8–1

Chapter 8

Process Costing

Learning Objectives

1. Explain the concept and purpose of equivalent units.

2. Assign costs to products using a five-step process.

3. Assign costs to products using weighted-average costing.

4. Prepare and analyze a production cost report.

5. Assign costs to products using first-in, first-out (FIFO) costing.

6. Analyze the accounting choice between FIFO and weighted-average costing.

7. Know when to use process or job costing.

8. Compare and contrast operation costing with job costing and process costing.

Chapter Overview

I. DETERMINING EQUIVALENT UNITS

II. USING PRODUCT COSTING IN A PROCESS INDUSTRY

• Step 1: Measure the Physical Flow of Resources

• Step 2: Compute the Equivalent Units of Production

• Step 3: Identify the Product Costs for Which to Account

III. REPORTING THIS INFORMATION TO MANAGERS: THE PRODUCTION COST

REPORT

• Sections 1 and 2: Managing the Physical Flow of Units

• Sections 3, 4, and 5: Managing Costs

IV. ASSIGNING COSTS USING FIRST-IN, FIRST-OUT (FIFO) PROCESS COSTING

• Step 1: Measure the Physical Flow of Resources

• Step 2: Compute the Equivalent Units of Production

• Step 3: Identify the Product Costs for Which to Account

• Step 4: Compute the Costs per Equivalent Unit: FIFO

• Step 5: Assign Product Cost: FIFO

• How this Looks in T-Accounts

V. DETERMINING WHICH IS BETTER: FIFO OR WEIGHTED AVERAGE?

VI. COMPUTING PRODUCT COSTS: SUMMARY OF THE STEPS

VII. USING COSTS TRANSFERRED IN FROM PRIOR DEPARTMENTS

• Who Is Responsible for Costs Transferred in From Prior Departments?

VIII. CHOOSING BETWEEN JOB AND PROCESS COSTING

IX. OPERATION COSTING

• Product Costing in Operations

• Operation Costing Illustration

X. COMPARING JOB, PROCESS, AND OPERATION COSTING

8–3

Chapter Outline

LO 8-1 Explain the concept and purpose of equivalent units.

• In job costing, each job is considered unique and can (but might not) follow the same path

through the production as other jobs. Processing costing assumes that all units are

homogeneous and follow the same path through the production processes.

DETERMINING EQUIVALENT UNITS

• Equivalent units (EU) represent the number of complete physical units to which units in

inventories are equal in terms of work done to date.

o Equivalent units = Number of physical units × Estimated (average) percentage of

completion with respect to the individual resource.

o Exhibit 8.2 illustrates the equivalent unit concept.

8–4

LO 8-2 Assign costs to products using a five-step process.

USING PRODUCT COSTING IN A PROCESS INDUSTRY

• Five-step process of assigning costs to products:

o Measure the physical flow of resources.

o Compute the equivalent units of production.

o Identify the product costs for which to account.

o Compute the costs per equivalent unit.

o Assign product cost to batches of work.

o The physical flow of resources in the Compounding Department of Torrance Tape, Inc.

(2T) for the month of March, Year 2 is provided in Exhibit 8.3.

• Step 1: Measure the Physical Flow of Resources

o The inventory equation (see Chapter 6) can be adapted to ensure that the work done has

been properly accounted for. That is,

Beginning work-in–

process inventory

+

Unit

started

=

Units

transferred out

+

Ending work-in–

process inventory

▪ Another way to look at the inventory equation is via the following statement format:

▪ A third way to study the inventory equation is through the T-account:

Work-in-Process Inventory

Beginning balance

Plus: Units started

Less: Units transferred out

Ending balance

o The production process for 2T is shown in Exhibit 8.4.

