Exercise 7-20 (LO 7-8)

Requirement 1

Step 1: Test for Impairment

The long-term asset is impaired since future cash flows ($7.1 million) are less than

book value ($8.6 million).

Requirement 2

Step 1: Test for Impairment

The long-term asset is not impaired since future cash flows ($10 million) exceed book

Exercise 7-21

Requirement 1

January 1

Debit

Credit

Equipment

19,500

Cash

19,500

(Purchase equipment for cash)

January 4

Debit

Credit

Accounts Payable

9,500

Cash

(Pay cash on account)

Inventory

82,900

Accounts Payable

82,900

(Purchase inventory on account)

January 15

Debit

Credit

Cash

22,000

Accounts Receivable

22,000

(Receive cash on account)

January 19

Debit

Credit

Salaries Expense

29,800

Cash

29,800

(Pay for salaries)

January 28

Debit

Credit

Utilities Expense

16,500

Cash

16,500

(Pay for utilities)

January 30

Debit

Credit

Accounts Receivable

Sales Revenue

(Sell inventory on account)

Cost of Goods Sold

Exercise 7-21 (continued)

Requirement 2

(a) January 31

Debit

Credit

Depreciation Expense

300

Accumulated Depreciation

300

(Record depreciation)

($300 = [$19,500−$1,500] / 60 months)

(b) January 31

Debit

Credit

Bad Debt Expense

5,900

Allowance for Uncollectible Accounts

5,900

(c) January 31

Debit

Credit

Interest Receivable

50

Interest Revenue

(Adjust interest revenue)

($50 = $12,000×5%×1/12)

(d) January 31

Debit

Credit

Salaries Expense

Salaries Payable

32,600

(Adjust salaries payable)

(e) January 31

Income Tax Expense

Income Tax Payable

9,000

(Adjust income taxes)

Exercise 7-21 (continued)

Requirement 3

TNT Fireworks

Adjusted Trial Balance

January 31, 2018

Accounts

Debit

Credit

Cash

$ 5,400

Accounts Receivable

223,000

Interest Receivable

50

Inventory

4,200

Notes Receivable

12,000

Land

155,000

Equipment

19,500

Allowance for Uncollectible Accounts

$ 8,100

Accumulated Depreciation

Accounts Payable

88,200

Salaries Payable

32,600

Income Tax Payable

9,000

Common Stock

220,000

Retained Earnings

50,000

Sales Revenue

220,000

Interest Revenue

50

Cost of Goods Sold

115,000

Salaries Expense

62,400

Utilities Expense

16,500

Bad Debt Expense

5,900

Depreciation Expense

Income Tax Expense

9,000

$628,250

$628,250

Exercise 7-21 (continued)

Requirement 3 (continued)

Accounts

Ending

Balance

Beginning balance in bold, entries during

January in blue, and adjusting entries in red.

Cash

5,400

=

58,700−19,500−9,500+22,000−29,800−16,500

Accounts Receivable

223,000

=

25,000−22,000+220,000

Interest Receivable

50

=

50

Inventory

4,200

=

36,300+82,900−115,000

Notes Receivable

=

Land

155,000

=

Equipment

=

Allowance for Uncollectible Accounts

8,100

=

2,200+5,900

Accumulated Depreciation

=

Accounts Payable

=

14,800−9,500+82,900

Salaries Payable

=

32,600

Income Tax Payable

9,000

=

Common Stock

220,000

=

Retained Earnings

=

Sales Revenue

220,000

=

Interest Revenue

50

=

50

Cost of Goods Sold

115,000

=

Salaries Expense

=

Utilities Expense

=

Bad Debt Expense

5,900

=

5,900

Depreciation Expense

=

Income Tax Expense

9,000

=

Exercise 7-21 (continued)

