199

CHAPTER 7

FIXED ASSETS AND INTANGIBLE ASSETS

CLASS DISCUSSION QUESTIONS

1. Fixed assets have the following characteris-

tics:

(a) They exist physically and thus are tan-

gible assets.

2. a. Property, plant, and equipment

b. Current assets (merchandise inventory)

3. Real estate acquired as speculation should

be listed in the balance sheet under the cap-

tion “Investments,” below the Current Assets

section. Investments are long-lived assets

that are not used in the normal operations

and are held for future resale.

4. $475,000

7. a. Capital expenditure

b. Revenue expenditure (Note: Changing oil

is a normal maintenance expense.)

c. Capital expenditure

8. Ordinarily not; if the book values closely

approximate the market values of fixed as-

sets, it is coincidental. Depreciation does not

measure a decline in the market value of a

fixed asset. Instead, depreciation is an allo-

alent outlay of cash in the period to

which the expense is allocated.

b. Depreciation is the cost of fixed assets

periodically charged to revenue over

tion for all fixed assets.

b. No

12. a. An accelerated depreciation method is

most appropriate for situations in which

the decline in productivity or earning

power of the asset is proportionately

greater in the early years of use than in

later years, and the repairs tend to in-

crease with the age of the asset.

asset cannot exceed the cost of the as-

set. To do so would create a negative

book value, which is meaningless.

b. The cost and accumulated depreciation

should be removed from the accounts

when the asset is no longer useful and it

is removed from service. Presumably,

the asset will then be sold, traded in, or

discarded.

EXERCISES

E7–1

E7–2

a. Yes. All expenditures incurred for the purpose of making the land suitable for

its intended use should be recorded as an increase in the land account.

E7–3

Initial cost of land ($100,000 + $400,000) ……………… $500,000

E7–4

Capital expenditures: 3, 4, 5, 6, 7, 9, 10

Revenue expenditures: 1, 2, 8

E7–5

E7–6

a. No. The $8,300,000 represents the original cost of the equipment. Its replace-

E7–7

(a) 50% (1/2); (b) 25% (1/4); (c) 10% (1/10); (d) 5% (1/20); (e) 4% (1/25); (f) 2.5%

(1/40); (g) 2% (1/50)

E7–9

First Year Second Year

a. 2.5% of $240,000 = $6,000 2.5% of $240,000 = $6,000

E7–10

a. 5% of ($210,000 – $30,000) = $9,000, or [($210,000 – $30,000) ÷ 20]

202

E7–11

a. 20Y5: 3/12 × [($42,000 – $6,000) ÷ 10] = $900

E7–12

a.

Year 1 Year 2

Vehicles ………………………………………… $ 5,981 $ 5,519

Aircraft ………………………………………….. 14,616 14,063

Land ……………………………………………… 1,114 1,081

b. A comparison of Years 1 and 2 reveals that each category of asset increased

during Year 2. UPS expanded its operations during Year 2 by $1,321 ($36,541

– $35,220) from purchases of property, plant, and equipment. At the same

time, accumulated depreciation also increased by $1,087 ($18,920 – $17,833).

203

E7–13

a.

