CHAPTER 8

SOLUTIONS TO EXERCISES—SET B

EXERCISE 8-1B

(a) The target cost formula is: Target cost = Market price – Desired profit.

(b) Target costing is particularly helpful when a company faces a competitive

EXERCISE 8-2B

The following formula may be used to determine return on investment

EXERCISE 8-3B

(a) (1) In this case the selling price would be $132 ($110 + [$110 X 20%]). The

problem with the $132 is that it is unlikely that Wave will be able to sell

any All-Body suits at that price. Market research seems to indicate that it

EXERCISE 8-3B (Continued)

(b) In this case the amount would be the selling price of $120.

(c) The highest acceptable cost would be the target cost. The target cost is

$100 as shown below:

EXERCISE 8-4B

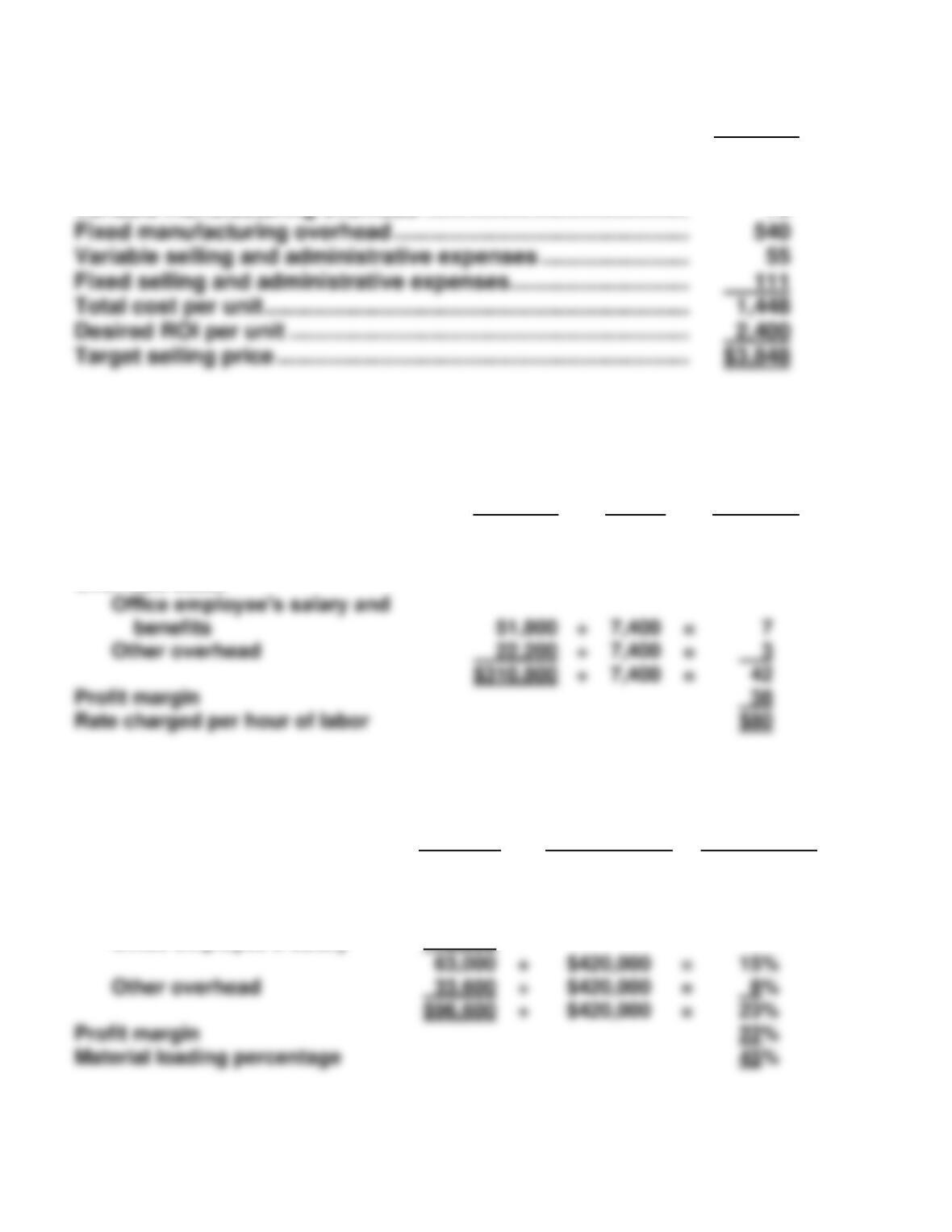

(a) Total cost per unit:

Per Unit

Direct materials ………………………………………………………………..

