Accounting Information

Systems

7-21

d. An employee of the finishing department walked off with several parts from the

storeroom and recorded the items in the inventory ledger as having been issued

to the assembly department.

PROBLEM: Employees can commit and conceal fraud when they have access to

e. A cashier cashed a check from a customer in payment of an account receivable,

pocketed the cash, and concealed the theft by properly posting the receipt to the

customer’s account in the accounts receivable ledger.

PROBLEM: The cashier had custody of the checks and was responsible for posting

f. Several customers returned clothing purchases. Instead of putting the clothes

into a return bin to be put back on the rack, a clerk put the clothing in a

separate bin under some cleaning rags. After her shift, she transferred the

clothes to a gym bag and took them home.

PROBLEM: The clerk was authorized to accept the return, grant credit, and had

custody of the inventory. It is also possible that the clerk may have had responsibility

Ch. 7: Control and Accounting Information Systems

g. A receiving clerk noticed that four cases of MP3 players were included in a

shipment when only three were ordered. The clerk put the extra case aside and

took it home after his shift ended.

PROBLEM: The receiving clerk had custody of arriving goods, counted the goods,

and compared the count to a purchase order. The problem is that, while the receiving

h. An insurance claims adjuster had check signing authority of up to $6,000. The

adjuster created three businesses that billed the insurance company for work not

performed on valid claims. The adjuster wrote and signed checks to pay for the

invoices, none of which exceeded $6,000.

PROBLEM: The adjuster had authorization to add vendors to vendor master file,

authorization to write checks up to $6,000, and had custody of the signed the checks.

i. An accounts payable clerk recorded invoices received from a company that he

and his wife owned and authorized their payment.

PROBLEM: The accounts payable clerk had recording duties and he authorized

payments.

Accounting Information

Systems

j. A cashier created false purchase return vouchers to hide his theft of several

thousand dollars from his cash register.

PROBLEM: The cashier had recording (creating return vouchers), custody (cash in

the cash register), and authorization (authorize the return of goods) duties.

k. A purchasing agent received a 10% kickback of the invoice amount for all

purchases made from a specific vendor.

PROBLEM: The purchasing agent has both recording (prepare the purchase order)

and authorization (select a vendor from a list of authorized vendors) duties. The

purchasing agent gets custody to cash when the vendor gives her the kickback.

Ch. 7: Control and Accounting Information Systems

7.3 The following description represents the policies and procedures for agent expense

reimbursements at Excel Insurance Company.

After the expenses are approved, the branch manager sends the expense report to the

home office. There, accounting records the transaction, and cash disbursements

prepares the expense reimbursement check. Cash disbursements sends the expense

reimbursement checks to the branch manager, who distributes them to the agents.

At the end of each month, internal audit at the home office reconciles the expense

reimbursements. It adds the total dollar amounts on the expense reports from each

branch, subtracts the sum of the dollar totals on each branch’s Cash Advance

Approval form, and compares the net amount to the sum of the expense

reimbursement checks issued to agents. Internal audit investigates any differences.

Accounting Information

Systems

7-25

Strengths

Weaknesses

Authorization

Excel has a formal statement of policies

and procedures for agent reimbursements.

There is no limit on the agent’s total weekly

expenditures or cash advances.

Recording

Accounting receives approved expense

reports and cash advance forms. This

facilitates the correct recording of all

authorized transactions.

The Branch Manager does not retain a copy of

expense reports or cash advances for audit

purposes.

The expense report is not checked for mathematical

Safeguarding

Expense reimbursement checks are issued

by the cash disbursements department.

Cash disbursements are made only after

receipt of an approved expense report or

Cash Advance Approval form.

Supporting documentation is not required for all

expenditures.

A copy of the Cash Advance Approval form should

be sent to the Branch Office Cashier so it can

compare it with the one submitted by the agent.

Reconciliation

Internal Audit compares reimbursement

checks with expense report totals less cash

advances in the home office.

There is no reconciliation of Branch Office

Cashier disbursements with Cash Advance

Approval forms.

Expense reports must be approved by the

Branch Manager prior to payment.

Expense reimbursement checks are sent to the

Branch Manager for distribution rather than to the

agent. This allows the Branch Manager to submit a

Ch. 7: Control and Accounting Information Systems

7.4 The Gardner Company, a client of your firm, has come to you with the following

problem. It has three clerical employees who must perform the following functions:

a. Maintain the general ledger

b. Maintain the accounts payable ledger

c. Maintain the accounts receivable ledger

Assuming equal abilities among the three employees, the company asks you to assign

the eight functions to them to maximize internal control. Assume that these employees

will perform no accounting functions other than the ones listed.

a. List four possible unsatisfactory pairings of the functions

All five of the unsatisfactory pairings below involve custody of cash and a recording

function that would allow a fraud perpetrator to conceal a theft.

1. General ledger – cash receipts. With custody to cash, this person could steal

2. Accounts receivable ledger – cash receipts. With custody to cash, this person

3. Bank reconciliation – cash receipts. With custody to cash, this person could

steal cash receipts and conceal the theft by falsifying (recording) the bank

reconciliation.

4. Credits on returns and allowances – cash receipts. This person could

5. Accounts payable ledger – prepare checks for signature. A person with both

6. Maintain accounts receivable – issue credit memos – this combines

authorization and recording. A person with both of these responsibilities could

write off accounts for friends.

b. State how you would distribute the functions among the three employees.

Assume that with the exception of the nominal jobs of the bank reconciliation

Accounting Information

Systems

and the issuance of credits on returns and allowances, all functions require an

equal amount of time.

Any distribution that avoids all of the above unsatisfactory combinations and spreads

the workload evenly is acceptable. The key is not to have anyone with both custody

Ch. 7: Control and Accounting Information Systems

7.5 During a recent review, ABC Corporation discovered that it has a serious internal

control problem. It is estimated that the impact associated with this problem is $1

million and that the likelihood is currently 5%. Two internal control procedures have

been proposed to deal with this problem. Procedure A would cost $25,000 and reduce

likelihood to 2%; procedure B would cost $30,000 and reduce likelihood to 1%. If

both procedures were implemented, likelihood would be reduced to 0.1%.

a. What is the estimated expected loss associated with ABC Corporation’s internal

control problem before any new internal control procedures are implemented?

if procedure B were implemented, and if both procedures were implemented.

Control

Procedure

Risk

Exposure

Revised

Expected

Loss

Reduction in

Expected

Loss

Cost of

Control(s)

Net

Benefit

(Cost)

A

0.02

$1,000,000

$20,000

$30,000

$25,000

$ 5,000

c. Compare the estimated costs and benefits of procedure A, procedure B, and both

procedures combined. If you consider only the estimates of cost and benefit, which

procedure(s) should be implemented?

Considering only the estimated costs and benefits, procedure B should be implemented

d. What other factors might be relevant to the decision

Another important factor to consider is how critical the $1,000,000 loss would be to

ABC Corporation.

Accounting Information

Systems

7-29

(as a form of insurance premium) to reduce the risk of loss to the smallest

possible level.

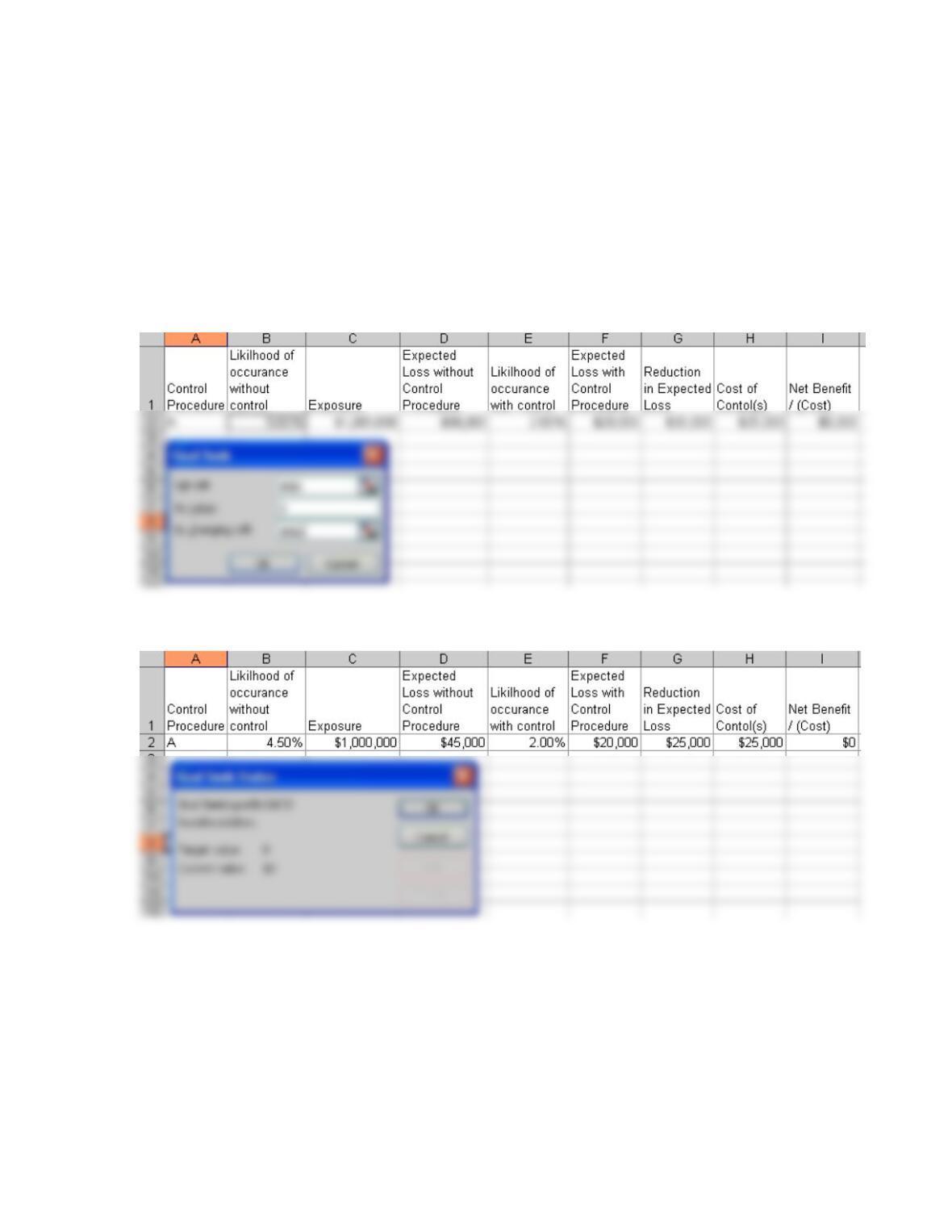

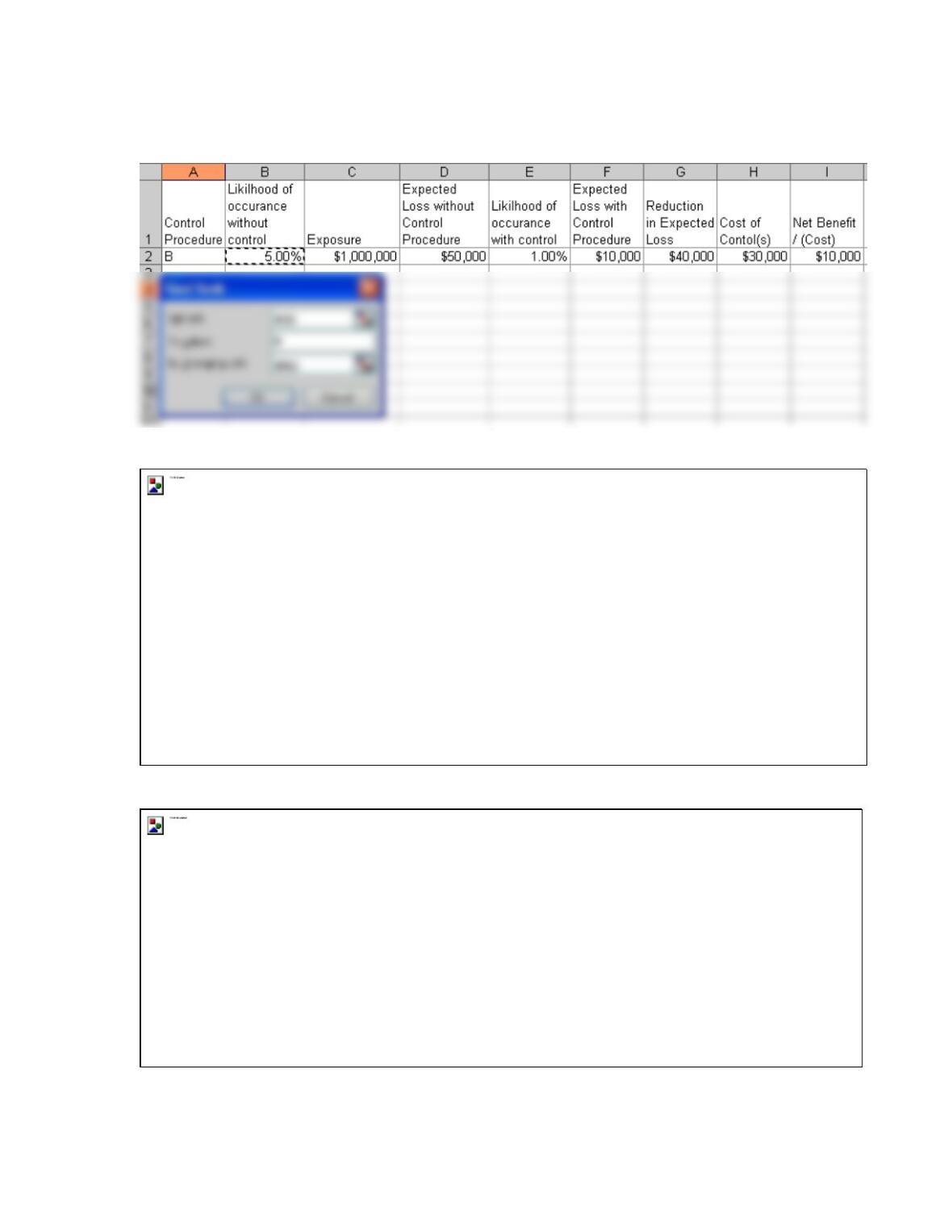

e. Use the Goal Seek function in Microsoft Excel to determine the likelihood of

occurrence without the control and the reduction in expected loss if the net

benefit/cost is 0. Do this for procedure A, procedure B, and both procedures together

Control Procedure A – Goal Seek-setup.

Control Procedure A – Goal Seek – solved.

Ch. 7: Control and Accounting Information Systems

Control Procedure B – Goal Seek-setup.

Control Procedure B – Goal Seek – solved.

Control Procedure Both – Goal Seek-setup.

Accounting Information

Systems

7-31

Control Procedure Both – Goal Seek – solved.

Ch. 7: Control and Accounting Information Systems

7.6 The management at Covington, Inc., recognizes that a well-designed internal control

system provides many benefits. Among the benefits are reliable financial records that

facilitate decision making and a greater probability of preventing or detecting errors

and fraud. Covington’s internal auditing department periodically reviews the

company’s accounting records to determine the effectiveness of internal controls. In

its latest review, the internal audit staff found the following eight conditions:

1. Daily bank deposits do not always correspond with cash receipts.

2. Bad debt write-offs are prepared and approved by the same employee.

5. There are many customer refunds and credits.

6. Many original documents are missing or lost. However, there are substitute

copies of all missing originals.

For each of the eight conditions detected by the Covington internal audit staff:

a. Describe a possible cause of the condition.

Accounting Information

Systems

7-33

#

a. Possible Cause

b. Recommendation to Correct Condition

1

Daily bank deposits do not always

correspond with cash receipts.

Timing difference between when cash is

received and when deposited in the bank

– Cash is received after the day’s bank

deposit is prepared and sent to the

bank.

Make two deposits for each day’s receipts.

An employee who does not handle cash

receipts daily reconciles each day’s cash

receipts per book with deposits per bank

2

Bad debt write-offs are prepared and

approved by the same employee.

Collusion between customers and the

Require all bad debt write-offs to be approved

3

Occasional discrepancies between

physical inventory counts and

perpetual inventory records.

Unauthorized access to physical

inventory and/or inventory records.

Limit physical and logical access to the

inventory records to authorized employees.

Ch. 7: Control and Accounting Information Systems

4

Alterations to physical inventory

counts and perpetual inventory

records

Unauthorized access to inventory

records.

Limit physical and logical access to the

inventory records to authorized employees.

5

Many customer refunds and credits.

Collusion among customers,

Segregate duties so refunds and credits are

6

Many original documents are missing

or lost. However, there are substitute

copies of all missing originals.

Failure to use pre-numbered documents.

Use pre-numbered documents to facilitate the

control and identification of documents.

Count inventory to be shipped before it is

removed from the storeroom, when received by

shipping, and when shipped; reconcile counts.

Accounting Information

Systems

7-35

7

An unexplained decrease in the gross

profit percentage has occurred.

Granting unauthorized discounts or

credits to customers.

