CHAPTER 8

SOLUTIONS TO PROBLEMS: SET B

PROBLEM 8-1B

(a)

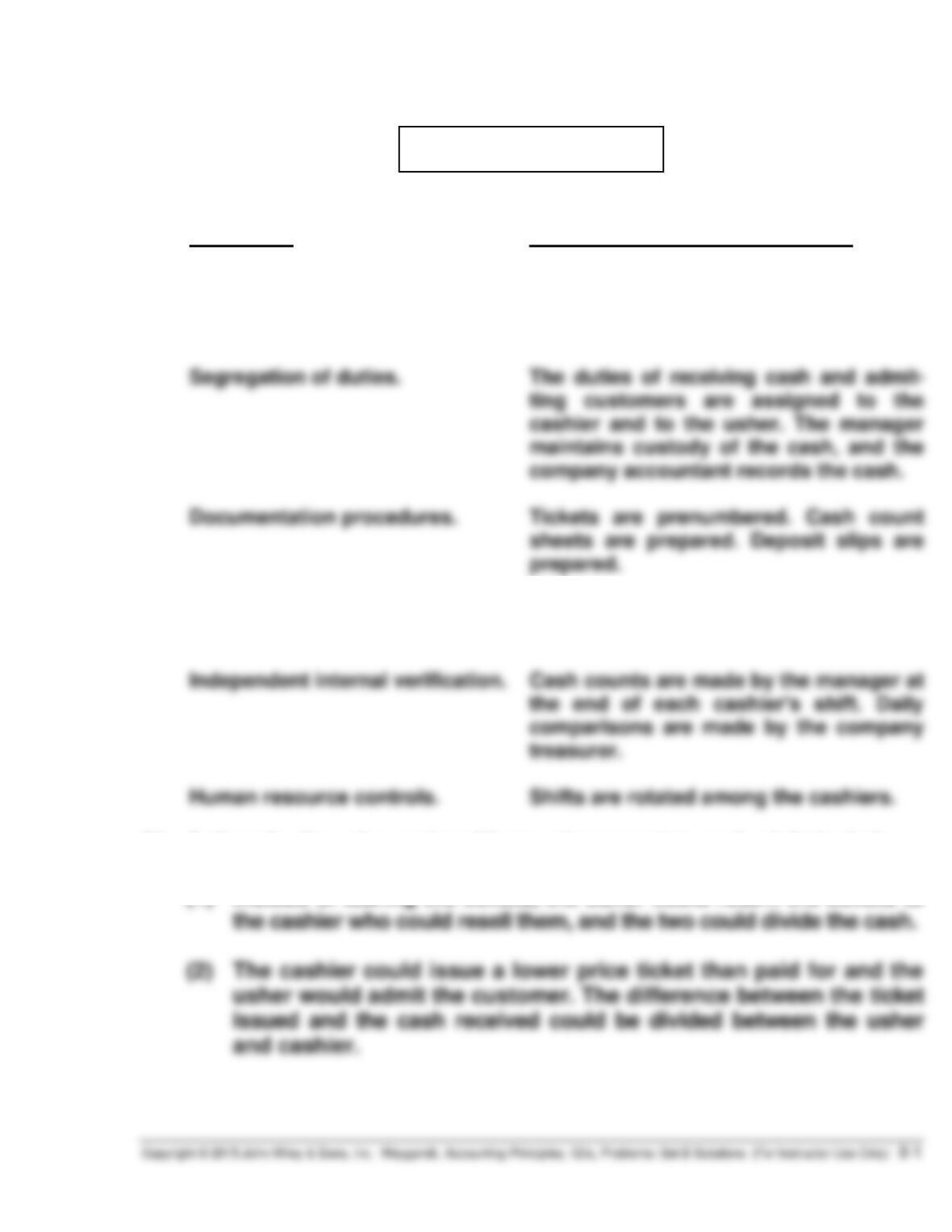

Principles

Application to Granada Theater

Establishment of responsibility.

