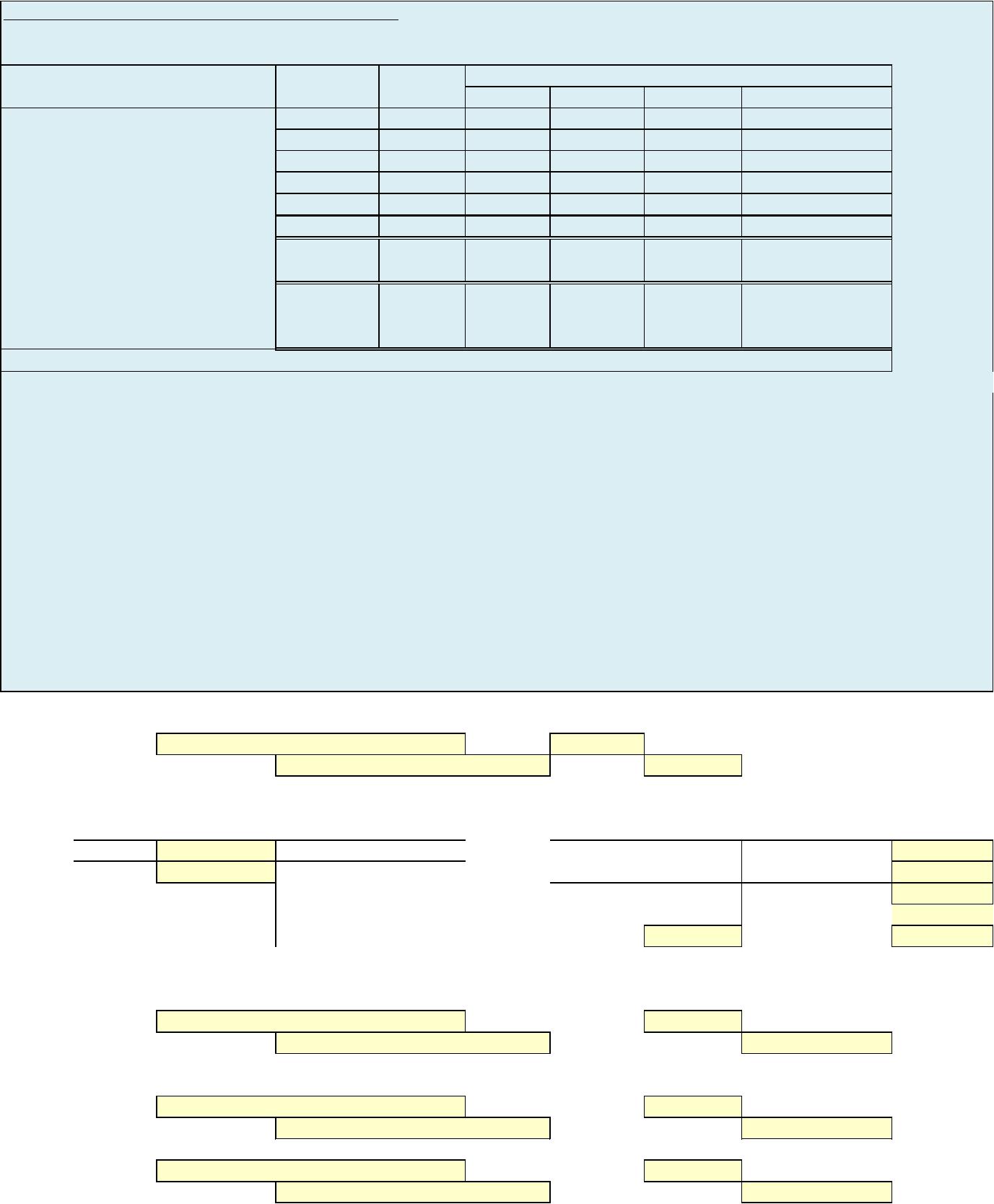

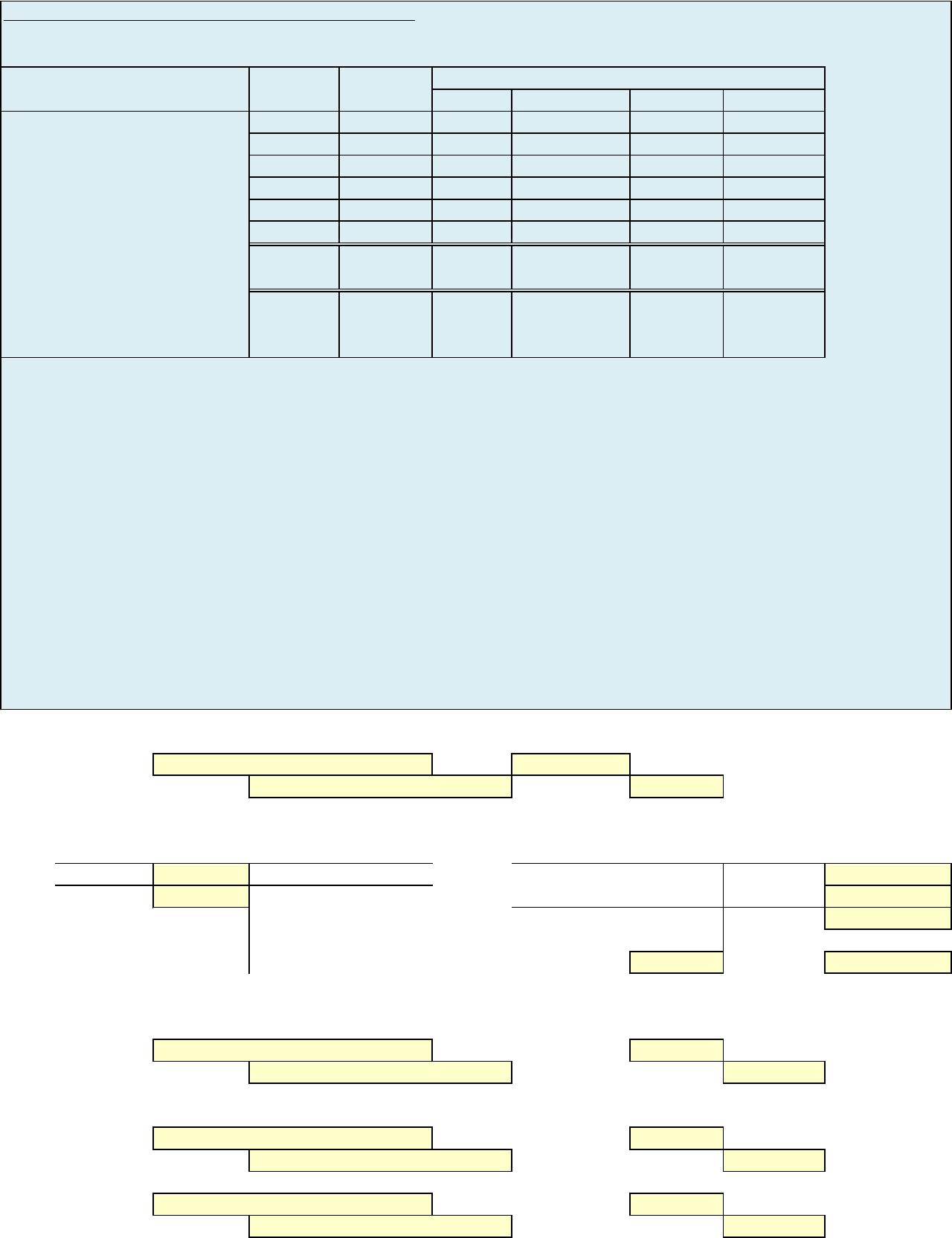

P8-3A Journalize transactions related to bad debts

Presented below is an aging schedule for Bryan Company.

Not Yet

Total Due 1-30 31-60 61-90 Over 90

Aneesh $24,000 $9,000 $15,000

Bird 30,000 $30,000

Cope 50,000 5,000 5,000 $40,000

DeSpears 38,000 38,000

Others 120,000 72,000 35,000 13,000

$262,000 $107,000 $49,000 $28,000 $40,000 $38,000

Estimated percentage

uncollectible 3% 7% 12% 24% 60%

Total estimated

bad debts $42,400 $3,210 $3,430 $3,360 $9,600 $22,800

At December 31, 2016, the unadjusted balance in Allowance for Doubtful Accounts us a

credit of $8,000.

Instructions

(a) Journalize and post the adjusting entry for bad debts at December 31, 2016. (use

T-accounts.)

(b) Journalize and post to the allowance account these 2017 events and transactions.

1. March 1, a $600 customer balance originating in 2016 is judged uncollectible.

2. May 1, a check for $600 is received from the customer whose account was written

off as uncollectible on March 1.

(c ) Journalize the adjusting entry for bad debts at December 31, 2017, assuming that the

unadjusted balance in Allowance for Doubtful Accounts is a debit of $1,400 and the

aging schedule indicates that total estimated bad debts will be $36,700.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a) Dec 31 Value

Value

(a) & (b)

12/31 Value 2016 12/31 Bal. Value

12/31 Bal. ? 12/31 Value

12/31 Bal. ?

2017

3/1 Value 6/1 Value

(b)(1) Mar. 1 Value

Value

(b)(2) May 1 Value

Value

1 Value

Value

Number of Days Past Due

Customer

Bad Debt Expense

Allowance for Doubtful Accounts

Account

2017

Account

Account

Account

Account

Account

Account

Account

(c ) Dec 31 Value

Value

After you have completed P8-3A, consider the following additional question.

