CHAPTER 7

Accounting Information Systems

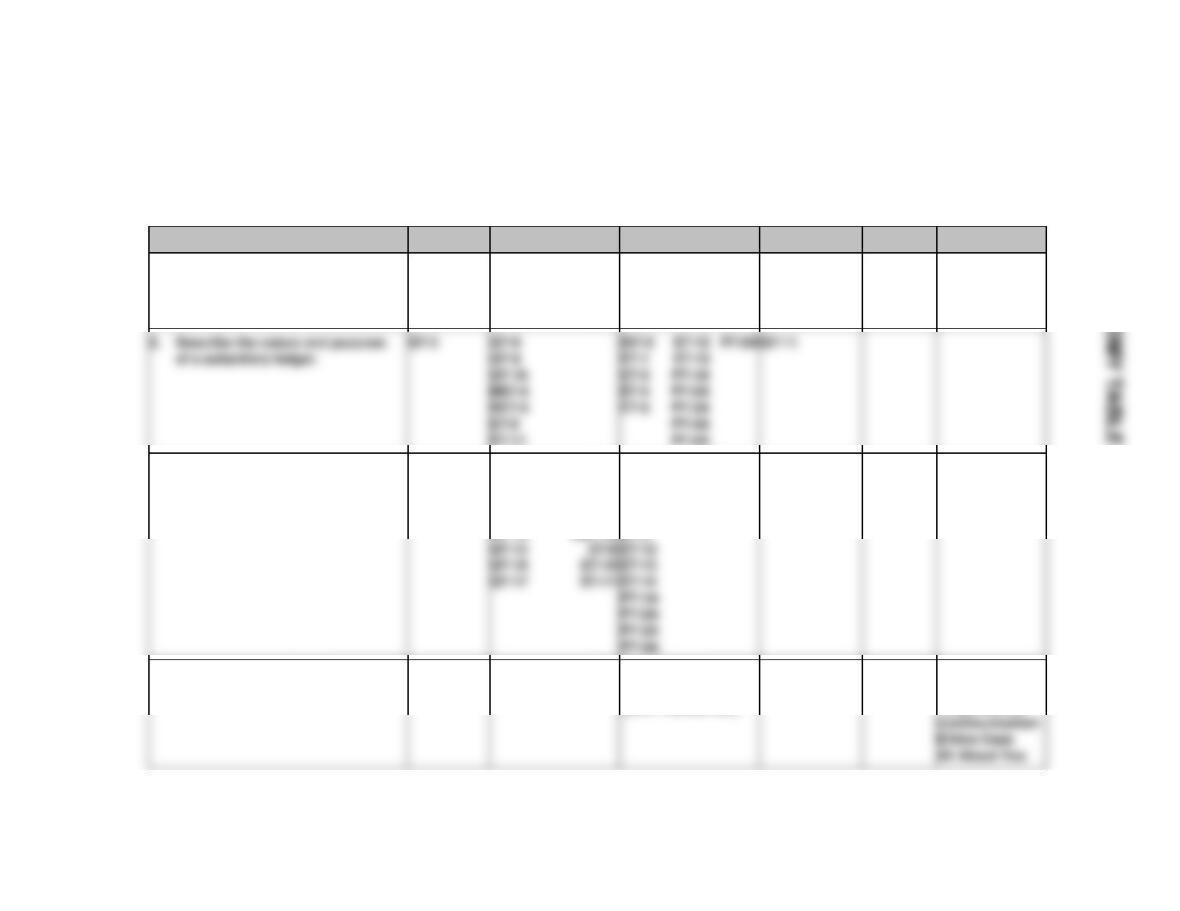

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Explain the basic concepts of

an accounting information

system.

1, 2, 3, 4

1, 2, 3

1

2. Describe the nature and

5, 6, 9, 11,

4, 5

2

1, 2, 3, 4, 5,

1A, 2A, 3A,

3. Record transactions in special

7, 8, 10, 11,

6, 7, 8, 9, 10

3

1, 3, 6, 7, 8,

1A, 2A, 3A,

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Journalize transactions in cash receipts journal;

post to control account and subsidiary ledger.

Simple

30–40

2A

Journalize transactions in cash payments journal;

post to control account and subsidiary ledgers.