Only cashiers are authorized to sell

tickets. Only the manager and cashier

can handle cash.

cashier and to the usher. The manager

company accountant records the cash.

Documentation procedures.

Tickets are prenumbered. Cash count

sheets are prepared. Deposit slips are

prepared.

Physical controls.

A safe is used for the storage of cash

and a machine is used to issue tickets.

the end of each cashier’s shift. Daily

comparisons are made by the company

treasurer.

Human resource controls.

(b) Actions by the usher and cashier to misappropriate cash might include:

(1) Instead of tearing the tickets, the usher could return the tickets to

the cashier who could resell them, and the two could divide the cash.

PROBLEM 8-2B

(a) July 1 Petty Cash ………………………………………… 100.00

Cash…………………………………………… 100.00

15 Freight-Out ……………………………………….. 51.00

Postage Expense ………………………………. 20.50

Aug. 15 Freight-Out ……………………………………….. 40.20

Entertainment Expense ……………………… 21.00

Postage Expense ………………………………. 16.00

Miscellaneous Expense ……………………… 19.80

(b)

Petty Cash

Date

Explanation

Ref.

Debit

Credit

Balance

July 1

CP

100

100

PROBLEM 8-2B (Continued)

(c) The internal control features of a petty cash fund include:

(1) A custodian is responsible for the fund.