Direct labor ………………………………………………………………………

Variable manufacturing overhead ……………………………………..

$20

10

11

EXERCISE 8-5B

(a) Total cost per unit:

Per Unit

Direct materials ………………………………………………………………..

Direct labor ………………………………………………………………………

Variable manufacturing overhead ……………………………………..

$ 8

9

15

EXERCISE 8-5B (Continued)

(c) Markup percentage using total cost per unit:

$15.05

EXERCISE 8-6B

(a)

Total cost per session:

Per Session

Direct materials …………………………………………..

$ 30

Direct labor …………………………………………………

400

Variable overhead

50

Fixed overhead ($950,000 ÷ 1,000) ………………..

950

Variable selling & administrative expenses …..

Fixed selling & administrative expenses

($540,000 ÷ 1,000) …………………………………….

540

Total cost per session …………………………...

$2,010

(b) Desired ROI per session = (22% X $2,300,000) ÷ 1,000 = $506

EXERCISE 8-7B

(a)

Fixed manufacturing overhead per unit

=

$2,160,000

=

$540 per unit

4,000

(b)

Desired ROI per unit

=

=

EXERCISE 8-7B (Continued)

(c)

Per Unit

Direct materials ………………………………………………………………..

Direct labor ………………………………………………………………………

Variable manufacturing overhead ……………………………………..

$ 380

290

72

EXERCISE 8-8B

(a)

Total

Cost

÷

Total

Hours

=

Per Hour

Charge

Hourly labor rate for repairs

Technician’s wages and benefits

Overhead costs

$236,800

÷

7,400

=

$32

(b)

Material

Loading

Charges

÷

Total

Invoice Cost,

Parts and

Materials

=

Material

Loading

Percentage

Overhead costs

Parts manager’s salary and

benefits

Office employee’s salary

$50,000

13,000

EXERCISE 8-8B (Continued)

