CHAPTER 7

SOLUTIONS TO PROBLEMS: SET B

PROBLEM 7-1B

(a)

Reject

Order

Accept

Order

Net Income

Increase

(Decrease)

Revenues (10,000 X $30)

Cost of goods sold

$0

0

$300,000

240,000

(1)

$ 300,000

( (240,000)

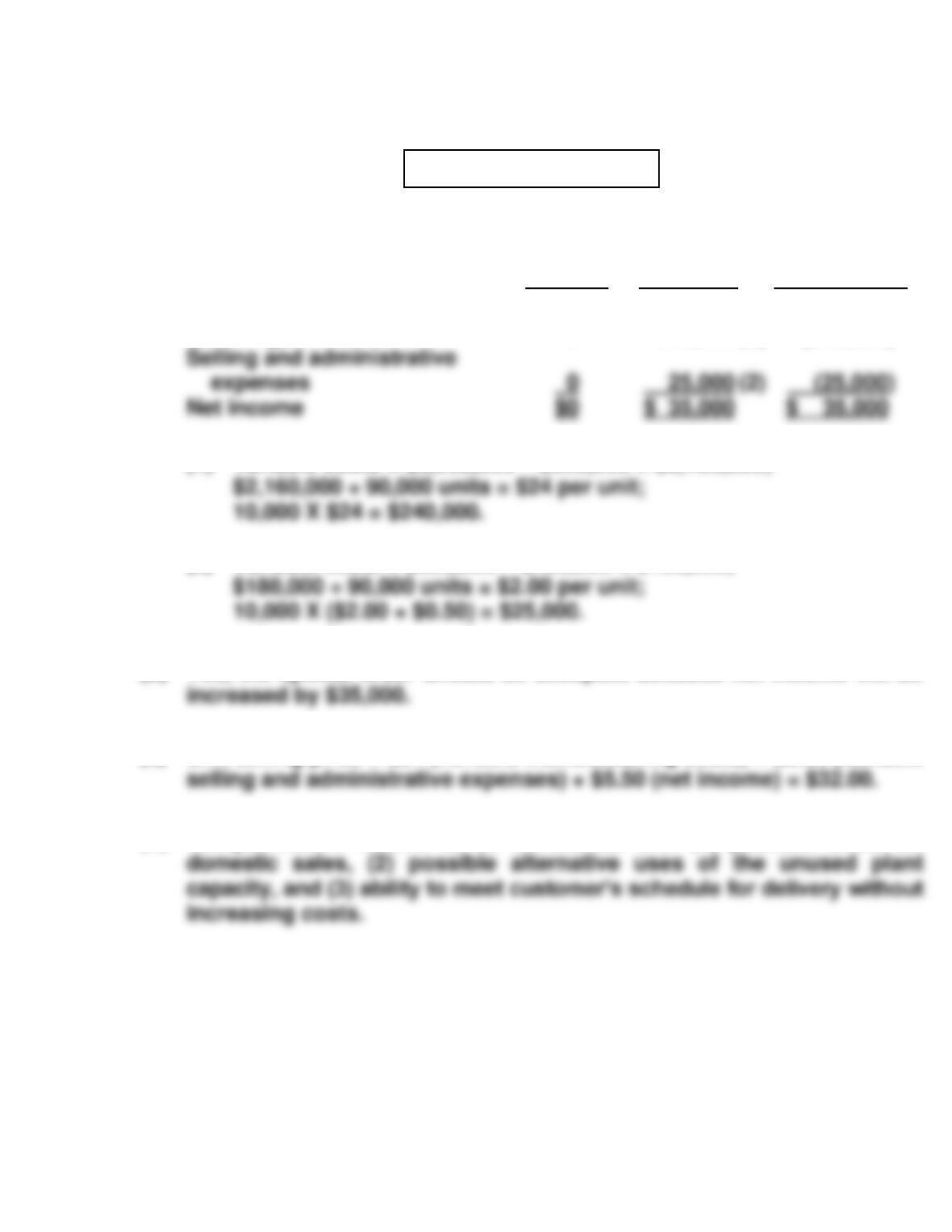

(1) Variable costs = $3,060,000 – $900,000 = $2,160,000;

