Chapter 8

Prospective Analysis: Valuation Implementation

Discussion Questions

1. How would the forecasts in Table 8-2 change if TJX were to maintain a sales growth rate of 10 percent per year from 2011 to 2020 (and all

the other assumptions are kept unchanged)?

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Sales growth rate

10.0%

10.0%

10.0%

10.0%

10.0%

10.0%

10.0%

10.0%

10.0%

10.0%

NOPAT margin

WC to sales

LT assets to sales

33.4%

34.0%

34.3%

34.5%

34.8%

35.0%

35.3%

35.5%

35.8%

36.0%

Debt ratio

57.5%

57.5%

57.5%

57.5%

57.5%

57.5%

57.5%

57.5%

57.5%

57.5%

After tax cost of debt

2.73%

2.73%

2.73%

2.73%

2.73%

2.73%

2.73%

2.73%

2.73%

2.73%

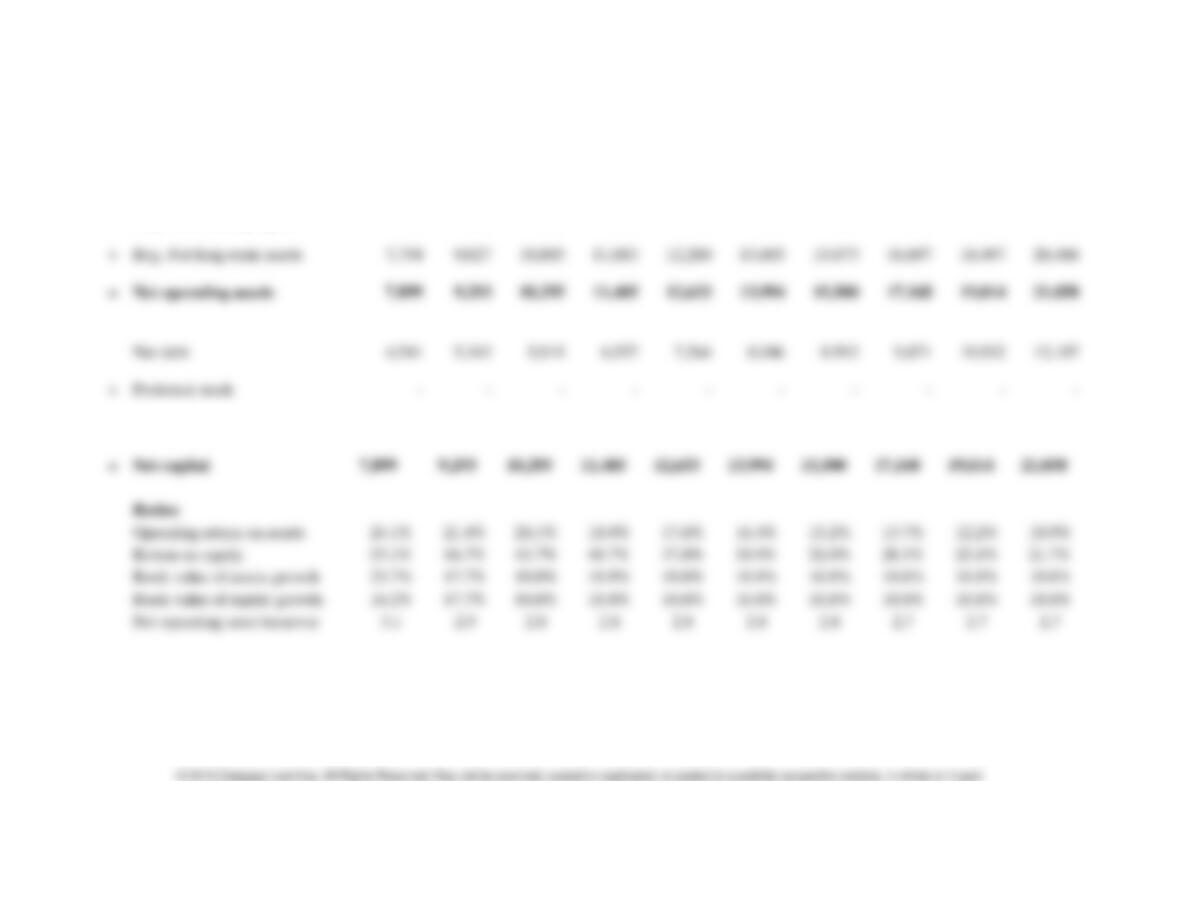

Income Statement

Sales

24,136

26,550

29,205

32,126

35,338

38,872

42,759

47,035

51,739

56,912

Net operating profit after tax

Net interest expense after tax

Net Income

Preferred dividends

Net income to common

2 Instructor’s Manual

Chapter 8 Prospective Analysis: Valuation Implementation 3

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Beginning Balance

Sheet

Beg. Net working capital

144

266

292

321

353

389

428

470

517

569

Beg. Net long-term assets

Net debt

+

Preferred stock

+

Common stock

3,357

3,950

4,376

4,847

5,370

5,948

6,588

7,297

8,082

8,950

Net capital

7,899

9,293

10,295

11,405

12,633

13,994

15,500

17,168

19,014

21,058

Ratios

Operating return on assets

Return on equity

Book value of assets growth

Book value of equity growth

Net operating asset turnover

3.1

2.9

4 Instructor’s Manual

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Cash flows

Net Income

1,783

1,846

1,912

1,974

2,028

2,074

2,109

2,082

2,030

1,946

Change in net working capital

Change in net debt

Free cash flow to equity

Net operating profit after tax

1,907

1,991

2,074

2,152

2,226

2,293

2,352

2,352

2,328

2,277

Change in net working capital

Change in net long-term assets

(1,273)

(1,081)

(1,197)

(1,325)

(1,467)

(1,625)

(1,799)

(1,992)

(2,049)

Free cash flow to capital

2. Recalculate the forecasts in Table 8-2 assuming that the NOPAT profit margin is held steady for the first five years of the forecast and then

declines by 0.1 percentage points per year thereafter (keeping all the other assumptions unchanged).

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Sales growth rate

5.7%

6.6%

7.1%

6.9%

6.7%

6.5%

6.3%

6.1%

5.9%

5.7%

NOPAT margin

7.9%

7.9%

7.9%

7.9%

7.9%

7.8%

7.7%

7.6%

7.5%

7.4%

LT assets to sales

Debt ratio

After tax cost of debt

Sales

23,193

24,724

26,479

28,306

30,203

32,166

34,192

36,278

38,418

40,608

Net operating profit after tax

1,832

1,953

2,092

2,236

2,386

2,509

2,633

2,757

2,881