Beginning work-in-process inventory

xxx

Plus: Units started

xxx

Total units to account for

xxx

Units transferred out

xxx

Plus: Ending work-in-process inventory

xxx

Total units accounted for

xxx

8–5

• Step 2: Compute the Equivalent Units of Production

o In cases where materials are added at the beginning of the production process, while

labor and overhead (conversion resources) are added continuously throughout the process,

the calculation of equivalent units has to be done separately for each resource (materials

and conversion) introduced during the process.

o The computation of equivalent units in 2T’s Compounding Department is shown in

Exhibit 8.4. (See Business Application box “Overstating Equivalent Units to Commit

Fraud.”)

▪ Materials

• Because all materials are added at the beginning of the production process, the

equivalents units are calculated as follows:

▪ Conversion

• Because labor and overhead (conversion resources) are added continuously

throughout the process, the equivalents units are calculated as follows::

Equivalent units = Number of units transferred out + (Units in work in process at

the end of the month x Percent compete with respect to conversion)

• Step 3: Identify the Product Costs for Which to Account

o The costs collected include not only those incurred for production but also those in the

beginning work-in-process inventory. The work that has been done comes from two

sources:

• Time Out! We Need to Make an Assumption About Costs and the Work-In-Process

Inventory

o There are two approaches available for product costing purposes.

▪ Weighted-average process costing is an inventory method that combines costs and

equivalent units of a period with the costs and the equivalent units in beginning

inventory from the last period.

▪ First-in, first-out (FIFO) process costing is an inventory method whereby the first

goods received are the first ones charged out when sold or transferred.

• The FIFO method separates the costs of the current work and the work in the

beginning work-in-process inventory, assuming that all beginning work-in–

process units are transferred out first.

LO 8-3 Assign costs to products using weighted-average costing.

• Step 4: Compute the Costs per Equivalent Unit: Weighted Average

o Exhibit 8.8 illustrates the calculation of the equivalent unit cost for materials and for

conversion using the weighted-average method.

• Step 5: Assign Product Cost to Batches of Work: Weighted-Average Process Costing

o Once the costs per equivalent unit are computed, the final step is to assign the total costs

to the two batches of work: the units transferred out and the units not complete.

▪ The total costs to account for must equal the total costs accounted for.

Costs in Beginning work in process inventory

$xxx

Plus: Current period costs

xxx

Total costs to account for

$xxx

Costs assigned to units transferred out

$xxx

Plus: Costs assigned to ending work in process inventory

xxx

Total costs accounted for

$xxx

Beginning balance

Plus: Current period costs

Less: Cost of units transferred out

Ending balance

o Recording the Cost Flows in T-Accounts

▪ Exhibit 8.10 shows the flow of costs through the T-accounts. A general format for the

work-in-process inventory account follows.

See Demonstration Problem 1

8–8

LO 8-4 Prepare and analyze a production cost report.

REPORTING THIS INFORMATION TO MANAGERS: THE PRODUCTION COST

REPORT

• A production cost report summarizes production and cost results for a period and is

generally used by managers to monitor production and cost flows.

o As illustrated in Exhibit 8.11, the report is presented in five sections, each of which

corresponds to a step for assigning costs to goods transferred out and to ending work–in–

process inventory.

▪ Section 1 summarizes the flow of physical units.

▪ Section 2 shows the equivalent unit calculation.

• Sections 1 and 2: Managing the Physical Flow of Units

o Sections 1 and 2 of the production cost report correspond to steps 1 and 2 of the cost flow

model.

LO 8-5 Assign costs to products using first-in, first-out (FIFO) costing.

ASSIGNING COSTS USING FIRST-IN, FIRST-OUT (FIFO) PROCESS COSTING

• A disadvantage of the weighted-average method is that it mixes current period costs with the

costs of products from the last period in the beginning inventory, making it impossible for

managers to know how much it cost to make a product this period.

8–9

o The FIFO method separates current period costs from those in the beginning inventory.

o The FIFO method gives managers better information about the work done in the current

period.

• If the production process is a FIFO process, the inventory numbers are more likely to reflect

reality under FIFO costing than under weighted-average costing because the units in ending

work-in-process inventory are likely to have been produced in the current period.

o Computing product costs using a FIFO process costing system requires the same five-step

procedure as the weighted-average approach.

