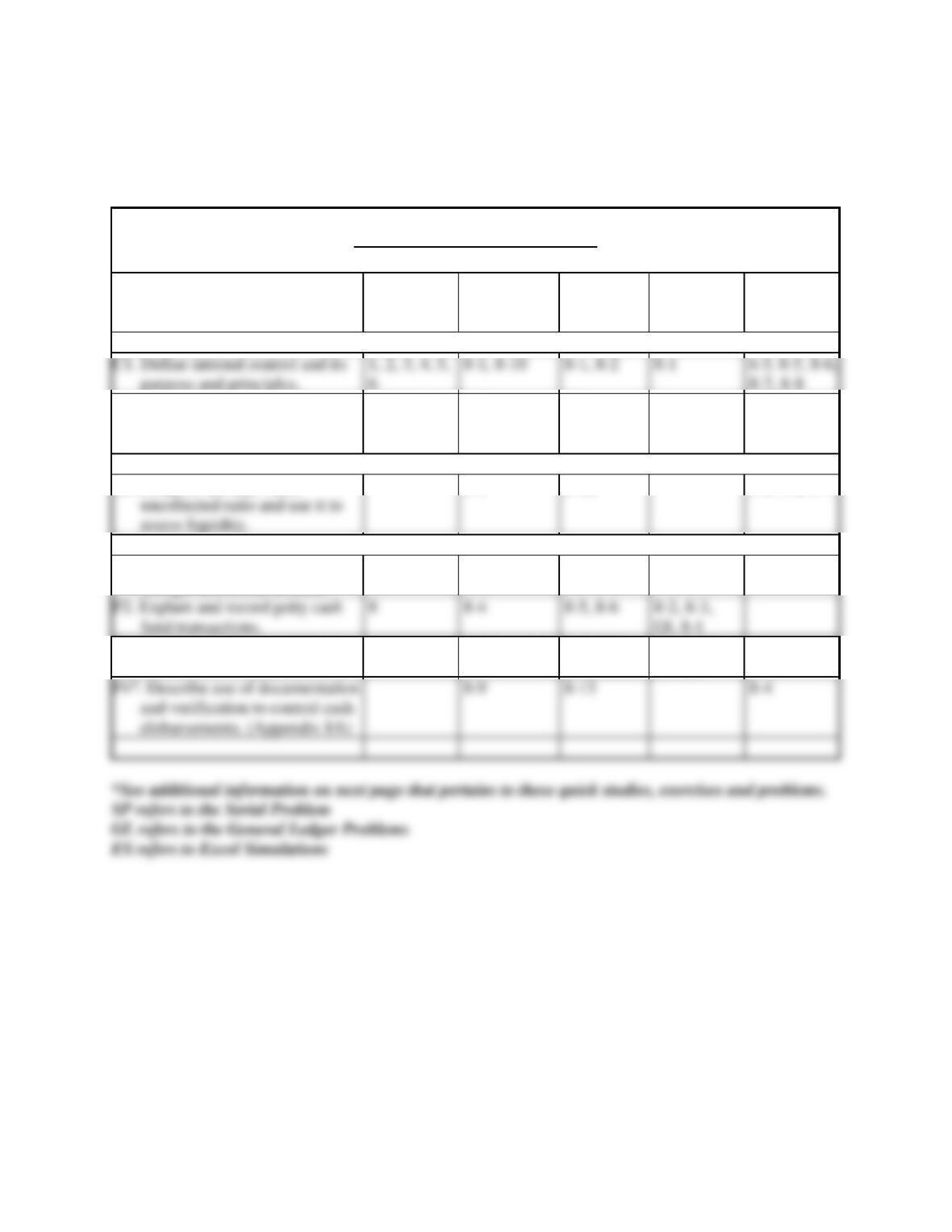

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C2. Define cash and cash

equivalents and explain how to

report them.

7, 10,11, 12,

13

8-2

8-3

8-1, 8-9

Analytical objectives:

uncollected ratio and use it to

assess liquidity.

A1 Compute the days’ sales

8-8

8-12

8-1, 8-2, 8-9

Procedural objectives:

P1. Apply internal control to cash

receipts and disbursements.

9

8-3, 8-10

8-4, 8-7

8-5, 8-7

P2. Explain and record petty cash

fund transactions.

8

8-4

8-5, 8-6

8-2, 8-3,

GL 8-1

P3. Prepare a bank reconciliation.

8-5, 8-6, 8-7

8-8, 8-9,

8-10, 8-11

8-4, 8-5,

SP, ES

and verification to control cash

disbursements. (Appendix 8A)

8-9

8-13

8-4

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

8-2

Additional Information on Related Assignment Material

Connect

Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all Exercises

and Problems Set A. Connect also provides algorithmic versions for Quick Study, Exercises and

Problems. It allows instructors to monitor, promote, and assess student learning. It can be used in

practice, homework, or exam mode.

Connect Insight

The first and only analytics tool of its kind, Connect Insight is a series of visual data displays that are each framed

The Serial Problem for Success Systems continues in this chapter.

General Ledger

Assignable within Connect, General Ledger (GL) problems offer students the ability to see how transactions post

from the general journal all the way through the financial statements. Critical thinking and analysis components are

added to each GL problem to ensure understanding of the entire process. GL problems are auto-graded and provide

instant feedback to the student.