3,005

Preferred dividends

6 Instructor’s Manual

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Beginning Balance Sheet

Beg. Net working capital

144

247

265

283

302

322

342

363

384

406

+

Beg. Net long-term assets

7,754

8,406

9,069

9,766

Net debt

Preferred stock

+

Common stock

3,357

3,678

3,967

4,271

4,589

4,922

5,268

5,628

6,001

6,386

=

Net capital

7,899

8,653

9,334

10,049

10,797

11,580

12,395

13,241

14,119

15,025

Ratios

Operating return on assets

Return on equity

Book value of assets growth

9.6%

7.9%

7.7%

7.5%

7.2%

7.0%

6.8%

6.6%

6.4%

Book value of equity growth

9.6%

7.9%

7.7%

7.5%

7.2%

7.0%

6.8%

6.6%

6.4%

Net operating asset turnover

Chapter 8 Prospective Analysis: Valuation Implementation 7

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Cash flows

Net Income

1,708

1,817

1,945

2,079

2,217

2,327

2,438

2,549

2,660

2,769

capital

Change in net debt

Free cash flow to equity

Change in net working

Net operating profit after tax

1,832

1,953

2,092

2,236

2,386

2,509

2,633

2,757

2,881

3,005

capital

Change in net long-term

assets

Free cash flow to capital

Change in net working

3. Recalculate the forecasts in Tables 8-2 assuming that the ratio of net operating working capital to sales is 3 percent, and the ratio of net long–

term assets to sales holds steady at 33.4 percent for all the years from fiscal 2011 to fiscal 2020. Keep all the other assumptions unchanged.

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Sales growth rate

5.7%

6.6%

7.1%

6.9%

6.7%

6.5%

6.3%

6.1%

5.9%

5.7%

NOPAT margin

7.9%

7.5%

7.1%

6.7%

6.3%

5.9%

5.5%

5.0%

4.5%

4.0%

Debt ratio

After tax cost of debt

Income Statement

Sales

23,193

24,724

26,479

28,306

30,203

32,166

34,192

36,278

38,418

40,608

Net operating profit after tax

1,832

1,854

1,880

1,897

1,903

1,899

1,881

1,814

1,729

1,624

Preferred dividends

Net income to common

Chapter 8 Prospective Analysis: Valuation Implementation 9

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Beginning Balance Sheet

Beg. Net working capital

144.1

742

794

849

906

965

1,026

1,088

1,153

1,218

+

Beg. Net long-term assets

7,754

8,258

8,844

9,454

+

Common stock

3,357

3,825

4,097

4,379

4,673

4,976

5,290

5,613

5,944

6,283

=

Net capital

7,899

8,999

9,638

10,303

10,994

11,708

12,446

13,205

13,984

14,781

Ratios

Operating return on assets

Return on equity

Book value of assets growth

Book value of equity growth

Net operating asset turnover

10 Instructor’s Manual

Cash flows

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Net Income

1,708

1,713

1,729

1,735

1,730

1,714

1,685

1,607

1,509

1,392

–

Change in net working capital

(598)

