8-34

PROBLEM 8-40 (40 MINUTES)

1.

The factors that should be present for an organization’s quality program to be

successful include the following:

• Training of those involved, including employees and suppliers.

2.

From an analysis of the cost-of-quality report, the program appears to have been

successful, because of the following:

• Total quality cost has declined from 23.4 to 13.1 percent of total production costs.

• External failure costs, those costs signaling customer dissatisfaction, have

8-35

PROBLEM 8-40 (CONTINUED)

3.

Tony Reese’s current reaction to the quality improvement program is more favorable

because he is seeing the benefits of having the quality problems investigated and

4.

To measure the opportunity cost of not implementing the quality program,

management could do the following:

PROBLEM 8-41 (60 to 180 MINUTES)

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-36

SOLUTION TO CASES

CASE 8-42 (35 MINUTES)

1. Absorption-costing operating income statements:

Year 1

Year 2

Sales revenue ……………………………………………………………………………..

$62,500

a

$62,500

d

Less: Cost of goods sold:

Beginning finished-goods inventory …………………………..

$ 0

$ 5,250

e

Cost of goods manufactured …………………………………………….

b

f

Cost of goods available for sale ………………………………………..

$31,500

$33,250

Ending finished-goods inventory ………………………………………

5,250

c

Cost of goods sold ……………………………………………………….

$26,250

$33,250

Gross margin ……………………………………………………………………………..

$36,250

$29,250

Selling and administrative expenses ……………………………………………

Operating income ……………………………………………………………………….

$13,750

$ 6,750

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-37

CASE 8-42 (CONTINUED)

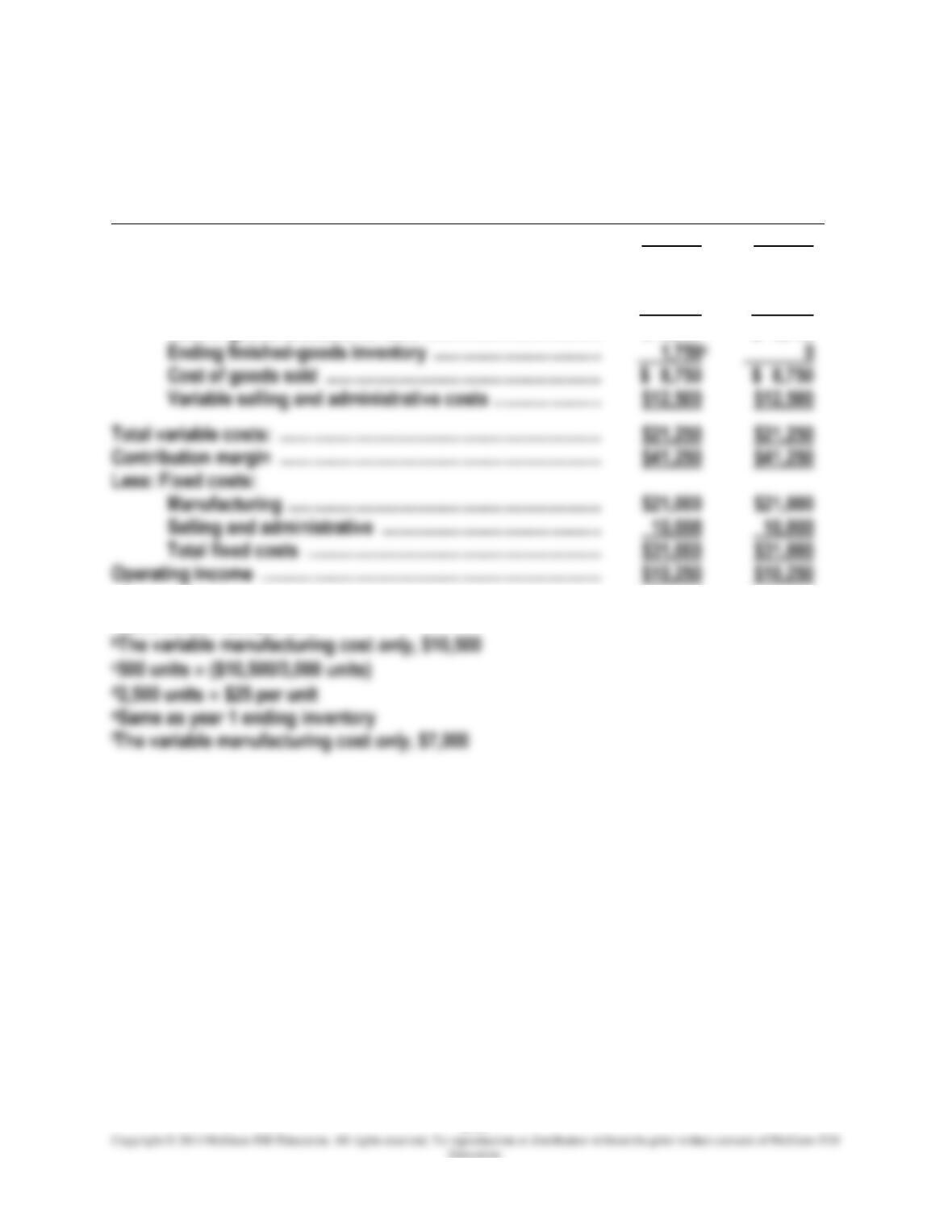

2. Variable-costing operating income statements:

Year 1

Year 2

Sales revenue ……………………………………………………………………………..

