7–35 Ch. 7—Problems

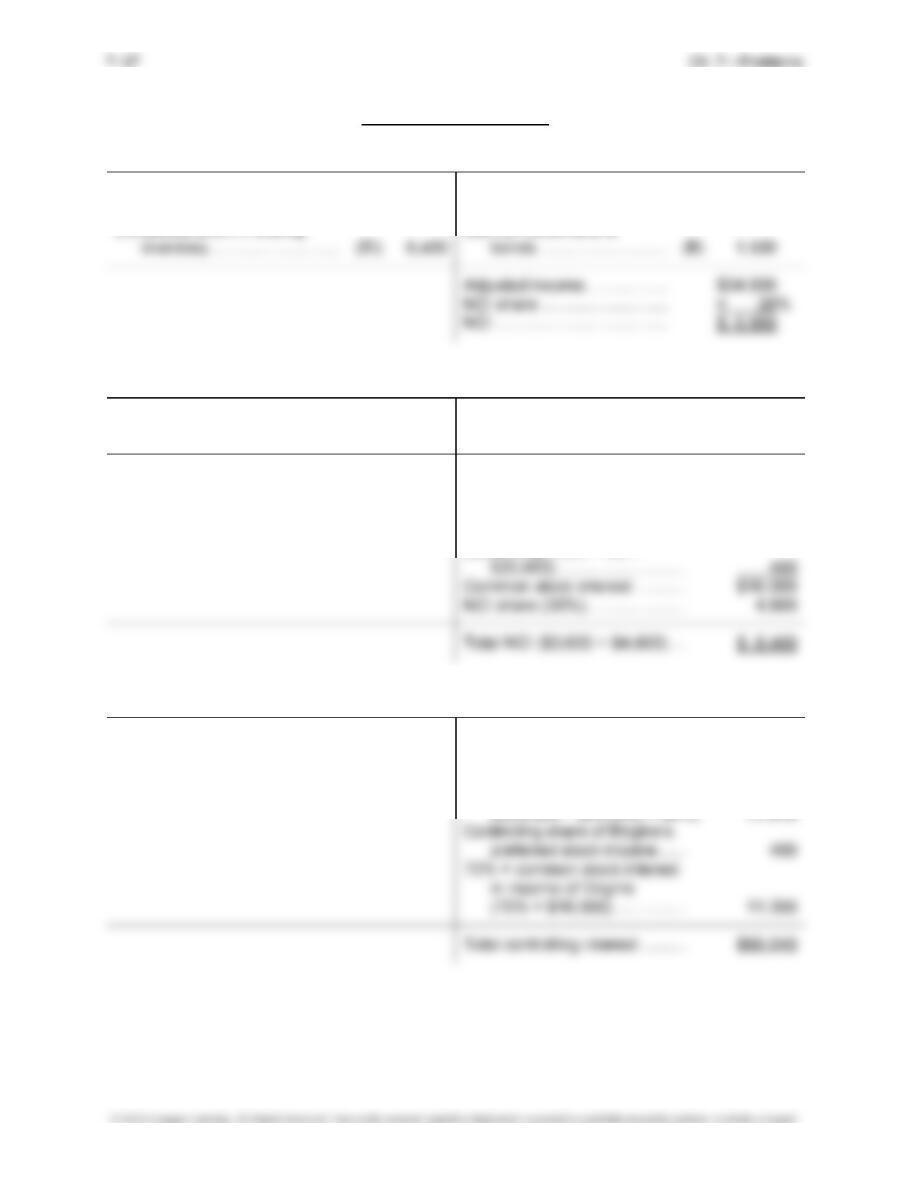

Problem 7-7, Continued

Titan Corporation and Subsidiaries Boat Corporation and Engine Corporation

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2018

(Concluded)

Eliminations Consolidated Controlling Consol.