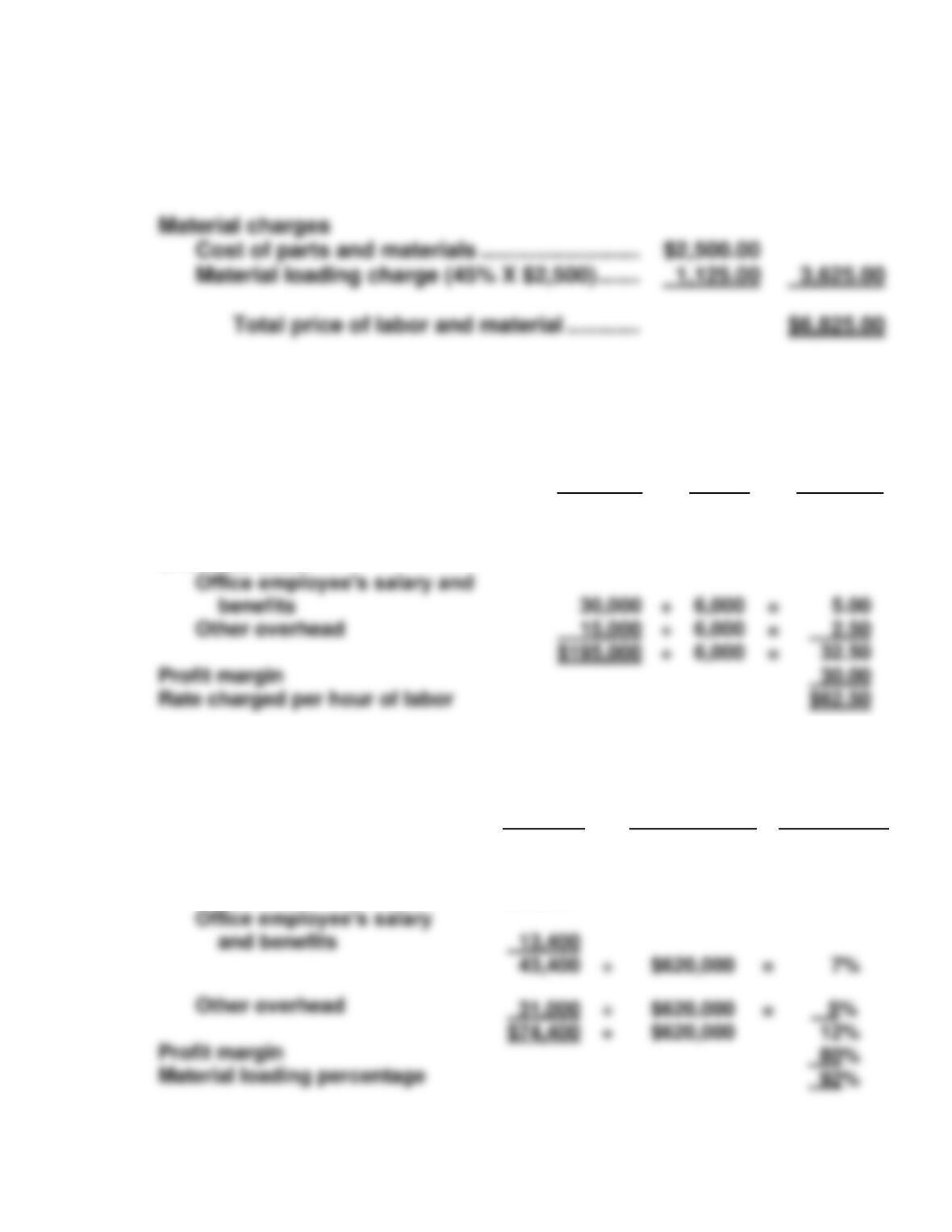

(c) Job: Lore Corporation—Rebuild spot welder

Labor charges

40 hours @ $80 ………………………………………. $3,200.00

EXERCISE 8-9B

(a)

Total

Cost

÷

Total

Hours

=

Per Hour

Charge

÷

=

Hourly labor rate for repairs

Technician’s wages and benefits

Overhead costs

$150,000

÷

6,000

=

$25.00

(b)

Material

Loading

Charges

÷

Total

Invoice Cost,

Parts and

Materials

=

Material

Loading

Percentage

Overhead costs

Parts manager’s salary and

benefits

$30,000

EXERCISE 8-9B (Continued)

(c) Job: Brock Casey

Labor charges

80 hours @ $62.50 ……………………………… $ 5,000

EXERCISE 8-10B

(a)

Total

Cost

÷

Total

Hours

=

Hourly

Charge

Hourly labor rate:

Restorers’ wages and fringes

$270,000

÷

15,000

=

$18.00

Overhead costs:

Administrative salaries & fringes

Other overhead costs

46,000

÷

=

Total hourly cost

$370,000

÷

=

$24.67

Profit margin = Hourly rate – total hourly cost

EXERCISE 8-10B (Continued)

(b)

Material

Loading

Charges

÷

Total Invoice

Cost, Parts &

Materials

=

Material

Loading

Percentage

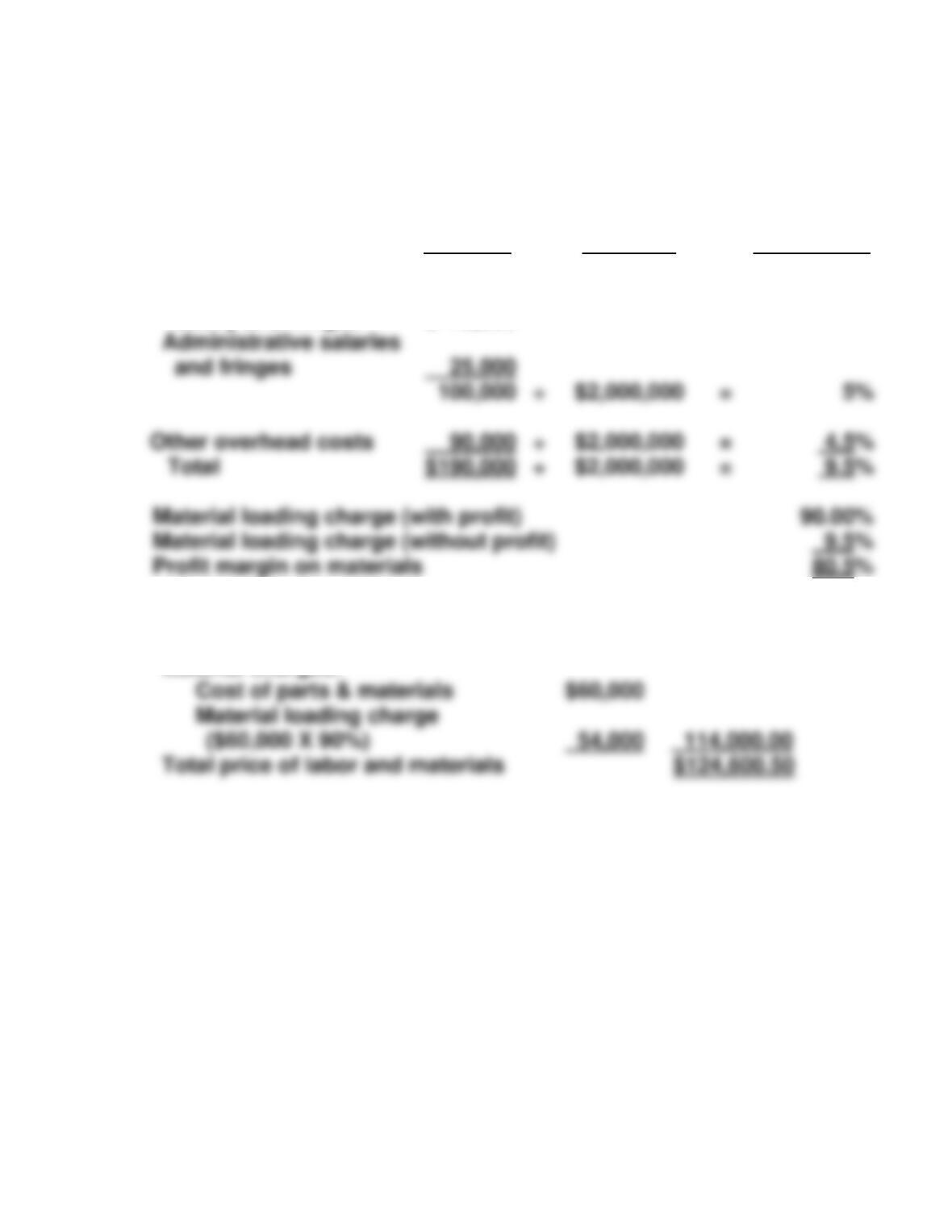

Overhead costs:

Purchasing agent’s

salary and fringes

$ 75,000

(c)

Labor charges:

150 hours @ $70.67

$ 10,600.50

Material charges:

Cost of parts & materials

Material loading charge

($60,000 X 90%)

Total price of labor and materials

Administrative salaries

and fringes

÷

=

Other overhead costs

÷

=

Total

$190,000

÷

=

EXERCISE 8-11B

(a) As indicated, BodyFrame has excess capacity and therefore should be

willing to accept any price that equals or exceeds its variable cost.

(1) The effect on Cycle Division is as follows:

Present Situation

Purchase from

BodyFrame

Selling price

Variable cost of goods sold

$2,000

$2,000

(2) The effect on BodyFrame is that it makes $30 on each frame sold as

shown below:

(3) As a result, the overall income for Morton increases $50,000 ($20,000

from Cycle Division and $30,000 from BodyFrame).