(2) Variable costs = $360,000 – $180,000 = $180,000;

(b) Yes, the special order should be accepted because net income will be

(c) Unit selling price = $24 (variable manufacturing costs) + $2.50 (variable

(d) Nonquantitative factors to be considered are: (1) possible effect on

PROBLEM 7-2B

(a)

Make FIZBE

Buy FIZBE

Net Income

Increase

(Decrease)

Direct materials (5,000 X $4.75)

Direct labor (5,000 X $4.60)

Indirect labor (5,000 X $.45)

$23,750

23,000

2,250

$ 0

0

0

($ 23,750

( 23,000

( 2,250

(b) The company should continue to make FIZBE because net income

(c) The decision would be different. Because of the opportunity cost of

$6,000, net income will be $1,250 higher if FIZBE is purchased as shown

below:

Make FIZBE

Buy FIZBE

Net Income

Increase

(Decrease)

(d) Nonfinancial factors include: (1) the adverse effect on employees

if FIZBE is purchased, (2) how long the supplier will be able to satisfy

PROBLEM 7-3B

(a) (1)

General-Purpose Cleaner Not Processed Further

Sales

ShineBrite (750,000 ÷ 25) X $15

$450,000

General-Purpose Cleaner (250,000 ÷ 20) X $20

250,000

Total revenue

$700,000

(2)