Trial Balance

and Adjustments Income NCI NCI Retained Balance

Titan Boat Engine Dr. Cr. Statement Boat Engine Earnings Sheet

Retained Earnings (preferred)—

Engine …………………………….. …………….. ……………. …………… (PS2) 2,000 (PS1) 20,000 …………….. …………… (18,000) ……………. ……………..

Sales ……………………………………. (1,050,000) (500,000) (650,000) (IS) 22,400 …………. (2,177,600) …………… …………… ……………. ……………..

Subsidiary Income:

Common Stock—Boat ……….. (16,000) …………… …………… (CY1a) 16,000 …………. …………….. …………… …………… ……………. ……………..

Preferred Stock—Engine ……. (400) …………… …………… (PS) 400 …………. …………….. …………… …………… ……………. ……………..

Common Stock—Engine ……. (11,200) …………… …………… (CY1b) 11,200 …………. …………….. …………… …………… ……………. ……………..

Cost of Goods Sold ………………… 650,000 300,000 400,000 (EI) 6,400 (IS) 22,400 1,334,000 …………… …………… ……………. ……………..

Other Expenses …………………….. 358,500 160,000 230,000 ………….. (B) 750 747,750 …………… ..…………. ……………. ……………..

Dividends Declared ………………… 22,000 30,000 …………… ………….. (CY2) 24,000 …………….. 6,000 …………… 22,000 ……………..