Simple

30–40

5A

Journalize in sales and cash receipts journals; post;

prepare a trial balance; prove control to subsidiary;

prepare adjusting entries; prepare an adjusted

trial balance.

Moderate

60–70

WEYGANDT ACCOUNTING PRINCIPLES 12E

CHAPTER 7

ACCOUNTING INFORMATION SYSTEMS

Number

LO

BT

Difficulty

Time (min.)

BE1

1

C

Simple

1–2

BE2

1

C

Simple

2–4

BE3

1

C

Simple

2–3

BE4

2

C

Simple

6–8

BE5

2

C

Simple

2–3

BE6

3

C

Simple

2–4

BE7

3

C

Simple

2–4

BE8

3

C

Simple

2–4

BE9

3

C

Simple

3–5

BE10

3

C

Simple

3–5

DI1

1

C

Simple

3–5

DI2

2

AP

Simple

6–8

DI3

3

K

Simple

2–4

EX1

2, 3

AP

Simple

6–8

EX2

2

C

Simple

6–8

EX3

2, 3

AP

Simple

10–12

EX4

2

AP

Simple

6–8

EX5

2

AP

Simple

6–8

EX6

3

AP

Simple

6–8

EX7

3

AP

Simple

8–10

EX8

3

C

Simple

EX9

3

AP

Simple

8–10

EX10

3

C

Simple

6–8

EX11

2, 3

C

6–8

EX12

2, 3

AP

Simple

8–10

EX13

AP

Simple

6–8

EX14

3

AP

8–10

ACCOUNTING INFORMATION SYSTEMS (Continued)

Number

LO

BT

Difficulty

Time (min.)

P1A

2, 3

AP

Simple

30–40

P2A

2, 3

AP

Simple

30–40

P3A

2, 3

AP

Moderate

40–50

P4A

2, 3

AP

Moderate

50–60

P5A

2, 3

AP

60–70

P6A

2, 3

AP

60–70

AP

Moderate

80–90

Simple

10–15

2, 3

Moderate

15–20

Simple

10–15

Simple

10–15

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Explain the basic concepts

of an accounting information

system.

Q7-1

Q7-2

Q7-3

Q7-4

BE7-1

BE7-2

BE7-3

DI7-1

E7–11

P7–5A

3. Record transactions in special

journals.

DI7-3

Q7-7

Q7-8

Q7–10

Q7–12

Q7–13

BE7-6

BE7-7

BE7-8

BE7-9

BE7-10

E7-1

E7-3

E7-6

E7-7

E7-9

P7–5A

P7–6A

Q7–11

Broadening Your Perspective

Real-World Focus

Comprehensive

Problem

(Mini Practice Set)

Decision Making

Across the

Organization

ANSWERS TO QUESTIONS

1. (a) An accounting information system collects and processes transaction data and communicates

2. There are three principles for developing an accounting information system:

Cost effectiveness. The system must be cost-effective; that is, the benefits obtained from the

information must outweigh the cost of providing it.

5. The advantages of using subsidiary ledgers are that they:

• Show in a single account transactions affecting a single customer or single creditor, thus

providing up-to-date information on specific account balances.

• Free the general ledger of excessive details relating to accounts receivable and accounts

Questions Chapter 7 (Continued)

7. Sales journal. Records entries for all sales of merchandise on account.

Cash receipts journal. Records entries for all cash received by the business.

Purchases journal. Records entries for all purchases of merchandise on account.

Cash payments journal. Records entries for all cash paid.

Some advantages of each journal are given below:

• Sales journal. (1) Since the sales journal employs only one line to record a Sales

transaction, its use reduces recording time; (2) the column totals are only posted to the

8. The entry for the sales return should be recorded in the general journal. Since Kensington

Company has a single-column sales journal, only credit sales can be recorded there. A purchase

10. The purpose of special journals is to facilitate the recording process of the business entity. Therefore,

the columns included in any special journal should correspond to the unique needs of the

11. (a) No, the customers’ ledger will not agree with the Accounts Receivable control account. The

Questions Chapter 7 (Continued)

13. (a) General journal. (d) Sales journal.

15. Typically included would be credit purchases of equipment, office supplies, and store supplies.

16. One such example is a purchase return. Here the Accounts Payable control and subsidiary account

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 7-1

BRIEF EXERCISE 7-2

BRIEF EXERCISE 7-3

BRIEF EXERCISE 7-4

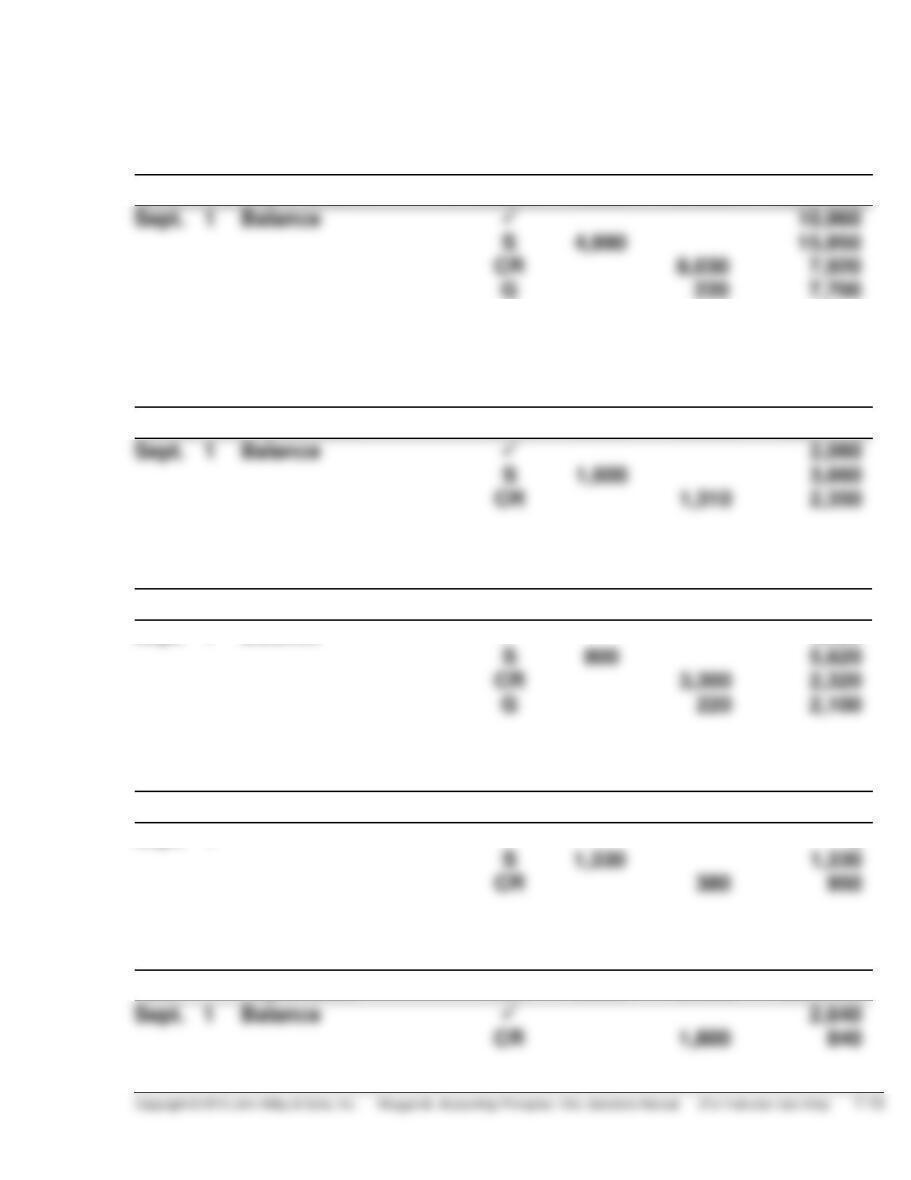

Accounts Receivable Subsidiary Ledger

General Ledger

Austin Co.

Accounts Receivable

Date

Ref.

Debit

Credit

Balance

Date

Ref.

Debit

Credit

Balance

Jan. 7

10,000

10,000

Jan. 31

27,000

27,000

Date

Debit

Credit

Balance

Jan. 15

Date

Debit

Credit

Balance

Jan. 23

BRIEF EXERCISE 7-5

(a) General ledger (c) General ledger

BRIEF EXERCISE 7-6

(a) Cash Receipts Journal (d) Sales Journal

BRIEF EXERCISE 7-7

(a) No (c) Yes

BRIEF EXERCISE 7-8

(a) General Journal (if a one-column Purchases Journal)

BRIEF EXERCISE 7-9

BRIEF EXERCISE 7-10

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 7-1

DO IT! 7-2

Subsidiary balances:

DO IT! 7-3

1. Sold merchandise on account: Sales journal

SOLUTIONS TO EXERCISES

EXERCISE 7-1

(a) $370,400. Beginning balance of $340,000 plus $161,400 debit from sales

EXERCISE 7-2

To: Sara Fogelman, Chief Financial Officer

From: Student

Subject: Jill Longley account

The explanation of the three entries in the subsidiary ledger for the Jill

Longley account is as follows:

Sept. 2 This was a credit sale of merchandise to Longley. The entry

was recorded on page 31 of the Sales Journal.

EXERCISE 7-3

(a) & (b) General Ledger

Accounts Receivable

Date

Explanation

Ref.

Debit

Credit

Balance

Accounts Receivable Subsidiary Ledger

Fowler

Date

Explanation

Ref.

Debit

Credit

Balance

Sogard

Date

Explanation

Ref.

Debit

Credit

Balance

Sept. 1

Balance

4,820

Giambi

Date

Explanation

Ref.

Debit

Credit

Balance

Sept. 1

0

Andino

Date

Explanation

Ref.

Debit

Credit

Balance

EXERCISE 7-3 (Continued)

Hurley

Date

Explanation

Ref.

Debit

Credit

Balance

(c) MONTGOMERY COMPANY

Schedule of Accounts Receivable

As of September 30, 2017

Fowler ……………………………………………………………………………. $2,350

EXERCISE 7-4

(a) $3,500 [$10,000 – ($4,000 + $2,500)].

EXERCISE 7-5

EXERCISE 7-6

(a) & (b)

GOMES COMPANY

Sales Journal S1

Date

Account

Debited

Invoice

No.

Ref.

Accounts Receivable Dr.

Sales Revenue Cr.

Cost of Goods Sold Dr.

Inventory Cr.

2017

GOMES COMPANY

Purchases Journal P1

Date

Account Credited

Terms

Ref.

Inventory Dr.

Accounts Payable Cr.

EXERCISE 7-7

(a) & (b)

R. SANTIAGO CO.

Cash Receipts Journal CR1

Date

Account

Credited

Ref.

Cash

Dr.

Sales

Discounts

Dr.

Accounts

Receivable

Cr.

Sales

Revenue

Cr.

Other

Accounts

Cr.

Cost of Goods Sold

Dr.

Inventory

Cr.

55,300

9,000

40,000

2017

May 1

Owner’s Cap.

40,000

40,000

EXERCISE 7-7 (Continued)

R. SANTIAGO CO.

Cash Payments Journal CP1

Date

Ck.

No.

Account Debited

Ref.

Other

Accounts

Dr.

Accounts

Payable

Dr.

Inventory

Cr.

Cash

Cr.

2017

EXERCISE 7-8

(a) Journal

(b) Columns in the journal

Cash Payments

1.

Cash Payments

Cash (Cr.), Other Accounts (Dr.).

EXERCISE 7-9

(a) Mar. 2 Equipment …………………………………………….. 7,400

Accounts Payable—Bole

(b) To: President Hasselback

From: Chief Accountant

Subject: Posting of Control and Subsidiary Accounts

The posting of these accounts varies with the journals used in recording

the transactions.