PROBLEM 8-3B

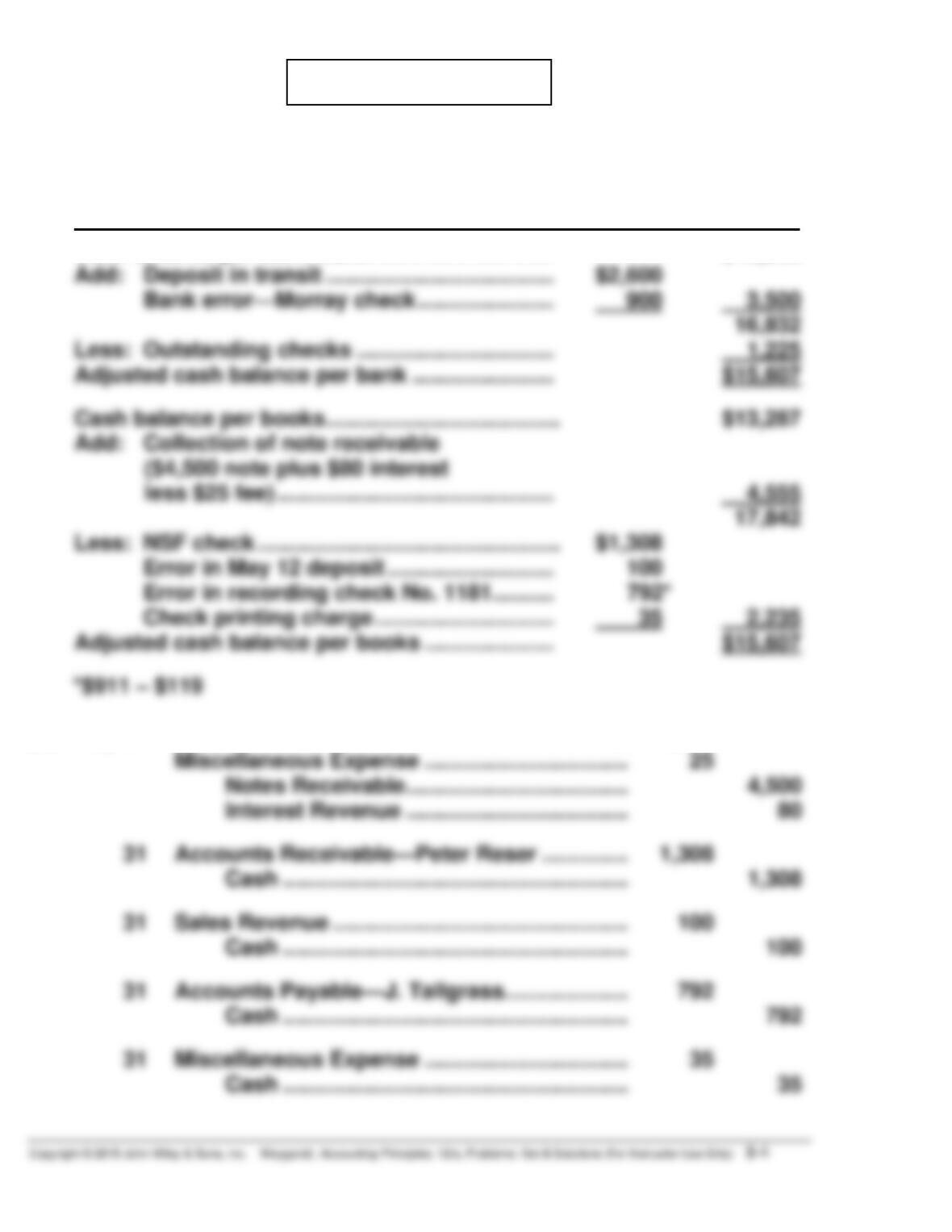

(a) DAVANEY GENETICS COMPANY

Bank Reconciliation

May 31, 2017

Cash balance per bank statement ………………… $13,332

Add: Deposit in transit ………………………………. $2,600

Bank error—Morray check …………………. 900 3,500

16,832

Less: Outstanding checks ………………………….. 1,225

Adjusted cash balance per bank ………………….. $15,607

(b) May 31 Cash ………………………………………………………. 4,555

Miscellaneous Expense …………………………... 25

Notes Receivable ……………………………… 4,500

Interest Revenue ……………………………… 80

PROBLEM 8-4B

(a) PHILLIPS COMPANY

Bank Reconciliation

November 30, 2017

Cash balance per bank statement …………….. $ 9,100

Add: Deposits in transit …………………………. 2,541

11,641

Less: Outstanding checks

No. 2451 …………………………………….. $700

No. 2472 …………………………………….. 270

No. 2478 …………………………………….. 300

Cash balance per books…………………………... $ 5,958

Add: Note collected by bank

($2,300 note plus $91 interest

Less: Check printing charge ……………………. $ 34

Error in recording check No. 2479 ……. 90*

Error in 11-21 deposit

PROBLEM 8-4B (Continued)

(b) Nov. 30 Cash …………………………………………………. 2,375

Miscellaneous Expense ……………………… 16

Notes Receivable ………………………… 2,300

Interest Revenue …………………………. 91

PROBLEM 8-5B

(a) ZHANG COMPANY

Bank Reconciliation

August 31, 2017

Cash balance per bank statement ………………….. $16,856

Add: Deposits in transit (1) ………………………….. $ 5,729

Bank error ($277 – $275) ……………………… 2 5,731

(1) August receipts per books ……………………… $50,050

August deposits per bank ………………………. $47,521

(2) Disbursements per books in

August……………………………….. $47,794

Less: Book error …………………… 90

Total disbursements to be

PROBLEM 8-5B (Continued)

(b) Aug. 31 Cash …………………………………………………….. 5,105

Notes Receivable ………………………….... 5,000

Interest Revenue …………………………….. 105

PROBLEM 8-6B

(a) GAMEL COMPANY

Bank Reconciliation

October 31, 2017

Cash balance per bank statement ……………………………… $15,313.00

Plus: Undeposited receipts ……………………………………… 3,226.18

18,539.18

Less: Outstanding checks

No.

Amount

No.

Amount

62

$107.74

862

$132.10

Cash balance per books……………………………………………. $18,608.81

Add: Bank credit (collection of note receivable) ……….. 460.00

(b) The cashier attempted to cover the theft of $1,445.50 by:

1. Not listing as outstanding three checks totaling $450.50 (No. 62,

$107.74; No. 183, $127.50; and No. 284, $215.26).

PROBLEM 8-6B (Continued)

(c) 1. The principle of independent internal verification has been violated

because the cashier prepared the bank reconciliation.