1. Assume that the unadjusted balance in the Allowance for Doubtful Accounts on December 31, 2017

was a credit balance of $1,950 and the aging schedule indicate that total estimated bad debts will be

$37,500. What is the adjusting entry for bad debts on December 31, 2017?

2017

Account

Account

Allowance for Doubtful Accounts

Accounts Receivable

2017

Bad Debt Expense

P8-3A Solution

(a) Dec 31 34,400

(a) & (b)

(b)(1) Mar. 1 600

600

Bad Debt Expense

Bad Debt Expense

Allowance for Doubtful Accounts

2017

Allowance for Doubtful Accounts

Accounts Receivable

Allowance for Doubtful Accounts

1. Assume that the unadjusted balance in the Allowance for Doubtful Accounts on December 31, 2017

was a credit balance of $1,950 and the aging schedule indicate that total estimated bad debts will be

$37,500. What is the adjusting entry for bad debts on December 31, 2017?

(a) Dec 31 34,400

Bad Debt Expense

Allowance for Doubtful Accounts

Accounts Receivable

Allowance for Doubtful Accounts

Accounts Receivable

2017

(a) & (b)

12/31 34,400 2016 12/31 Bal. 8,000

12/31 Bal. 34,400 12/31 34,400

(b)(1) Mar. 1 600

600

Allowance for Doubtful Accounts

Bad Debt Expense

Bad Debt Expense

Allowance for Doubtful Accounts

2017

Accounts Receivable

P8-3B Journalize transactions related to bad debts

Presented below is an aging schedule for Harper Company.

Not Yet

Total Due 1-30 31-60 61-90 Over 90

Allen $18,000 $12,000 $6,000

Brian 24,000 $24,000

Charles 40,000 $25,000 15,000

Dwight 52,000 52,000

Others 196,000 97,000 60,000 39,000

$330,000 $122,000 $87,000 $45,000 $24,000 $52,000

Estimated percentage

uncollectible 1% 3% 9% 20% 40%

Total estimated

bad debts $33,480 $1,220 $2,610 $4,050 $4,800 $20,800

At December 31, 2013, the unadjusted balance in Allowance for Doubtful Accounts us a

credit of $9,000.

Instructions

(a) Journalize and post the adjusting entry for bad debts at December 31, 2013. (use

T-accounts.)

(b) Journalize and post to the allowance account these 2014 events and transactions.

1. February 1, a $900 customer balance originating in 2013 is judged uncollectible.

2. July 1, a check for $900 is received from the customer whose account was written

off as uncollectible on February 1.

(c ) Journalize the adjusting entry for bad debts at December 31, 2014, assuming that the

unadjusted balance in Allowance for Doubtful Accounts is a debit of $2,800 and the

aging schedule indicates that total estimated bad debts will be $30,600.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a) Dec 31 Account Value

Account Value

(a) & (b)

12/31 Value 2013 12/31 Bal. Value

12/31 Bal. ? 12/31 Value

12/31 Bal. ?

2014

2/1 Value 7/1 Value

(b)(1) Feb.. 1 Value

Value

(b)(2) July 1 Value

Value

1 Value

Value

Customer

Number of Days Past Due

Bad Debt Expense

Allowance for Doubtful Accounts

2014

Account

Account

Account

Account

Account

Account

(c ) Dec 31 Value

Value

After you have completed P8-3B, consider the following additional question.

1. Assume that the amount judged uncollected changed to $1,250 and that the customer sent in a check for $650

on July 1. Also assume that on December 31, the Allowance for Doubtful Accounts had a debit balance of $3,500

and the aging schedule estimated that total estimated bad debts will be $36,500. Show the impact of these changes

on the appropriate journal entries.

2014

Account

Account

Allowance for Doubtful Accounts

Accounts Receivable

Allowance for Doubtful Accounts

Accounts Receivable

Bad Debt Expense

P8-3B Solution

(a) Dec 31 Bad Debt Expense 24,480

(a) & (b)

12/31 24,480 2013 12/31 Bal. 9,000

(b)(1) Feb. 1 900

900

Bad Debt Expense

Allowance for Doubtful Accounts

2014

Allowance for Doubtful Accounts

Accounts Receivable

P8-3B Solution to additional question

1. Assume that the amount judged uncollected changed to $1,250 and that the customer sent in a check for $650

on July 1. Also assume that on December 31, the Allowance for Doubtful Accounts had a debit balance of $3,500

and the aging schedule estimated that total estimated bad debts will be $36,500. Show the impact of these changes

on the appropriate journal entries.

(a) Dec 31 Bad Debt Expense 24,480

(a) & (b)

12/31 24,480 2013

12/31 Bal.

9,000

12/31 Bal.

12/31 Bal.

Allowance for Doubtful Accounts

Accounts Receivable

2014

(b)(1) Feb. 1 1,250

1,250

Bad Debt Expense

Allowance for Doubtful Accounts

2014

Allowance for Doubtful Accounts

Accounts Receivable