General-Purpose is Processed Further

Sales

ShineBrite (750,000 ÷ 25) X $15

$450,000

Premium Cleaner (250,000 ÷ 20) X $16

200,000

Premium Stain Remover (250,000 ÷ 20) X $16

200,000

Total revenue

$850,000

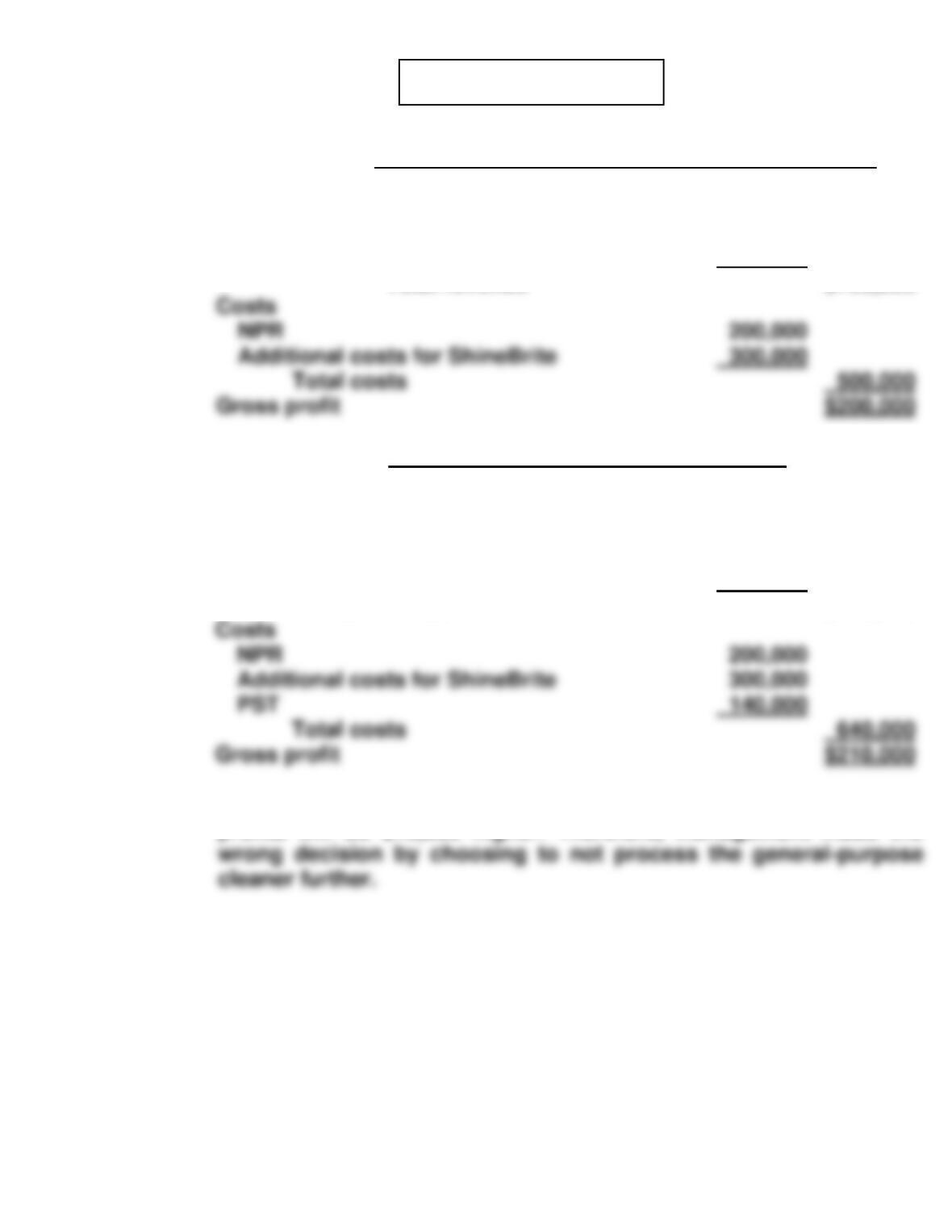

Costs

NPR

Additional costs for ShineBrite

140,000

Total costs

Gross profit

$210,000

(3) If the general-purpose cleaner is processed further overall company

profits will be $10,000 higher. Therefore, management made the

Costs

NPR

200,000

Additional costs for ShineBrite

300,000

Gross profit

$200,000

PROBLEM 7-3B (Continued)

(b)

Don’t Process

G-P Cleaner

Further

Process

G-P Cleaner

Further

Net Income

Increase

(Decrease)

