7-41

SOLUTION

7-42

7-43

7-34 (30 min.) Direct manufacturing labor and direct materials variances, missing data.

(CMA, heavily adapted) Young Bay Surfboards manufactures fiberglass surfboards. The

standard cost of direct materials and direct manufacturing labor is $223 per board. This includes

40 pounds of direct materials, at the budgeted price of $2 per pound, and 10 hours of direct

manufacturing labor, at the budgeted rate of $14.30 per hour. Following are additional data for

the month of July:

There were no beginning inventories.

Required:

1. Compute direct manufacturing labor variances for July.

2. Compute the actual pounds of direct materials used in production in July.

3. Calculate the actual price per pound of direct materials purchased.

4. Calculate the direct materials price variance.

SOLUTION

7-44

7-35 (35 min.) Direct materials efficiency, mix, and yield variances.

Nature’s Best Nuts produces specialty nut products for the gourmet and natural foods market. Its

most popular product is Zesty Zingers, a mixture of roasted nuts that are seasoned with a secret

spice mixture and sold in 1-pound tins. The direct materials used in Zesty Zingers are almonds,

cashews, pistachios, and seasoning. For each batch of 100 tins, the budgeted quantities and

budgeted prices of direct materials are as follows:

Changing the standard mix of direct material quantities slightly does not significantly affect the

overall end product, particularly for the nuts. In addition, not all nuts added to production end up

in the finished product, as some are rejected during inspection.