$62,500

a

$62,500

d

Less: Cost of goods sold:

Beginning finished-goods inventory …………………………..

$ 0

$ 1,750

e

Cost of goods manufactured …………………………………………….

10,500

b

7,000

f

Cost of goods available for sale ………………………………………..

$10,500

$ 8,750

Ending finished-goods inventory ………………………………………

c

Cost of goods sold ……………………………………………………….

$ 8,750

$ 8,750

Variable selling and administrative costs …………………………..

$12,500

$12,500

Total variable costs: ……………………………………………………………………

$21,250

$21,250

Contribution margin ……………………………………………………………………

$41,250

$41,250

Less: Fixed costs:

Manufacturing ……………………………………………………….…………

$21,000

$21,000

Selling and administrative ………………………………………………..

Total fixed costs ……………………………………………………….

$31,000

$31,000

Operating income ……………………………………………………………………….

$10,250

$10,250

a2,500 units $25 per unit

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-38

CASE 8-42 (CONTINUED)

3. Reconciliation of reported operating income under absorption and variable costing:

Year

Change in

Inventory

(in units)

Actual

Fixed-

Overhead

Rate

Difference in

Fixed

Overhead

Expensed

Absorption-

Minus Variable-

Costing

Op’g Income

1

500 increase

$7

$ 3,500

$3,500

Explanation: At the end of year 1, under absorption costing, $3,500 of fixed overhead

remained stored in finished-goods inventory as a product cost (year 1 fixed-overhead rate

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-39

CASE 8-43 (30 MINUTES)

1. Reconciliation of reported operating income:

Year 1

Absorption Costing

Operating Income

Statement

Variable Costing

Operating Income

Statement

Cost of goods sold ……………………………………

$26,250

$8,750

Fixed cost (expensed as period expense) ……

Total …………………………………………………………

$36,250

$39,750

Reported operating income ……………………….

$13,750

$10,250

Year 2

Absorption Costing

Operating Income

Statement

Variable Costing

Operating Income

Statement

Cost of goods sold ……………………………………

$33,250

$ 8,750

Fixed cost (expensed as period expense) ……

Total …………………………………………………………

$43,250

$39,750

Reported operating income ……………………….

$ 6,750

$10,250

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-40

CASE 8-43 (CONTINUED)

2. Total operating income across both years:

3. Total sales revenue across both years:

4. Total of all costs expensed across both years:

5. Total sales revenue minus total costs expensed across both years.

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-41

CASE 8-43 (CONTINUED)

6. The total sales revenue across both of Huron’s first two years of operation is the

same under absorption and variable costing, $125,000, as shown in requirement (3).

Sales revenue has nothing to do with the costing method used. Huron sold 5,000

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-42

CASE 8-44 (40 MINUTES)

1. At the end of year 1, Huron has 500 units in its finished-goods inventory (production

minus sales). The year-end balance in finished-goods inventory is higher under

2. At the end of year 2, Huron has no finished-goods inventory on hand. The two-year

3. Yes, this relationship will be true at any balance sheet date. For any balance sheet

date when the company has nonzero finished-goods inventory, the cost of that

4.

Finished-Goods Inventory

End of Year 1

End of Year 2

Amount of

Decline

Absorption costing …………………………..

Variable costing ……………………………………………………….

5.

Amount of Decline in Finished-

Goods Inventory Balance During Year 2

Absorption costing ……………………………………………………….

$5,250

Variable costing ……………………………………………………….

Difference …………………………………………………………………………………..

$3,500

Reported Operating Income for Year 2

Absorption costing ……………………………………………………….

$ 6,750

Variable costing ……………………………………………………….

Difference …………………………………………………………………………………..

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

CASE 8-44 (CONTINUED)

Reported operating income for year 2 is $3,500 lower under absorption costing. This

amount matches the difference in the amount by which the year-end finished-goods

6. Yes, this relationship will always hold true at any balance sheet date. There are two

ways to think about this issue.

(a) As explained in the text, during any time period during which the amount of

inventory increases (i.e., unit production exceeds unit sales), income reported

8-44

CASE 8-44 (CONTINUED)

The following diagram may help in understanding the foregoing explanation.

(b) Another way to explain the answer to this question involves the basic accounting

equation, which follows.

Entire life of the enterprise

up to the current time

Time

Inventory is

either some

decrease, depending

on the relationship

•

•

•

•

•

•

•

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-45

CASE 8-44 (CONTINUED)

The only elements in the accounting equation that are affected by the choice of absorption

Chapter 08 – Variable Costing and the Costs of Quality and Sustainability

8-46

FOCUS ON ETHICS (See pages 336-337 in the text.)

It is often asserted that absorption costing results in an incentive for managers to

overproduce inventory, even during a period of slack demand, in order to boost income.

This scenario is just such an example.

The year 1 and year 2 income statements presented in the text for Brandolino Company are

prepared under absorption costing. While sales revenue, direct manufacturing costs, and

Sales (10,000,000 units at $6)………………………. $ 60,000,000

Less: Cost of goods sold (10,000,000 at $2)……. (20,000,000)

What has happened in this company? Brandolino’s new president, taking advantage of the