(b) (1) The answer would not change from (a)(1). Cycle Division would

gain $20,000 if it purchased the frames from BodyFrame.

(2) However, BodyFrame would incur a loss of $80,000 as computed

below:

Selling price to outside buyer $ 360

Selling price to Cycle Division (280)

(3) The effect on the overall income to Morton is a net loss of

$60,000 as shown below:

Cycle Division gain $20,000

EXERCISE 8-12B

(a) The minimum transfer price that Winton should accept is:

(b) The lost contribution margin per unit to the company is:

Contribution margin lost by Winton [($87 – $31) – $2] ……….. $54

(c) If management insists that it wants Winton to provide the stereo units,

and Winton is operating at full capacity, then it must be willing to pay the

minimum transfer price for those units. Otherwise it will be penalizing the

EXERCISE 8-13B

(a) Minimum transfer price = ($124 – $5) + $0 = $119

EXERCISE 8-14B

(a) The minimum transfer price for Division B would be variable costs, which

are $9.00 per unit ($10.00, variable cost – $1.00, variable selling expense).

(b) Minimum transfer price = variable costs + opportunity cost

Variable costs = $9.00 (as in (a))

(c) Minimum transfer price = variable costs + opportunity cost

Variable costs = $9.00 (as in (a))

*EXERCISE 8-15B

(a) Cost per unit:

Per Unit

Direct materials ………………………………………………………………..

Direct labor ………………………………………………………………………

Variable manufacturing overhead ……………………………………..

$ 8

9

15

(b) Desired ROI per unit = (25% X $24,080,000)/400,000 = $15.05

*EXERCISE 8-15B (Continued)

=

*EXERCISE 8-16B

(a) The cost base of absorption-cost pricing includes only manufacturing

costs. All selling and administrative costs are excluded from the cost

base and are added back in the numerator of the markup percentage.

(b) The cost base of variable-cost pricing includes only variable costs. All

fixed costs are excluded from the cost base and are added back in the

numerator of the markup percentage.

*EXERCISE 8-17B

(a)

Fixed manufacturing

overhead per unit

=

$2,160,000

=

$540 per unit

4,000

Fixed selling and administrative

expenses per unit

(b)

Desired ROI per unit

=

20% X $48,000,000

=

$2,400 per unit

4,000

*EXERCISE 8-17B (Continued)

(c)