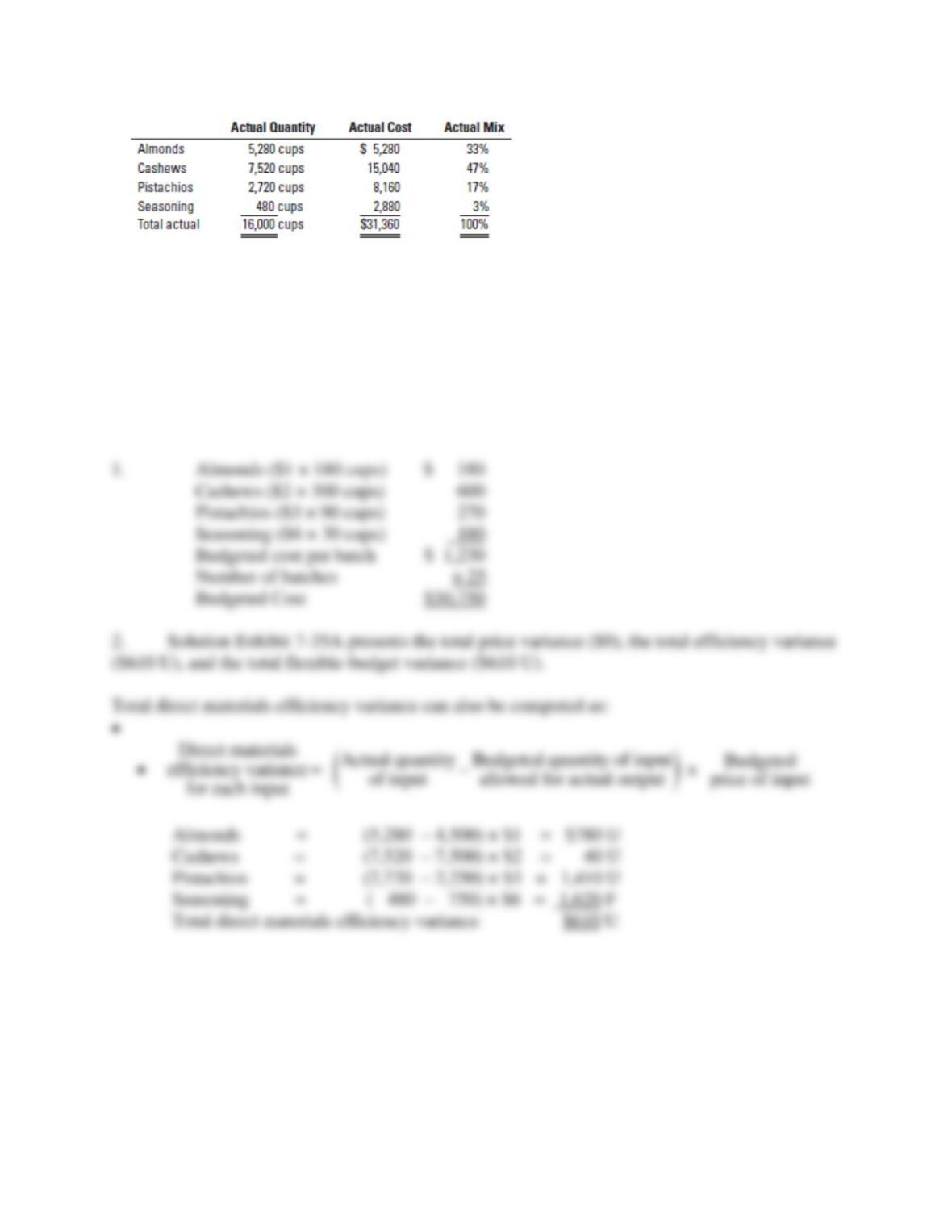

In the current period, Nature’s Best made 2,500 tins of Zesty Zingers in 25 batches with the

following actual quantity, cost, and mix of inputs:

7-45

Required:

1. What is the budgeted cost of direct materials for the 2,500 tins?

2. Calculate the total direct materials efficiency variance.

3. Why is the total direct materials price variance zero?

4. Calculate the total direct materials mix and yield variances. What are these variances telling

you about the 2,500 tins produced this period? Are the variances large enough to investigate?

SOLUTION

• SOLUTION EXHIBIT 7-35A

Columnar Presentation of Direct Materials Price and Efficiency Variances for Nature’s Best

Company.

