Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Exercise 9-14

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Face Amount

x Stated Rate

Carrying Value

x Market Rate

(3) – (2)

Prior Carrying

Value + (4)

Requirement 2

January 1, 2018

Cash

186,580

Bonds Payable

186,580

(To record the bond issue)

Exercise 9-15

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

Face Amount

x Stated Rate

Carrying Value

x Market Rate

(2) – (3)

Prior Carrying

Value – (4)

Requirement 2

January 1, 2018

Cash

214,720

Bonds Payable

214,720

(To record the bond issue)

Exercise 9-16

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Face Amount

x Stated Rate

Carrying Value

x Market Rate

(3) – (2)

Prior Carrying

Value + (4)

1/ 1 /18

$ 466,024

6/30/18

$ 17,500

$ 18,641

$ 1,141

467,165

Requirement 2

If the market rate drops to 6%, it will cost $531,403 to retire the bonds.

Calculator Input

Bond

characteristics

Key

Amount

1. Face amount

FV

$500,000

Calculator Output

Issue price

PV

$531,403

December 31, 2019

Bonds Payable

470,869

Exercise 9-17

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

Face Amount

x Stated Rate

Carrying Value

x Market Rate

(2) – (3)

Prior Carrying

Value – (4)

1/ 1 /18

$ 214,877

6/30/18

$ 7,000

$ 6,446

$ 554

214,323

12/31/18

7,000

6,430

570

213,753

Requirement 2

If the market rate increases to 8%, it will cost $189,437 to retire the bonds.

Calculator Input

Bond

Characteristics

Key

Amount

2. Interest payment each period

PMT

$7,000

= $200,000 x 7% x ½ year

4. Periods to maturity

N

14

= 7 years x 2 periods each year

Calculator Output

December 31, 2018

Bonds Payable

211,296

Exercise 9-18

Requirement 1

($ in thousands)

Total

Liabilities

÷

Stockholders’

Equity

=

Debt to Equity

Ratio

E-Travel

$3,984,378

÷

$2,672,544

=

1.49

Requirement 2

($ in thousands)

Net Income +

Interest + Taxes

÷

Interest

=

Times Interest

Earned Ratio

E-Travel

$608,270

÷

$66,428

=

9.2

Chapter 07 - Long-Term Assets

Chapter 10

Stockholders’ Equity

Exercise 10-1

Terms

__g___ 1. Limited liability company

Definitions

a. Allows for legal treatment as a corporation, but tax treatment as a partnership.

Exercise 10-2

Authorized stock is the number of shares the company is authorized to sell, stated in

the company’s articles of incorporation.

Exercise 10-3

Requirement 1

January 1, 2018

Cash (500 shares x $20)

10,000

Requirement 2

January 1, 2018

Cash (500 shares x $20)

10,000

Common Stock (500 shares x $1.00)

500

April 1, 2018

Cash (200 shares x $24)

4,800

Exercise 10-4

Requirement 1

Preferred dividends in arrears for 2017

$12,000

Requirement 2

Preferred dividends in arrears for 2017

$ 0

Exercise 10-5

February 1

Debit

Credit

Cash (4,000 x $12)

48,000

Common Stock (4,000 x $12)

48,000

(Issue common stock no-par value))

May 15

Cash (1,000 x $11)

11,000

October 1

Dividends (5,000 shares x $1.00)

5,000

October 15

No Entry

October 31

Exercise 10-6

January 2, 2018

Debit

Credit

Cash (100,000 x $15)

1,500,000

Common Stock (100,000 x $1)

100,000

February 6, 2018

Cash (200 x $120)

24,000

September 10, 2018

Treasury Stock (10,000 shares x $18)

180,000

December 15, 2018

Cash (5,000 shares x $20)

