E7-5 Use incremental analysis for make-or-buy decision

Pottery Ranch Inc. has been manufacturing its own finials for its curtain rods. The company is currently operating at 100% of capacity, and

variable manufacturing is charged to production at the rate of 70% of direct labor cost. The direct materials and the direct labor cost

per unit to make a pair of finials are $4 and $5, respectively. Normal production is 30,000 curtain rods per year.

A supplier offers to make a pair of finials at a price of $12.95 per unit. If Pottery Ranch accepts the supplier’s offer, all variable manufacturing

costs will be eliminated, but the $45,000 of fixed manufacturing overhead currently being charged to the finials will have to be absorbed by

other products.

Instructions

(a) Prepare the incremental analysis for the decision to make or buy the finials.

(b) Should Pottery Ranch buy the finials?

(c )

Would your answer be different in (b) if the productive capacity released by not making the finials could be used to produce income

of $20,000.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a) Prepare the incremental analysis for the decision to make or buy the finials.

Make Buy

Net income

Increase

(Decrease)

Direct materials ? Value Value

Direct labor ? Value Value

Variable overhead costs ? Value Value

Fixed manufacturing costs Value Value Value

Purchase price ? Value Value

Total annual costs ? ? ?

(b) Should Pottery Ranch buy the finials?

(c ) Would your answer be different in (b) if the productive capacity released by not making

the finials could be used to produce income of $20,000.

Make Buy

Net income

Increase

(Decrease)

Total annual cost (above) Value Value Value

Opportunity cost Value Value

Total cost ? ? ?

After you have completed E7-5, consider the following additional question.

1. Assume that the direct materials and direct labor cost per unit to make the finials are $4.75 and $5.50, respectively.

What impact do these changes on your analysis and the decision to make-or-buy the finials?

E7-5 Solution

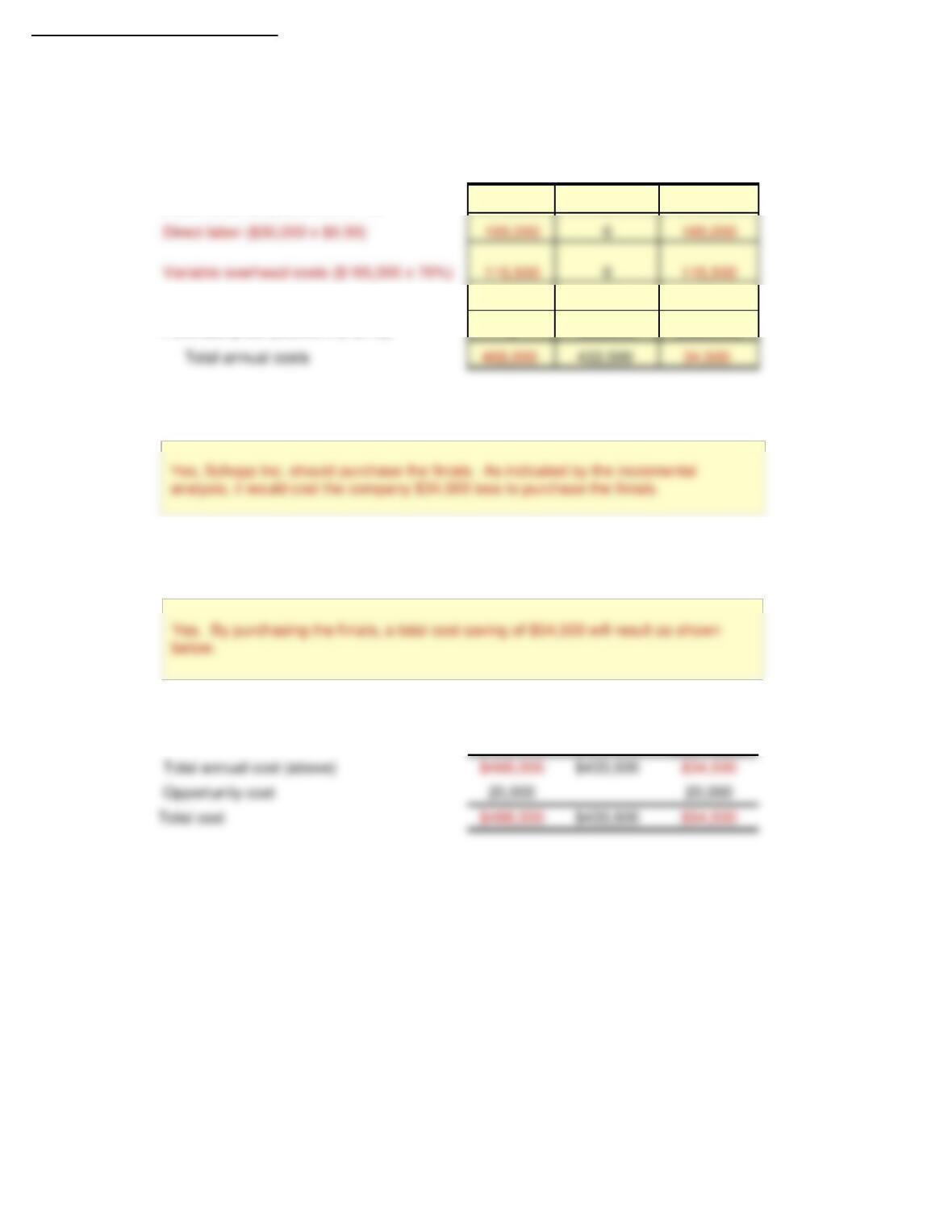

(a) Prepare the incremental analysis for the decision to make or buy the finials.

Make Buy

Net income Increase

(Decrease)

Direct materials(30,000 x $4.00) $120,000 $0 $120,000

Direct labor (30,000 x $5.00) 150,000 0 $150,000

(b) Should Pottery Ranch buy the finials?

(c ) Would your answer be different in (b) if the productive capacity released by not making the

finials could be used to produce income of $20,000.

Make Buy

Net income Increase

(Decrease)

Total annual cost (above) $420,000 $433,500 (13,500)

Opportunity cost 20,000 20,000

Total cost $440,000 $433,500 $6,500

E7-5 Solution to additional question

1. Assume that the direct materials and direct labor cost per unit to make the finials are $4.75 and $5.50, respectively.

What impact do these changes on your analysis and the decision to make-or-buy the finials?

(a)

Make Buy

Net income

Increase

(Decrease)

Direct materials(30,000 x $4.75) $142,500 $0 $142,500

Fixed manufacturing costs 45,000 45,000 0

Purchase price (30,000 x $12.75) 0 388,500 (388,500)

(b) Should Pottery Ranch buy the finials?

(c ) Would your answer be different in (b) if the productive capacity released by not making the

finials could be used to produce income of $20,000.

Make Buy

Net income

Increase

(Decrease)

E7-8 Prepare incremental analysis concerning make-or-buy decision.

Innova uses 1.000 units of the component IMC2 every month to manufacture one of its products. The unit costs incurred to

manufacture the components are as follows:

Direct materials $65.00

Direct labor 45.00

Overhead 126.50

Total 236.50

Overhead costs include variable material handling costs of $6.50, which are applied to products on the basis of direct material

costs. The remainder of the overhead costs are applied on the basis of direct labor dollars and consist of 60% variable costs and

40% fixed costs. A vendor has offered to supply the IMC2 component at a price of $200 per unit.

Instructions

(a) Should Innova purchase the component from the outside vendor if Innova’s capacity remains idle?

(b) Should Innova purchase the component from the outside vendor if it can use its facilities to manufacture

another product? What information will Innova need to make an accurate decision? Show your calculations.

(c ) What are the qualitative factors that Innova will have to consider when making its decision?

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a) Should Innova purchase the component from the outside vendor if Innova’s capacity remains idle?

Make IMC2 Buy IMC2

Net income

Increase

(Decrease)

Direct materials Value Value Value

Direct labor Value Value Value

Material handling Value Value Value

Variable overhead costs Value Value Value

Purchase price Value Value Value

Total unit cost ? ? ?

(b) Should Innova purchase the component from the outside vendor if it can use its facilities to manufacture

another product? What information will Innova need to make an accurate decision? Show your calculations.

(c ) What are the qualitative factors that Innova will have to consider when making its decision?

After you have completed E7-8, consider the following additional question.

1. Assume that unit cost for direct materials changed to $68.00 and that overhead costs changed to $130.00.

What impact do these changes have on the make-or-buy decision?

Response:

Response:

Response:

E7-8 Solution

(a) Should Innova purchase the component from the outside vendor if Innova’s capacity remains idle?

Make IMC2 Buy IMC2

Net income

Increase

(Decrease)

Direct materials $65.00 0 $65.00

Direct labor 45.00 0 45.00

Material handling 6.50 0 6.50

Variable overhead costs* 72.00 0 72.00

Purchase price 0.00 200.00 (200.00)

Total annual costs $188.50 $200.00 ($11.50)

* Variable overhead = 60% x ($126.50 – $6.50)

(b) Should Innova purchase the component from the outside vendor if it can use its facilities to manufacture

another product? What information will Innova need to make an accurate decision? Show your calculations.