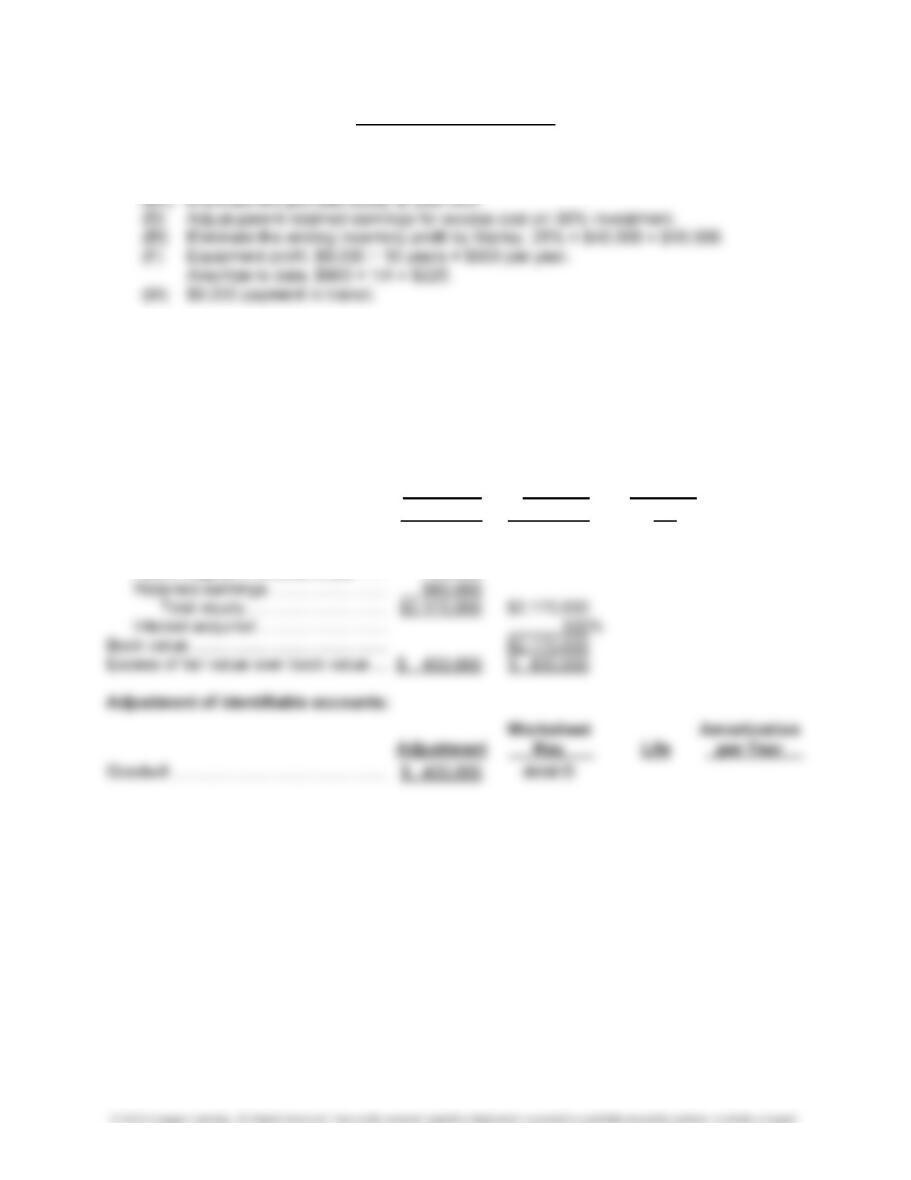

Problem 7-7, Continued

Eliminations and Adjustments:

(CY1a) Eliminate the current year’s income from the investment in Boat Corporation.

(CY1b) Eliminate the current year’s income from investment in Engine Corporation—

Common Stock.

(PS2) Eliminate the parent’s 10% interest in preferred stock and Retained Earnings

(preferred)—Engine, against Investment in Engine Corporation—Preferred Stock.

Eliminate the income from Preferred Stock—Engine against investment.

(EL2) Eliminate the parent’s interest in Engine Corporation common stock. Retained

earnings applicable to common stock:

$200,000 = $80,000. Parent’s share 70% × $80,000 = $56,000.

Gain remaining at year-end:

Carrying value of bonds at December 31, 2018 …………. $25,000

Investment in bonds at December 31, 2018 ………………. 23,800 $1,200

Gain amortized during the year:

Interest revenue eliminated ($750 stated interest for half

Problem 7-7, Concluded

Subsidiary Boat Corporation Income Distribution

Interest adjustment Internally generated net

($1,050 – $750) ……………… (B) $ 300 income ……………………… $40,000

Unrealized profit in ending Gain on retirement of

Subsidiary Engine Corporation Income Distribution

Internally generated net

income …………………………. $20,000

Adjusted income …………………. $20,000

Less preferred interest:

NCI [90% × ($50,000/$250,000)

× $20,000]……………………….. 3,600

Controlling (10% × 1/5 ×

Parent Titan Corporation Income Distribution

Internally generated net

income …………………………. $44,600

80% × Boat Corporation

income for one-half year

PROBLEM 7-8

(1)

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (60%) (40%)

Fair value of subsidiary …………………… $185,000 $111,000 $ 74,000

Less book value of interest acquired:

Common stock ($10 par) ……………. $100,000

Paid-in capital in excess of par …… 20,000

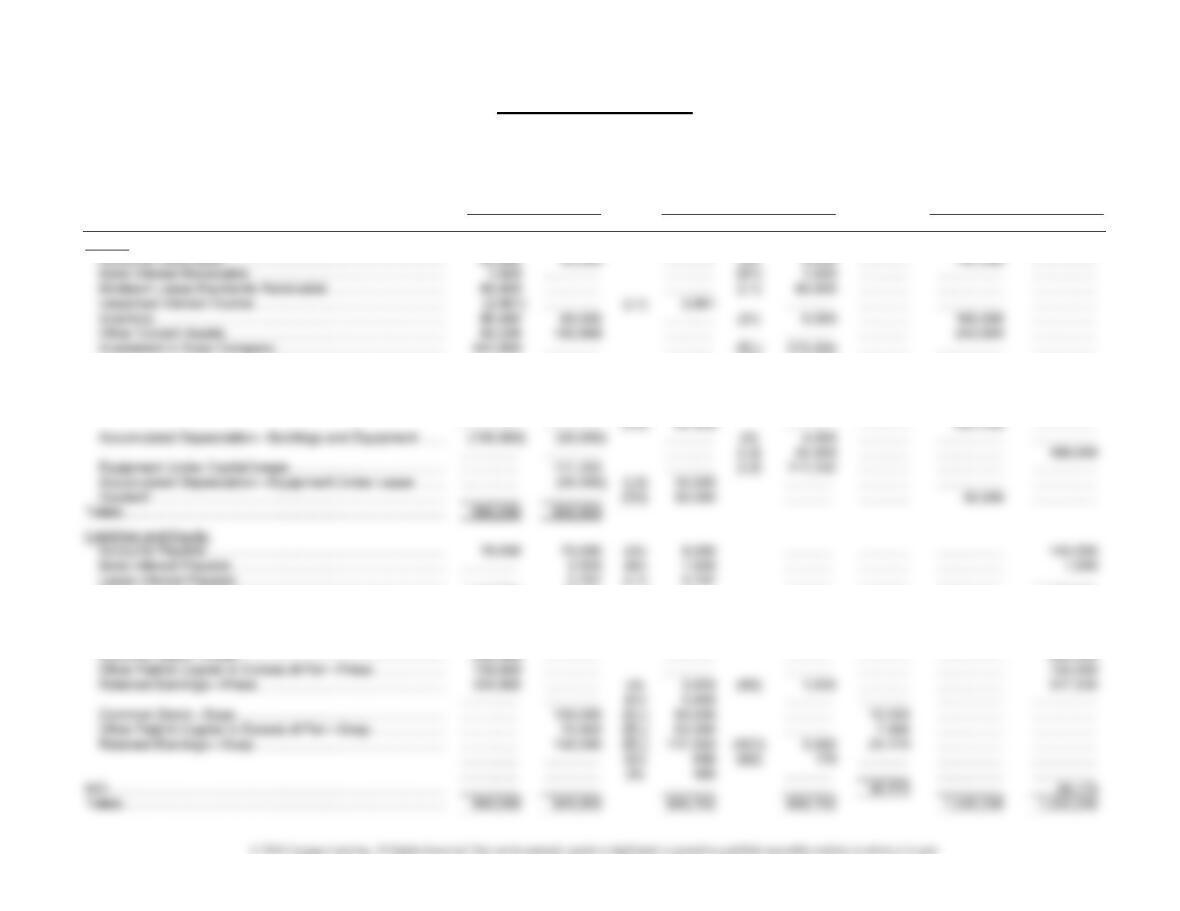

Problem 7-8, Continued

Black Jack Corporation and Subsidiary Zeppo Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2018

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Black Jack Zeppo Dr. Cr. Statement NCI Earnings Sheet

Cash …………………………………………………….. 30,400 10,000 …………….. …………….. …………….. …………….. …………….. 40,400

…………….. …………….. (F2) 1,000 …………….. …………….. …………….. …………..… (453,750)

Investment in Zeppo Preferred Stock ………… 56,000 …………….. …………….. (ELP) 56,000 …………..… …………….. …………….. ……………..

Investment in Zeppo Common Stock …………. 121,200 …………….. …………….. (CY1b) 3,600 …………….. …………….. …………….. ……………..

…………….. …………….. …………….. (ELC) 91,800 …………….. …………….. …………….. ……………..

…………….. …………….. …………….. (D) 25,800 …………….. …………….. …………..… ……………..

…………….. …………….. (ELC) 19,800 …………….. …………….. …………….. …………….. ……………..

…………….. …………….. (F1) 1,600 …………….. …………….. …………….. …………..… ……………..

…………….. …………….. (BI) 180 …………….. …………….. …………….. …………….. ……………..

…………….. …………….. (A) 2,150 …………….. …………….. …………….. …………..… ……………..