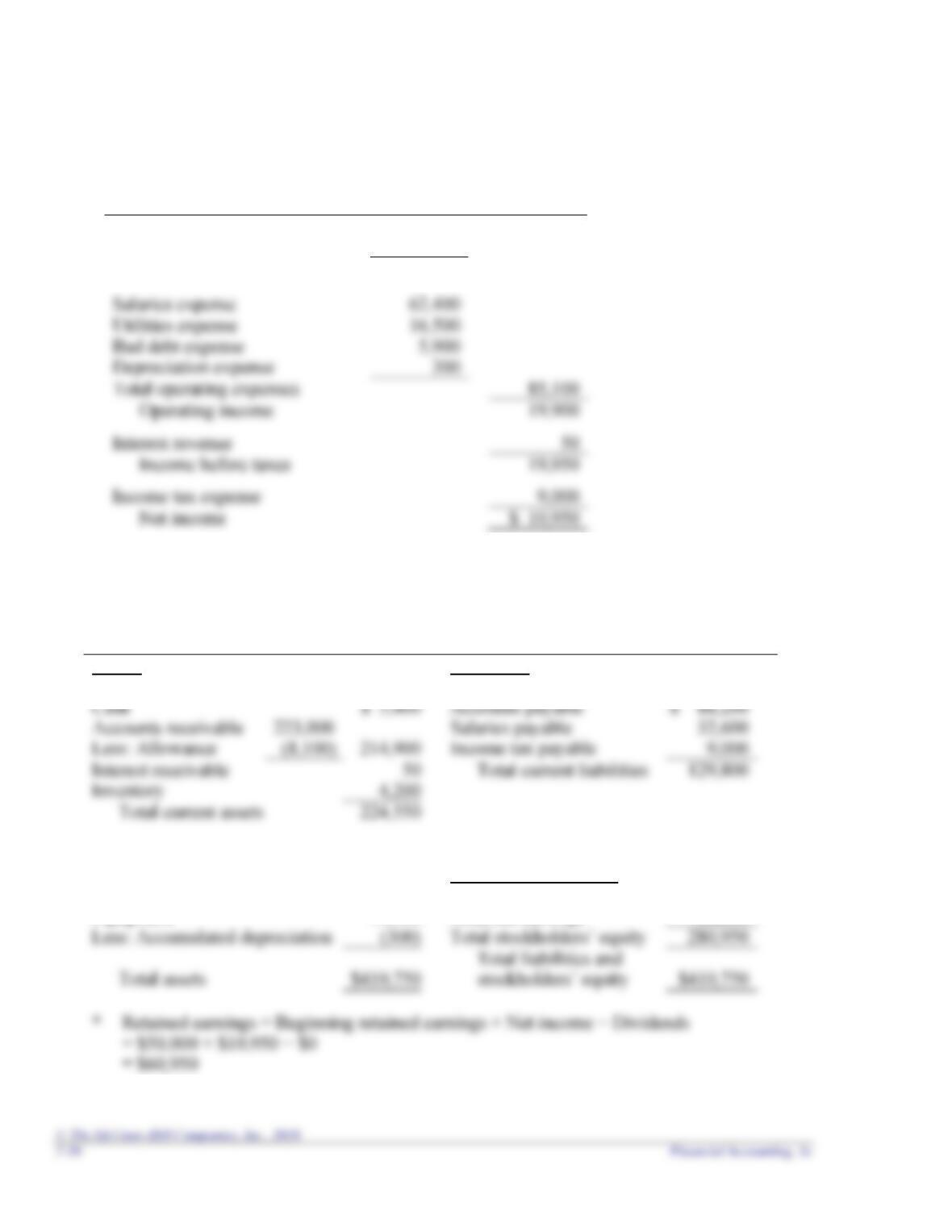

Requirement 4

TNT Fireworks

Multiple-Step Income Statement

For the month ended January 31, 2018

Sales revenue

$220,000

Cost of goods sold

115,000

Gross profit

$105,000

Utilities expense

Bad debt expense

Depreciation expense

Total operating expenses

Interest revenue

Income tax expense

Net income

$ 10,950

Requirement 5

TNT Fireworks

Balance Sheet

January 31, 2018

Assets

Liabilities

Current assets:

Current liabilities:

Cash

$ 5,400

Accounts payable

Accounts receivable

223,000

Salaries payable

Less: Allowance

214,900

Income tax payable

Interest receivable

Total current liabilities

129,800

Inventory

Total current assets

224,550

Long-term assets:

Notes receivable

12,000

Stockholders’ Equity

Land

155,000

Common stock

220,000

Equipment

19,500

Retained earnings

60,950

*

Less: Accumulated depreciation

280,950

Total assets

$410,750

$410,750

Exercise 7-21 (concluded)

Requirement 6

January 31, 2018

Debit

Credit

Sales Revenue

220,000

Interest Revenue

50

Retained Earnings

220,050

(Close revenue accounts)