▪ Step 1: Measure the physical flow of resources.

• Step 1: Measure the Physical Flow of Resources

o The choice of accounting for production costs does not change the physical flow of

production. But the number of units completed and transferred out can be separated into

two groups: those that came from the beginning work-in-process inventory and those that

• Step 2: Compute the Equivalent Units of Production

o The FIFO equivalent unit computation is confined only to what was produced this period.

Under FIFO, equivalent units are computed in three parts for each distinct resource:

8–10

• Example 2: There are 200 units in the beginning work-in-process inventory, 40

percent complete with respect to materials, labor, and overhead. In the current

period, additional 4,800 units are started. After transferring out 4,500 completed

units, the factory is left with 500 units in the ending work-in-process inventory,

25 percent complete with respect to materials, labor, and overhead.

If the FIFO method is adopted, it can be determined that 4,300 units (= 4,500

units – 200 units) are started and completed during the current period.

The equivalent units can be calculated as follows:

Physical

Units

Equivalent units

Materials, Labor, Overhead

To complete beginning inventory

200

120

o The equivalent units under FIFO are less than or equal to those under the weighted-

average method because the FIFO computations refer to the current period’s production

only; weighted-average equivalent units consider all units in the department, whether

produced this period or in the previous period.

• Step 3: Identify the Product Costs for Which to Account

• Step 4: Compute the Costs per Equivalent Unit: FIFO

o Under FIFO, the costs per equivalent unit are confined to the costs incurred this period

and the equivalent units produced this period. That is,

Units started and completed (100%)

Work in ending inventory (25%)

500

125

8–11

See Demonstration Problem 2

LO 8-6 Analyze the accounting choice between FIFO and weighted-average

costing.

DETERMINING WHICH IS BETTER: FIFO OR WEIGHTED AVERAGE?

• Weighted-average costing does not separate beginning inventory from current period activity.

Unit costs are a weighted average of the two, whereas FIFO costing bases unit costs on

current period activity only.

• Exhibit 8.14 compares the unit costs, costs transferred out, and ending work–in-process

inventory values under the two methods for 2T’s Compounding Department.

o Although either weighted-average or FIFO costing is acceptable for assigning costs to

inventories and cost of goods sold for external reporting, the weighted-average method

has been criticized for masking current period costs.

COMPUTING PRODUCT COSTS: SUMMARY OF THE STEPS

• Exhibit 8.15 provides a summary of the steps for assigning costs to units of production using

process costing and assuming either a weighted-average or FIFO cost flow.

USING COSTS TRANSFERRED IN FROM PRIOR DEPARTMENTS

• As the product passes from one department to another, its costs must follow.

See Demonstration Problem 3

• Who Is Responsible for Costs Transferred in From Prior Departments?

o An important question for performance evaluation is whether a department manager

should be held accountable for all costs charged to the department. The answer is usually

no.

8–13

LO 8-7 Know when to use process or job costing.

CHOOSING BETWEEN JOB AND PROCESS COSTING

• In job costing, costs are collected for each unit produced. Process costing accumulates costs

in a department for an accounting period and then spreads them evenly, or on an average

basis, over all units produced during the period.

• The choice of process versus job costing systems involves a comparison of the costs and

benefits of each system. The production process being utilized is also a major factor in

choosing a cost system.

LO 8-8 Compare and contrast operation costing with job costing and

process costing.

OPERATION COSTING

• Exhibit 8.17 shows a comparison of the three product costing methods.

• Operation costing is a hybrid of job and process costing that is used in manufacturing goods

that have some common characteristics and some individual characteristics.

o An operation is a standardized method of making a product that is repeatedly performed.

8–14

• Product Costing in Operations

o The key difference between operation costing and the two methods discussed in this

chapter and the previous chapter, job and process costing, is that for each work order or

batch passing through a particular operation, direct materials are different but conversion

costs (direct labor and manufacturing overhead) are the same.

o Exhibit 8.18 shows the flow of products through St. Ignace’s three departments,

Assembly, Painting, and Customization.