7-46

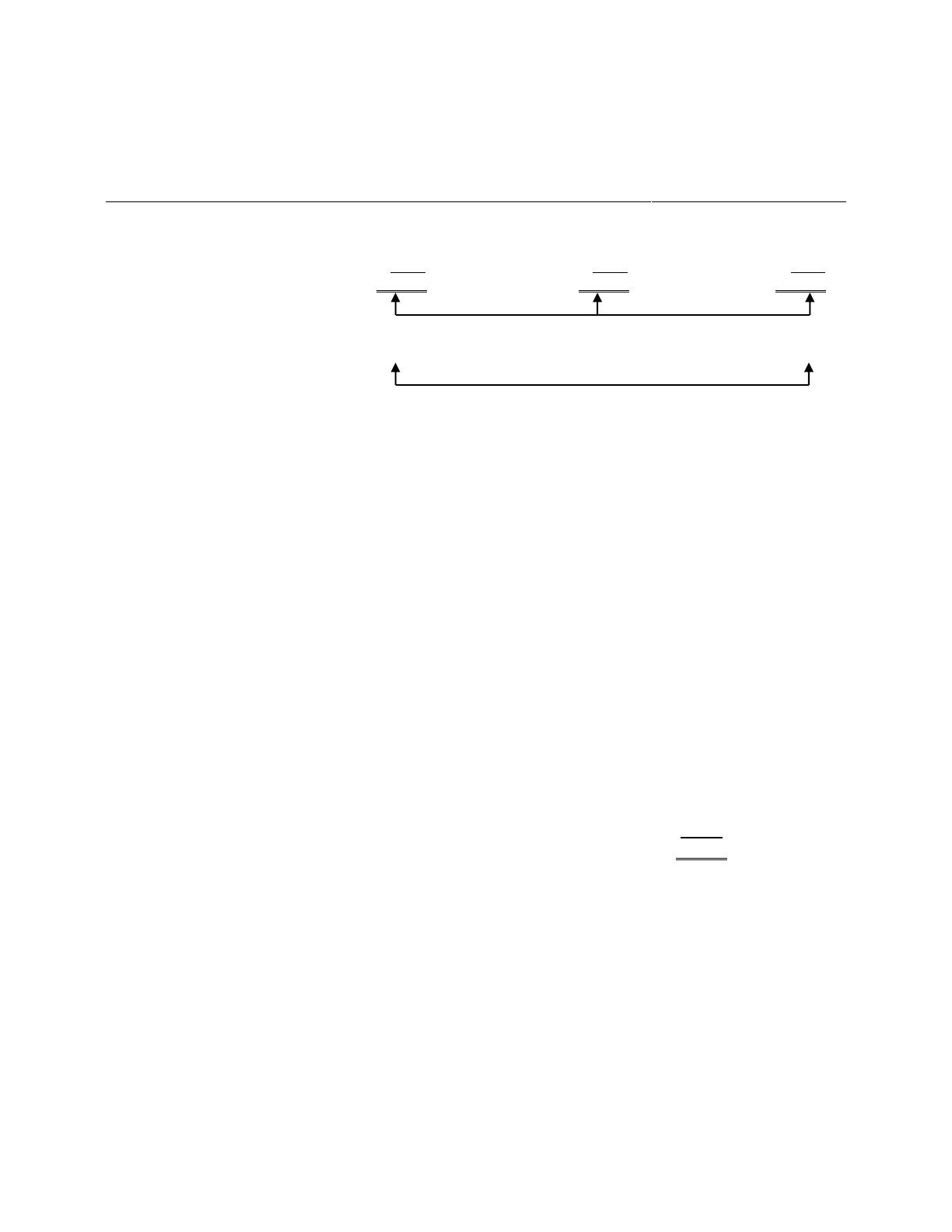

Actual Costs

Incurred

(Actual Input Quantity

× Actual Price)

(1)

Actual Input Quantity

× Budgeted Price

(2)

Flexible Budget

(Budgeted Input Quantity

Allowed for Actual Output

× Budgeted Price)

(3)

Almonds

Cashews

Pistachios

Seasoning

5,280 × $1 = $ 5,280

7,520 × $2 = 15,040

2,720 × $3 = 8,160

480 × $6 = 2,880

$31,360

5,280 × $1 = $ 5,280

7,520 × $2 = 15,040

2,720 × $3 = 8,160

480 × $6 = 2,880

$31,360

4,500 × $1 = $ 4,500

7,500 × $2 = 15,000

2,250 × $3 = 6,750

750 × $6 = 4,500

$30,750

$0 $610 U

Total price variance Total efficiency variance

$610 U

Total flexible-budget variance

F = favorable effect on operating income; U = unfavorable effect on operating income

3. The total direct materials price variance equals zero because, for all four inputs, actual price

per cup equals the budgeted price per cup.