(c) What are the qualitative factors that Innova will have to consider when making its decision?

The unit should not be purchased from the outside vendor, as the per unit cost

would be $11.50 greater than if they made it.

In order for Innova to make an accurate decision, they would have to know the

opportunity cost of manufacturing the other product. As determined in (a),

purchasing the product from outside would cost $11,500 more ($1,000 x

$11.50). Innova would have to increase their contribution margin by more than

$11,500 through the manufacture of the other product, before it would be

economical for them to purchase the IMC2 from the outside vendor.

Qualitative factors to consider would be (1) quality of the component (2) on-time

delivery, and (3) reliability of the vendor.

E7-8 Solution to additional question

1. Assume that unit cost for direct materials changed to $68.00 and that total overhead costs changed to $130.00.

What impact do these changes have on the make-or-buy decision?

Make IMC2 Buy IMC2

Net income

Increase

(Decrease)

Material handling 6.50 $0 6.50

(b) Should Innova purchase the component from the outside vendor if it can use its facilities to manufacture

another product? What information will Innova need to make an accurate decision? Show your calculations.

(c) What are the qualitative factors that Innova will have to consider when making its decision?

In order for Innova to make an accurate decision, they would have to know the

opportunity cost of manufacturing the other product. As determined in (a),

E7-10 Determine whether to sell or process further, joint products

Stahl Inc. produces three separate products from a common process costing $100,000. Each of the products

can be sold at the split-off point or can be processed further and then sold for a higher price. Shown below

are cost and selling price data for a recent period.

Sales Value Cost to Sales Value

at Split-off Process after Further

Point Further Processing

Product 10 $60,000 $100,000 $190,000

Product 12 15,000 30,000 35,000

Product 14 55,000 150,000 215,000

Instructions

(a) Determine total net income if all products are sold at the split-off point.

(b) Determine total net income if all products are sold after further processing.

(c ) Using incremental analysis, determine which products should be sold at the split-off

point and which should be processed further.

(d) Determine total net income using the results from (c ) and explain why the net income

is different from that determined in (b).

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

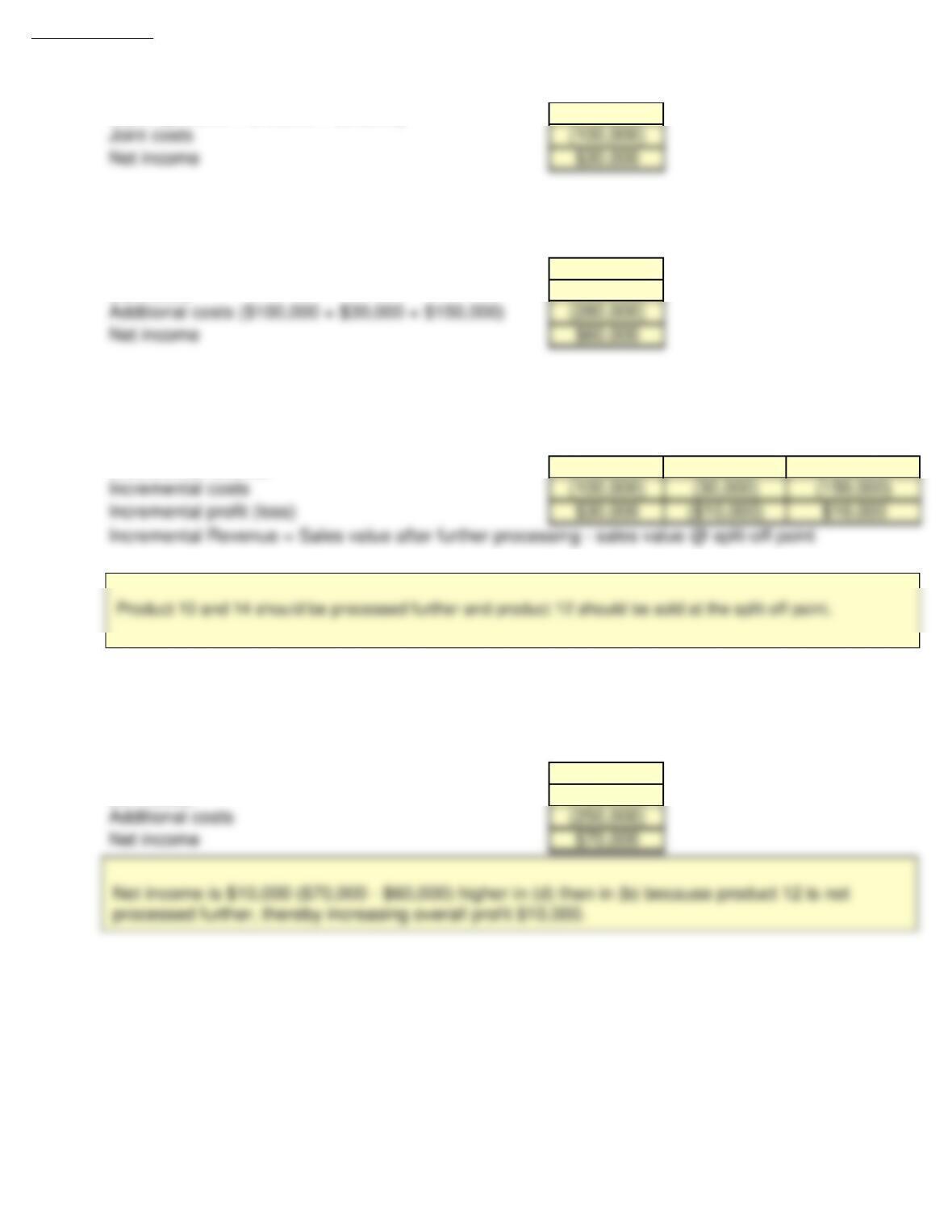

(a) Determine total net income if all products are sold at the split-off point.

Sales Value

Joint costs Value

Net income ?

(b) Determine total net income if all products are sold after further processing.

Sales Value

Joint costs Value

Additional costs Value

Net income ?

(c) Using incremental analysis, determine which products should be sold at the split-off

point and which should be processed further.

Product 10 Product 12 Product 14

Incremental revenue Value Value Value

Incremental costs Value Value Value

Incremental profit (loss) ? ? ?

(d) Determine total net income using the results from (c ) and explain why the net income

is different from that determined in (b).

Sales Value

Joint costs Value

Additional costs Value

Net income ?

Response:

After you have completed E7-10, consider the additional question.

1. Assume that sales value at split-off point for Product 10 changed to $75,000 and

the cost to process Product 14 further changed to $162,000. What impact do these

changes have on total net income at split-off point and after further processing?

Response:

E7-10 Solution

(a) Determine total net income if all products are sold at the split-off point.

Sales ($60,000 + $15,000 + $55,000) $130,000

(b) Determine total net income if all products are sold after further processing.

Sales ($190,000 + $35,000 + $215,000) $440,000

Joint costs (100,000)

(c) Using incremental analysis, determine which products should be sold at the split-off

point and which should be processed further. Product 10 Product 12 Product 14

Incremental revenue $130,000 $20,000 $160,000

(d)

Determine total net income using the results from (c ) and explain why the net income

is different from that determined in (b).

Sales ($190,000 + $15,000 + $215,000) $420,000

Joint costs (100,000)

