Continuing Cookie Chronicle 1

Continuing Cookie Chronicle

(Note: This is a continuation of the Cookie Chronicle from Chapters 1 through 6.)

CCC7 Part 1 Natalie is struggling to keep up with the recording of her accounting

transactions. She is spending a lot of time marketing and selling mixers and

giving her cookie classes. Her friend John is an accounting student who runs his

own accounting service. He has asked Natalie if she would like to have him do

her accounting.

John and Natalie meet and discuss her business. John suggests that he do

the following for Natalie.

1. Hold onto cash until there is enough to be deposited. (He would keep the

cash locked up in his vehicle). He would also take all of the deposits to the

bank at least twice a month.

2. Write and sign all of the checks.

3. Record all of the deposits in the accounting records.

4. Record all of the checks in the accounting records.

5. Prepare the monthly bank reconciliation.

6. Transfer all of Natalie’s manual accounting records to his computer

accounting program. John maintains all of the accounting information that

he keeps for his clients on his laptop computer.

7. Prepare monthly financial statements for Natalie to review.

8. Write himself a check every month for the work he has done for Natalie.

Instructions

Identify the weaknesses in internal control that you see in the system that John is

recommending. (Consider the principles of internal control identified in the

chapter.) Can you suggest any improvements if John is hired to do Natalie’s

accounting?

Part 2 Natalie decides that she cannot afford to hire John to do her accounting.

One way that she can ensure that her cash account does not have any errors

and is accurate and up–to-date is to prepare a bank reconciliation at the end of

each month.