Customers given lower, preferential sales

prices

Require the approval of a responsible party

before granting customer discounts or credits.

Require the approval of a responsible party

before granting preferential sales prices

8

Many documents are not approved.

Lack of, misunderstanding of, or failure

to comply with written procedures.

Prepare or update written procedures and train

employees using the procedures

Ch. 7: Control and Accounting Information Systems

7.7 Consider the following two situations:

For the situations presented, describe the recommendations the internal auditors

should make to prevent the following problems. Adapted from the CMA Examination

Situation 1: Many employees of a firm that manufactures small tools pocket some of

the tools for their personal use. Since the quantities taken by any one employee are

immaterial, the individual employees do not consider the act as fraudulent or

detrimental to the company. The company is now large enough to hire an internal

auditor. One of the first things she did was to compare the gross profit rates for

industrial tools to the gross profit for personal tools. Noting a significant difference,

she investigated and uncovered the employee theft.

• Implement and communicate through proper training a policy regarding the theft of

company goods and services and the repercussions associated with theft.

Situation 2: A manufacturing firm’s controller created a fake subsidiary. He then

ordered goods from the firm’s suppliers, told them to ship the goods to a warehouse

he rented, and approved the vendor invoices for payment when they arrived. The

controller later sold the diverted inventory items, and the proceeds were deposited to

the controller’s personal bank account. Auditors suspected something was wrong

when they could not find any entries regarding this fake subsidiary office in the

property, plant, and equipment ledgers or a title or lease for the office in the real–

estate records of the firm

• Implement a better segregation of duties. The company controller should not be able to

order goods, specify shipment locations, and authorize payment for inventory.

Accounting Information

Systems

7-37

7.8 Tralor Corporation manufactures and sells several different lines of small electric

components. Its internal audit department completed an audit of its expenditure

processes. Part of the audit involved a review of the internal accounting controls for

payables, including the controls over the authorization of transactions, accounting for

transactions, and the protection of assets. The auditors noted the following items:

1. Routine purchases are initiated by inventory control notifying the purchasing

department of the need to buy goods. The purchasing department fills out a

2. For efficiency and effectiveness, purchases of specialized goods and services are

3. Accounts payable maintains a list of employees who have purchase order approval

4. Prenumbered vendor invoices are recorded in an invoice register that indicates the

receipt date, whether it is a special order, when a special order is sent to the

5. Prior to making entries in accounting records, the accounts payable clerk checks

the mathematical accuracy of the transaction, makes sure that all transactions are

6. All approved invoices are filed alphabetically. Invoices are paid on the 5th and

20th of each month, and all cash discounts are taken regardless of the terms.

7. The treasurer signs the checks and cancels the supporting documents. An original

document is required for a payment to be processed.

8. Prenumbered blank checks are kept in a locked safe accessible only to the cash

disbursements department. Other documents and records maintained by the

accounts payable section are readily accessible to all persons assigned to the

section and to others in the accounting function.

Ch. 7: Control and Accounting Information Systems

a. For each internal control strength you identified, explain how the procedure

helps achieve good authorization, accounting, or asset protection control.

#

a. Why it is a strength

b. Why it is a weakness

b. Recommendation to

correct weakness

1

The use of pre-numbered

purchase orders allows all

POs to be accounted for.

identification.

User authorization means

the right materials and

quantities will be ordered.

A purchase order copy should not be

used as a receiving report unless the

quantities have been blanked out.

The receiving report is

prepared after an

independent count and

2

It increases the potential for collusive

agreements.

The purchasing department

should approve orders before

the purchase, not before

payment is made.

Accounting Information

Systems

7-39

6

Taking unearned cash discounts

causes additional paperwork when

disputed by suppliers and creates

animosity. This policy may lead to

fewer discounts being offered.

them after payment reduces

duplicate payments.

Pay suppliers on or before

the discount date.

Lost discounts should be

analyzed for cause and future

avoidance.

8

Proper protection of blank

checks (locked safe only

accessible to cash

disbursements department

in a loss of control, a loss of

accountability, or a loss of assets – as

well as improper or inaccurate

accounting or destruction of records.

established and monitored.

Unlimited access to cash disbursement

documents (other than blank checks)

permits unauthorized alteration of

payables documents. This could result

A policy limiting access to

and physical protection of

accounts payable documents

and records should be

minimize errors and helps

Approved, unpaid invoices