Retained Earnings

209,100

115,000

(Close expense accounts)

Requirement 7

(a) The return on assets ratio is:

(b) The profit margin is:

(c) The asset turnover ratio is:

PROBLEMS: SET A

Problem 7-1A (LO 7-1)

Land

Building

Purchase price of land

$70,000

Demolition of old building

9,000

Sale of salvaged materials

Architect fees (for new building)

Legal fees (for title investigation of land)

3,000

Building construction costs

Interest costs related to the construction

Totals

$643,000

Problem 7-2A (LO 7-1)

Requirement 1

The ovens should be recorded in the equipment account as detailed in the

following schedule:

Purchase price

$700,000

Freight costs

35,000

Electrical connections

Labor costs

Bread dough used in testing ovens

Safety guards

Total equipment

$780,200

Requirement 2

The repair costs of $4,000 for the oven damaged during installation should not be

Problem 7-3A (LO 7-2)

1. The amount Fresh Cut paid for goodwill is $1 million calculated

as follows:

(in millions)

Purchase price

$12.0

Less:

(2.7)

Goodwill

$ 1.5

2.

(in millions)

Debit

Credit

Accounts Receivable (at fair value)

1.6

Equipment (at fair value)

9.9

Notes Payable (at fair value)

Cash (at purchase price)

7-30 Financial Accounting, 1e

Problem 7-4A (LO 7-3)

1. Capitalize

2. Expense

3. Capitalize

4. Capitalize

5. Expense

6. Expense

increase earnings reported in the current year.

Problem 7-5A (LO 7-4)