Excel Simulations

Synopsis of Chapter Revisions

NEW opener—Robinhood and entrepreneurial assignment.

New image for certificate of bond coverage.

New discussion of controls over social media with reference to Facebook’s “mood” posts.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

8-3

Chapter Outline

Notes

I. Fraud and Internal Control

A. Purpose of Internal Control

An internal control system consists of policies and procedures

managers use to:

2. Ensure reliable accounting.

4. Uphold company policies.

whose stock is traded on an exchange (called public companies) to

document and certify the system of internal controls.

B. Sarbanes Oxley Act (SOX)

C. Principles of Internal Control:

1. Establish responsibilities.

3. Insure assets and bond key employees.

5. Divide responsibility for related transactions.

7. Perform regular and independent reviews.

D. Technology, Fraud, and Internal Control

Technology allows quick access to information. Examples of how

technology impacts internal control:

1. Reduced processing errors.

2 More extensive testing of records.

4. Separation of duties – must be carefully distributed among

fewer employees.

E. Limitations of Internal Control

2. Cost-benefit principle—the costs of internal controls must not

1. Human Element

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

8-4

Chapter Outline

Notes

II. Control of Cash—Basic guidelines for control of cash and cash

equivalents include: handling of cash must be separate from

recordkeeping of cash, cash receipts are promptly deposited in bank,

and disbursements of cash are by check.

A. Cash, Cash Equivalents, and Liquidity

1. Liquidity refers to a company’s ability to pay for its near term

obligations.

3. Cash equivalent (examples; short-term U.S. Treasury bills and

money market funds) are short-term, highly liquid investment

assets meeting two criteria:

Note: Only investments purchased within three months of

B. Cash Management

1. Goals of Cash Management

2. Effective cash management principles:

a. Encourage collection of receivables

C. Control of Cash Receipts

Procedures for protecting cash received over-the-counter and by

mail:

D. Control of Cash Disbursements – to safeguard against theft:

Use a cash budget to summarize receipts and disbursements.

2. Deny access to the accounting records to anyone, other than

the owner, who has authority to sign checks.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

8-5

Chapter Outline

Notes

3. Voucher system of control establishes procedures for:

a. Verifying, approving and recording obligations for

4. Petty cash system of control:

a. Write and cash a check to establish petty cash fund.

Record as a debit to Petty Cash and credit to Cash.

(Use the Petty Cash account only when the fund is

established or size of fund is increased or decreased.)

III. Banking Activities as Controls

A. Basic Bank Services

Bank accounts permit depositing money for safeguarding and

helps control withdrawals. Electronic Funds Transfer (EFT) is an

electronic communication transfer of cash from one party to

another.

B. Bank Statement

Shows activities of a bank account and is used to prove the

accuracy of the depositor’s cash records in preparing a bank

reconciliation.

1. Bank reconciliation –a report that explains (reconciles) the

2. Factors causing the bank statement balance to differ from the

depositor’s book balance are:

recorded obligations.

appendix notes)

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

8-6

Chapter Outline

Notes

3. Steps in preparing the bank reconciliation:

a. Identify the bank balance of the cash account (balance per

bank).

b. Identify and list any unrecorded deposits (deposits in

transit) and any bank errors understating the bank balance.

4. Adjusting entries from a bank reconciliation

a. All reconciling additions to book balance are debits to

cash. Credit depends on reason for addition (Examples:

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

8-7

Chapter Outline

Notes

IV. Decision Analysis—Days’ Sales Uncollected

A. Also called days’ sales in receivables.

V. Documents and Verification —Appendix 8A

Important documents of a voucher system of control include:

A. Purchase Requisition—lists the merchandise needed and requests

that it be purchased.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

8-8

VISUAL #8-1

BANK RECONCILIATION

Reasons for discrepancies between

bank statement balance and checkbook

balance: Handle as follows:

Unrecorded deposits Add to Bank Balance

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

8-9

Chapter 8 Alternate Demonstration Problem

The Betsy Dough Company wants to prepare a bank reconciliation for the

month of June. When the bank statement for the month of June arrives

from the bank, the following steps are performed:

1. The deposits to the bank account, as recorded on the bank statement,

are compared to the deposit slips retained by the company. It is noted

2. Checks returned with the bank statement are compared to the checks

3. The ending balances on the statement and in the company’s books are

4. Other information contained on the bank statement, not previously

known to the company, is determined. This includes the following: (a) a

5. A bank reconciliation is prepared; it does not balance! The difference is

$18, so a transposition error is looked for (whenever the difference is a

multiple of 9, there is a very good chance that there has been an

Required:

Prepare a bank reconciliation for the Betsy Dough Company at June 30,

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

8-10

Chapter 8 Solution: Alternate Demonstration Problem

BETSY DOUGH COMPANY

Bank Reconciliation

June 30, 2018

Bank Statement

Bank statement balance ………………………………………

$10,129

Depositor’s Books

Book balance of cash ………………………………………….

$ 9,000

Add:

Deduct:

NSF check from Frank Ony …………………………

Bank service charges …………………………………

$ 9,073

Adjusting entries Based on the Bank Reconciliation (made by depositor)

Cash………………………………………………………………. 218

Add:

Deduct:

$ 9,073