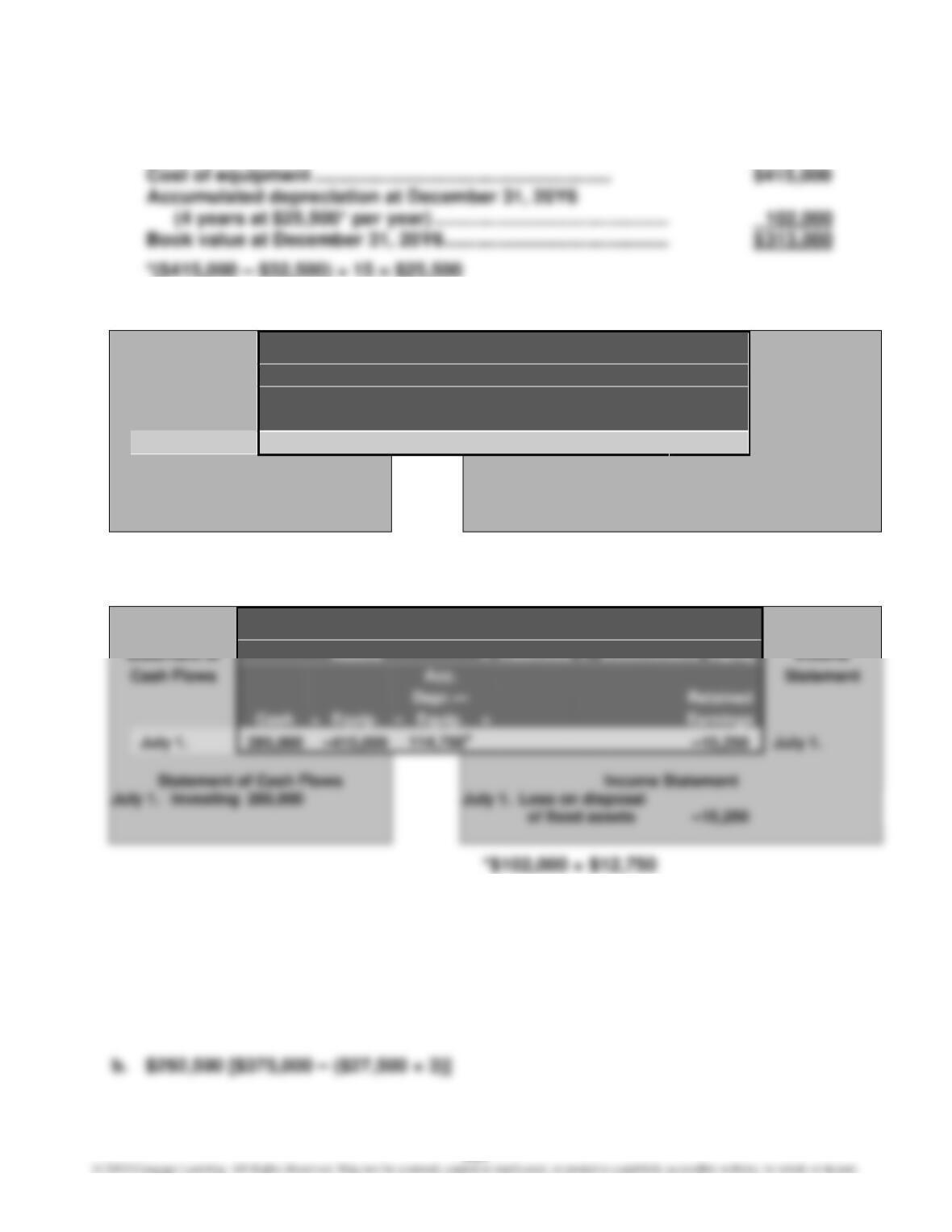

b. 1.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

– Acc. Depr.—

Retained

Statement

Equipment

=

Earnings

July 1.

–12,750

–12,750

July 1.

Income Statement

July 1. Depr. expense

–12,750*

*$25,500 × 6/12

2.

Balance Sheet

Statement of

Income

–

Equip.

Earnings

July 1.

–15,250

July 1.

–15,250

E7–14

a. 20Y1 depreciation expense: $27,500 [($375,000 – $45,000) ÷ 12]

20Y2 depreciation expense: $27,500

20Y3 depreciation expense: $27,500

204

E7–14, Concluded

c.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Acc.

Statement

Depr.—

Retained

Cash

+

Equip.

–

Equip.

=

Earnings

Jan. 7.

280,000

–375,000

82,500

Jan. 7.

of fixed assets

–12,500

d.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Acc.

Statement

Depr.—

Retained

Cash

+

Equip.

–

Equip.

=

Earnings

Jan. 7.

300,000

–375,000

82,500

7,500

Jan. 7.

of fixed assets

7,500

E7–15

a. $16,500,000 ÷ 75,000,000 tons = $0.22 depletion per ton

29,800,000 × $0.22 = $6,556,000 depletion expense

b.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Retained

Statement

Depletion

=

Earnings

Depletion exp.

–6,556,000

205

E7–16

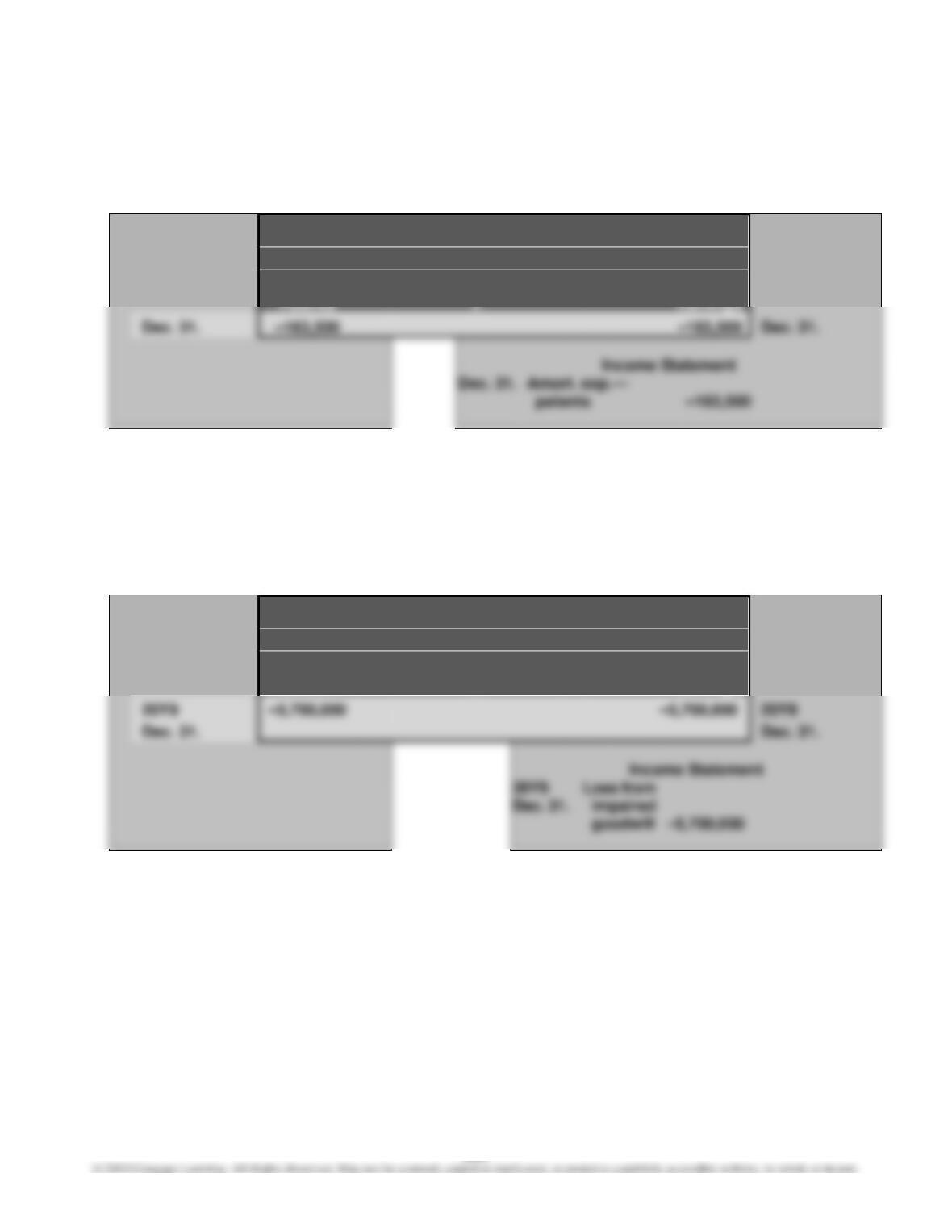

a. ($1,350,000 ÷ 10) + ($199,500 ÷ 7) = $163,500 total patent expense

b.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Retained

Statement

=

E7–17

a. $8,000,000. The goodwill is not amortized; thus, the book value of goodwill

has remained unchanged since originally recognized on January 1, 20Y3.

b.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Retained

Statement

Goodwill

=

Earnings

206

E7–18

a. Property, Plant, and Equipment (in millions):

Year 2 Year 1

Land and buildings ……………………………………………. $ 2,439 $ 2,059

Machinery, equipment, and internal-use software . 15,743 6,926

Office furniture and equipment ………………………….. 241 184

Other fixed assets related to leases …………………… 3,464 2,599

b. The book value of fixed assets should normally increase during the year.

Although additional depreciation expense will reduce the book value, most

companies invest in new assets in an amount that is at least equal to the

depreciation expense. However, during periods of economic downturn, com-

panies purchase fewer fixed assets, and the book value of their fixed assets

may decline.

E7–19

1. Fixed assets should be reported at cost and not replacement cost.

PROBLEMS

P7–1

1.

Land Other

Item Land Improvements Building Accounts

a. $ 75,000

b. $ 18,000

c. 12,500

d. $ 14,500

m. (775,000)*

n. 800,000

o. (4,500)*

p. 6,000

q. (6,500)*

r. (1,000)*

s. 9,000

2. $ 470,250 $ 26,500 $ 920,000

*Receipt

3. Since land used as a plant site does not lose its ability to provide services, it

208

P7–2

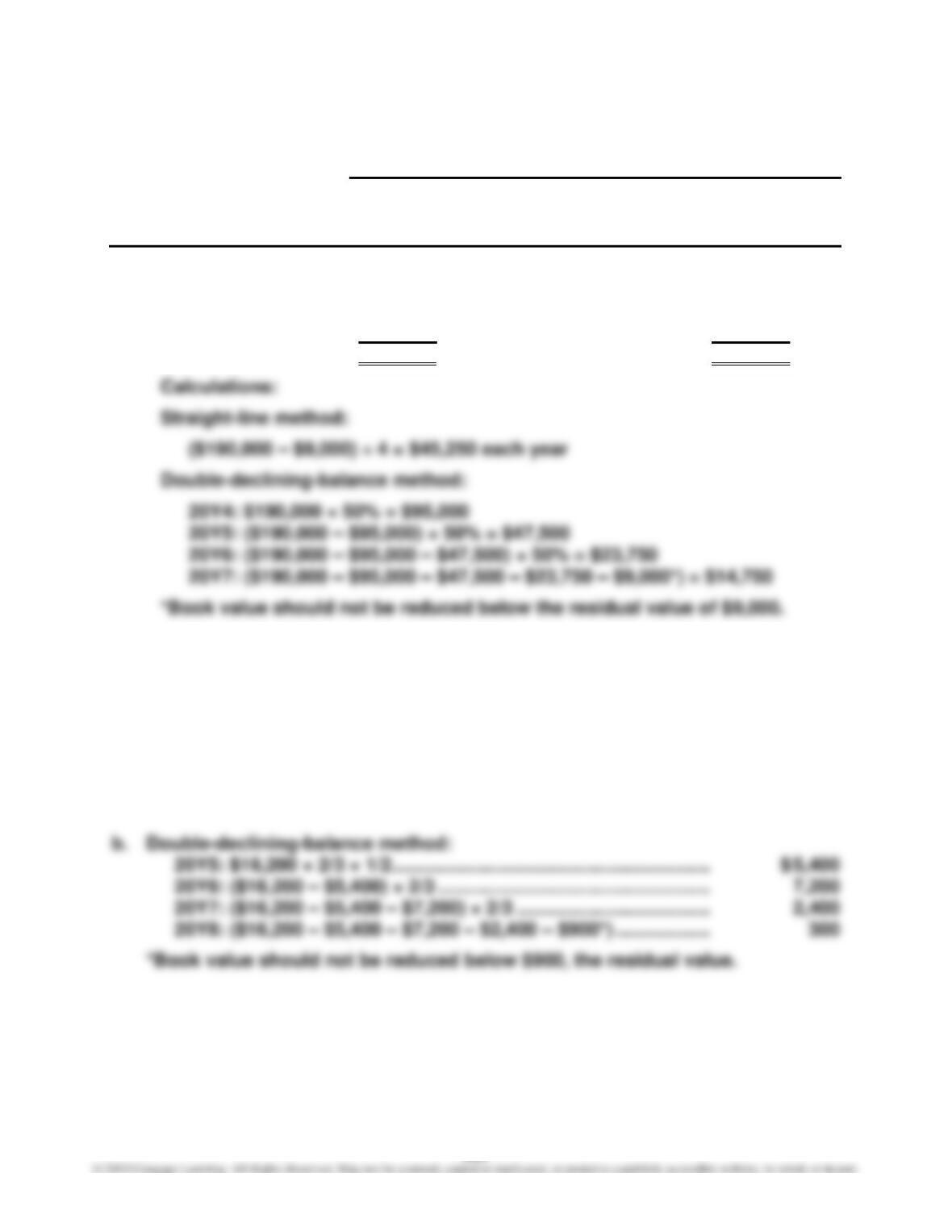

Depreciation Expense

a. Straight- b. Double-

Line Declining-Balance

Year Method Method

20Y4 $ 45,250 $ 95,000

20Y5 45,250 47,500

20Y6 45,250 23,750

20Y7 45,250 14,750*

Total $181,000 $ 181,000

P7–3

a. Straight-line method:

20Y5: [($16,200 – $900) ÷ 3] × 1/2 ……………………………………….. $ 2,550

20Y6: ($16,200 – $900) ÷ 3 …………………………………………………. 5,100

20Y7: ($16,200 – $900) ÷ 3 …………………………………………………. 5,100

20Y8: [($16,200 – $900) ÷ 3] × 1/2 ……………………………………….. 2,550

P7–4

1.

Accumulated

Depreciation Depreciation, Book Value,

Year Expense End of Year End of Year

a. 1 $32,500* $ 32,500 $ 107,500

2 32,500 65,000 75,000

3 32,500 97,500 42,500

2.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Acc.

Statement

Depr.—

Retained

Cash

+

Equip.

–

Equip.

=

Earnings

23,300

–140,000

122,500

5,800*

Statement of Cash Flows

Income Statement

Investing

23,300

Gain on disposal

of equipment

5,800

*[$23,300 – ($140,000 – $122,500)]

3.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Acc.

Statement

Depr.—

Retained

Cash

+

Equip.

–

Equip.

=

Earnings

Statement of Cash Flows

Income Statement

Investing

Loss on disposal

of equipment