▪ Tigers pass through only the first two departments, where operations are identical for

both types of snowmobiles, but Ocelots pass through all three departments.

• Operation Costing Illustration

o Exhibit 8.19 shows the data on production and costs associated with this work order

COMPARING JOB, PROCESS, AND OPERATION COSTING

• Every company has its own unique costing methods that do not precisely fit any of these

three categories.

8–15

Matching

A.

Equivalent unit

E.

Prior department costs

B.

First-in, first-out FIFO process costing

F.

Production cost report

C.

Operation

G.

Weighted-average process costing

D.

Operation costing

_____ 1. An inventory costing method that combines costs and equivalent units of a period

with the costs and the equivalent units in beginning inventory from the last period.

_____ 2. Summarizes production and cost results for a period.

_____ 3. The manufacturing costs of units transferred out of one department and into a

subsequent department in the manufacturing process.

_____ 4. A hybrid of job and process costing that is used in manufacturing goods that have

some common characteristics and some individual characteristics.

_____ 5. A standardized method of making a product that is repeatedly performed.

_____ 6. An inventory costing method whereby the first goods received are the first ones

charged out when sold or transferred.

_____ 7. The number of complete physical units to which units in inventories are equal in

terms of work done to date.

8–16

Matching Answers

1. G

Multiple Choice

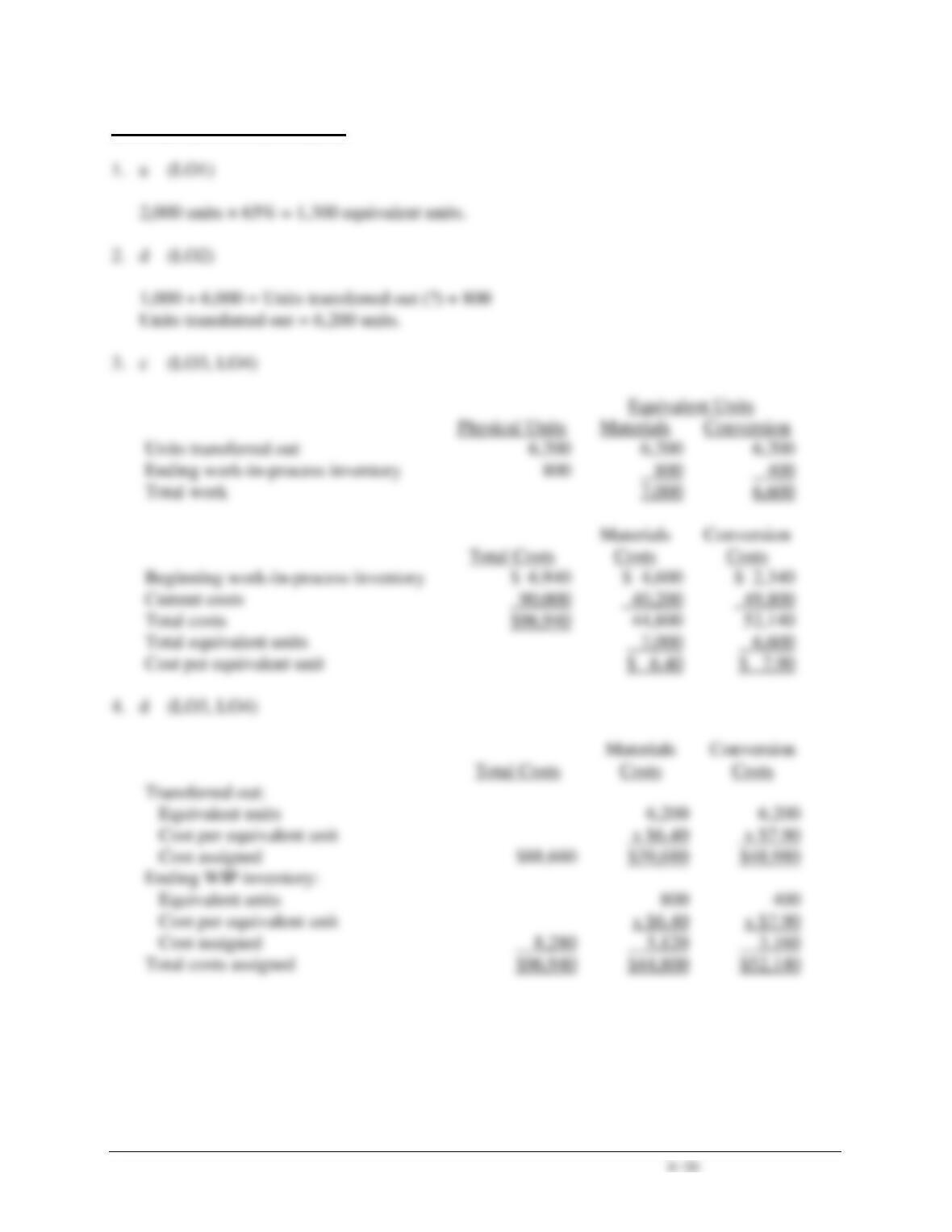

1. There are 2,000 units in the ending work-in-process inventory which are 65 percent complete

with respect to conversion costs. What are the equivalent units of production for the ending

inventory with respect to conversion?

a. 1,300 equivalent units.

b. 1,500 equivalent units.

c. 1,700 equivalent units.

d. 2,100 equivalent units.

Use the following information to answer questions 2 through 7:

At Mixing Department, all materials are added at the beginning of the process. Labor and

overhead (conversion resources) are added evenly throughout the process. The following

information pertains to the Mixing Department for the month of August.

Physical Units

Materials

Conversion

Beginning work-in-process

inventory

1,000 units

(60% complete)

$ 4,600

$ 2,340

Units started in August

6,000 units

Ending work-in-process inventory

800 units

(50% complete)

Costs added in August

40,200

49,800

2. How many units were completed and transferred out?

a. 4,100 units

b. 5,300 units

c. 5,900 units

d. 6,200 units

3. Using the weighted-average method, what is the conversion cost per equivalent unit?

a. $8.50

b. $8.10

c. $7.90

d. $7.50

4. Using the weighted-average method, what is the cost assigned to the ending work-in-process

inventory?