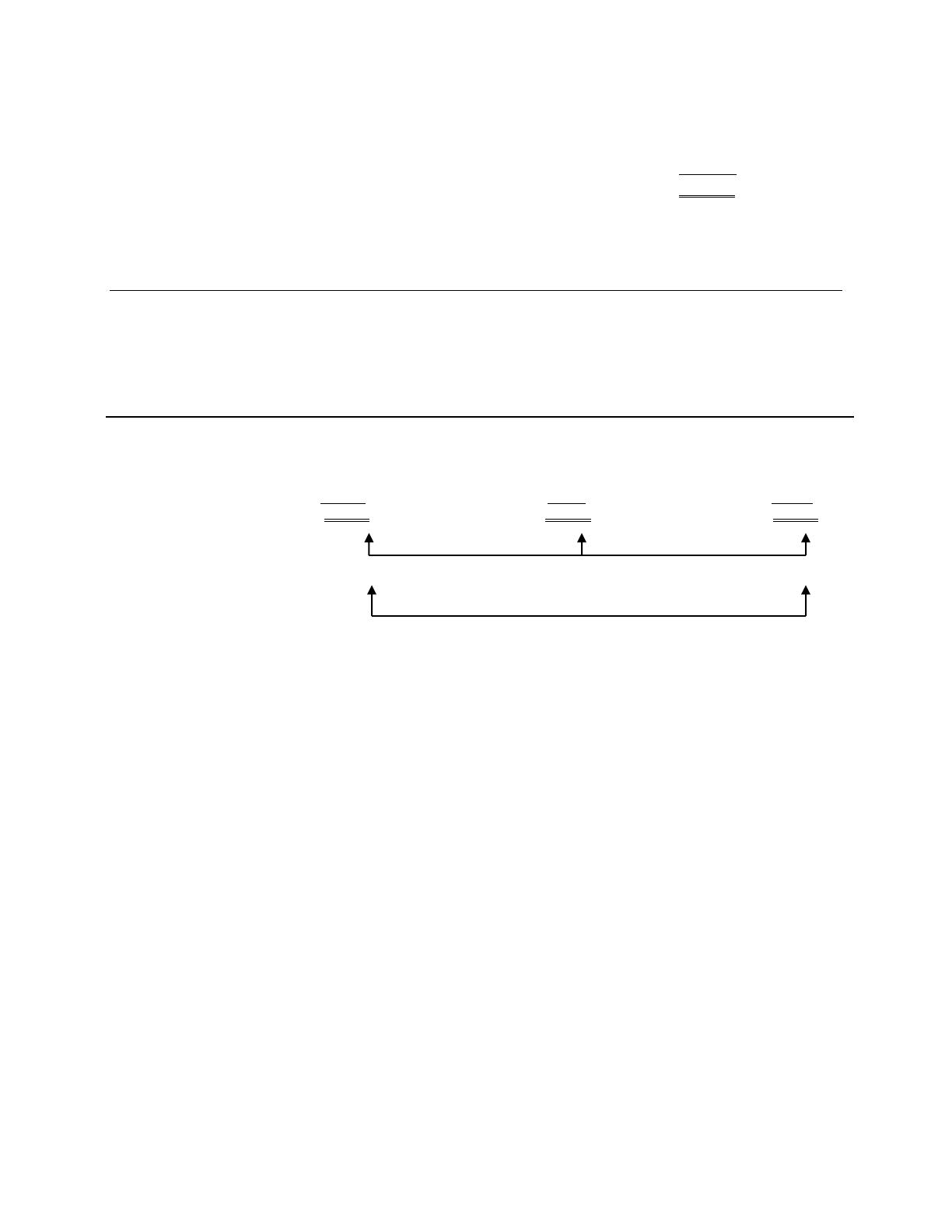

4. Solution Exhibit 7-35B presents the total direct materials yield and mix variances.

The total direct materials yield variance can also be computed as the sum of the direct

materials yield variances for each input:

Direct

materials

yield variance

for each input

=

Actual total Budgeted total quantity

quantity of all of all direct materials inputs

direct materials allowed for actual output

inputs used

−

×

Budgeted

direct materials

input mix

percentage

×

Budgeted

price of

direct materials

inputs

Almonds = (16,000 – 15,000) × 0.30a × $1 = 1,000 × 0.30 × $1 = $ 300 U

Cashews = (16,000 – 15,000) × 0.50b × $2 = 1,000 × 0.50 × $2 = 1,000 U

Pistachios = (16,000 – 15,000) × 0.15c × $3 = 1,000 × 0.15 × $3 = 450 U

Seasoning = (16,000 – 15,000) × 0.05d × $6 = 1,000 × 0.05 × $6 = 300 U

Total direct materials yield variance $2,050 U

a 180

600; b 300

600; c 90

600; d30

600

The total direct materials mix variance can also be computed as the sum of the direct materials

mix variances for each input:

Direct

materials

mix variance

for each input

=

Actual Budgeted

direct materials direct materials

input mix input mix

percentage percentage

−

×

Actual total

quantity of all

direct materials

inputs used

×

Budgeted

price of

direct materials

inputs

Almonds = (0.33 – 0.30) × 16,000 × $1 = 0.03 × 16,000 × $1 = $ 480 U

7-47

Cashews = (0.47 – 0.50) × 16,000 × $2 = –0.03 × 16,000 × $2 = 960 F

Pistachios = (0.17 – 0.15) × 16,000 × $3 = 0.02 × 16,000 × $3 = 960 U

Seasoning = (0.03 – 0.05) × 16,000 × $6 = –0.02 × 16,000 × $6 = 1,920 F

Total direct materials mix variance $ 1,440 F

• SOLUTION EXHIBIT 7-35B

Columnar Presentation of Direct Materials Yield and Mix Variances for Nature’s Best Company.

Actual Total Quantity

of All Inputs Used

× Actual Input Mix

× Budgeted Price

(1)

Actual Total Quantity

of All Inputs Used

× Budgeted Input Mix

× Budgeted Price

(2)

Flexible Budget:

Budgeted Total Quantity of

All Inputs Allowed for

Actual Output ×

Budgeted Input Mix

× Budgeted Price

(3)

Almonds 16,000 × 0.33 × $1 = $ 5,280

Cashews 16,000 × 0.47 × $2 = 15,040

Pistachios 16,000 × 0.17 × $3 = 8,160

Seasoning 16,000 × 0.03 × $6 = 2,880

$31,360

16,000 × 0.30 × $1 = $ 4,800

16,000 × 0.50 × $2 = 16,000

16,000 × 0.15 × $3 = 7.200

16,000 × 0.05 × $6 = 4,800

$32,800

15,000 × 0.30 × $1 = $ 4,500

15,000 × 0.50 × $2 = 15,000

15,000 × 0.15 × $3 = 6,750

15,000 × 0.05 × $6 = 4,500

$30,750

$1,440 F $2,050 U

Total mix variance Total yield variance

$610 U

Total efficiency variance

F = favorable effect on operating income; U = unfavorable effect on operating income.

The direct materials mix variance of $1,440 F indicates that the actual product mix uses relatively more

of less-expensive ingredients than planned. In this case, the actual mix contains slightly more almonds

and pistachios while using fewer cashews and substantially less seasoning.

The direct materials yield variance of $2,050 U occurs because the amount of total inputs needed

(16,000 cups) exceeded the budgeted amount (15,000 cups) expected to produce 2,500 tins.

The direct materials yield variance is significant enough to be investigated. The mix variance may be

within expectations but should be monitored since it is favorable largely due to the use of less

seasoning, which is considered an important element of the product’s appeal to customers.

7-48

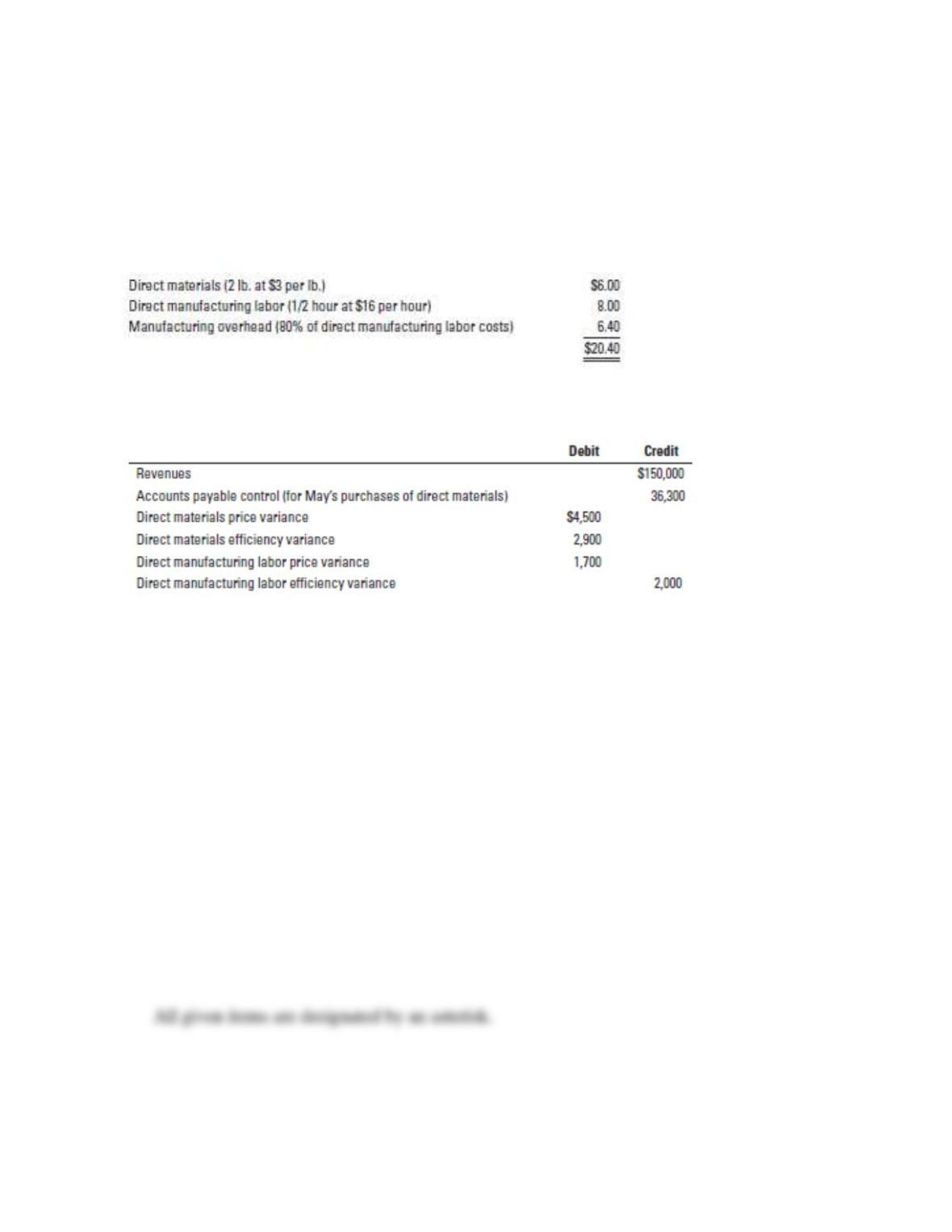

7-36 (20–30 min.) Direct materials and manufacturing labor variances, solving

unknowns.

(CPA, adapted) On May 1, 2014, Lowell Company began the manufacture of a new paging

machine known as Dandy. The company installed a standard costing system to account for

manufacturing costs. The standard costs for a unit of Dandy follow:

The following data were obtained from Lowell’s records for the month of May:

Actual production in May was 4,700 units of Dandy, and actual sales in May were 3,000 units.

The amount shown for direct materials price variance applies to materials purchased during

May.

There was no beginning inventory of materials on May 1, 2014.

Compute each of the following items for Lowell for the month of May. Show your computations.

Required:

1. Standard direct manufacturing labor-hours allowed for actual output produced

2. Actual direct manufacturing labor-hours worked

3. Actual direct manufacturing labor wage rate

4. Standard quantity of direct materials allowed (in pounds)

5. Actual quantity of direct materials used (in pounds)

6. Actual quantity of direct materials purchased (in pounds)

7. Actual direct materials price per pound

SOLUTION

7-49

7-50

7-37 (20 min.) Direct materials and manufacturing labor variances, journal entries.

Zanella’s Smart Shawls, Inc., is a small business that Zanella developed while in college. She

began hand-knitting shawls for her dorm friends to wear while studying. As demand grew, she

hired some workers and began to manage the operation. Zanella’s shawls require wool and labor.

She experiments with the type of wool that she uses, and she has great variety in the shawls she

produces. Zanella has bimodal turnover in her labor. She has some employees who have been

with her for a very long time and others who are new and inexperienced.

Zanella uses standard costing for her shawls. She expects that a typical shawl should take 3

hours to produce, and the standard wage rate is $9.00 per hour. An average shawl uses 13 skeins

of wool. Zanella shops around for good deals and expects to pay $3.40 per skein.

Zanella uses a just–in-time inventory system, as she has clients tell her what type and color of

wool they would like her to use.

For the month of April, Zanella’s workers produced 200 shawls using 580 hours and 3,500

skeins of wool. Zanella bought wool for $9,000 (and used the entire quantity) and incurred labor

costs of $5,520.

Required:

1. Calculate the price and efficiency variances for the wool and the price and efficiency

variances for direct manufacturing labor.