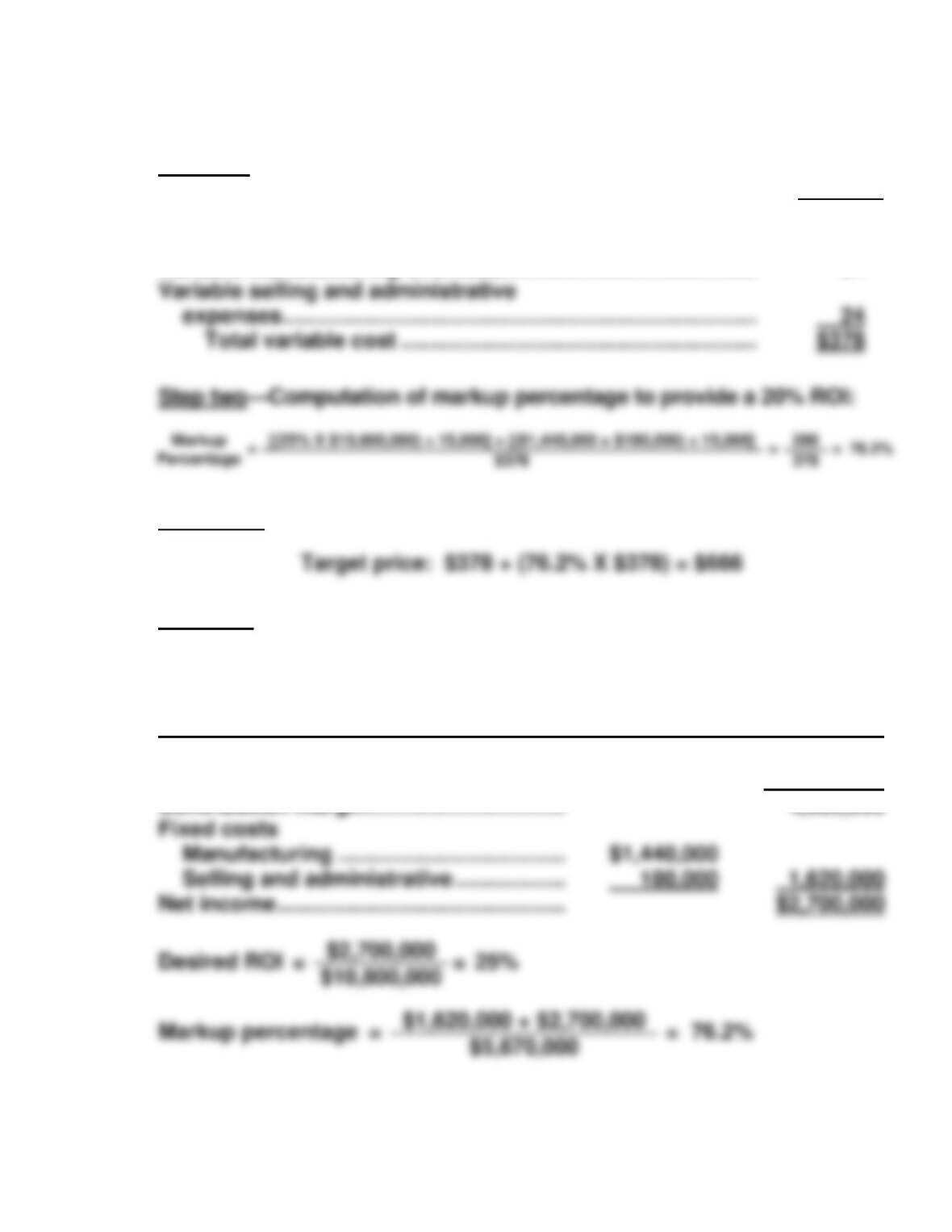

Absorption-cost pricing

markup percentage

=

$2,400 + ($55 + $111)

=

200.16%

$380 + $290 + $72 + $540

markup percentage

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 8-1C

(a) Direct materials ………………………………………………………………. $ 8

Direct labor …………………………………………………………………….. 16

Variable manufacturing overhead …………………………………….. 7

Variable selling and administrative expenses……………………. 5

Variable cost per unit ………………………………………………………. $36

(b) Total cost per unit …………………………………………………………… $ 76

(c) Total cost per unit …………………………………………………………… $76.00

(d) Variable cost per unit ………… $36.00 (same as above)

PROBLEM 8-2C

(a) Direct materials ………………………………………………………………. $34

Direct labor …………………………………………………………………….. 20

Total

Costs

÷

Budgeted

Volume

=

Cost

Per Unit

expenses

Fixed cost per unit

÷

100,000

100,000

=

=

Fixed manufacturing overhead

Fixed selling and administrative

$2,500,000

÷

100,000

=

$25

Desired ROI per unit

=

30% X $3,200,000

=

9.60

100,000

Total cost per unit …………………………………………………………… $116.00

(b) Variable cost per unit ……………………………………… $84 (same as (a))

Total

Costs

÷

Budgeted

Volume

=

Cost

Per Unit

Fixed selling and administrative

expenses

Fixed cost per unit

700,000

÷

=

Fixed manufacturing overhead

$2,500,000

÷

80,000

=

$31.25

PROBLEM 8-2C (Continued)

Variable cost per unit ………………………………………………………. $ 84.00

Fixed cost per unit ………………………………………………………….. 40.00

Total cost per unit …………………………………………………………… $124.00

PROBLEM 8-3C

(a) Computation of time charge rate

Total

Cost

Total

Hours

Per Hour

Charge

(b) Computation of material loading charge

Material

Loading

Charges

Total Invoice Cost,

Parts and Materials

Material

Loading

Percentage

Total

Overhead costs

Parts manager’s salary

and benefits

$30,000

PROBLEM 8-3C (Continued)