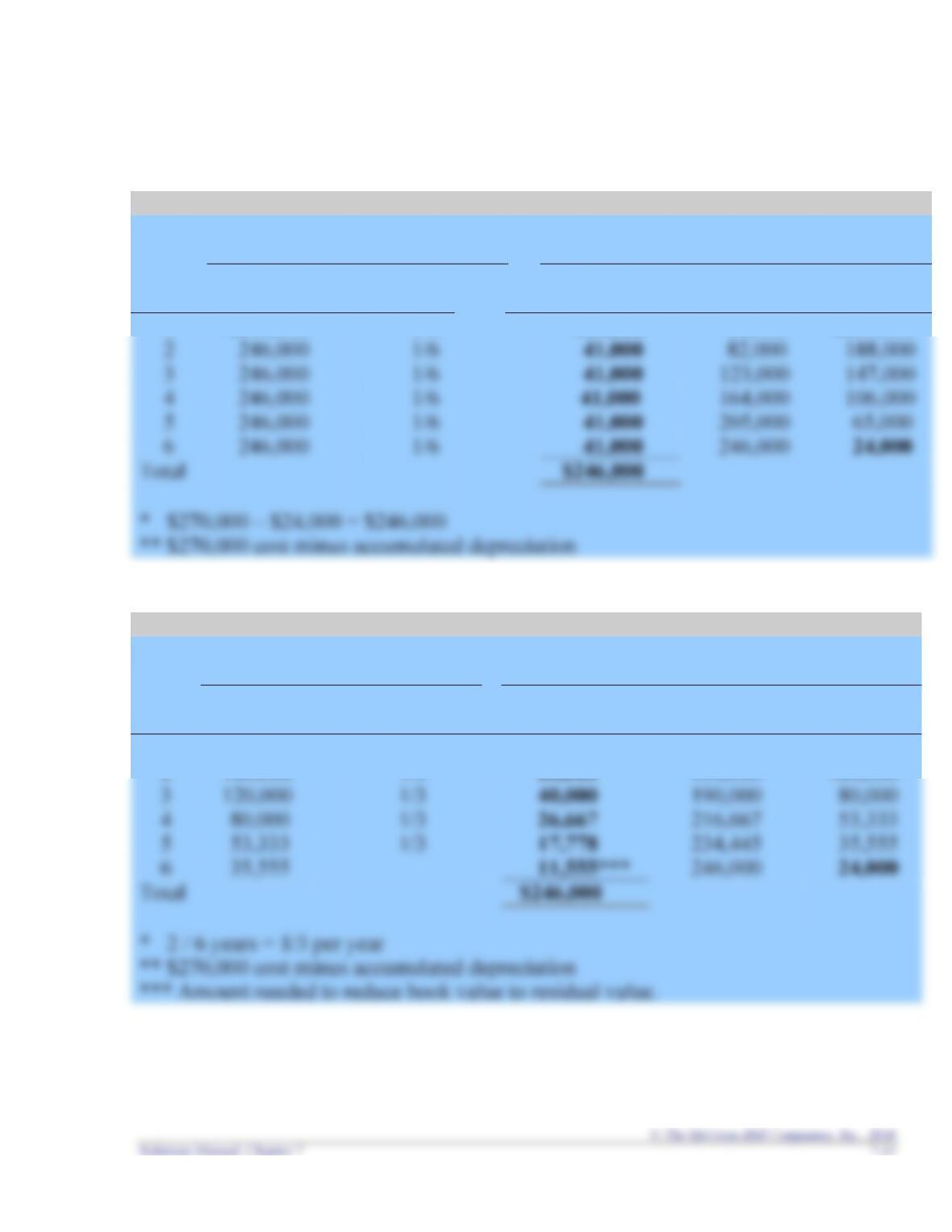

Requirement 1 Straight-Line

University Car Wash

Calculation

End of Year Amounts

Year

Depreciable

Cost*

X

Depreciation

Rate

=

Depreciation

Expense

Accumulated

Depreciation

Book

Value**

1

$246,000

1/6

$41,000

41,000

$239,000

2

1/6

82,000

3

1/6

5

1/6

6

1/6

Total

Requirement 2 Double-declining-balance

University Car Wash

Calculation

End of Year Amounts

Year

Beginning

Book Value

X

Depreciation

Rate*

=

Depreciation

Expense

Accumulated

Depreciation

Book

Value**

1

$270,000

1/3

$90,000

90,000

$180,000

3

1/3

190,000

4

1/3

216,667

5

1/3

234,445

6

Total

*** Amount needed to reduce book value to residual value.

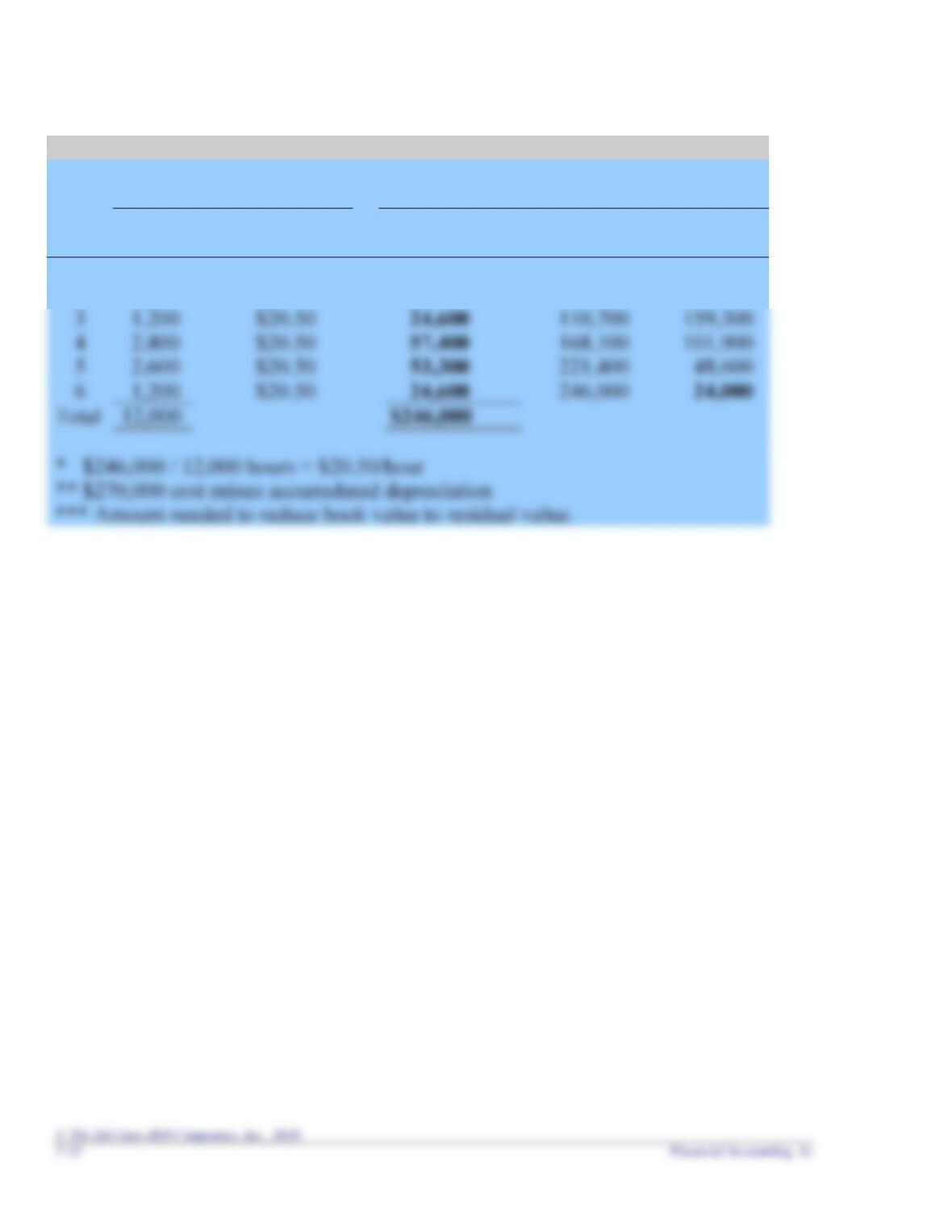

Requirement 3 Activity-based

University Car Wash

Calculation

End of Year Amounts

Year

Hours

Used

X

Depreciation

Rate*

=

Depreciation

Expense

Accumulated

Depreciation

Book

Value**

1

3,100

$20.50

$63,550

63,550

$206,450

2

1,100

$20.50

22,550

86,100

183,900

3

1,200

$20.50

24,600

159,300

4

2,800

$20.50

57,400

101,900

6

1,200

$20.50

24,600

Problem 7-6A (LO 7-5)

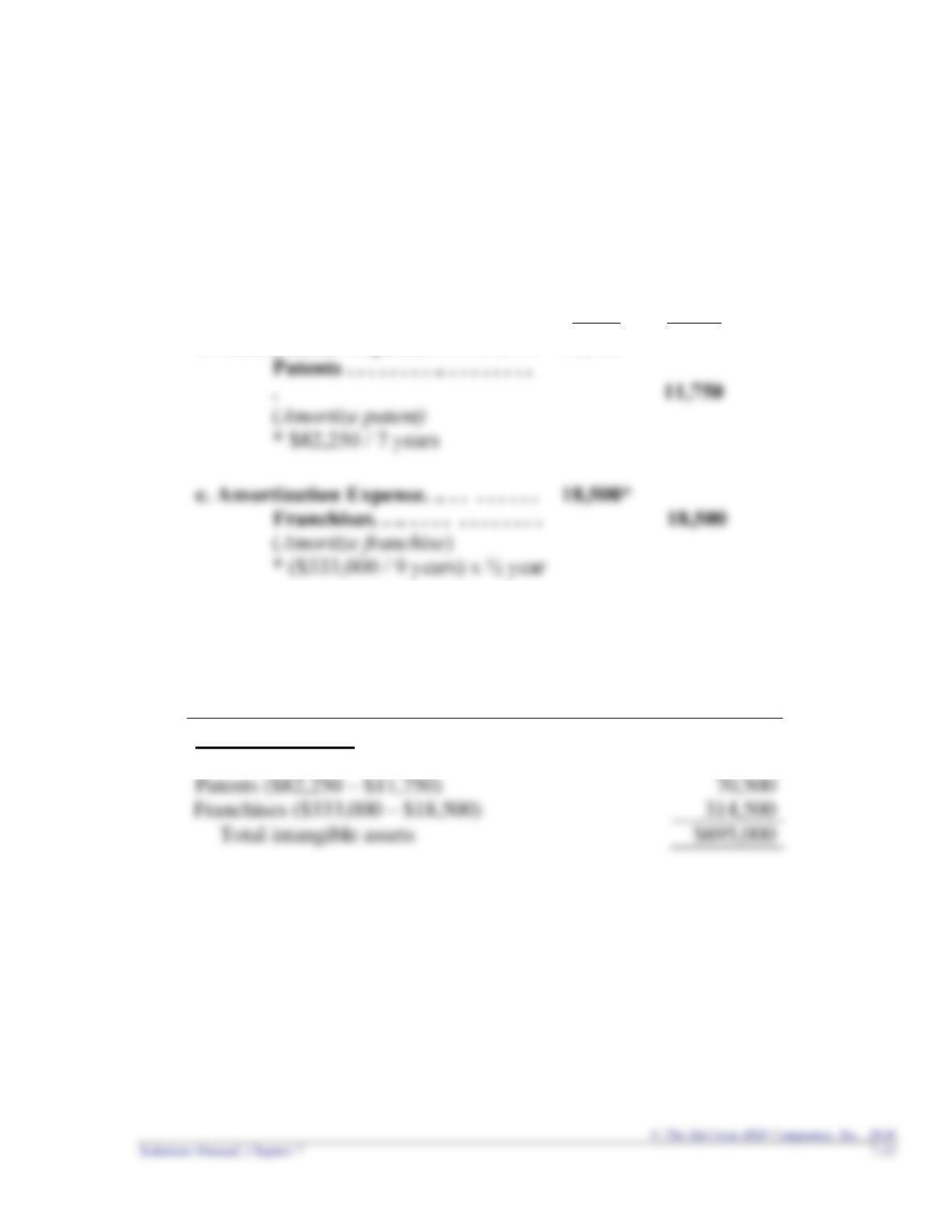

Requirement 1

a. Goodwill is not amortized.

Debit

Credit

b. Amortization Expense. . . . . .. .. . . .

11,750*

11,750

18,500*

Requirement 2

University Testing Services

Balance Sheet

December 31, 2018

(Intangible Assets section)

Intangible Assets

Goodwill

$310,000

Patents ($82,250 – $11,750)

Problem 7-7A (LO 7-4, 7-5)

Requirement 1

Debit

Credit

Depreciation Expense

58,880*

Accumulated Depreciation

58,880

Depreciation Expense

25,000*

Accumulated Depreciation

25,000

Requirement 2

Debit

Credit

Amortization Expense

50,000*

Patent

50,000

Requirement 3

Solich Sandwich Shop

December 31, 2018

Cost

Accumulated

Depreciation

Book

Value

Land

$ 95,000

–

$ 95,000

Building

Equipment

Patent

Problem 7-8A (LO 7-6)

Requirement 1

Requirement 2

Cost of the oven

$910,000

Less: Accumulated depreciation

(170,000)

$740,000

Requirement 3

Sale amount

$700,000

Less:

Cost of the oven

$910,000

Less: Accumulated depreciation

(170,000)

Loss

Requirement 4

Debit

Credit

Cash

700,000

Accumulated Depreciation

Loss

Equipment

Problem 7-9A (LO 7-7)

Requirement 1

Sub Station

Net

Income

÷

Average

Total Assets

=

Return

on Assets

$25,922

÷

($75,183 + $116,371)/2

=

27.1%

÷

Average

Total Assets

=

÷

($75,183 + $116,371)/2

=

Requirement 2

Planet Sub

Net

Income

÷

Average

Total Assets

=

Return

on Assets

$3,492

÷

($38,599 + $44,533)/2

=

8.4%

÷

Average

Total Assets

=

÷

($38,599 + $44,533)/2

=

1.5 times

Requirement 3

Sub Station has the higher profit margin, while Planet Sub has the higher asset

Problem 7-10A (LO 7-7)

Requirement 1

Sandwiches Only

Net

Income

÷

Average

Total Assets

=

Return

on Assets

$170,000

÷

$500,000

=

34.0%

÷

Average

Total Assets

=

÷

$500,000

=

Requirement 2

Sandwiches and Smoothies

Net

Income

÷

Average

Total Assets

=

Return

on Assets

$260,000

÷

$900,000

=

28.9%

÷

Average

Total Assets

=

÷

$900,000

=

Requirement 3

Do not go forward with the expansion plans. The return on assets, profit margin, and

7-38 Financial Accounting, 1e

PROBLEMS: SET B

Problem 7-1B (LO 7-1)

Land

Building

Purchase price of land

$90,000

Land clearing costs

5,000

Sale of firewood to a worker

Architect fees (for new building)

Legal fees (for title investigation of land)

3,500

Building construction costs

Problem 7-2B (LO 7-1)

Requirement 1

Purchase price

$341,000

Shipping costs

16,000

Labor costs

17,000

Electrical work

Pizza dough for testing ovens

New timers

Total equipment

$379,900

Requirement 2