2. Record the journal entries for the variances incurred.

3. Discuss logical explanations for the combination of variances that Zanella experienced.

SOLUTION

7-51

7-52

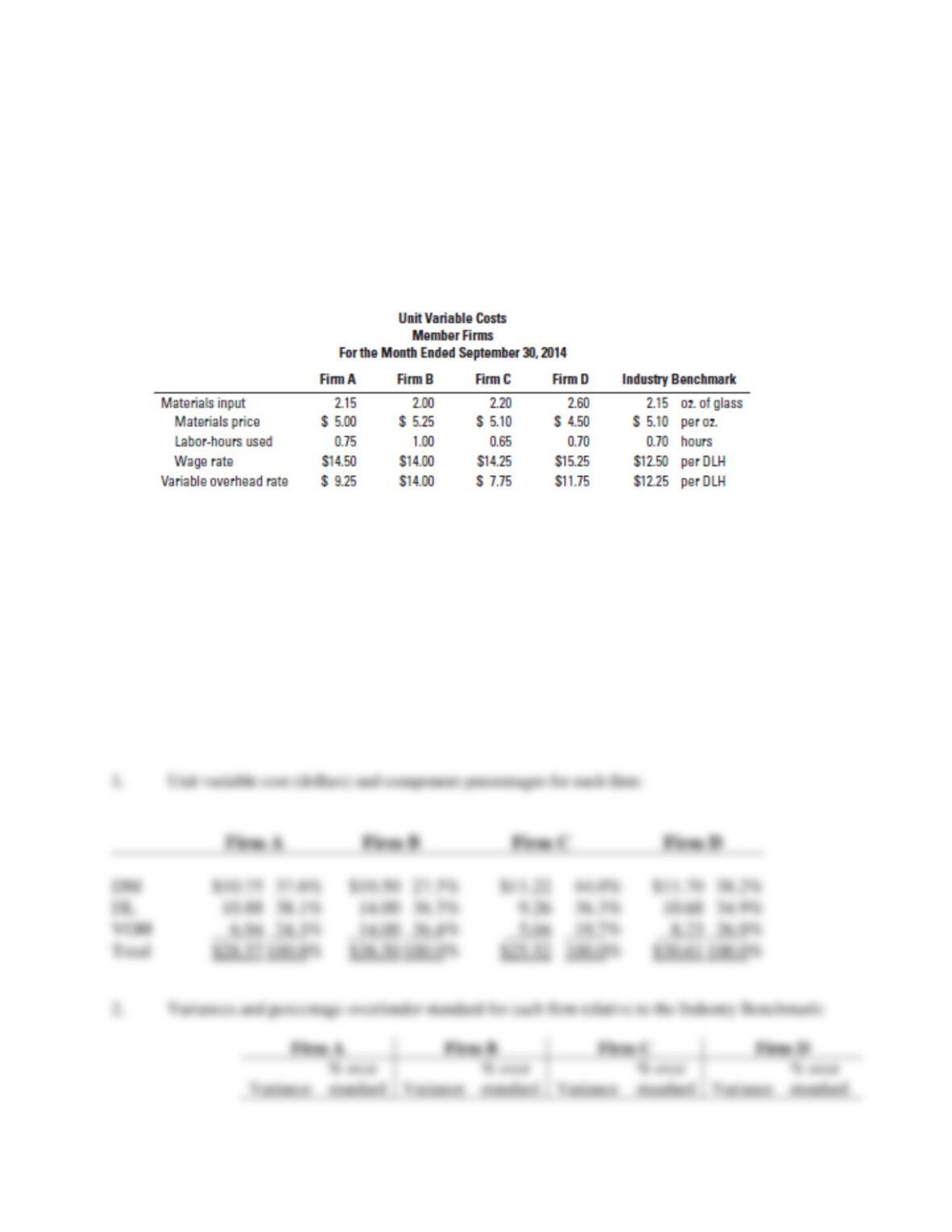

7-38 (30 min.) Use of materials and manufacturing labor variances for benchmarking.

You are a new junior accountant at In Focus Corporation, maker of lenses for eyeglasses. Your

company sells generic-quality lenses for a moderate price. Your boss, the controller, has given

you the latest month’s report for the lens trade association. This report includes information

related to operations for your firm and three of your competitors within the trade association. The

report also includes information related to the industry benchmark for each line item in the

report. You do not know which firm is which, except that you know you are Firm A.

Required:

1. Calculate the total variable cost per unit for each firm in the trade association. Compute the

percent of total for the material, labor, and variable overhead components.

2. Using the trade association’s industry benchmark, calculate direct materials and direct

manufacturing labor price and efficiency variances for the four firms. Calculate the percent

over standard for each firm and each variance.

3. Write a brief memo to your boss outlining the advantages and disadvantages of belonging to

this trade association for benchmarking purposes. Include a few ideas to improve

productivity that you want your boss to take to the department heads’ meeting.

SOLUTION

7-53

7-54