Problem 7-8, Continued

Black Jack Corporation and Subsidiary Zeppo Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2018

(Concluded)

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Black Jack Zeppo Dr. Cr. Statement NCI Earnings Sheet

Subsidiary Income—Preferred ………………….. (4,000) …………….. (CY1a) 4,000 …………… ………….…. …………….. …………….. ……………..

Subsidiary Income—Common ………………….. (3,600) …………….. (CY1b) 3,600 …………… …………….. …………….. …………….. ……………..

7–41 Ch. 7—Problems

Problem 7-8, Continued

Eliminations and Adjustments:

(CY1a) Eliminate the entries made concerning the investment in preferred stock during

2018.

(PS) Distribute retained earnings at the beginning of the year; preferred share is

$4,000 × 2 years of arrearage.

(ELP) Eliminate the investment in preferred stock:

Adjustment to paid-in capital in excess of par resulting from retirement

of preferred stock on January 1, 2017:

Price paid ………………………………………………….. $ 56,000

Book value:

(ELC) Eliminate 60% of subsidiary equity against the investment in common stock.

This equity includes 60% of the January 1, 2018, retained earnings applicable to

common stock ($41,000 less $8,000 preferred claim).

(D)/(NCI) Distribute the excess of book value to plant asset (see schedule).

(A) Amortize the decrease in depreciation for one past year and for the current year.

(F1) Eliminate the gain on equipment sale ($5,000), less one year’s depreciation of

$1,000 at the beginning of the year.

(F2) Decrease depreciation for the current year.

(IS) Eliminate intercompany sales.

(IA) Eliminate intercompany trade debt.

(BI) Eliminate the beginning inventory profit:

Problem 7-8, Concluded

Subsidiary Zeppo Company Income Distribution

Unrealized gross profit Internally generated

in ending inventory ………… (EI) $ 600 income …………………………. $10,000

Depreciation adjustment ……… (A) 5,375 Realized gross profit in

beginning inventory …… (BI) 450

Realized profit on

equipment sale ……….. (F1) 1,000

Parent Black Jack Corporation Income Distribution

Unrealized gross profit Internally generated

in ending inventory ………… (EI) $2,000 income ………………………………. $40,000

Share of Zeppo common income

(2) Entries to record sale:

(a) Adjust investment for amortization of excess cost:

Retained Earnings ($5,375 × 2 years × 60% ownership) ……… 6,450

Investment in Zeppo Common Stock …………………………….. 6,450

7–43 Ch. 7—Problems

APPENIDIX PROBLEMS

PROBLEM 7A-1

Analysis of 30% purchase

September 1, 2019:

Price paid …………………………………………………………….. $100,000

Less interest acquired:

Equity, December 31, 2019 ……………………………… $252,000

Add dividends declared December 31 ………………. 40,000

Deduct income for last 4 months ………………………. (32,000)

Marley Corporation and Subsidiary Foster Corporation

Worksheet for Consolidated Balance Sheet

December 31, 2019

Eliminations Consolidated

Balance Sheet

and Adjustments Balance

Marley Foster Dr. Cr. NCI Sheet

Cash …………………………………. 167,250 101,000 (IA) 8,000 ………….. ……………. 276,250

Accounts Receivable …………… 170,450 72,000 …………. (IA) 8,000 ……………. 234,450

Notes Receivable ……………….. 87,500 28,000 …………. ………….. ……………. 115,500

Accounts Payable ………………. (222,000) (76,000) …………. ………….. ……………. (298,000)

Notes Payable ……………………. (79,000) (89,000) …………. ………….. ……………. (168,000)

Dividends Payable ……………… …………… (40,000) (CY) 36,000 ………….. ……………. (4,000)

Common Stock ($10 par)—

Marley ……………………………. (400,000) …………… …………. ………….. ……………. (400,000)

Common Stock ($10 par)—

Foster …………………………….. …………… (100,000) (EL) 90,000 ………….. (10,000) ……………

Ch. 7—Problems 7–44

Problem 7A-1, Concluded

Eliminations and Adjustments:

(CY) Eliminate intercompany dividends.