(53)

(55)

(57)

(59)

(61)

(63)

(64)

(66)

(69)

Change in net debt

633

Free cash flow to equity

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Net operating profit after tax

1,832

1,854

1,880

1,897

1,903

1,899

1,881

1,814

1,729

1,624

–

Change in net working capital

(598)

(53)

(55)

(57)

(59)

(61)

(63)

(64)

(66)

(69)

–

Change in net long-term assets

(503)

(586)

(610)

(633)

(656)

(677)

(697)

(715)

(731)

(773)

Free cash flow to capital

Chapter 8 Prospective Analysis: Valuation Implementation 11

4. Calculate TJX’s cash payouts to its shareholders in the years 2011–2020 that are implicitly assumed in the projections in Table 8-2.

The cash payouts made to shareholders are simply the free cash flows to equity. These are the surplus cash flows available after

5. How would the abnormal earnings calculations in Table 8-3 change if the cost of equity assumption is changed to 12%?

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Equity Valuation

Abnormal earnings

Abnormal ROE

12 Instructor’s Manual

6. What would be the total equity value (as calculated for scenarios in Table 8-6 using abnormal earnings) if the sales growth in years 2021 and

beyond is 8.5 percent and the company is able to generate abnormal returns at the same level as in fiscal 2020 forever (keeping all the other

assumptions in the table unchanged)?

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Sales growth rate

5.7%

6.6%

7.1%

6.9%

6.7%

6.5%

6.3%

6.1%

5.9%

5.7%

8.5%

WC to sales

0.6%

1.0%

1.0%

1.0%

1.0%

1.0%

1.0%

1.0%

1.0%

1.0%

1.0%

LT assets to sales

Debt ratio

After tax cost of debt

Income Statement

Sales

23,193

24,724

26,479

28,306

30,203

32,166

34,192

36,278

38,418

40,608

44,060

Net operating profit after tax

Net interest expense after tax

Net Income

1,507

Preferred dividends

Net income to common

1,507

Chapter 8 Prospective Analysis: Valuation Implementation 13

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Beginning Balance Sheet

Beg. Net working capital

441

Beg. Net long-term assets

7,754

9,069

11,258

Net debt

4,541

4,975

5,367

5,778

6,208

6,658

7,126

7,613

8,118

8,639

9,373

+

Preferred stock

–

–

–

–

–

–

–

–

–

–

–

Common stock

3,357

3,967

Net capital

7,899

Ratios

Operating return on assets

23.2%

21.4%

20.1%

18.9%

17.6%

16.4%

15.2%

13.7%

12.2%

10.8%

10.8%

Return on equity

50.9%

46.7%

43.7%

40.7%

37.8%

34.9%

32.0%

28.5%

25.1%

21.7%

21.7%

growth

23.7%

growth

turnover

2.7

14 Instructor’s Manual

Valuation

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Abnormal earnings

1,414

1,396

1,386

1,364

1,331

1,285

1,224

1,113

981

829

899

Discount factor

2021 on

7. Calculate the proportion of terminal value to total estimated value of equity under the

abnormal earnings method and the discounted cash flow method for the Scenario 2 results

shown in Table 8-6. Why are these proportions different?

8. What will TJX’s cost of equity be if the equity market risk premium is 5 percent?

Market risk premium

5.0%

4.0%

3.4%

= Cost of common equity

7.4%

9. Assume that TJX changes its capital structure so that its market value weight of debt to

capital increases to 30%, and its after-tax interest rate on debt at this new leverage level is 3.5%.

Assume that the equity market risk premium is 6.7%. What will be the cost of equity at the new

debt level? What will be the new weighted average cost of capital?

The first task is to compute the new equity beta. The beta of TJX’s assets will not change, since its

16 Instructor’s Manual

The revised cost of equity and WACC will then be as follows:

Cost of Equity

Market risk premium

6.7%

5.5%

= Cost of common equity

Weighted Average Cost of Capital

After tax cost of debt

3.5%

Cost of common equity

= Weighted Average Cost of Capital

7.3%

Chapter 8 Prospective Analysis: Valuation Implementation 17

10. Nancy Smith says she is uncomfortable making the assumption that TJX’s dividend payout

will vary from year to year. If she makes a constant dividend payout assumption, what changes

does she have to make in her other valuation assumptions to make them internally consistent

with each other?

If Nancy Smith doesn’t want to allow dividend payout to vary across the years, then she can hold