a. $5,780

b. $6,960

c. $7,640

d. $8,280

8–18

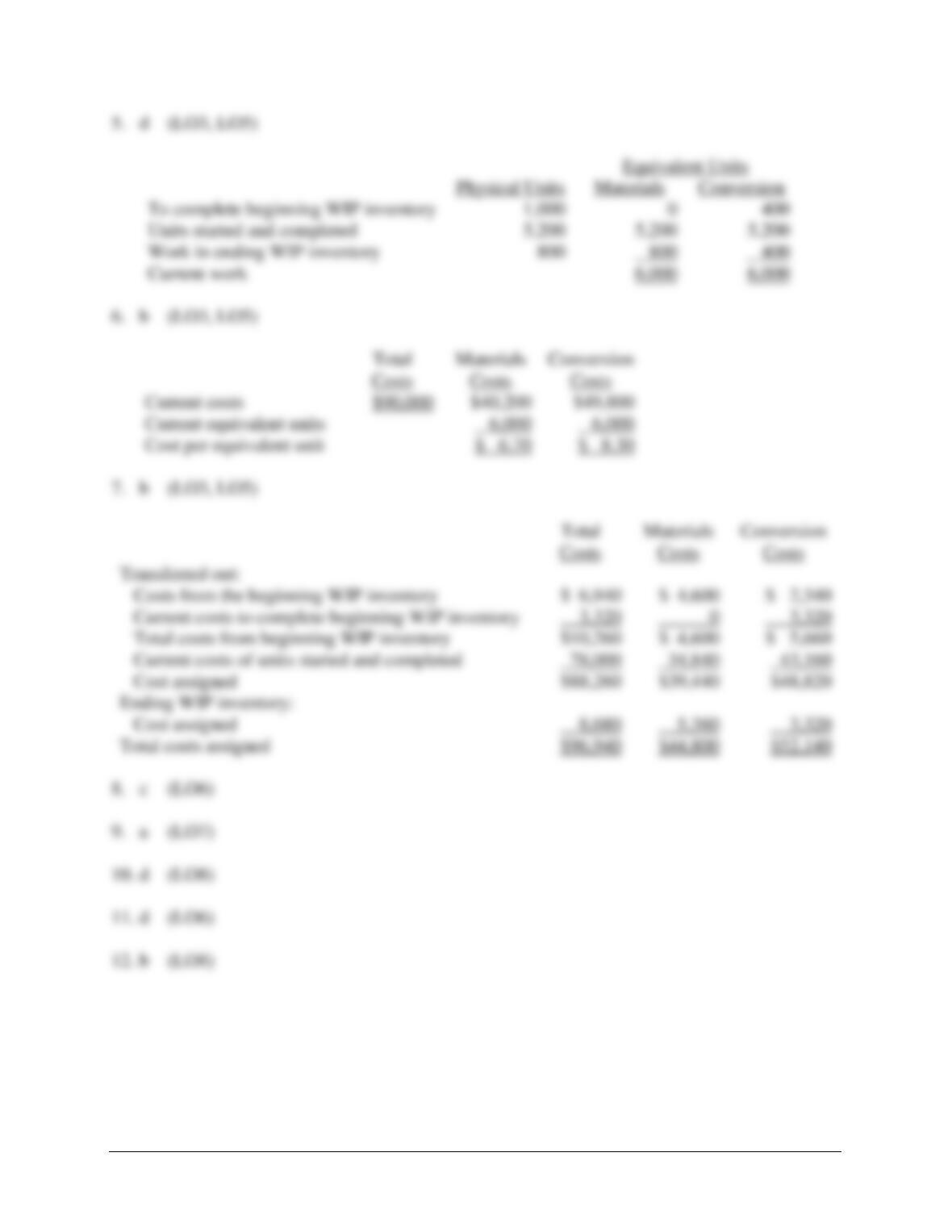

5. Using the FIFO method, what is the number of equivalent units for conversion?

a. 4,800

b. 5,400

c. 5,600

d. 6,000

6. Using the FIFO method, what is the conversion cost per equivalent unit?

a. $7.90

b. $8.30

c. $8.60

d. $9.10

7. Using the FIFO method, what is the cost assigned to the ending work-in-process inventory?

a. $8,280

b. $8,680

c. $9,140

d. $10,260

8. Which of the following statements is not correct?

a. Weighted-average costing does not separate beginning inventory from current period

activity.

b. As the product passes from one department to another, its costs must follow.

c. Equivalent whole units in terms of prior department costs cannot be determined.

d. The FIFO method results in unit costs that better reflect current costs.

9. Which of the following statements is correct?

a. Process costing assumes that each unit produced is relatively uniform.

b. Process costing maintains a detailed record of the cost of each unit produced.

c. Process costing provides as much information as job costing.

d. The difference between job costing and process costing is in the basic concepts.

10. Operation costing system:

a. Is a hybrid system.

b. Treats materials costs using job order costing method.

c. Treats conversion costs using process costing approach

d. All of the above.

11. Prior department costs are:

a. Also called transferred-in costs.

b. The manufacturing costs of units transferred from one department to another.

c. Treated as direct materials added at the beginning of the process.

d. All of the above.

12. Which of the following statements is correct?

a. In practice, only one of the production methods can be found.

b. An operation is a standardized method of making a product repeatedly performed.

c. Every company follows a standard costing method mandated by regulators.

d. The system that costs the most should be adopted because it provides the most accurate

information.

Multiple Choice Answers

8–21

8–22

Demonstration Problem 1

Process Excellence (PE), Inc. has two production departments: Mixing and Packaging.