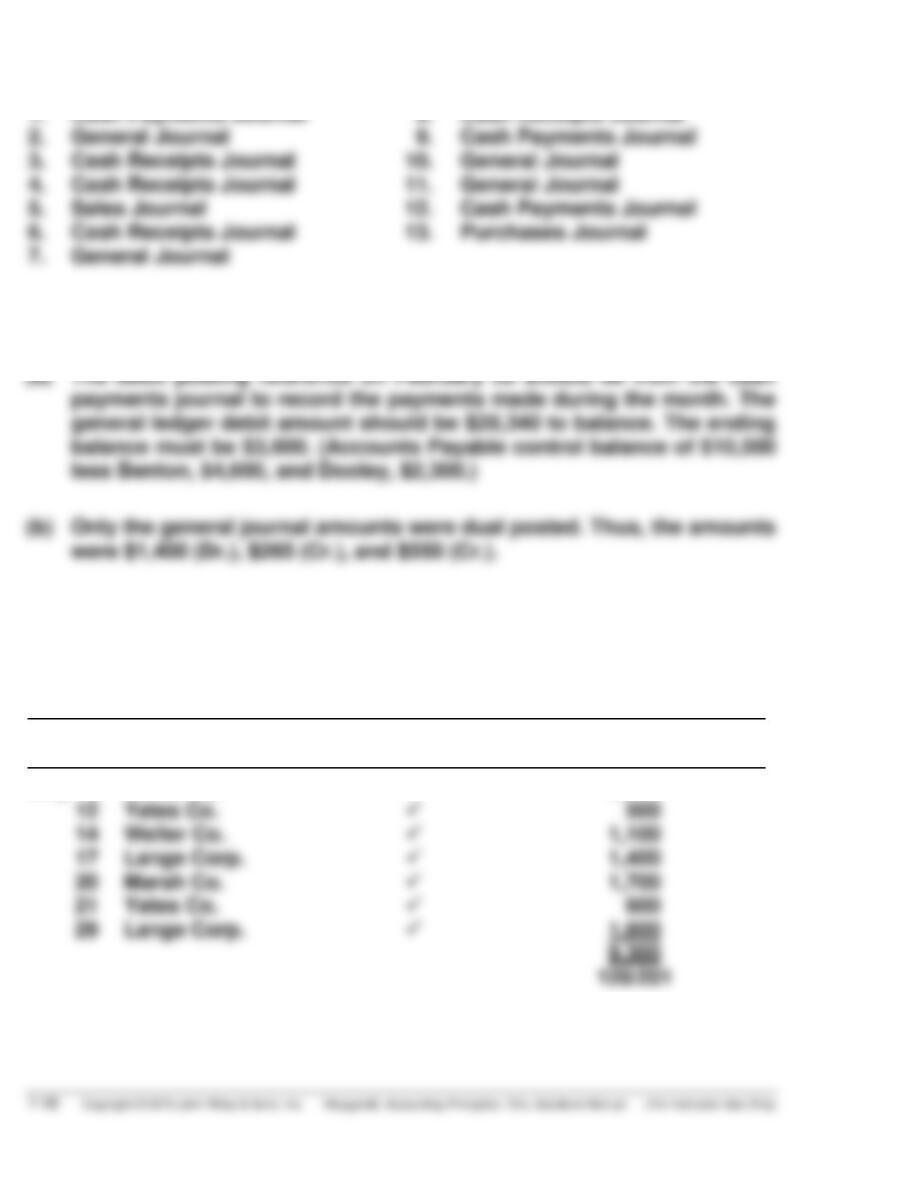

EXERCISE 7-10

EXERCISE 7-11

EXERCISE 7-12

(a)

Purchases Journal P1

Date

Account Credited

Ref.

Inventory Dr.

Accounts Payable Cr.

July 3

Marsh Co.

2,400

EXERCISE 7-12 (Continued)

(b)

General Journal

Date

Accounts and Explanations

Ref.

Debit

Credit

July 1

Inventory …………………………………….

120/

400

Accounts Payable—Lange

Equipment ………………………………….

157/

3,900

EXERCISE 7-13

EXERCISE 7-14

SOLUTIONS TO PROBLEMS

PROBLEM 7-1A

(a)

Cash Receipts Journal CR1

Date

Account

Credited

Ref.

Cash

Dr.

Sales

Discounts

Dr.

Accounts

Receivable

Cr.

Sales

Revenue

Cr.

Other

Accounts

Cr.

Cost of Goods Sold

Dr.

Inventory

Cr.

(112)

7,245

Apr. 1

Owner’s

(b) General Ledger

Accounts Receivable No. 112

Date

Explanation

Ref.

Debit

Credit

Balance

Accounts Receivable Subsidiary Ledger

Morrow

Date

Explanation

Ref.

Debit

Credit

Balance