PROBLEM 7-4B

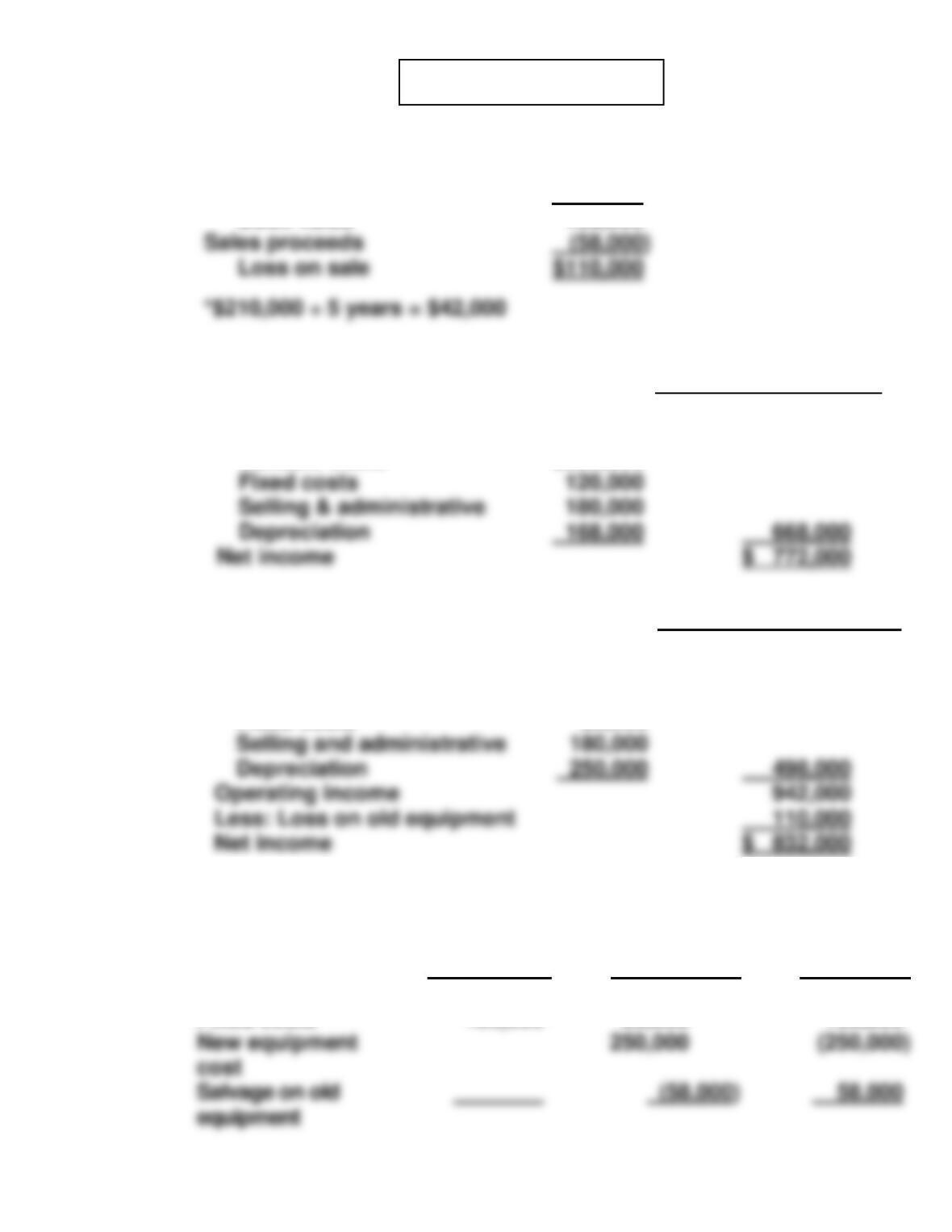

(a)

Cost

$210,000

Accumulated depreciation

(42,000*)

Book value

168,000

Sales proceeds

Loss on sale

(b) (1)

Retain Old Equipment

Revenues ($360,000 X 4 yrs.)

$1,440,000

Less costs:

Variable costs

$200,000

Fixed costs

120,000

Selling & administrative

180,000

Depreciation

Net income

$ 772,000

(2)

Replace Old Equipment

Revenues

$1,440,000

Less costs:

Variable costs

$ 48,000

Fixed costs

20,000

Selling and administrative

Depreciation

Operating income

Less: Loss on old equipment

Net income

(c)

Retain Old

Equipment

Replace Old

Equipment

Net

Income

Increase

(Decrease)

Variable costs

$200,000

$ 48,000

$152,000

Fixed costs

120,000

20,000

100,000

equipment

58,000

PROBLEM 7-4B (Continued)

(d) MEMO

TO: Gene Simmons

FROM: Student

SUBJECT: Relevant Data for Decision to Replace Old Equipment

When deciding whether or not to replace any old equipment, the analysis

should only include cost data relevant to the replacement decision. The

$110,000 loss that would be experienced if we replace the old equipment

PROBLEM 7-5B

(a)

Division

III

Division

IV

Sales

Variable expenses

Cost of goods sold

$310,000

189,000

$170,000

140,400

(b)

(1)

Division III

Continue

Eliminate

Net Income

Increase

(Decrease)

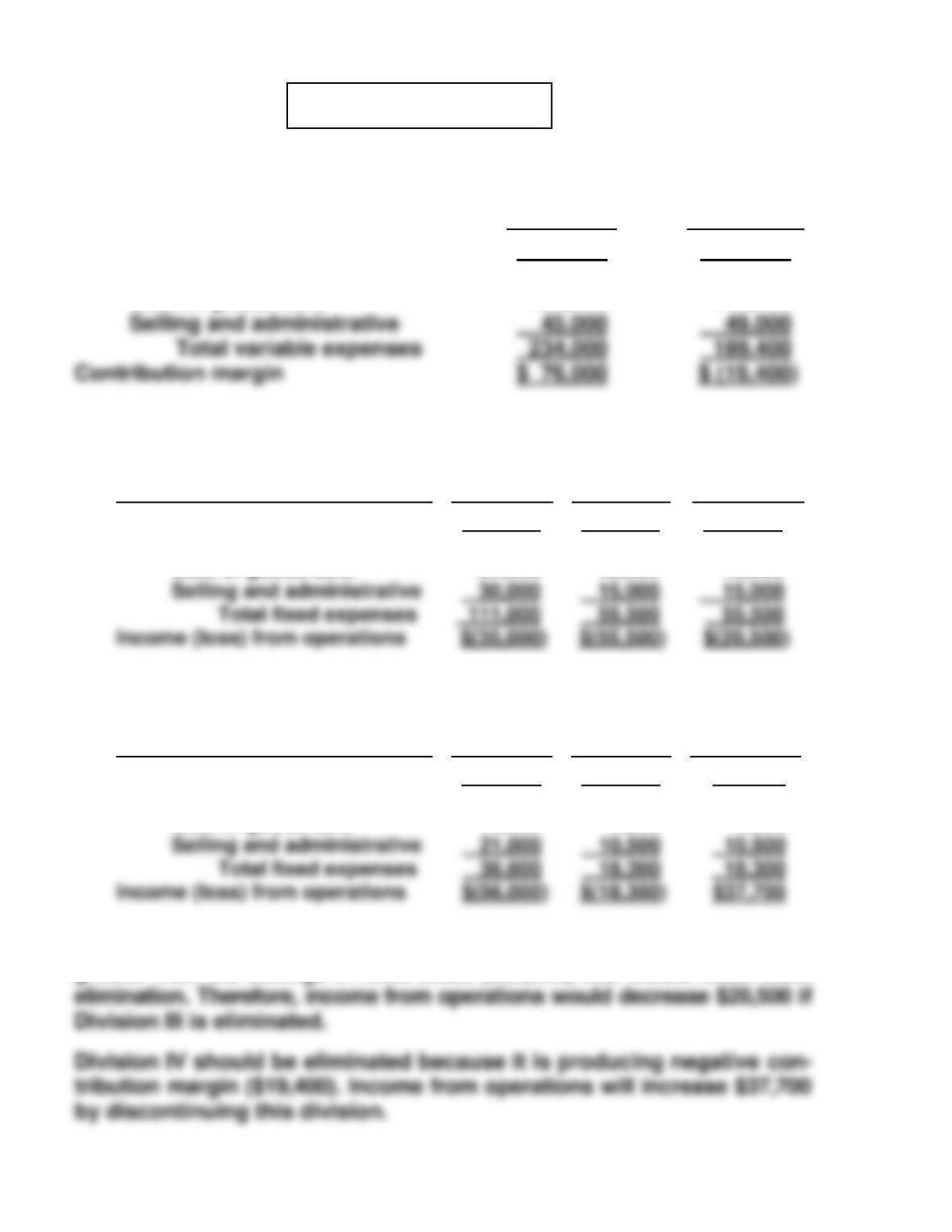

Contribution margin (above)

Fixed expenses

Cost of goods sold

$ 76,000

81,000

$ 0

(40,500

$(76,000)

40,500

(2)

Division IV

Continue

Eliminate

Net Income

Increase

(Decrease)

Contribution margin (above)

Fixed expenses

Cost of goods sold

$(19,400)

(15,600)

$ 0

7,800

$19,400

7,800

Division III should be continued as contribution margin ($76,000) is

greater than the savings in fixed costs ($55,500) that would result from

PROBLEM 7-5B (Continued)

(c) PANDA COMPANY

CVP Income Statement

For the Quarter Ended March 31, 2017

Divisions

I

II

III

Total

Sales

Variable expenses

Cost of goods sold

Selling and

administrative

Total variable

$510,000

210,000

24,000

$400,000

200,000

40,000

$310,000

189,000

45,000

$1,220,000

599,000

109,000

(1) Division’s fixed cost of goods sold plus 1/3 of Division IV’s unavoid-

able fixed cost of goods sold [$156,000 X (100% – 90%) X 50% =

(2) Division’s fixed selling and administrative expenses plus 1/3 of

Division IV’s unavoidable fixed selling and administrative expenses

(d) Income from operations with Division IV of $129,000 (given) plus incre-