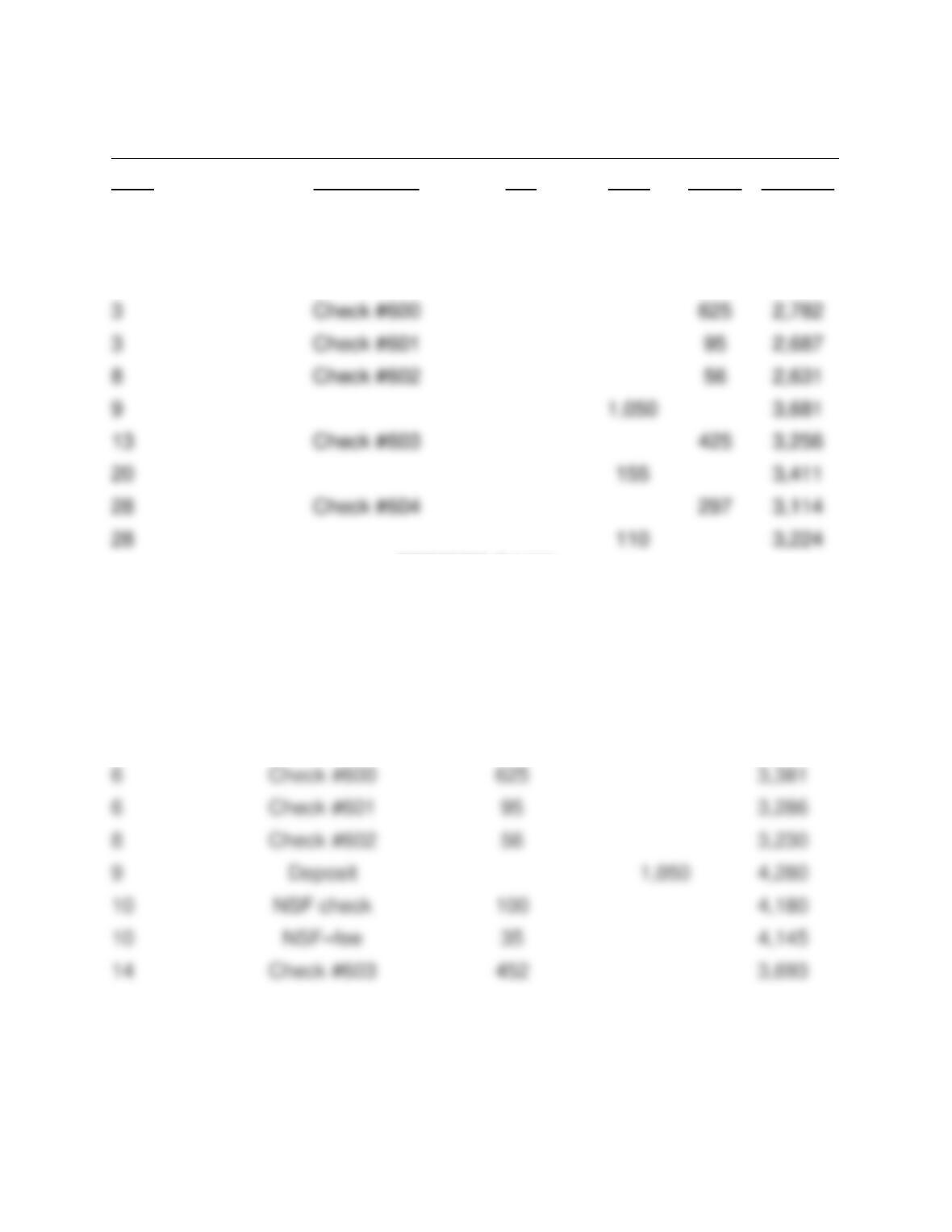

GENERAL LEDGER—COOKIE CREATIONS INC.

Cash

Date

2015

Explanation

Ref

Debit

Credit

Balance

June 1

Balance

2,657

1

750

3,407

3

625

2,782

3

2,687

8

2,631

9

1,050

3,681

425

3,256

155

3,411

297

3,114

110

3,224

PREMIER BANK

Statement of Account—Cookie Creations Inc.

June 30, 2015

Date

Explanation

Checks and Other

Debits

Deposits

Balance

May 31

Balance

3,256

June 1

Deposit

750

4,006

3,381

95

3,286

56

3,230

Deposit

4,280

10

4,180

10

35

4,145

14

3,693

20

Deposit

125

3,818

23

EFT–Telus

85

3,733

28

Check #599

361

3,372

30

Bank charges

13

3,359

Additional information:

1. On May 31, there were two outstanding checks: #595 for $238 and #599

for $361.

2. Premier Bank made a posting error to the bank statement: check #603 was

issued for $425, not $452.

Instructions

(a) Prepare Cookie Creations’ bank reconciliation for June 2015.

(b) Prepare any necessary general journal entries.

(c) If a balance sheet is prepared for Cookie Creations Inc. at June 30, 2015,

what balance will be reported as cash in the current assets section?

Part 1

The weaknesses in internal accounting controls in the system recommended by

John are:

(1) The cash could be stolen from John’s car before it is deposited in the

bank.

Improvements should include the following:

(1) Cash should be deposited in the bank daily. At a minimum cash

should be locked in a safe until it can be deposited.

(2) John should be responsible for the accounting function only. Natalie

(or some other independent person) should sign all checks and

make all deposits. Checks should only be signed when there is

documentation present to support the payment. All invoices should

be stamped “PAID” to avoid duplicate payment.

(5) John should submit a monthly invoice for the work he has done to

Natalie for her approval. Natalie should then write and sign the check.

Part 2

(a) COOKIE CREATIONS INC.

Bank Reconciliation

June 30, 2015

Cash balance per bank statement ……………………………..

$3,359

Add: Deposit in transit …………………………………………….

$110

Bank error Check No. 603 ($452 – $425) …………

Less: Outstanding checks ($238 + $297) ……………………

Cash balance per books ……………………………………………

NSF check ($100 + $35 service charge)…………..

(b)

June 30

Miscellaneous Expense ………………………….

13

Cash …………………………………………….

13

Service Revenue …………………………………….

30

30

85

85

Accounts Receivable—Ron Black …………..