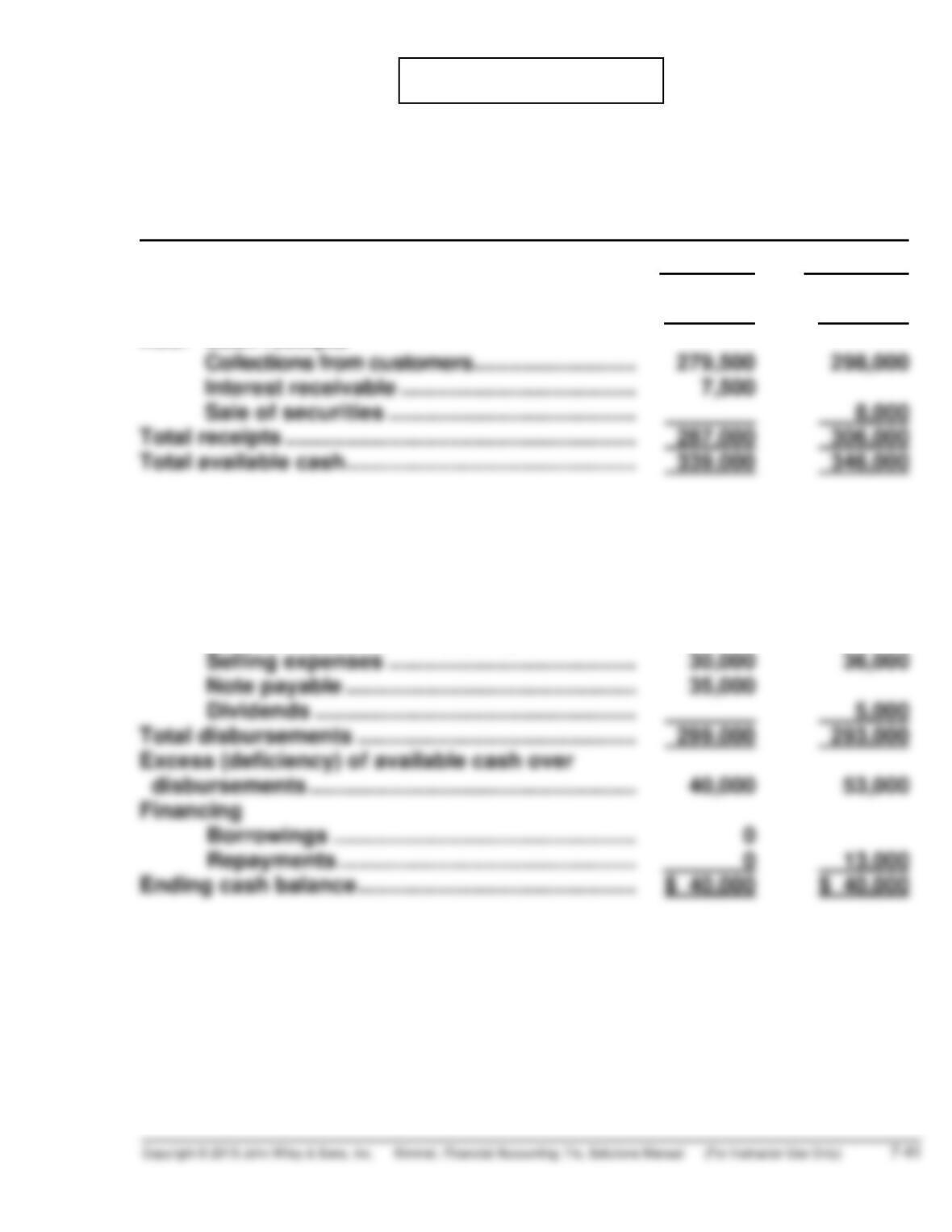

PROBLEM 7-7B

NOBLE CORPORATION

Cash Budget

For the Two Months Ending February 28, 2014

January February

Beginning cash balance …………………………………. $ 52,000 $ 40,000

Add: Cash receipts

Less: Cash disbursements

Purchases ……………………………………………. 106,000 116,000

Salaries ………………………………………………… 72,000 78,000

Administrative expenses (Jan. $58,000 –

$2,000; Feb. $60,000 – $2,000) ……………….. 56,000 58,000

PROBLEM 7-8B

(a) ELITE SERVICE COMPANY

Bank Reconciliation

March 31, 2014

Balance per bank statement ……………………………………….. $5,931.51

Plus: Undeposited receipts ……………………………………….. 1,591.63

7,523.14

Less: Outstanding checks

No. Amount No. Amount

206

441

590

$358.53

292.00

283.00

781

782

783

$286.00

319.47

303.14

1,842.14

Adjusted balance per bank …………………………………………. $5,681.00

Cash balance per books …………………………………………….. $6,889.53

Add: Bank credit (collection of note receivable) ………… 175.00

Adjusted balance per books (before theft) ………………….. 7,064.53

Theft ($7,064.53 – $5,681.00) ………………………………………. 1,383.53

Adjusted balance per books ………………………………………. $5,681.00

(b) The cashier attempted to cover the theft of $1,383.53 by:

1. Not listing as outstanding three checks totaling $933.53 (No. 206,

$358.53; No. 441, $292.00; and No. 590, $283.00).

2. Underfooting the outstanding checks listed by $100. (The correct

total is $908.61.)

3. Subtracting the $175 credit from the bank balance instead of add-

ing it to the book balance, thereby concealing $350 of the theft.

PROBLEM 7-8B (Continued)

(c) 1. The principle of independent internal verification has been violated

because the cashier prepared the bank reconciliation.

COMPREHENSIVE PROBLEM SOLUTION

(a) Dec. 7 Cash …………………………………………………..

.

Accounts Receivable ……………………

.

3,600

3,600

12 Inventory …………………………………………….

.

Accounts Payable …………………………

.

12,000

12,000

.

.

22 Accounts Payable ……………………………….

.

Cash ($12,000 X .99) ……………………..

.

Inventory ……………………………………..

.

12,000

11,880

120

.

.

.

COMPREHENSIVE PROBLEM SOLUTION (Continued)

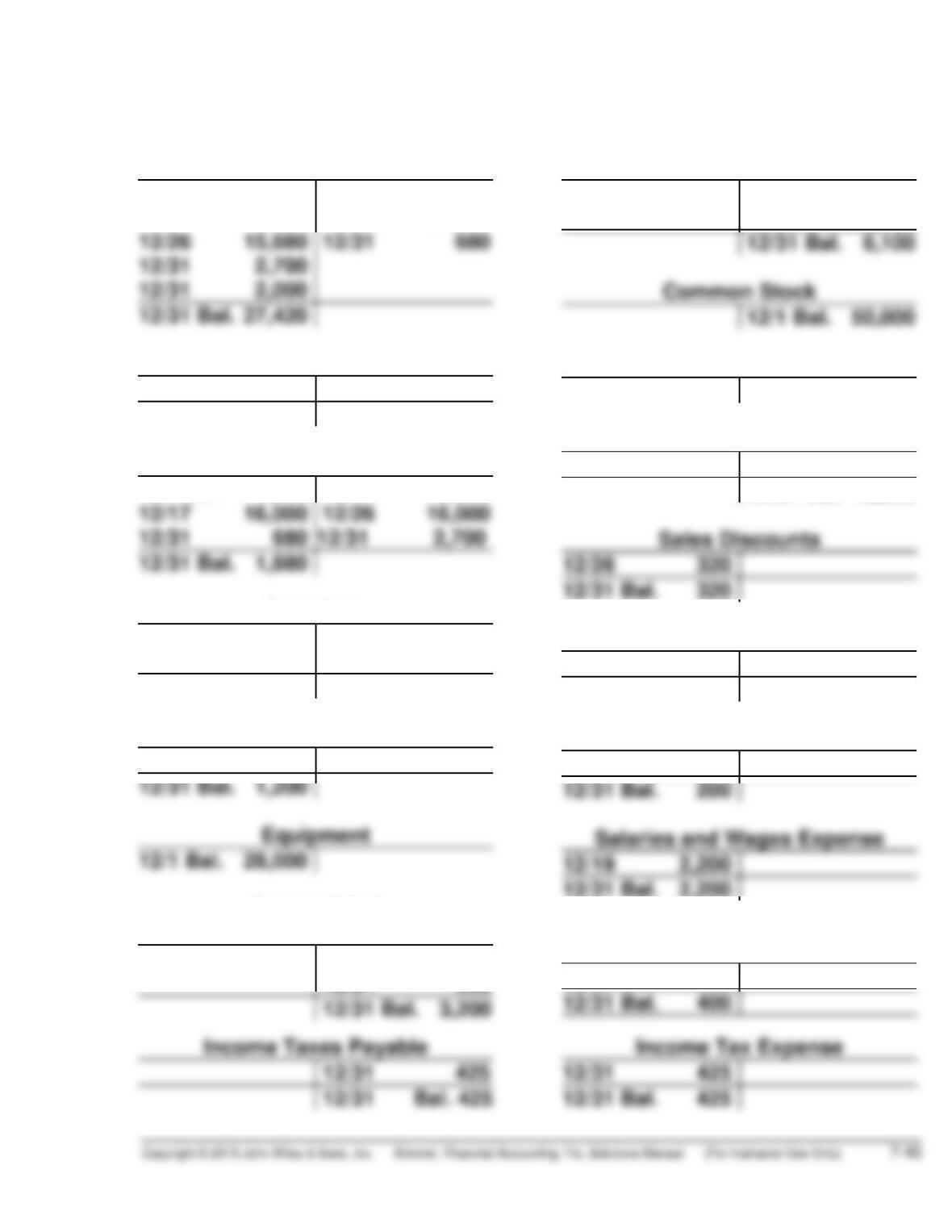

(b) & (e) General Ledger

Cash

12/1 Bal. 18,200

12/7 3,600

12/19 2,200

12/22 11,880

Notes Receivable

12/1 Bal. 2,000 12/31 2,000

12/31 Bal. – 0 –

Accounts Receivable

12/1 Bal. 7,500

12/7 3,600

Inventory

12/1 Bal. 16,000

12/12 12,000

12/17 10,000

12/22 120

12/31 Bal. 17,880

Prepaid Insurance

12/1 Bal. 1,600 12/31 400

Accumulated

Depreciation—Equipment

12/1 Bal. 3,000

12/31 200

Accounts Payable

12/22 12,000 12/1 Bal. 6,100

12/12 12,000

Retained Earnings

12/1 Bal. 14,200

Sales Revenue

12/17 16,000

12/31 Bal. 16,000

Cost of Goods Sold

12/17 10,000

12/31 Bal. 10,000

Depreciation Expense

12/31 200

12/31 Bal. 2,200

Insurance Expense

12/31 400

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(c) HAVENHILL COMPANY

Bank Reconciliation

December 31, 2014

Cash balance per bank statement …………………….. $25,930

Add: Deposits in transit ……………………………………. 2,700

28,630

(d) Dec. 31 Cash ………………………………………………….. 2,000

Notes Receivable …………………………. 2,000

31 Insurance Expense …………………………….. 400

Prepaid Insurance ………………………… 400

31 Income Tax Expense ………………………….. 425

Income Taxes Payable ………………….. 425

COMPREHENSIVE PROBLEM SOLUTION (Continued)

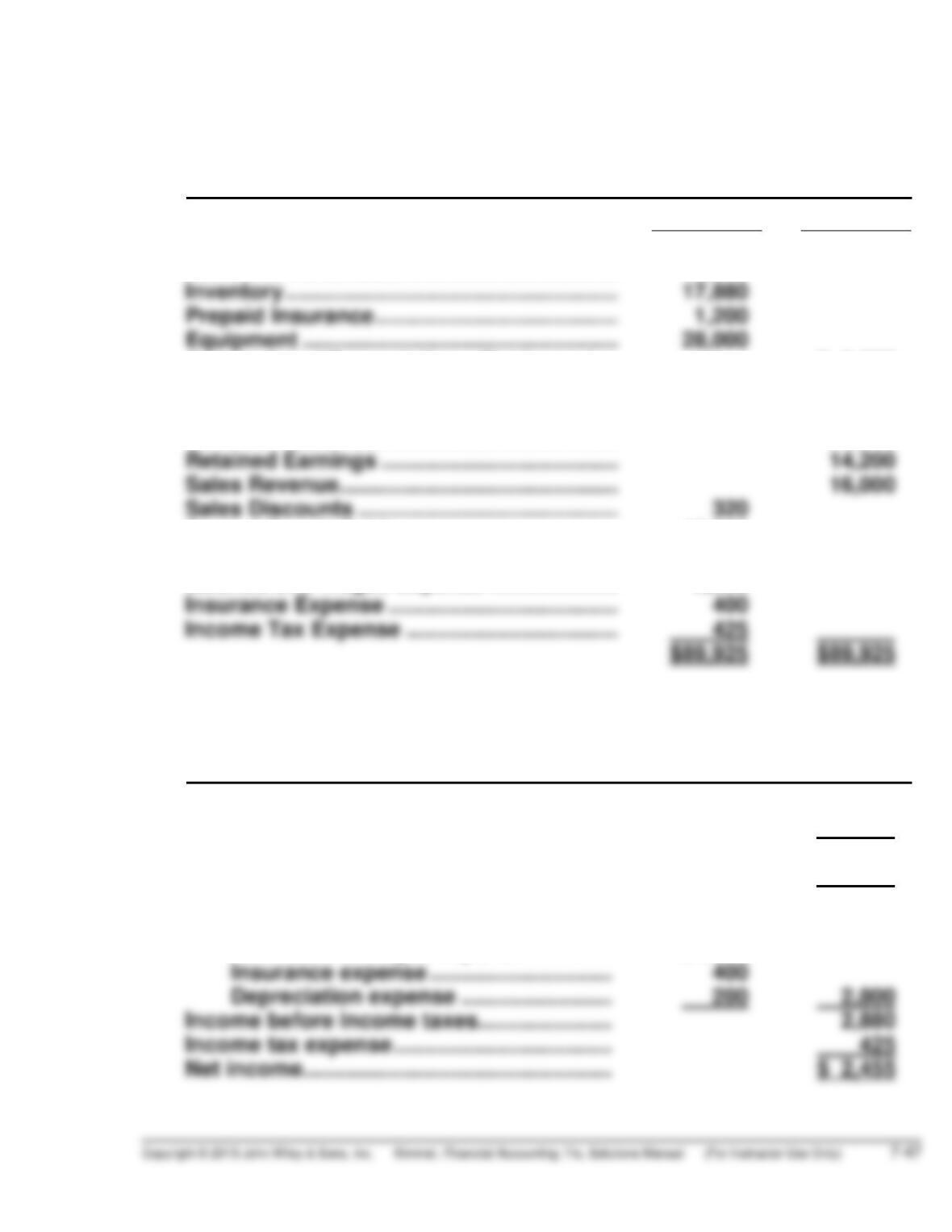

(f) HAVENHILL COMPANY

Adjusted Trial Balance

December 31, 2014

DR. CR.

Cash …………………………………………………….. $27,420

Accounts Receivable…………………………….. 1,880

Accumulated Depreciation

—

Equipment…. $ 3,200

Accounts Payable …………………………………. 6,100

Income Taxes Payable…………………………… 425

Common Stock ……………………………………… 50,000

Cost of Goods Sold ………………………………. 10,000

Depreciation Expense …………………………… 200

Salaries and Wages Expense ………………… 2,200

(g) HAVENHILL COMPANY

Income Statement

For the Month Ending December 31, 2014

Sales revenue ………………………………………. $16,000

Less: Sales discounts …………………………. 320

Net sales ……………………………………………… 15,680

Cost of goods sold ………………………………. 10,000

Gross profit …………………………………………. 5,680

Operating expenses

Salaries and wages expense ………….. $2,200

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(g) HAVENHILL COMPANY

Balance Sheet

December 31, 2014

Assets

Current assets

Cash ………………………………………………… $27,420

Accounts receivable …………………………. 1,880

Property, plant, and equipment

Equipment ………………………………………. 28,000

Less: Accumulated

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable …………………………….. $6,100

Income taxes payable ……………………….. 425 $6,525

Stockholders’ equity

BYP 7-1 FINANCIAL REPORTING PROBLEM

(a) The first paragraph of the independent registered public accounting

firm’s report states that: In our opinion, the accompanying consolidated

statements of financial position and the related consolidated statements

(b) The consolidated statement of financial position shows the combined

cash and cash equivalent balances (in thousands) at December 31,

2011 and 2010:

(c) The consolidated statement of cash flows indicates that three activities

(d) The notes say: The company considers temporary cash investments

with an original maturity of three months or less to be cash equivalents.

(e) The management of Tootsie Roll Industries, Inc. is responsible for estab-

lishing and maintaining adequate internal control over financial reporting.

After performing an evaluation of company procedures, management

concluded that its internal control over financial reporting was effective.

BYP 7-2 COMPARATIVE ANALYSIS PROBLEM

(In thousands)

Tootsie

Roll

Hershey

Company

(c) Cash provided by operating activities $50,390 $580,867

(d) The objective in cash management is to ensure that a company has

sufficient cash to meet payments as they come due, yet minimize the

amount of non-revenue-generating cash on hand. The decrease in cash as

a percentage of total assets experienced by both companies is a cause

BYP 7-3 RESEARCH CASE

(a) The article lists 8 different forms of payment. They are: wire transfer,

paper checks, automated clearing house (ACH) credits, ACH debits, pur-

chasing cards (p-cards), paying from statements, petty cash, payment

via travel and expense (T&E) reimbursement.

(c) The controls suggested in the article are:

1. Limit payment type i.e. only p-card.

2. Make sure purchase orders are extinguished whenever a payment

is made.

BYP 7-4 INTERPRETING FINANCIAL STATEMENTS

(a) The global percentage of companies that experienced a significant

instance of fraud during the period covered by the survey was 16%

and Western Europe had the highest rate at 21%.

(b) 44% of survey respondents performed a fraud risk assessment in the

six months prior to the survey. 15% of survey respondents have never