PROBLEM 7A-2

(1)

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (100%) (0%)

Fair value of subsidiary …………………… $2,600,000 $2,600,000 NA

Less book value of interest acquired:

Common stock ($25 par) ……………. $1,000,000

Paid-in capital in excess of par …… 190,000

Problem 7A-2, Continued

Book, Inc. and Subsidiary Cray, Inc.

Worksheet for Consolidated Balance Sheet

December 31, 2014

Eliminations Consolidated

Trial Balance

and Adjustments Balance

Book Cray Dr. Cr. Sheet

Cash ………………………………….. 825,000 330,000 …………….. …………….. 1,155,000

Accounts and Other Current

Investment in Cray, Inc. ……….. 2,860,000 ………………. …………….. (EL) 2,430,000 ………………

……………… ………………. …………….. (D) 430,000 ………………

Long-Term Investments and

Other Assets ……………………. 865,000 385,000 …………….. (B1) 320,000 930,000

Accounts Payable and Other

Current Liabilities ……………… (2,465,000) (1,145,000) (IA) 720,000 …………….. ………………

……………… ………………. (B2) 8,000 …………….. (2,882,000)

Eliminations and Adjustments:

(EL) Eliminate the parent’s investment in the subsidiary and the subsidiary equity

accounts.

(D) Distribute excess to goodwill.

(B1) Eliminate the intercompany long-term debt. There is no adjustment to retained

earnings because issue and repurchase of the bonds were at face value.

(B2) Eliminate the intercompany receivable and payable for interest bonds (1/2 year ×

10% × 1/2 interest period × $320,000).

Problem 7A-2, Concluded

(2) Book, Inc. and Subsidiary Cray, Inc.

Consolidated Statement of Retained Earnings

December 31, 2014:

PROBLEM 7A-3

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (90%) (10%)

Fair value of subsidiary …………………… $360,000 $324,000 $ 36,000

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Land …………………………………………….. $ 20,000 debit D1

7–47 Ch. 7—Problems

Problem 7A-3, Continued

Press Company and Subsidiary Soap Company

Worksheet for Consolidated Balance Sheet

For Year Ended December 31, 2016

Eliminations Consolidated

Trial Balance

and Adjustments Balance Sheet

Press Soap Dr. Cr. NCI Dr. Cr.

Assets:

…………… …………… …………. (D) 81,000 …………. …………….. ……………..

Investment in Soap Bonds ………………………………………….. 59,225 …………… …………. (B2) 59,225 …………. …………….. ……………..

Land ………………………………………………………………………… 60,000 30,000 (D1) 20,000 ….……… …………. 110,000 ……………..

Buildings and Equipment …………………………………………….. 300,000 230,000 (L2) 111,332 …………. …………. …………….. ……………..

Other Current Liabilities ………………………………………………. 57,000 48,911 …………. …………. …………. …………….. 105,911

Lease Obligation Payable …………………………………………… …………… 71,332 (L1) 71,332 …….…… …………. …………….. ……………..

Bonds Payable ………………………………………………………….. 150,000 100,000 (B2) 60,000 …………. …………. …………….. 190,000

Premium on Bonds …………………………………………………….. …………… 1,550 (B2) 930 ……..….. …………. …………….. 620

Problem 7A-3, Concluded

Eliminations and Adjustments:

(EL) Eliminate 90% of the subsidiary equity accounts against the investment in subsidiary account.

(A) Depreciate the write-up to building for two years.

(EI) Eliminate the intercompany gross profit in the ending inventory.

(IA) Eliminate the intercompany receivable and payable.

(B2) Eliminate the bond investment against 60% of bonds payable and premium on bonds. The

(L1) Eliminate the lease payable (lease obligation payable plus lease interest payable) against the

lease receivable (minimum lease payments receivable less unearned interest income).

(L3) Reclassify the accumulated depreciation on the leased equipment.