E7-10 Solution to additional question

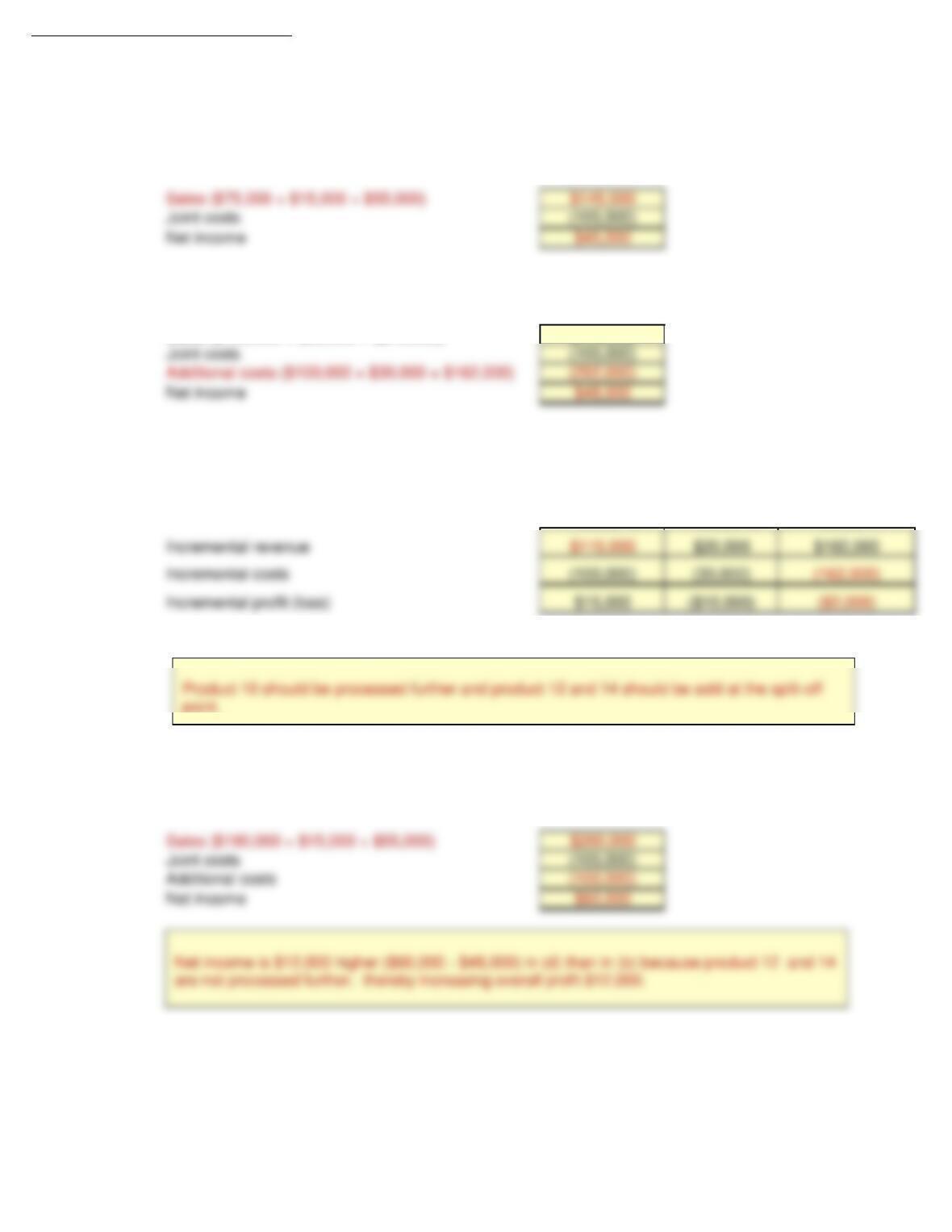

1. Assume that sales value at split-off point for Product 10 changed to $75,000 and

the cost to process Product 14 further changed to $162,000. What impact do these

changes have on total net income at split-off point and after further processing?

(a) Determine total net income if all products are sold at the split-off point.

(b) Determine total net income if all products are sold after further processing.

Sales ($190,000 + $35,000 + $215,000) $440,000

(c) Using incremental analysis, determine which products should be sold at the split-off

point and which should be processed further.

Product 10 Product 12 Product 14

Incremental revenue = Sales value after further processing – sales value @ split-off point

(d) Determine total net income using the results from (c ) and explain why the net income

is different from that determined in (b).

E7-11 Determine whether to sell or process further, joint products

Kirk Minerals processes materials extracted from mines. The most common raw material that it processes

results in three joint products: Spock, Uhura, and Suhu. Each of these products can be sold as is, or each can

be processed further and sold for a higher price. The company incurs joint costs of $180,000 to process one batch

of the raw material that produces the three joint products. The following cost and sales information is available

for one batch of each product.

Sales Value at Allocated Cost to Process Sales Value of

Split-off Point Joint Costs Further

Processed Product

Spock $210,000 $40,000 $110,000 $300,000

Uhura 300,000 60,000 85,000 400,000

Suhu 455,000 80,000 250,000 800,000

Instructions

Determine whether each of the three joint products should be sold as is, or processed further.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

Spock Uhura Suhu

Sales value of processed product Value Value Value

Sales value @ split-off point Value Value Value

Incremental revenue ? ? ?

Incremental costs Value Value Value

Incremental profit (loss) ? ? ?

After you have completed E7-11, consider the additional question.

1. Assume that sales value at split-off point for Uhura changed to $350,000 and the cost to process

further for Sulu changed to $325,000. What impact do these changes have on the decision to

sell as is or to process further for each product?

Response:

E7-11 Solution

To determine whether each of the three joint products should be sold as is, or processed further,

we must determine the incremental profit or loss that would be earned by each. The allocated

joint costs are irrelevant to the decision since these costs will not change whether or not the

products are sold as is or processed further.

Spock Uhura Sulu

Sales value of processed product $300,000 $400,000 $800,000

Sales value @ split-off point (210,000) (300,000) (455,000)

To determine whether each of the three joint products should be sold as is, or processed further, we

must determine the incremental profit or loss that would be earned by each. The allocated joint costs

E7-11 Solution to additional question

1. Assume that sales value at split-off point for Uhura changed to $350,000 and the cost to process

further for Sulu changed to $325,000. What impact do these changes have on the decision to

sell as is or to process further for each product?

Spock Uhura Sulu

Sales value of processed product $300,000 $400,000 $800,000

To determine whether each of the three joint products should be sold as is, or processed further,

we must determine the incremental profit or loss that would be earned by each. The allocated

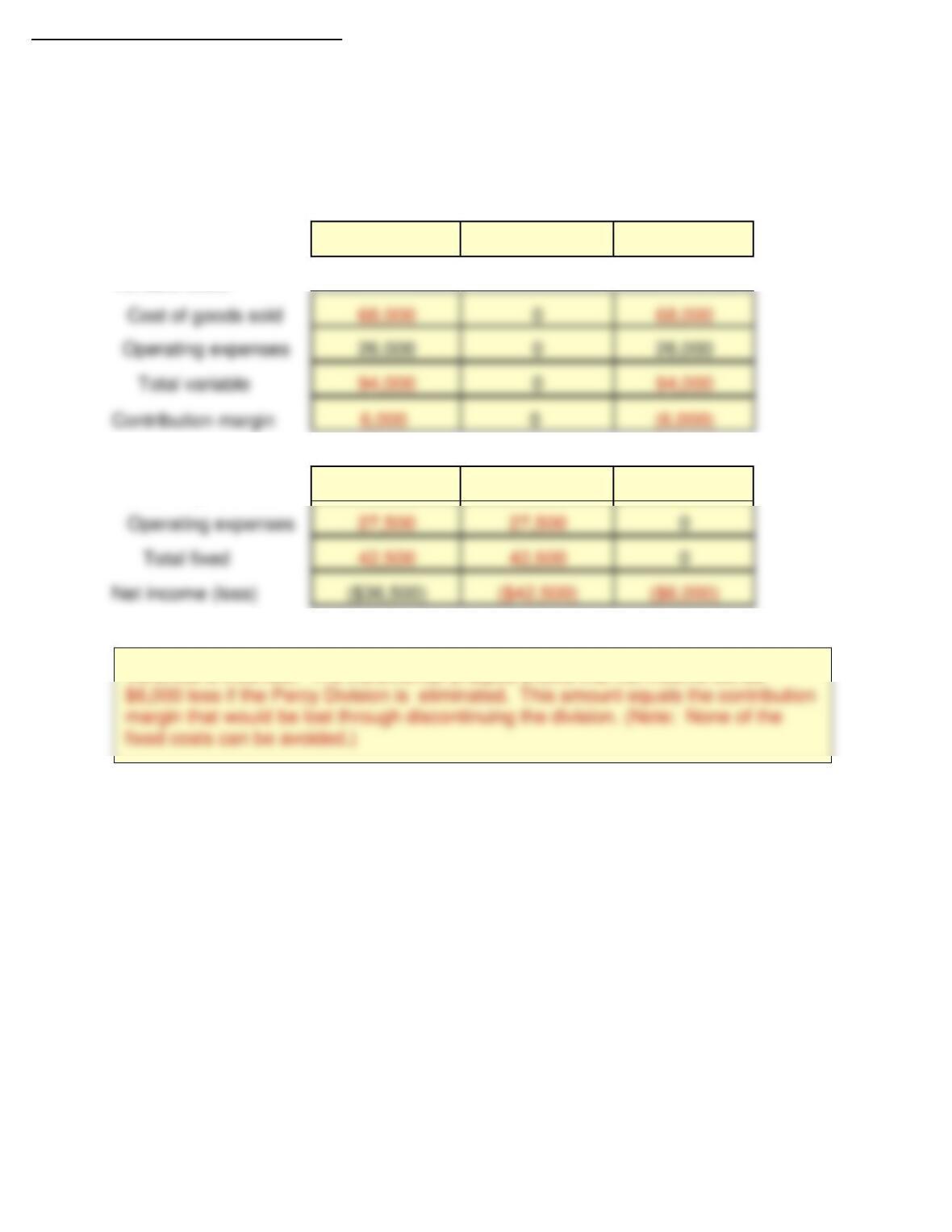

E7-15 Use incremental analysis concerning elimination of division.

Veronica Mars, a recent graduate of Bell’s accounting program, evaluated the operating performance

of Dunn Company‘s six divisions. Veronica made the following presentation to Dunn’s board of directors

and suggested the Percy Division be eliminated. “If the Percy Division is eliminated,” she said, “our

total profits would increase by $26,000.”

The Other Percy

Five Divisions Division Total

Sales $1,664,200 $100,000 $1,764,200

Cost of goods sold 978,520 76,000 1,054,520

Gross Profit 685,680 24,000 709,680

Operating expenses 527,940 50,000 577,940

Net income $157,740 ($26,000) $131,740

In the Percy Division, cost of goods sold is $61,000 variable and $15,000 fixed, and operating expenses

are $30,000 variable and $20,000 fixed. None of the Percy Division’s fixed costs will be eliminated if the

division is discontinued.

Instructions

Is Veronica right about eliminating the Percy Division? Prepare a schedule to support your answer.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

Is Veronica right about eliminating the Percy Division? Prepare a schedule to support your answer.

Continue Eliminate

Net income

Increase

(Decrease)

Sales Value Value Value

Variable costs

Cost of goods sold Value Value Value

Operating expenses Value Value Value

Total variable ? ? ?

Contribution margin ? ? ?

Fixed costs

Cost of goods sold Value Value Value

Operating expenses Value Value Value

Total fixed ? ? ?

Net income (loss) ? ? ?

After you have completed E7-15, consider the following additional question.

1. Assume that variable cost of goods sold for the Percy Division changed to $68,000 and fixed

operating expenses changed to $27,500. There was no change to variable operating costs.

How would these changes impact your answer?

Response:

E7-15 Solution

Continue Eliminate

Net income

Increase

(Decrease)

Sales $100,000 $0 ($100,000)

Variable costs

Fixed costs

Cost of goods sold 15,000 15,000 0

Operating expenses 20,000 20,000 0

Veronica is incorrect. The incremental analysis shows that net income will be $9,000

E7-15 Solution to additional question

1. Assume that variable cost of goods sold for the Percy Division changed to $68,000 and fixed

operating expenses changed to $27,500. There was no change to variable operating costs.

How would these changes impact your answer?

Continue Eliminate

Net income

Increase

(Decrease)

Sales $100,000 $0 ($100,000)

Variable costs

Fixed costs

Cost of goods sold 15,000 15,000 0

Veronica is incorrect. The incremental analysis shows that net income will be

P7-3A Determine if product should be sold or processed further.

Thompson Industrial Products Inc. (TIPI) is a diversified industrial-cleaner processing company. The company’s Dargar plant

produces two products: a table cleaner and a floor cleaner from a common set of chemical inputs (CDG). Each week 900,000

ounces of chemical input are processed at a cost of $210,000 into 600,000 ounces of floor cleaner and 300,000 ounces of table

cleaner. The floor cleaner has no market value until it is converted into a polish with the trade name FloorShine. The additional

processing costs for this conversion amount to $240,000.

FloorShine sells at $20 per 30-ounce bottle. The table cleaner can be sold for $17 per 25-ounce bottle. However, the table

cleaner can be converted into two other products by adding 300,000 ounces of another compound (TCP) to the 300,000 ounces

of table cleaner. This joint process will yield 300,000 ounces each of table stain remover (TSR) and table polish (TP). The

additional processing costs for this process amounts to $100,000. Both table products can be sold for $14 per $25-ounce bottle.

The company decided not to process the table cleaner into TSR and TP based on the following analysis.

Table Table Stain Table

Cleaner Remover (TSR) Polish (TP) Total

Production in ounces 300,000 300,000 300,000

Revenue $204,000 $168,000 $168,000 $336,000

Costs:

CDG costs 70000* 52,500 52,500 105,000 **

TCP costs 0 50,000 50,000 100,000

Total costs 70,000 102,500 102,500 205,000

Weekly gross profit $134,000 $65,500 $65,500 $131,000

*If table cleaner is not processed further, it is allocated 1/3 of the $210,000 of CDG cost, which is equal to 1/3 of the

total physical output.

** If table cleaner is processed further, total physical output is 1,200,000 ounces. TSR and TP combined account for

50% of the total physical output and are each allocated 25% of the CDG cost.

Instructions

(a) Determine if management made the correct decision to not process the table cleaner further by doing the following.

(1) Calculate the company’s total weekly gross profit assuming the table cleaner is not processed further.

(2) Calculate the company’s total weekly gross profit assuming the table cleaner is processed further.

(3) Compare the resulting net incomes and comment on management’s decision.

(b) Compare the resulting net incomes and comment on management’s decision.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

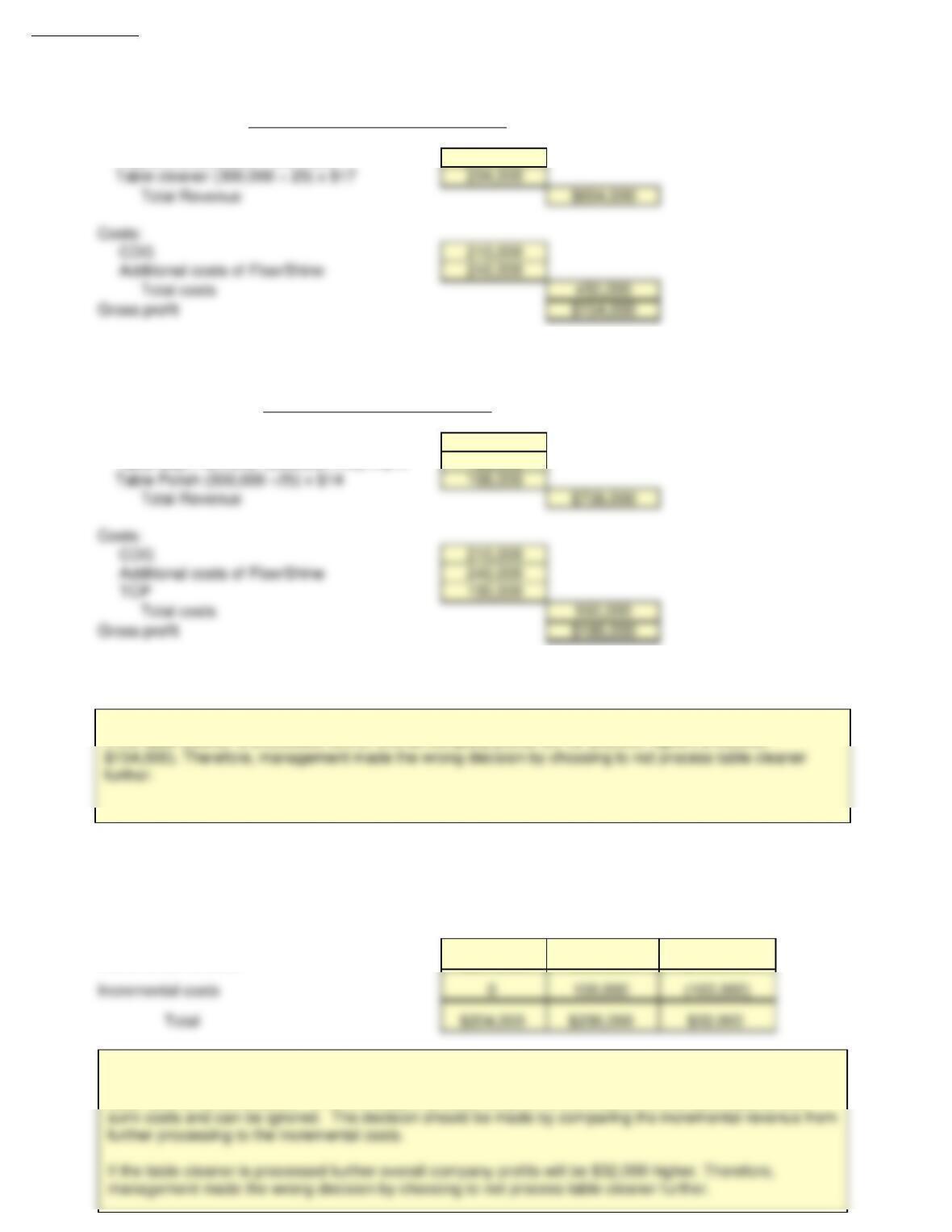

(a) Determine if management made the correct decision to not process the table cleaner further by doing the following.

(1) Calculate the company’s total weekly gross profit assuming the table cleaner is not processed further.

Sales:

FloorShine ?

Table cleaner ?

Total Revenue ?

Costs:

CDG Value

Additional costs of FloorShine Value

Total costs ?

Gross profit ?

(a) Determine if management made the correct decision to not process the table cleaner further by doing the following.

(2) Calculate the company’s total weekly gross profit assuming the table cleaner is processed further.

Sales:

FloorShine Value

Table Stain Remover Value

Table Polish Value

Total Revenue ?

Costs:

Process Further

Table Cleaner Not Processed Further

Table Cleaner Processed Further

CDG Value

Additional costs of FloorShine Value

TCP Value

Total costs ?

Gross profit ?

(a) Determine if management made the correct decision to not process the table cleaner further by doing the following.

(3) Compare the resulting net incomes and comment on management’s decision.

(b) Compare the resulting net incomes and comment on management’s decision.

Don’t Process Process Net Income

Table Cleaner Table Cleaner Increase

Further Further (Decrease)

Incremental revenue Value Value Value

Incremental costs Value Value Value

Total ? ? ?

1. After you have completed P7-3A, consider the following additional question.

Assume that the selling price of the two table products after further processing changed to $13

for each 25-ounce bottle and the cost of TCP compound to further process changed to $120,000.

How do these changes impact the decision to process or not process further?

Response:

Response:

P7-3A Solution

(a) Determine if management made the correct decision to not process the table cleaner further by doing the following.

(1) Calculate the company‘s total weekly gross profit assuming the table cleaner is not processed further.

Sales:

FloorShine (600,000 ÷ 30) x $20 $400,000

(a) Determine if management made the correct decision to not process the table cleaner further by doing the following.

(2) Calculate the company‘s total weekly gross profit assuming the table cleaner is processed further.

Sales:

FloorShine $400,000

Table Stain Remover (300,000 ÷ 25) x $14 168,000

(a) Determine if management made the correct decision to not process the table cleaner further by doing the following.

(3) Compare the resulting net incomes and comment on management’s decision.

(b) Compare the resulting net incomes and comment on management’s decision.

Don’t Process Process Net Income

Table Cleaner Table Cleaner Increase

Further Further (Decrease)

Incremental revenue $204,000 $336,000 $132,000

Table Cleaner Not Processed Further

Table Cleaner Processed Further

If the table cleaner is processed further overall company profits will be $32,000 higher( $186,000 –

When trying to decide if the table cleaner should be processed further into TSR and TP, only the relevant

data need to be considered. All of the costs that occurred prior to the creation of the table cleaner are

P7-3A Solution to additional question

1. Assume that the selling price of the two table products after further processing changed to $13

for each 25-ounce bottle and the cost of TCP compound to further process changed to $120,000.

How do these changes impact the decision to process or not process further?

(a) Determine if management made the correct decision to not process the table cleaner further by doing the following.

(1) Calculate the company’s total weekly gross profit assuming the table cleaner is not processed further.

Sales:

FloorShine (600,000 ÷ 30) x $20 $400,000

Table cleaner (300,000 ÷ 25) x $17 204,000

(a) Determine if management made the correct decision to not process the table cleaner further by doing the following.

(2) Calculate the company’s total weekly gross profit assuming the table cleaner is processed further.

Sales:

FloorShine $400,000

Costs:

CDG 210,000

Additional costs of FloorShine 240,000

TCP 120,000

(a) Determine if management made the correct decision to not process the table cleaner further by doing the following.

(3) Compare the resulting net incomes and comment on management’s decision.

(b) Compare the resulting net incomes and comment on management’s decision.

Don’t Process Process Net Income

Table Cleaner Table Cleaner Increase

Further Further (Decrease)

Table Cleaner Processed Further

Table Cleaner Not Processed Further

P7-5A Prepare incremental analysis concerning elimination of divisions.

Brislin Company has four operating divisions. During the first quarter of 2017, the company reported

aggregate income from operations of $213,000 and the following divisional results.

III III IV

Sales $250,000 $200,000 $500,000 $450,000

Cost of goods sold 200,000 192,000 300,000 250,000

Selling and administrative expenses 75,000 60,000 60,000 50,000

Income (loss) from operations ($25,000) ($52,000) $140,000 $150,000

Analysis reveals the following percentages of variable costs in each division.

III III IV

Cost of good sold 70% 90% 80% 75%

Selling and administrative expenses 40 60 50 60

Discontinuance of any division would save 50% of the fixed costs and expenses for that division. Top management is

very concerned about the unprofitable divisions (I and II). Consensus is that one or both of the divisions should be discontinued.

Instructions

(a) Compute the contribution margin for Division I and II.

(b) Prepare an incremental analysis concerning the possible discontinuance of (1) Division I and

(2) Division II. What course of action do you recommend for each division?

(c ) Prepare a columnar condensed income statement for Brislin Company, assuming Division II

is eliminated. (Use the CVP format.) Division II’s unavoidable fixed costs are allocated equally

to the continuing divisions.

(d) Reconcile the total income from operations ($213,000) with the total income from operations

without Division II.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a) Compute the contribution margin for Division I and II.

Division I Division II

Sales Value Value

Variable costs

Cost of goods sold

Value Value

Selling and administrative

Value Value

Total variable expenses

? ?

Contribution margin

? ?

(b) (1) Prepare an incremental analysis concerning the possible discontinuance of Division I

Net Income

Increase

Continue Eliminate (Decrease)

Contribution margin (above)

Value Value Value

Fixed costs

Cost of goods sold

Value Value Value

Selling and administrative

Value Value Value

Total fixed expenses

? ? ?

Income (loss) from operations

? ? ?

(b) (2) Prepare an incremental analysis concerning the possible discontinuance of Division II.

Net Income

Increase

Continue Eliminate (Decrease)

Contribution margin (above)

Value Value Value

Fixed costs

Cost of goods sold

Value Value Value

Selling and administrative

Value Value Value

Total fixed expenses

? ? ?

Income (loss) from operations

? ? ?

Division

Division I

Division II

What course of action do you recommend for each division?

(c) Prepare a columnar condensed income statement for Brislin Company, assuming Division II

is eliminated. (Use the CVP format.) Division II’s unavoidable fixed costs are allocated equally

to the continuing divisions.

IIII IV Total

Sales

Value Value Value ?

Variable costs

Cost of goods sold

Value Value Value ?

Selling and administrative

Value Value Value ?

Total variable costs

? ? ? ?

Contribution margin

? ? ? ?

Fixed costs

Cost of goods sold

Value Value Value ?

Selling and administrative

Value Value Value ?

Total fixed costs

? ? ? ?

Income (loss) from operations

? ? ? ?

(d) Reconcile the total income from operations ($213,000) with the total income from operations

without Division II.

After you have completed P7-5A, consider the following additional question.

1. Assume that Division II’s cost of goods sold and selling and administrative expenses changed to $180,000

and $75,000 respectively. How do these changes impact the decision to drop or not drop Division II?

Divisions

BRISLIN COMPANY

CVP Income Statement

For the Quarter Ended March 31, 2017

Response:

Response:

P7-5A Solution

(a) Compute the contribution margin for Division I and II.

Division I Division II

Sales $250,000 $200,000

Variable costs

Cost of goods sold

140,000 172,800

(b) (1) Prepare an incremental analysis concerning the possible discontinuance of Division I

Net Income

Increase

Continue Eliminate (Decrease)

Contribution margin (above)

$80,000 $0 ($80,000)

Fixed costs

Cost of goods sold

$60,000 $30,000 $30,000

$45,000 $22,500 $22,500

(b) (2) Prepare an incremental analysis concerning the possible discontinuance of Division II.

Net Income

Increase

Continue Eliminate (Decrease)

Contribution margin (above)

($8,800) $0 $8,800

Fixed costs

Cost of goods sold

$19,200 $9,600 $9,600

$43,200 $21,600 $21,600

($52,000) ($21,600) $30,400

$24,000 $12,000 $12,000

What course of action do you recommend for each division?

(c) Prepare a columnar condensed income statement for Brislin Company, assuming Division II

is eliminated. (Use the CVP format.) Division II’s unavoidable fixed costs are allocated equally

to the continuing divisions.

IIII IV Total

Sales

$250,000 $500,000 $450,000 $1,200,000

Variable costs

Cost of goods sold

140,000 240,000 187,500 567,500

170,000 270,000 217,500 657,500

Divisions

Division I

Division II

BRISLIN COMPANY

CVP Income Statement

For the Quarter Ended March 31, 2017

Division I should be continued because it is producing positive contribution margin of $80,000.

Fixed costs

Cost of goods sold (1)

63,200 63,200 65,700 192,100

(1) Division’s fixed cost of goods sold plus 1/3 of Division II’s unavoidable fixed cost of goods sold

[$192,000 x (100% -90%) x 50% = $9,600]. Each division’s share is $3,200.

(d) Reconcile the total income from operations ($213,000) with the total income from operations

without Division II.

P7-5A Solution to additional question

1. Assume that Division II’s cost of goods sold and selling and administrative expenses changed to $180,000

and $75,000 respectively. How do these changes impact the decision to drop or not drop Division II?

(a) Compute the contribution margin for Division I and II.

Division I Division II

Sales $250,000 $200,000

Variable costs

(b) (1) Prepare an incremental analysis concerning the possible discontinuance of Division I

Net Income

Increase

Continue Eliminate (Decrease)

Contribution margin (above)

$80,000 $0 ($80,000)

(b) (2) Prepare an incremental analysis concerning the possible discontinuance of Division II.

Net Income

Increase

Continue Eliminate (Decrease)

Contribution margin (above)

($7,000) $0 $7,000

Fixed costs

Cost of goods sold

$18,000 $9,000 $9,000

What course of action do you recommend for each division?

(c ) Prepare a columnar condensed income statement for Brislin Company, assuming Division II

is eliminated. (Use the CVP format.) Division II’s unavoidable fixed costs are allocated equally

to the continuing divisions.

Division I

Division II

Division I should be continued because it is producing positive contribution margin of $80,000.

Income from operations will decrease by $27,500 by discontinuing this division.

IIII IV Total

Sales

$250,000 $500,000 $450,000 $1,200,000

Variable costs

Cost of goods sold

140,000 240,000 187,500 567,500

Selling and administrative

30,000 30,000 30,000 90,000

(1) Division’s fixed cost of goods sold plus 1/3 of Division II’s unavoidable fixed cost of goods sold

(d)

Reconcile the total income from operations ($210,000) with the total income from operations

without Division II.

Divisions

BRISLIN COMPANY

CVP Income Statement

For the Quarter Ended March 31, 2017

CD7 EXCEL Tutorial

CURRENT DESIGNS

Current Designs faces a number of important decisions that require incremental analysis. Consider each

of the following situations independently.

Situation 1

Recently, Mike Cichanowski, owner and CEO of Current Designs, received a phone call from the president

of a brewing company. He was calling to inquire about the possibility of Current Designs producing “floating

coolers” for a promotion his company was planning. These coolers resemble a kayak but are about one-third

the size. They are used to float food and beverages while paddling down the river on a weekend leisure trip.

The company would be interest in purchasing 100 coolers for the upcoming summer. It is willing to pay $250

per cooler. The brewing company would pick up the coolers upon completion of the order.

Mike met with Diane Buswell, controller, to identify how much it would cost Current Designs to produce

the coolers. After careful analysis, the following costs were identified.

Direct materials $80/unit Variable overhead $20/unit

Direct labor $60/unit Fixed overhead $1,000

Current Designs would be able to modify an existing mold to produce the coolers. The cost of these

modifications would be approximately $2,000.

Instructions

(a) Prepare an incremental analysis to determine whether Current Designs should accept this special order to

produce the coolers.

(b) Discuss additonal factors that Mike and Diane should consider if Current Designs is currently operating at

full capacity.

Situation 2

Current Designs is always working to identify ways to increase efficiency while becoming more environmentally

conscious. During a recent brainstorming session, one employee suggested to Diane Buswell, controller, that the

company should consider replacing the current rotomold oven as a way to realize savings from reduced energy

consumption. The oven operates on natural gas, using 17,000 therms of natural gas for an entire year. A new,

energy-efficient rotomold oven would operate on 15,000 therms of natural gas for an entire year. After seeking out

price quotes from a few suppliers, Diane determined that it would cost approximately $250,000 to purchase a new,

energy-efficient rotomold oven. She determines that the expected useful life of the new oven would be 10 years, and

it would have no salvage value at the end of its useful life. Current Designs would be able to sell the current oven for

Instructions

(a) Prepare an incremental analysis to determine if Current Designs should purchase the new rotomold oven,

assuming that the average price for natural gas over the next 10 years will be $0.65 per therm.

(b) Diane is concerned that natural gas prices might increase at a faster rate over the next 10 years. If the company

projects that the average natural gas price of the next 10 years could be as high as $0.85 per therm, discuss

how that might change your conclusion in (a).

Situation 3

One of Current Designs’ competitive advantages is found in the ingenuity of its owners and CEO, Mike Cichanowski. His

involvement in the design of kayak molds and production techniques has led to Current Designs being recognized as an

industry leader in the design and production of kayaks. This ingenuity was evident in an improved design of one of the

most important component of a kayak, the seat. The “Revolution Seating System” is one-of-a-kind, rotating axis seat

that gives unmatched, full contact, under-leg support. It is quickly adjustable with a lever-lock system that allows for a

customizable seat position that maximizes comfort for the rider.

Having just designed the “Revolution Seating System”, Current Designs must now decide whether to produce the seats

internally or buy them from an outside supplier. The costs for Current Designs to produce the seats are as follows.

Direct materials $20/unit Direct labor $15/unit

Variable overhead $12/unit Fixed overhead $20,000

Current Designs will need to produce 3,000 seats this year; 25% of the fixed overhead will be avoided if the seats are

$10,000

purchased from an outside vendor. After soliciting prices from outside suppliers, the company determined that it will

cost $50 to purchase a seat from an outside vendor.

Instructions

(a) Prepare an incremental analysis showing whether Current Designs should make or buy the “Revolution Seating

System.”

(b) Would your answer in (a) change if the productive capacity released by not making the seats could be used to

produce income of $20,000?

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

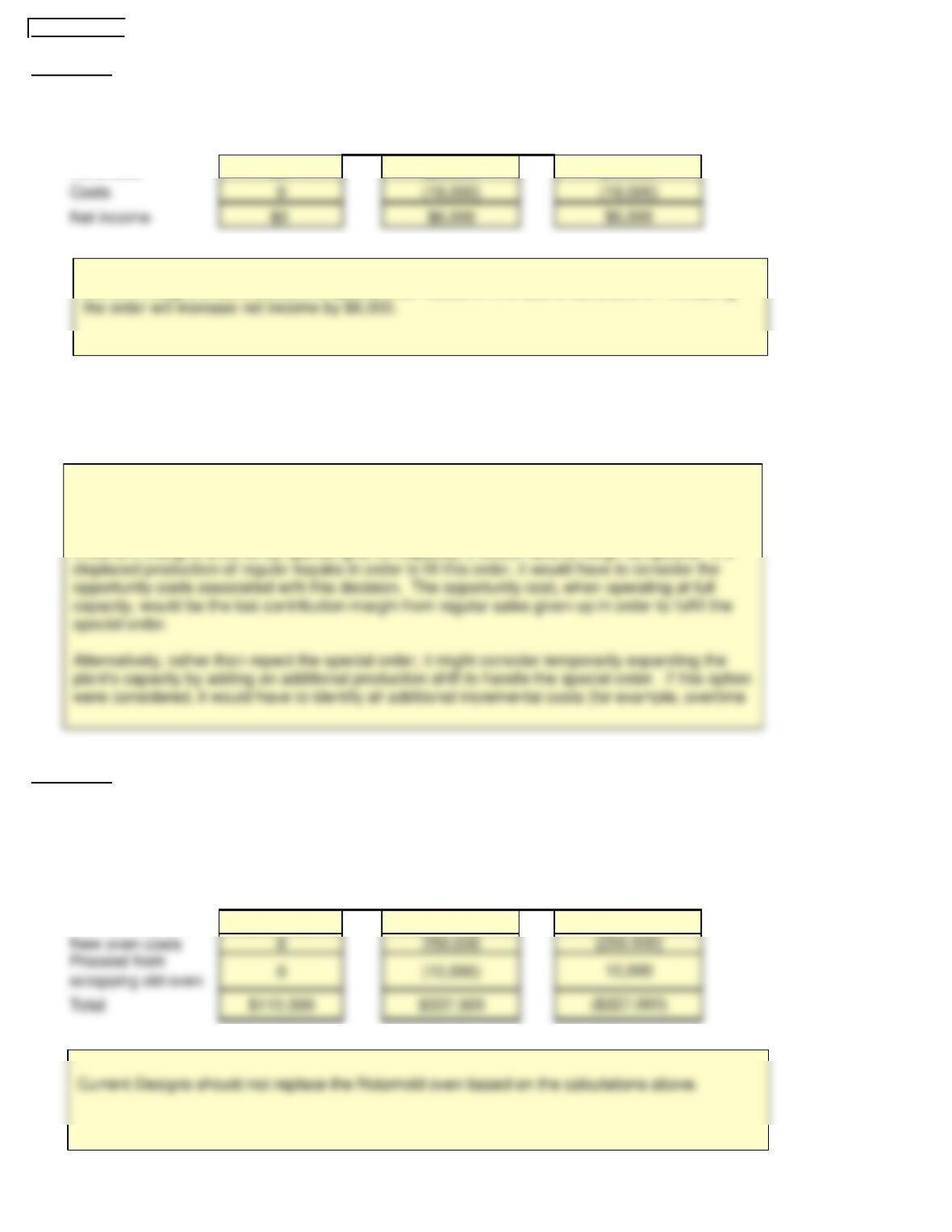

Situation 1

(a) Prepare an incremental analysis to determine whether Current Designs should accept this special order to

produce the coolers.

Reject Order Accept Order Increase (Decrease)

Revenues Value ?

Costs Value ?

Net income ? ?

(b) Discuss additonal factors that Mike and Diane should consider if Current Designs is currently operating at

full capacity.

Situation 2

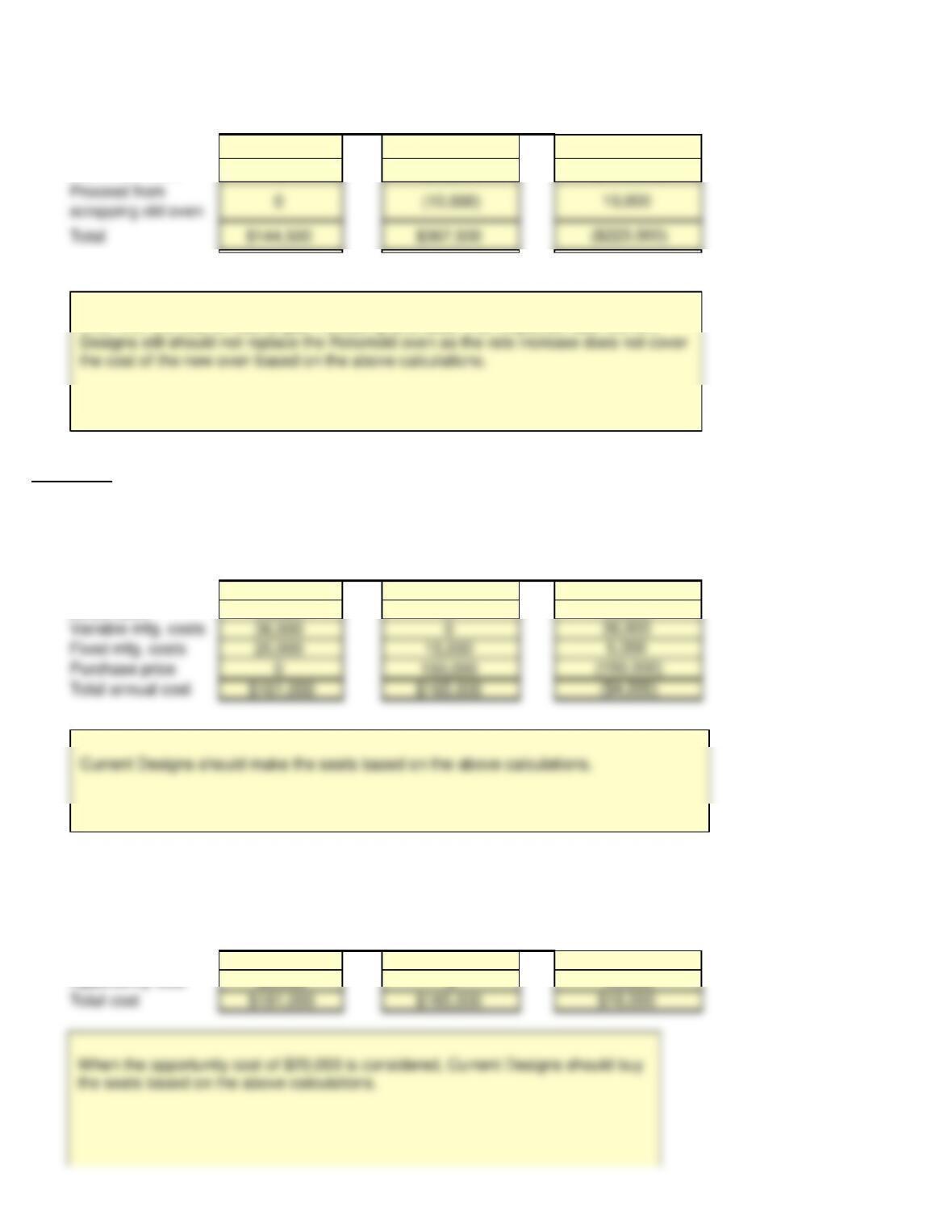

(a) Prepare an incremental analysis to determine if Current Designs should purchase the new rotomold oven,

assuming that the average price for natural gas over the next 10 years will be $0.65 per therm.

Retain Oven Replace Oven

Variable mfg. costs ? ?

New oven costs Value Value

Value Value

Total ? ?

Net Income

Increase

Proceed from

scrapping old oven

Net Income

Value

Value

?

?

?

?

?

Response:

Response:

(b) Diane is concerned that natural gas prices might increase at a faster rate over the next 10 years. If the company

projects that the average natural gas price of the next 10 years could be as high as $0.85 per therm, discuss

how that might change your conclusion in (a).

Retain Oven Replace Oven

Variable mfg. costs ? ?

New oven costs Value Value

Value Value

Total ? ?

Situation 3

(a) Prepare an incremental analysis showing whether Current Designs should make or buy the “Revolution Seating

System.”

Make Buy

Direct materials ? Value

Direct labor ? Value

? Value

Fixed mfg. costs Value ?

Purchase price Value ?

Total annual cost ? ?

(b) Would your answer in (a) change if the productive capacity released by not making the seats could be used to

produce income of $20,000?

Make Buy

Total annual cost Value Value

Opportunity cost Value Value

Total cost ? ?

Net Income

Increase

?

?

Value

?

?

?

Proceed from

scrapping old oven

?

?

Net Income

Increase

Value

?

Value

Variable mfg. costs

Value

Value

Net Income

Increase

Response:

Response:

Response:

After you have completed CD7, consider the following additional questions.

1. Assume in situation 1, the unit selling price changed to $195, fixed overhead changed to $1,800 and

the cost of modifications changed to $3,000. Show the impact of these changes on decision to accept or

reject the special order.

2. Assume in situation 2, the purchase price of the new oven changed to $100,000. Would this change

the decision to retain or replace the oven?

3. Assume in situation 3, that the estimated number of seats to be produced changed to 3,500 and the cost to purchase

one seat from an outside supplier changed to $55. Should Current Designs make or buy the seats?

Response:

CD7 Solution

Situation 1

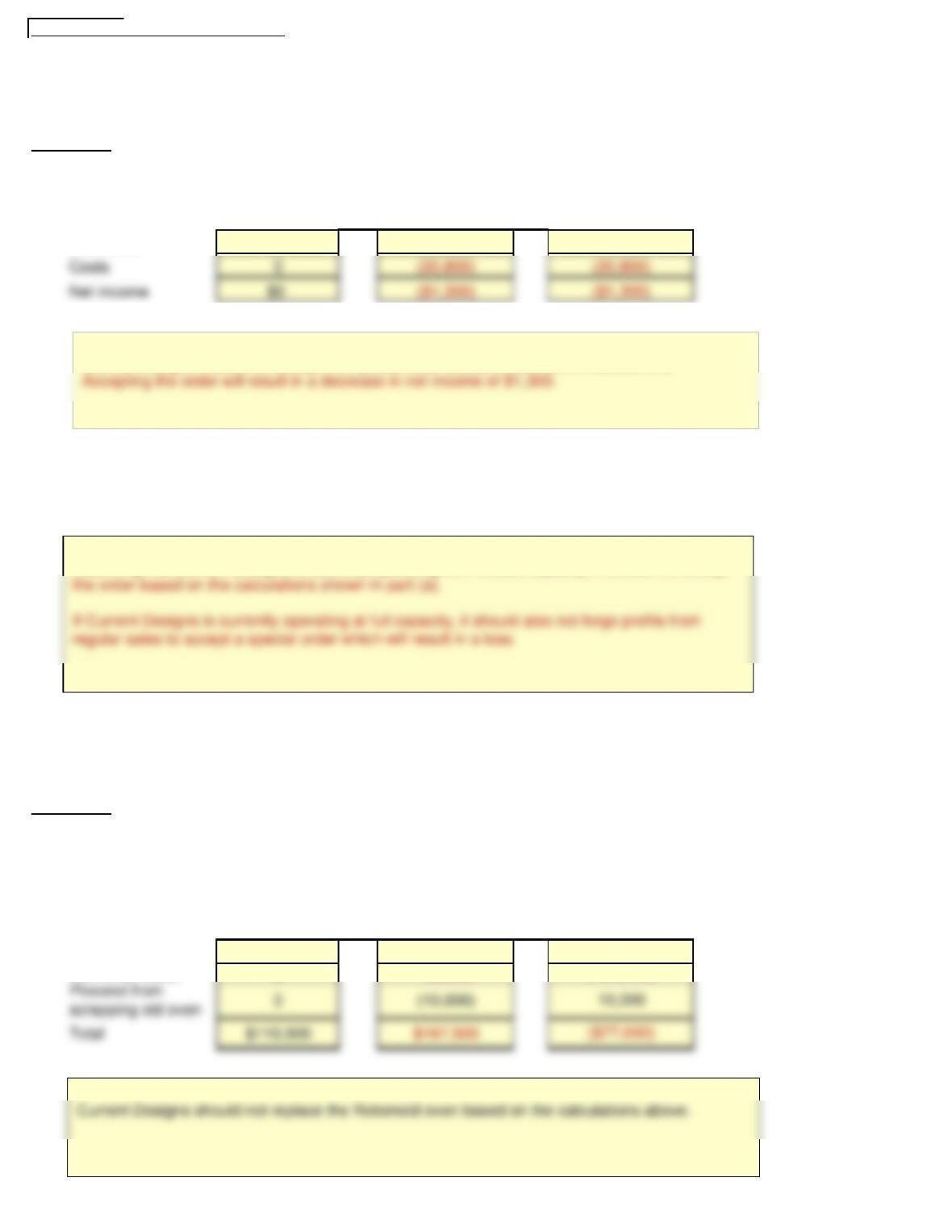

(a) Prepare an incremental analysis to determine whether Current Designs should accept this special order to

produce the coolers.

Reject Order Accept Order Increase (Decrease)

Revenues $0 $25,000

(b) Discuss additonal factors that Mike and Diane should consider if Current Designs is currently operating at

full capacity.

Situation 2

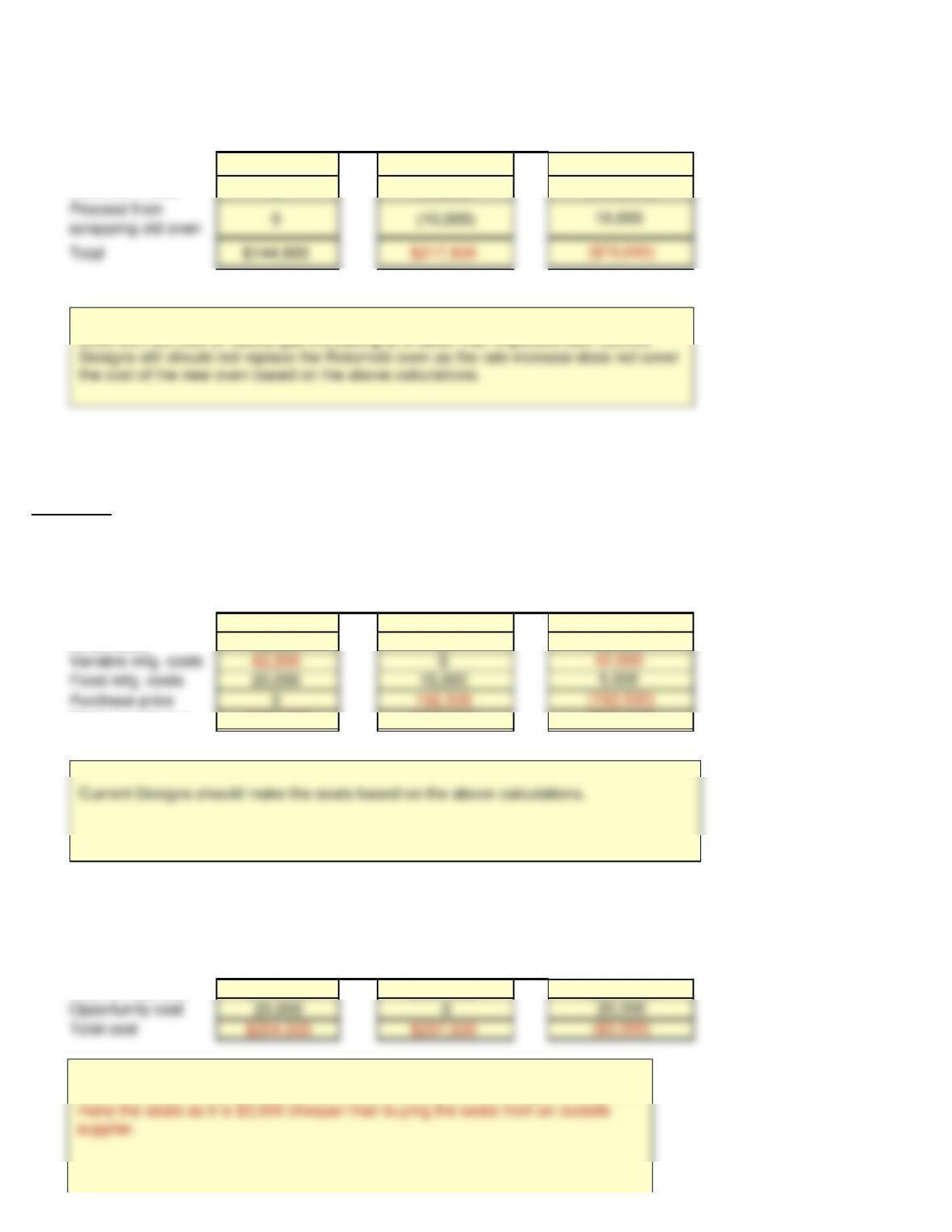

(a) Prepare an incremental analysis to determine if Current Designs should purchase the new Rotomold oven,

assuming that the average price for natural gas over the next 10 years will be $0.65 per therm.

Retain Oven Replace Oven

Variable mfg. costs $110,500 $97,500

Increase

$13,000

Net Income

$25,000

Net Income

Current Designs should accept the special order based on the above calculations. Accepting

Assuming that Current Designs is currently operating with excess capacity, it should accept the

order based on the calculations shown in part (a).

If Current Designs is currently operating at full capacity, it would have to weigh its options. If it

(b) Diane is concerned that natural gas prices might increase at a faster rate over the next 10 years. If the company

projects that the average natural gas price of the next 10 years could be as high as $0.85 per therm, discuss

how that might change your conclusion in (a).

Retain Oven Replace Oven

Variable mfg. costs $144,500 $127,500

New oven costs 0 250,000

Situation 3

(a) Prepare an incremental analysis showing whether Current Designs should make or buy the “Revolution Seating

System.”

Make Buy

36,000

(3, 000 units) (3,000 units)

Direct materials $60,000 $0

Direct labor 45,000 0

(b) Would your answer in (a) change if the productive capacity released by not making the seats could be used to

produce income of $20,000?

Make Buy

(3, 000 units) (3,000 units)

Total annual cost $161,000 $165,000

Opportunity cost 20,000 0

Net Income

Increase

$17,000

(250,000)

Net Income

Increase

$60,000

45,000

20,000

Net Income

Increase

($4,000)

Even with the cost of natural gas increasing at a faster than expected rate, Current

CD7 Solution to additional questions

1. Assume in situation 1, the unit selling price changed to $195, fixed overhead changed to $1,800 and

the cost of modifications changed to $3,000. Show the impact of these changes on decision to accept or

reject the special order.

Situation 1

(a) Prepare an incremental analysis to determine whether Current Designs should accept this special order to

produce the coolers.

Reject Order Accept Order Increase (Decrease)

Revenues $0 $19,500

(b) Discuss additonal factors that Mike and Diane should consider if Current Designs is currently operating at

full capacity.

2. Assume in situation 2, the purchase price of the new oven changed to $100,000. Would this change

the decision to retain or replace the oven?

Situation 2

(a) Prepare an incremental analysis to determine if Current Designs should purchase the new rotomold oven,

assuming that the average price for natural gas over the next 10 years will be $0.65 per therm.

Retain Oven Replace Oven

Variable mfg. costs $110,500 $97,500

New oven costs 0 100,000

$13,000

(100,000)

Increase

Net Income

$19,500

Net Income

Current Designs should not accept the special order based on the above calculations.

Assuming that Current Designs is currently operating with excess capacity, it should not accept

(b) Diane is concerned that natural gas prices might increase at a faster rate over the next 10 years. If the company

projects that the average natural gas price of the next 10 years could be as high as $0.85 per therm, discuss

how that might change your conclusion in (a).

Retain Oven Replace Oven

Variable mfg. costs $144,500 $127,500

New oven costs 0 100,000

3. Assume in situation 3, that the estimated number of seats to be produced changed to 3,500 and the cost to purchase

one seat from an outside supplier changed to $55. Should Current Designs make or buy the seats?

Situation 3

(a) Prepare an incremental analysis showing whether Current Designs should make or buy the “Revolution Seating

System.”

Make Buy

42,000

(3, 500 units) (3,500 units)

Direct materials $70,000 $0

Direct labor 52,500 0

Total annual cost $184,500 $207,500

(b) Would your answer in (a) change if the productive capacity released by not making the seats could be used to

produce income of $20,000?

Make Buy

(3, 000 units) (3,000 units)

Total annual cost $184,500 $207,500

($23,000)

Net Income

Increase

($23,000)

Net Income

Increase

$70,000

52,500

Net Income

Increase

$17,000

(100,000)

When the opportunity cost of $20,000 is considered, Current Designs should still