Chapter 07 – Cost-Volume-Profit Analysis

7-1

CHAPTER 7

Cost-Volume-Profit Analysis

ANSWERS TO REVIEW QUESTIONS

7-1 a. In the contribution-margin approach, the break-even point in units is calculated

using the following formula:

expenses fixed

point even–Break =

7-2 The term unit contribution margin refers to the contribution that each unit of sales

7-3 In addition to the break-even point, a CVP graph shows the impact on total expenses,

7-5 An increase in the fixed expenses of any enterprise will increase its break-even

7-6 A decrease in the variable expense per pound of oysters results in an increase in the

Chapter 07 – Cost-Volume-Profit Analysis

7-2

7-7 The president is correct. A price increase results in a higher unit contribution

margin. An increase in the unit contribution margin causes the break-even point to

7-8 When the sales price and unit variable cost increase by the same amount, the unit

7-11 The most important assumptions of a cost-volume-profit analysis are as follows:

(a) The behavior of total revenue is linear (straight line) over the relevant range. This

7-12 Operating managers frequently prefer the contribution income statement because it

Chapter 07 – Cost-Volume-Profit Analysis

7-3

7-13 The gross margin is defined as sales revenue minus all variable and fixed

7-14 East Company, which is highly automated, will have a cost structure dominated by

fixed costs. West Company’s cost structure will include a larger proportion of

7-15 When sales volume increases, Company X will have a higher percentage increase in

profit than Company Y. Company X’s higher proportion of fixed costs gives the firm

7-16 The sales mix of a multiproduct organization is the relative proportion of sales of its

products.

7-17 The car rental agency’s sales mix is the relative proportion of its rental business

7-18 Cost-volume-profit analysis shows the effect on profit of changes in expenses, sales

7-4

7-19 Budgeting begins with a sales forecast. Cost-volume-profit analysis can be used to

determine the profit that will be achieved at the budgeted sales volume. A CVP

7-20 The low-price company must have a larger sales volume than the high-price

company. By spreading its fixed expense across a larger sales volume, the low-price

firm can afford to charge a lower price and still earn the same profit as the high-price

company. Suppose, for example, that companies A and B have the following

expenses, sales prices, sales volumes, and profits.

Company A

Company B

Sales revenue:

350 units at $10 ……………………………………….

$3,500

7-21 The statement makes three assertions, but only two of them are true. Thus, the

statement is false. A company with an advanced manufacturing environment

7-22 Activity-based costing (ABC) results in a richer description of an organization’s cost

Chapter 07 – Cost-Volume-Profit Analysis

7-5

SOLUTIONS TO EXERCISES

EXERCISE 7-23 (20 MINUTES)

1. Break-even point (in units) =

margin oncontributiunit

expenses fixed

2. Contribution-margin ratio =

price salesunit

margin oncontributiunit

3. Break-even point (in sales dollars) =

ratio margin–oncontributi

expenses fixed

4. Let X denote the sales volume of pizzas required to earn a target net profit of

$60,000.

7-6

EXERCISE 7-24 (25 MINUTES)

Sales

Revenue

Variable

Expenses

Total

Contribution

Margin

Fixed

Expenses

Net

Income

Break-Even

Sales

Revenue

1

$360,000

$120,000

$240,000

$90,000

$150,000

$135,000 a

2

55,000

44,000

3

4

30,000

Explanatory notes for selected items:

cBreak-even sales revenue ……………………………………………………….……………

$80,000

$20,000

Therefore, variable expenses are 25 percent of sales revenue.

When variable expenses amount to $80,000, sales revenue is $320,000.

Chapter 07 – Cost-Volume-Profit Analysis

7-7

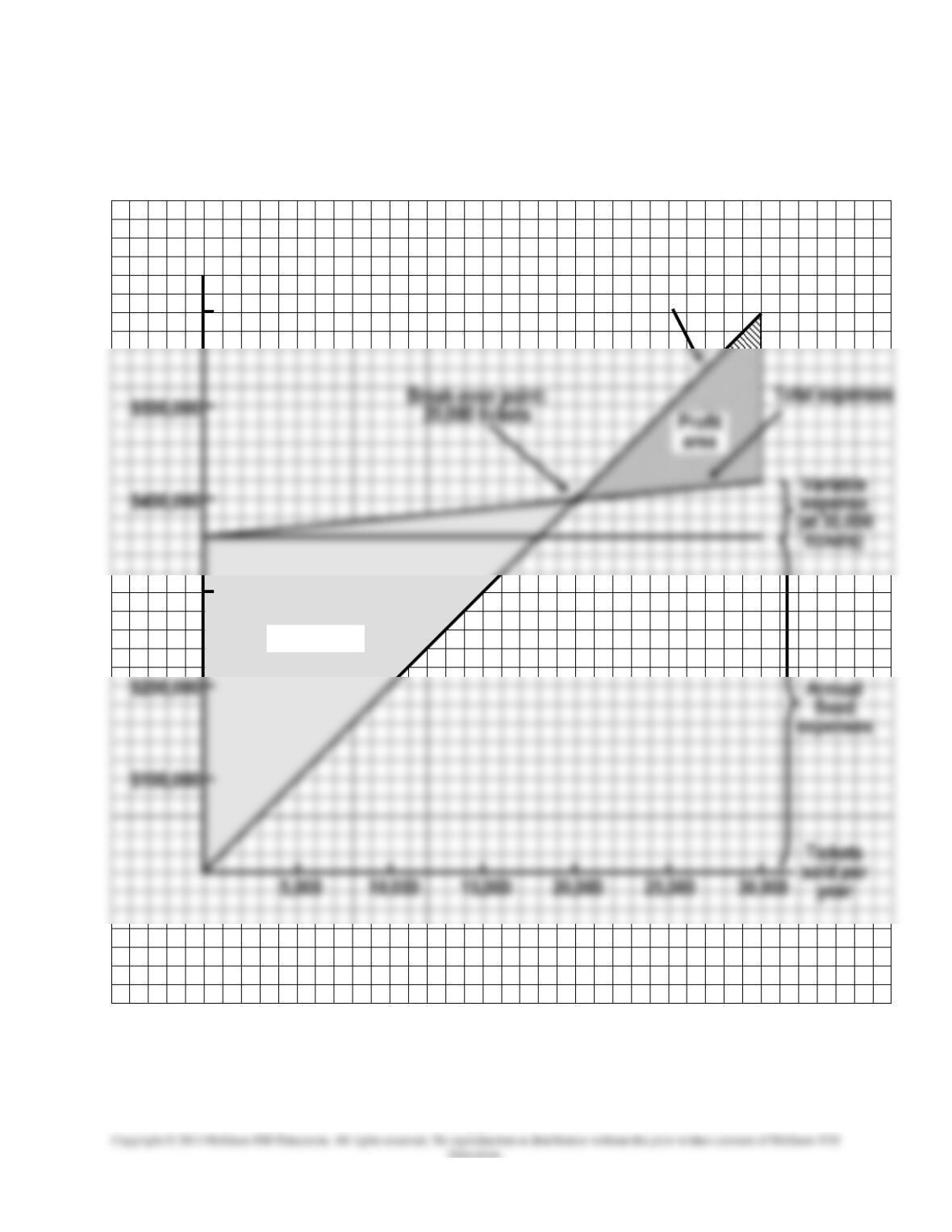

EXERCISE 7-25 (25 MINUTES)

1. Cost-volume-profit graph:

$500,000

$400,000

Total revenue

$200,000

$100,000

Dollars per year

$600,000

$300,000

Loss area

Chapter 07 – Cost-Volume-Profit Analysis

7-8

EXERCISE 7-25 (CONTINUED)