100,000

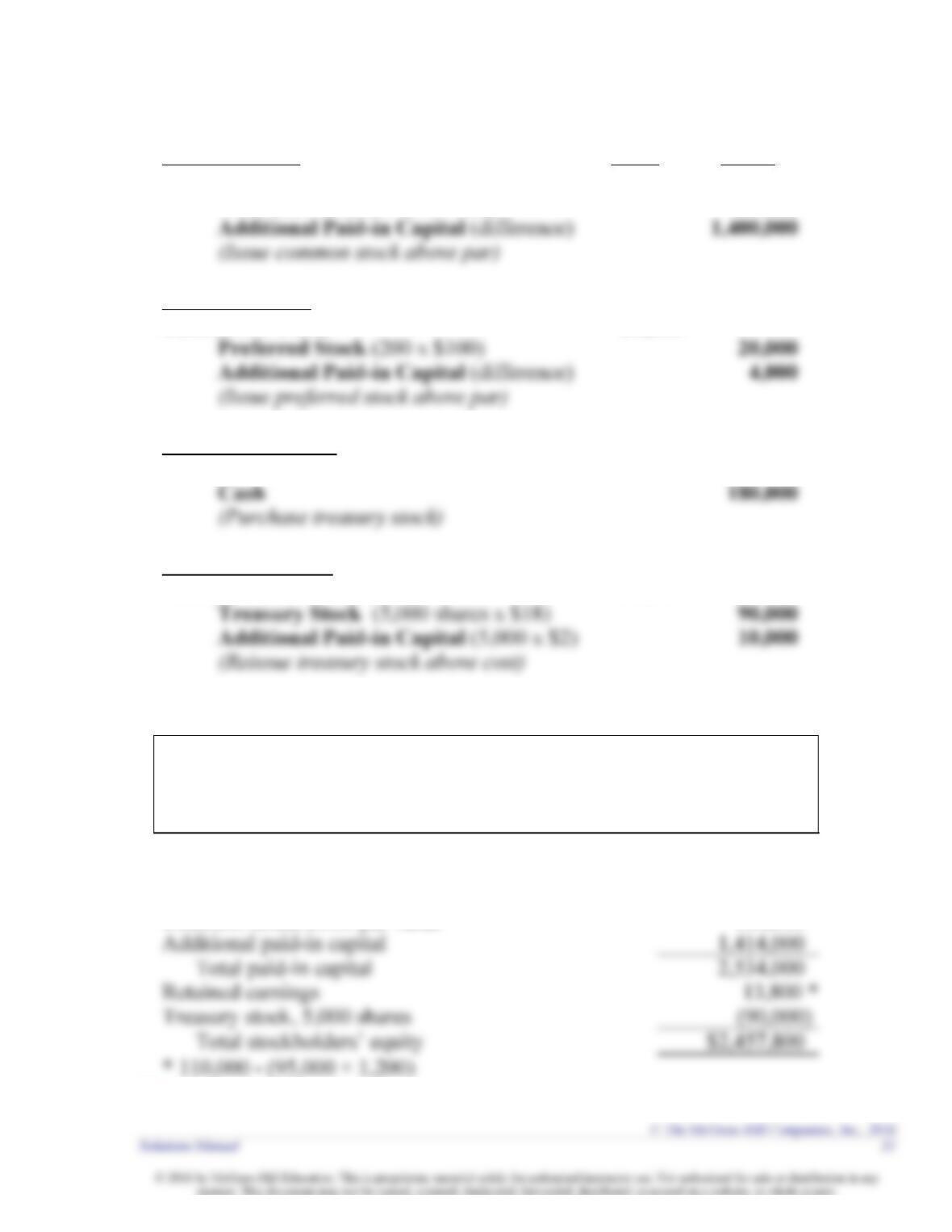

Exercise 10-7

Finishing Touches

Balance Sheet

(Stockholders’ Equity Section)

December 31, 2018

Stockholders’ equity:

Preferred stock, $100 par value

$ 20,000

Common stock, $1.00 par value

100,000

Exercise 10-8

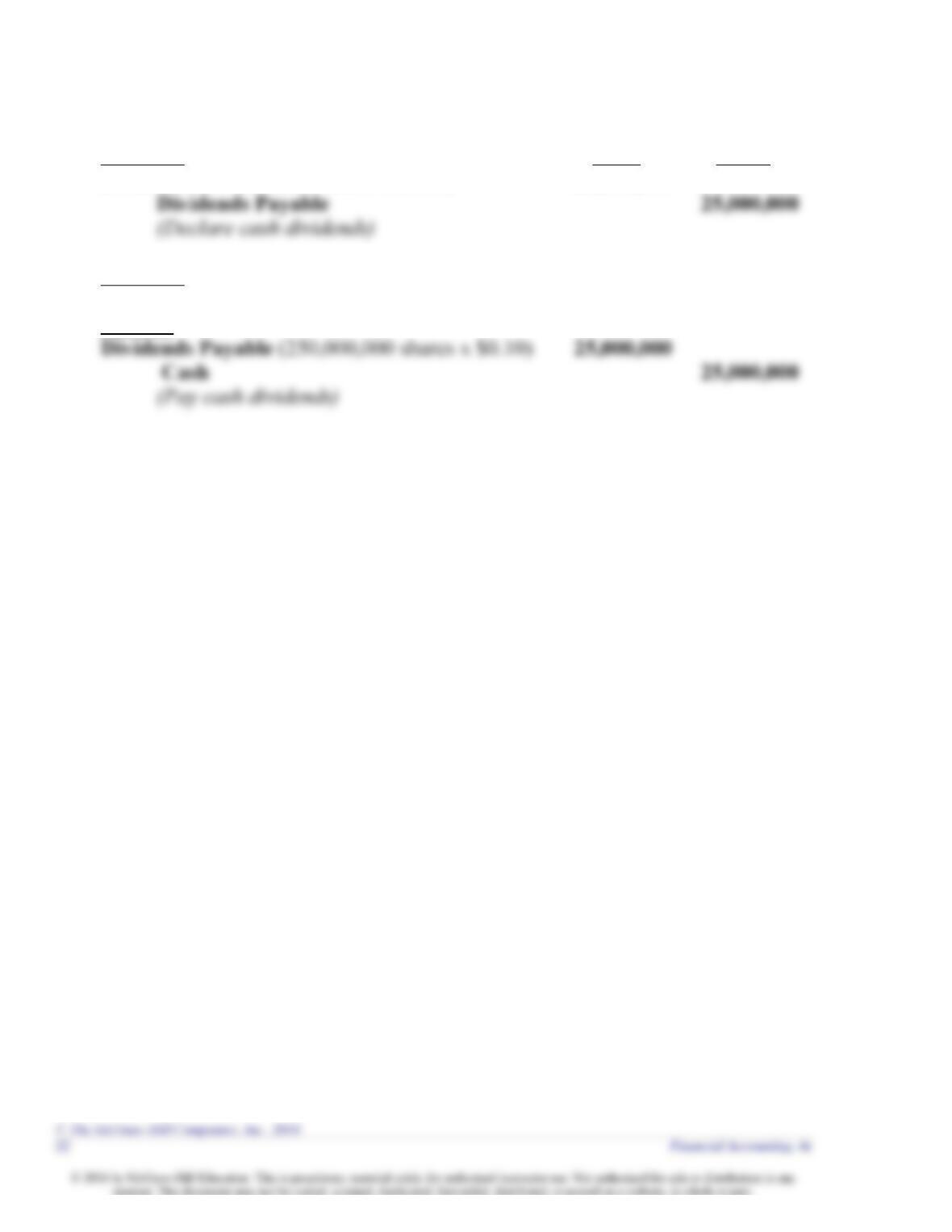

Chapter 07 - Long-Term Assets

March 15

Debit

Credit

Dividends (250,000,000 shares x $0.10)

25,000,000

March 30 - No Entry

April 13

Exercise 10-9

March 1, 2018

Debit

Credit

Cash (25,000 x $18)

450,000

Common Stock (25,000 x $1)

25,000

May 10, 2018

June 1, 2018

Dividends (219,000 shares x $1.00)

219,000

July 1, 2018

Dividends Payable (219,000 shares x $1.00)

219,000

October 21, 2018

Cash (4,000 shares x $25)

100,000

Exercise 10-10 (LO 10-6)

Requirement 1

September 1

Stock Dividends (20,000 x 5% x $40)

40,000

Requirement 2

September 1

Stock Dividends (20,000 shares x $1)

20,000

Requirement 3

• No entry is recorded for a 2-for-1 stock split, because the balance in all of the

Exercise 10-11

Power Drive Corporation

Balance Sheet

(Stockholders’ Equity Section)

December 31, 2018

Stockholders’ equity:

Common stock, $1.00 par value

$ 225,000

Additional paid-in capital

4,245,000

Exercise 10-12

Power Drive Corporation

Statement of Stockholders’ Equity

For the Year Ended December 31, 2018

Common

Stock

Additional

Paid-in

Capital

Retained

Earnings

Treasury

Stock

Total

Stockholders’

Equity

Exercise 10-13

Transaction

Total

Assets

Total

Liabilities

Total

Stockholders’

Equity

Issue common stock

+

NE

+

Exercise 10-14

United Apparel

Balance Sheet

(Stockholders’ Equity Section)

December 31, 2018

Stockholders’ equity:

Preferred stock

$ 1,500,000

Common stock

600,000

Exercise 10-15

Requirement 1

($ in millions)

Net Income

÷

Average

Stockholders’ Equity

=

Return on

Equity

Requirement 2

($ in millions)

Dividends

Per Share

÷

Stock Price

=

Dividend

Yield

Requirement 3

($ in millions)

Net Income

÷

Shares Outstanding

=

Earnings per Share

Requirement 4

($ in millions)

Stock Price

÷

Earnings Per Share

=

Price-Earnings

Ratio

Exercise 10-16

Requirement 1

Chapter 07 - Long-Term Assets

($ in millions)

Net Income

(less preferred

stock dividends)

÷

Average

Shares

Outstanding

=

Earnings per

Share

2017

$450

÷

340

=

$1.32

Requirement 2

($ in millions)

Stock Price

÷

Earnings Per

Share

=

Price-Earnings

Ratio

2017

$18.60

÷

$1.32

=

14.1

Chapter 11

Statement of Cash Flows

Exercise 11-1

Items

__e__ 1. Indirect method

__d__ 2. Direct method

Descriptions

a. Cash transactions involving net income.

b Cash transactions for the purchase and sale of long-term assets.

Exercise 11-2

The $10,000 decrease in notes receivable should be properly recorded as an increase

in cash from investing activities. While most changes in current assets and current

liabilities are included in operating activities, loaning money to a supplier is clearly an

investing activity.

Exercise 11-3

1. Operating activities