(c) Price quotation for time and material

RAJIB BIKE REPAIR SHOP

Time and Material Price Quotation

Job: Fix Alpine Mountain bike

Labor charges: 3 hours @ $22.00 ……………… $ 66.00

Material charges

PROBLEM 8-4C

(a) Assuming no available capacity, the printing operation’s variable cost is

$0.015 per page and its opportunity cost is $0.01 ($0.025 – $0.015) per

(b) Assuming that the printing operation has available capacity, the printing

operation’s variable cost is $0.015 and its opportunity cost is $0. The

minimum transfer price would be $0.015 ($0.015 + $0). Therefore, in this

case, the printing operation should accept the offer to print internally. The

(c) The advantages of having all of the company’s printing done internally

include: (1) ensuring that the company’s quality expectations are met, (2)

ensuring that all projects are completed on a timely basis, and (3)

ensuring that jobs are scheduled in a manner consistent with the

(d) The printing operation would lose:

($0.025 – $0.018) X 64 pages X 18,000 copies = $(8,064)

PROBLEM 8-5C

(a) The minimum transfer price is based on the variable cost of units

transferred internally, plus the opportunity cost of units sold externally. The

variable cost of internal sales would be $0.14 ($0.20 – $0.06). The

(b) If the Peg Division rejects the offer, the Alto division will suffer a loss of

contribution margin, as well as the company as a whole. The amount of

this loss is calculated as:

Lost contribution margin by Alto Division:

Cost of buying externally, per Peg $0.30

Cost of buying internally, per Peg 0.26

Lost contribution margin by Peg Division:

Unit contribution margin on internal sales

($0.26 – $0.14) $0.12

PROBLEM 8-6C

(a) Assuming no available capacity, and that the number of new units

produced would be equal to the number of standard units forgone,

variable cost of the special circuit board would be $51 ($30 + $21) and the

(b) Assuming no available capacity, and that in order to produce the 200,000

circuit boards, 280,000 standard circuit boards would be forgone, the

minimum variable cost would be ($30 + $21) or $51 and the opportunity

cost would be:

(c) Assuming that the PC Division has available capacity, variable cost

would be $51 ($30 + $21) and the opportunity cost would be zero.

*PROBLEM 8-7C

(a) Absorption-cost pricing:

Computation of unit manufacturing cost and target selling price

Direct materials ……………………………………………………………… $ 50

Direct labor ……………………………………………………………………. 35

Variable manufacturing overhead ……………………………………. 15

(b) Variable-cost pricing:

Computation of total variable cost and target selling price

Direct materials ……………………………………………………………. .. $ 50

Direct labor ……………………………………………………………………. 35

Variable manufacturing overhead ……………………………………. 15

*PROBLEM 8-8C

Absorption-cost pricing

(a) Step one—Computation of unit manufacturing cost:

Per Unit

Direct materials ………………………………………………………………

Direct labor …………………………………………………………………….

$200

120

(b) Step three—Computation of target price:

Step four—Proof of 25% ROI under absorption-cost approach:

HALO BIKES INC.

Budgeted Absorption-Cost Income Statement

(Mountain Bike)

Revenues (15,000 units X $666) …………………………. $9,990,000

Cost of goods sold (15,000 units X $450.00) ……….. 6,750,000

Gross ………………………………………………………………. 3,240,000

*PROBLEM 8-8C (Continued)

Variable-cost pricing

(c) Step one—Computation of unit variable cost:

Per Unit

Direct materials …………………………………………………………….

Direct labor …………………………………………………………………..

Variable manufacturing overhead …………………………………..

$200

120

34

(d) Step three—Computation of target price:

Step four—Proof of 25% ROI under variable-cost pricing:

HALO BIKES INC.

Budgeted Variable-Cost Income Statement

(Tinted Window)

Revenue (15,000 units X $666) …………… $9,990,000

Variable costs (15,000 units X $378) …… 5,670,000

Contribution margin ………………………….. 4,320,000