Mixing

Department

Packaging

Department

Warehouse

At Mixing Department, all materials are added at the beginning of the process. Labor and

overhead (conversion resources) are added evenly throughout the process. The following

information pertains to the Mixing Department for the month of July.

Physical units

Materials

Conversion

Beginning work-in-process inventory

1,000 units

(40% complete)

$8,500

$7,552

Units started in July

5,000 units

Ending work-in-process inventory

400 units

(30% complete)

Costs added in July

60,500

130,872

Required:

1. Determine the number of units completed and transferred to the Packaging Department in

July.

2. Compute the equivalent units using the weighted-average method.

3. Compute the costs per equivalent unit using the weighted-average method.

4. Compute the costs of goods transferred out and the ending work-in-process inventory using

the weighted-average method.

8–23

Demonstration Problem 1 – Solution

Part 1

Work-in-Process Inventory

Beginning balance 1,000

Part 2

Since materials and conversion (labor and overhead) were added at different pace during the

production process, separate equivalent units have to be calculated, one for materials and the

other for conversion.

Physical Units

Conversion

Units transferred out

Total work

Part 3

Under the weighted-average method, the costs for current work and work in beginning work-in–

process inventory are combined. This total cost is then divided by the total equivalent units of

production for July.

Beginning work-in-process inventory

Current costs

Total costs

Total equivalent units

Cost per equivalent unit

Plus: Units started 5,000

Less: Units transferred out ?

Ending balance 400

8–24

Demonstration Problem 1 – Solution, continued

Part 4

Total

Costs

Materials

Costs

Conversion

Costs

Transferred out:

Equivalent units

5,600

5,600

Cost per equivalent unit

x $11.50

Cost assigned

$ 64,400

Ending WIP inventory:

Equivalent units

Cost per equivalent unit

x $11.50

Cost assigned

$ 4,600

Total costs assigned

$ 69,000

16,052

8–25

Demonstration Problem 2

(Continued from Demonstration Problem 1)

The information that pertains to the Mixing Department for the month of July is reproduced here.

All materials are added at the beginning of the process. Labor and overhead (conversion

resources) are added evenly throughout the process.

Physical Units

Materials

Conversion

Beginning work-in-process inventory

1,000 units

(40% complete)

$8,500

$7,552

Units started in July

5,000 units

Ending work-in-process inventory

400 units

(30% complete)

Costs added in July

60,500

130,872

Required:

1. Determine the number of units completed and transferred to the Packaging Department in

July.

2. Compute the equivalent units using the FIFO method.

3. Compute the cost per equivalent unit using the FIFO method.

4. Compute the costs of goods transferred out and the ending work-in-process inventory using

the FIFO method.

8–26

Demonstration Problem 2 – Solution

Part 1

Work-in-Process Inventory

Beginning balance 1,000

Part 2

Since materials and conversion (labor and overhead) were added at different paces during the

production process, separate equivalent units have to be calculated, one for materials and the

other for conversion.

Equivalent Units

Physical units

Materials

Conversion

To complete beginning WIP inventory

Units started and completed

Current work

a

Plus: Units started 5,000

Less: Units transferred out ?

Ending balance 400

Conversion

Current costs

$191,372

$60,500

Current equivalent units

Cost per equivalent unit

Demonstration Problem 2 – Solution, continued

Part 3

Under the FIFO method, current period costs are divided by the current equivalent units of

production in July to determine the cost per equivalent unit.

Part 4

Total

Costs

Materials

Costs

Conversion

Costs

Transferred out:

Costs from the beginning WIP inventory

$ 16,052

$ 8,500

$ 7,552

Current costs to complete beginning WIP inventory

14,760

0

Total costs from beginning WIP inventory

$ 30,812

$ 8,500

$ 22,312

Current costs of units started and completed

168,820

Cost assigned

$199,632

$64,160

Ending WIP inventory:

Cost assigned

7,792

Total costs assigned

$207,424

$69,000

7,792

8–28

Demonstration Problem 3

(Continued from Demonstration Problem 1)

Process Excellence (PE), Inc., has two production departments: Mixing and Packaging.