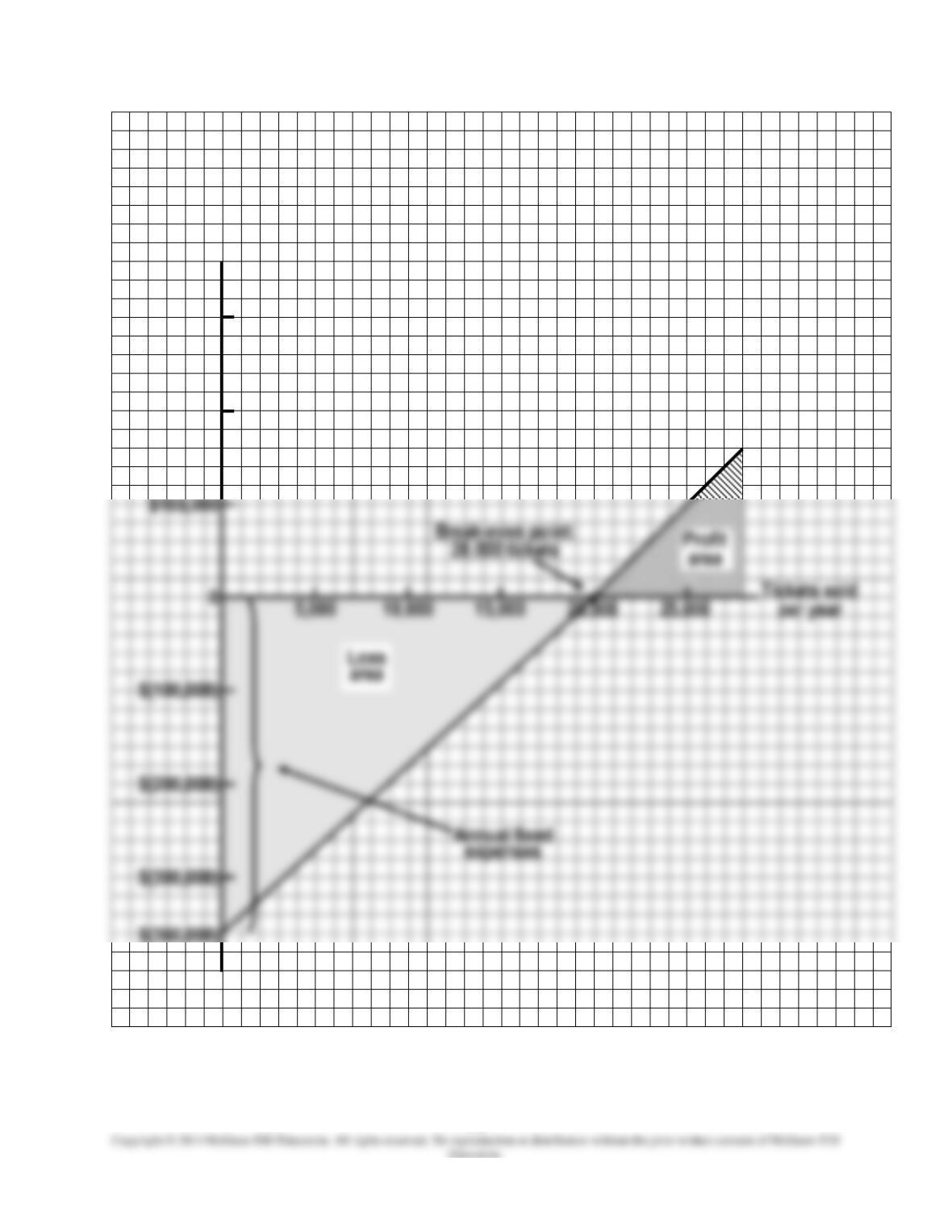

EXERCISE 7-26 (25 MINUTES)

Chapter 07 – Cost-Volume-Profit Analysis

7-9

Dollars per year

$300,000

$200,000

$100,000

$(300,000)

Chapter 07 – Cost-Volume-Profit Analysis

EXERCISE 7-26 (CONTINUED)

2.

Safety margin:

Budgeted sales revenue

Break-even sales revenue

Safety margin …………………………………………………………………………………….

3.

Let P denote the break-even ticket price, assuming a 10-game season and 40 percent

attendance:

7-11

EXERCISE 7-27 (25 MINUTES)

1. Break-even point (in units) =

margin oncontributiunit

costs fixed

2. New break-even point (in units) =

pp

p

1,000 1,500

(1.05) )(2,000,000

−

3. Sales revenue (7,000 1,500p) …………………………………………. 10,500,000p

p

2,000,000

5. Analysis of price change decision:

Price

1,500p

1,400p

Sales revenue: (7,000 1,500p) …………………………..

10,500,000p

Chapter 07 – Cost-Volume-Profit Analysis

EXERCISE 7-28 (25 MINUTES)

1. (a) Traditional income statement:

PACIFIC RIM PUBLICATIONS, INC.

INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 20XX

Sales ……………………………………………………….……… $1,000,000

(b) Contribution income statement:

PACIFIC RIM PUBLICATIONS, INC.

INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 20XX

Sales ……………………………………………………….……… $1,000,000

Less: Variable expenses:

Chapter 07 – Cost-Volume-Profit Analysis

7-13

EXERCISE 7-28 (CONTINUED)

3.

=factor leverage

operating

revenue sales in

increase percentage

incomenet in increase Percentage

4.

Most operating managers prefer the contribution income statement for answering this

EXERCISE 7-29 (30 MINUTES)

Chapter 07 – Cost-Volume-Profit Analysis

7-14

EXERCISE 7-30 (30 MINUTES)

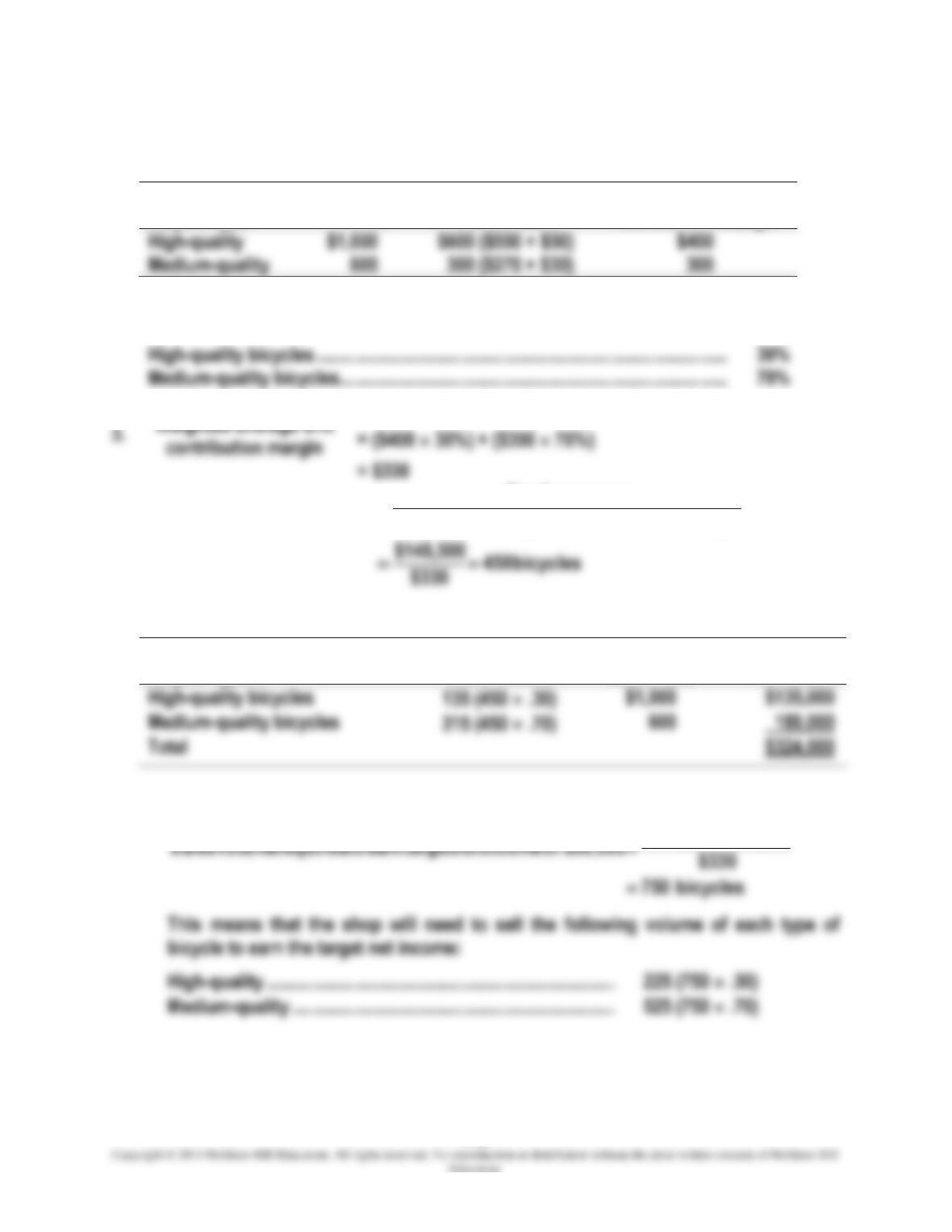

1.

Bicycle Type

Sales

Price

Unit

Variable Cost

Unit

Contribution Margin

High-quality

$600 ($550 + $50)

Medium-quality

300 ($270 + $30)

2.

Sales mix:

High-quality bicycles …………………………………………………………………………….

30%

Medium-quality bicycles ………………………………………………………………………..

70%

= $330

4.

margin oncontributiunit average–weighted

expenses fixed

units) (inpoint even–Break

=

Bicycle Type

Break-Even

Sales Volume

Sales Price

Sales

Revenue

5. Target net income:

$99,00048,5001$

+

Chapter 07 – Cost-Volume-Profit Analysis

7-15

EXERCISE 7-31 (25 MINUTES)

1. The following income statement, often called a common-size income statement,

provides a convenient way to show the cost structure.

Amount

Percent

Revenue ……………………………………………………..

$1,500,000

100

Variable expenses ……………………………………….

Contribution margin …………………………………….

$600,000

Fixed expenses …………………………………………..

2.

Decrease in

Revenue

Contribution Margin

Percentage

Decrease in

Net Income

3.

incomenet

margin oncontributi

)$1,500,000 of revenue(at factor leverage Operating

=

4.

factor

leverage operating

revenue in

increase percentage

incomenet in change Percentage

=

Chapter 07 – Cost-Volume-Profit Analysis

7-16

EXERCISE 7-32 (10 MINUTES)

Requirement (1)

Requirement (2)

Revenue ……………………………………………….

$1,875,000

$1,500,000

Less: Variable expenses………………………

1,125,000

Contribution margin ……………………………..

$ 750,000

$ (300,000)

Less: Fixed expenses ………………………….

675,000

350,000

EXERCISE 7-33 (20 MINUTES)

1.

ratio margin oncontributi

expenses fixed

revenue service of volumeeven–Break

=

2.

rate tax 1

incomenet tax–aftertarget

income tax–beforeTarget

−

=

3.

Service revenue required to earn

target after-tax income of

ratio margin oncontributi

) (1

incomenet tax–aftertarget

expenses fixed

−

+

=t

Chapter 07 – Cost-Volume-Profit Analysis

7-17

SOLUTIONS TO PROBLEMS

PROBLEM 7-34 (30 MINUTES)

1.

Break-even point in sales dollars, using the contribution-margin ratio:

ratio margin–oncontributi

expenses fixed

point even–Break

=

2.

Target net income, using contribution-margin approach:

margin oncontributiunit

incomenet target expenses fixed

$540,000 of income earn torequired units Sales

+

=

3.

New unit variable manufacturing cost

= $12 110%

Chapter 07 – Cost-Volume-Profit Analysis

7-18

PROBLEM 7-34 (CONTINUED)

4.

Let P denote the selling price that will yield the same contribution-margin ratio:

$6.00 $13.20

$30.00

$6.00 $12.00 $30.00

−−

=

−−

P

P

Check: New contribution-margin ratio is:

Chapter 07 – Cost-Volume-Profit Analysis

7-19

PROBLEM 7-35 (30 MINUTES)

1.

margin oncontributiunit

costs fixed

units) (inpoint even–Break

=

2.

ratio margin–oncontributi

cost fixed

dollars) sales (inpoint even–Break

=

3.

Number of sales units required to

earn target net profit

margin oncontributiunit

profitnet target costs fixed

+

=

4.

Margin of safety

= budgeted sales revenue – break-even sales revenue

= (140,000)($25) – $3,375,000 = $125,000

5.

Break-even point if direct-labor costs increase by 10 percent:

New unit contribution margin

= $25.00 – $8.20 – ($4.00)(1.10) – $6.00 – $1.60

Chapter 07 – Cost-Volume-Profit Analysis

7-20

PROBLEM 7-35 (CONTINUED)

6.

Contribution-margin ratio

price sales

margin oncontributiunit

=

Let P denote sales price required to maintain a contribution-margin ratio of .208. Then

P is determined as follows:

.208

$1.60$6.0010)($4.00)(1.$8.20

=

−−−−

P

(rounded) .208

=