Mixing

Department

Packaging

Department

Warehouse

At the Packaging Department, all materials are added at the beginning of the process. Labor and

overhead (conversion resources) are added evenly throughout the process. The following

information pertains to the Packaging Department for the month of July.

Physical Units

Transferred-In

Materials

Conversion

Beginning work-in-process

inventory

900 units

(60% complete)

$10,680

$3,888

$5,130

Units completed

6,000 units

Ending work-in-process

inventory

500 units

(50% complete)

Costs added in July

199,920a

42,912

54,245

a This is the cost of goods completed and transferred out of the Mixing Department in July using

the weighted-average method.

Required:

1. Determine the number of units started in July.

2. Compute the equivalent units using the weighted-average method.

3. Compute the cost per equivalent unit using the weighted-average method.

4. Compute the costs of goods transferred out and the ending work-in-process inventory using

the weighted-average method.

8–29

Demonstration Problem 3 – Solution

Part 1

Work-in-Process Inventory

Part 2

Since materials and conversion (labor and overhead) were added at different paces during the

production process, separate equivalent units have to be calculated, one for materials and the

other for conversion. Transferred-in is considered an input added at the beginning of the

production process at the Packaging Department.

Equivalent Units

Physical

Units

Transferred-in

Materials

Conversion

Units transferred out

Total work

Beginning balance 900

Plus: Units started ?

Less: Units transferred out 6,000

Ending balance 500

8–30

Demonstration Problem 3 – Solution, continued

Part 3

Under the weighted-average method, the costs for current work and work in beginning work-in–

process inventory are combined. This total cost is then divided by the total equivalent units of

Part 4

Total Costs

Transferred-in

Materials

Conversion

Transferred out:

Equivalent units

6,000

6,000

6,000

Cost per equivalent unit

$ 32.40

Cost assigned

$194,400

Ending WIP inventory:

Equivalent units

Cost per equivalent unit

$ 32.40

Cost assigned

16,200

Total costs assigned

$210,600

Total Costs

Beginning WIP inventory

$ 10,680

Current costs

Total costs

$210,600

Total equivalent units

8–31

Demonstration Problem 4

Operations Excellence (OE), Inc. has two production departments: Mixing and Packaging.

Mixing

Department

Packaging

Department

Warehouse

OE manufactures two products: Compound H and Compound L. Compound H is a high-end

product that requires more expensive materials than Compound L and is produced at smaller

volume. The two products go through the two production departments in essentially the same

conversion processes. There is no work-in-process inventory for either product.

OE uses an operation costing system that assigns materials cost to the specific product for which

the underlying materials are used and assigns conversion costs to all products evenly as each

product undergoes the same process in each production department.

The production and cost data are available for July:

Compound H

Compound L

Total

2,500 Units

4,800 Units

Materials:

Mixing

$220,000

$100,000

$120,000

Packaging

75,900

37,500

38,400

Total materials cost

$295,900

$137,500

$158,400

Conversion:

Mixing

$219,000

Packaging

131,400

Total conversion cost

$350,400

Required:

Determine the unit cost for Compound H and Compound L.

Demonstration Problem 4 – Solution

For materials costs, the costing system at OE operates like a job order system. For conversion, a

process costing system is appropriate.

Compound H

Compound L

Total

2,500 Units

4,800 Units

Materials:

Mixing

$220,000

$100,000

$120,000

Packaging

75,900

37,500

38,400

Total materials cost

$295,900

$137,500

$158,400

Conversion:

Mixing

$219,000

$ 75,000

$144,000

Packaging

131,400

45,000

86,400

Total conversion cost

120,000

230,400

Total product cost

$646,300

Number of units

4,800

Cost per unit

$ 81

The conversion cost is assigned to the two products based on total units.

For Mixing Department:

Conversion cost for Compound L in the Mixing Department becomes: