7–21 Ch. 7—Problems

Problem 7-2, Concluded

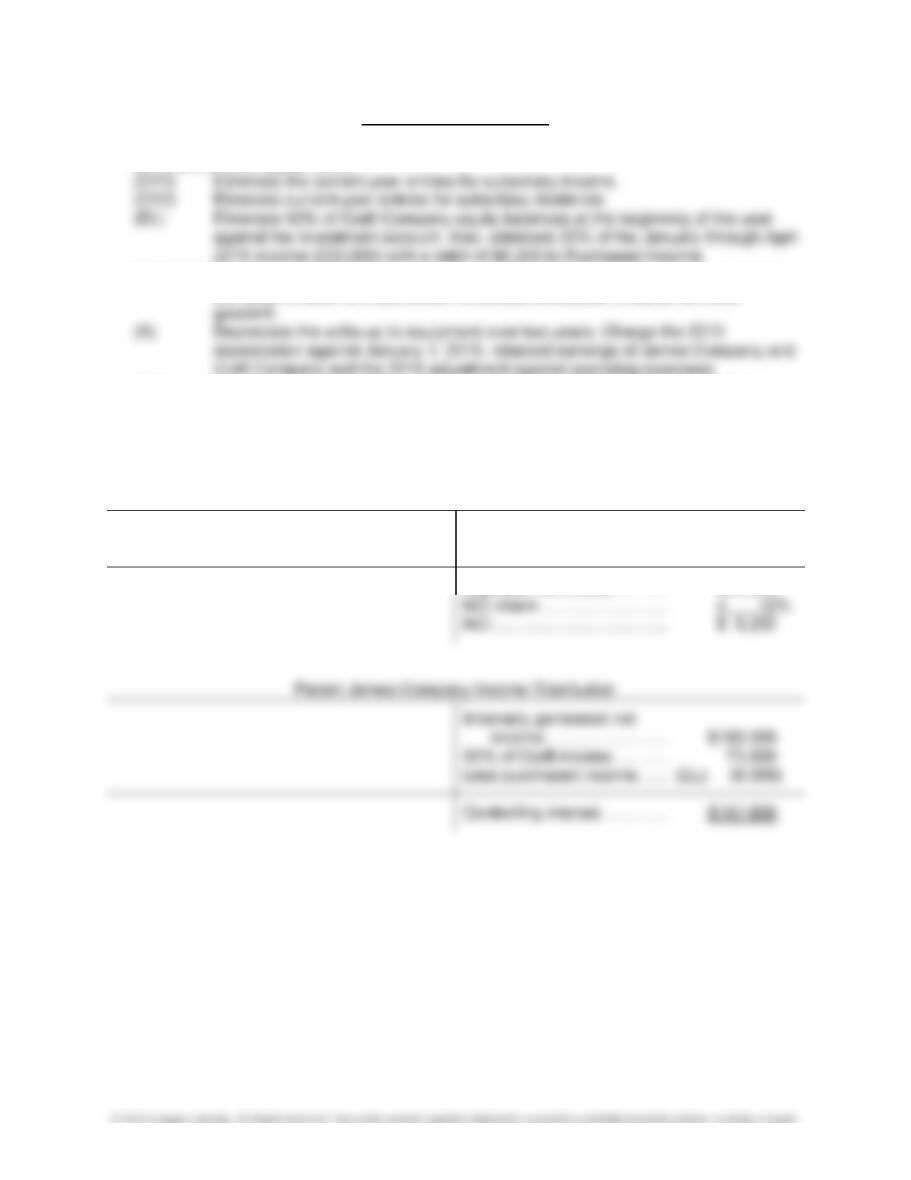

Eliminations and Adjustments:

(D1)/(NCI) Distribute the $35,000 excess cost and $15,000 NCI adjustment as required by

the determination and distribution of excess schedules to equipment and

(D2) Distribute excess on 20% investment. Eliminate NCI of $2,667 and debit James

Company’s Retained Earnings for $15,333.

(IS) Eliminate the intercompany sale and purchase.

(EI) Eliminate the $3,000 of gross profit in the ending inventory.

Subsidiary Craft Company Income Distribution

Ending inventory profit …………. (EI) $3,000 Internally generated net

Equipment depreciation ……….. (A) 5,000 income ……………………… $90,000

Adjusted net income ………… $82,000

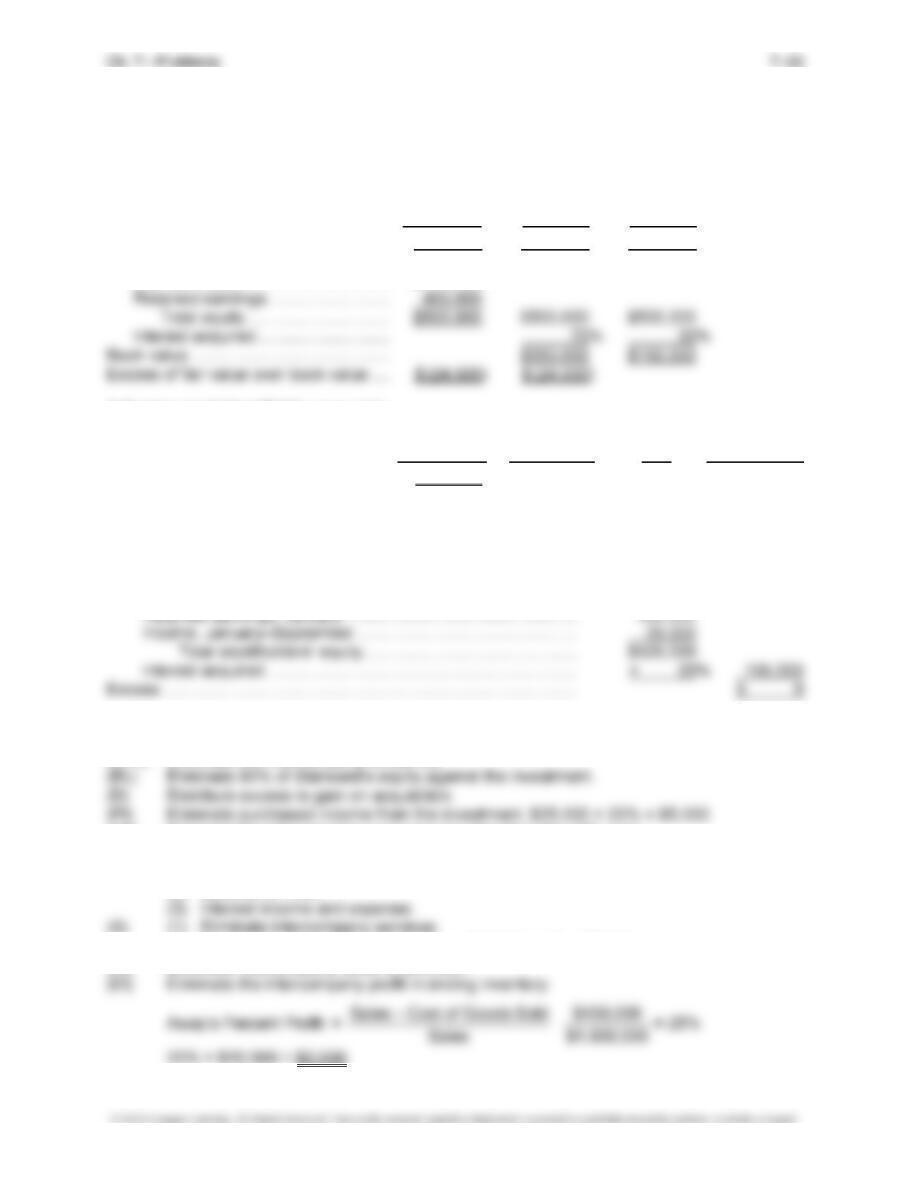

PROBLEM 7-3

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (70%) (30%)

Price paid for investment …………………. $475,500 $325,500 $150,000*

Less book value of interest acquired:

Common stock ………………………….. $100,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Gain on acquisition …………………………. $ (24,500) credit D

*NCI value cannot be less than fair (equal to book) value of interest in net assets.

Analysis of September 30, 2017, purchase:

Price paid …………………………………………………………………………… $105,000

Less interest acquired:

Common stock …………………………………………………………….. $100,000

Eliminations and Adjustments:

(CY1) Eliminate the subsidiary income.

(CY2) Eliminate the intercompany dividends.

(LN) Eliminate the intercompany accounts resulting from the 12% note:

(1) Payment of installment and interest on December 31 was made by Stallward but

not received by Away.

(2) Balance on note.

(2) Eliminate profit in deferred charges, $16,500 × 1/3 = $5,500.

(IS) Eliminate intercompany sales of $60,000.

7–23 Ch. 7—Problems

Problem 7-3, Continued

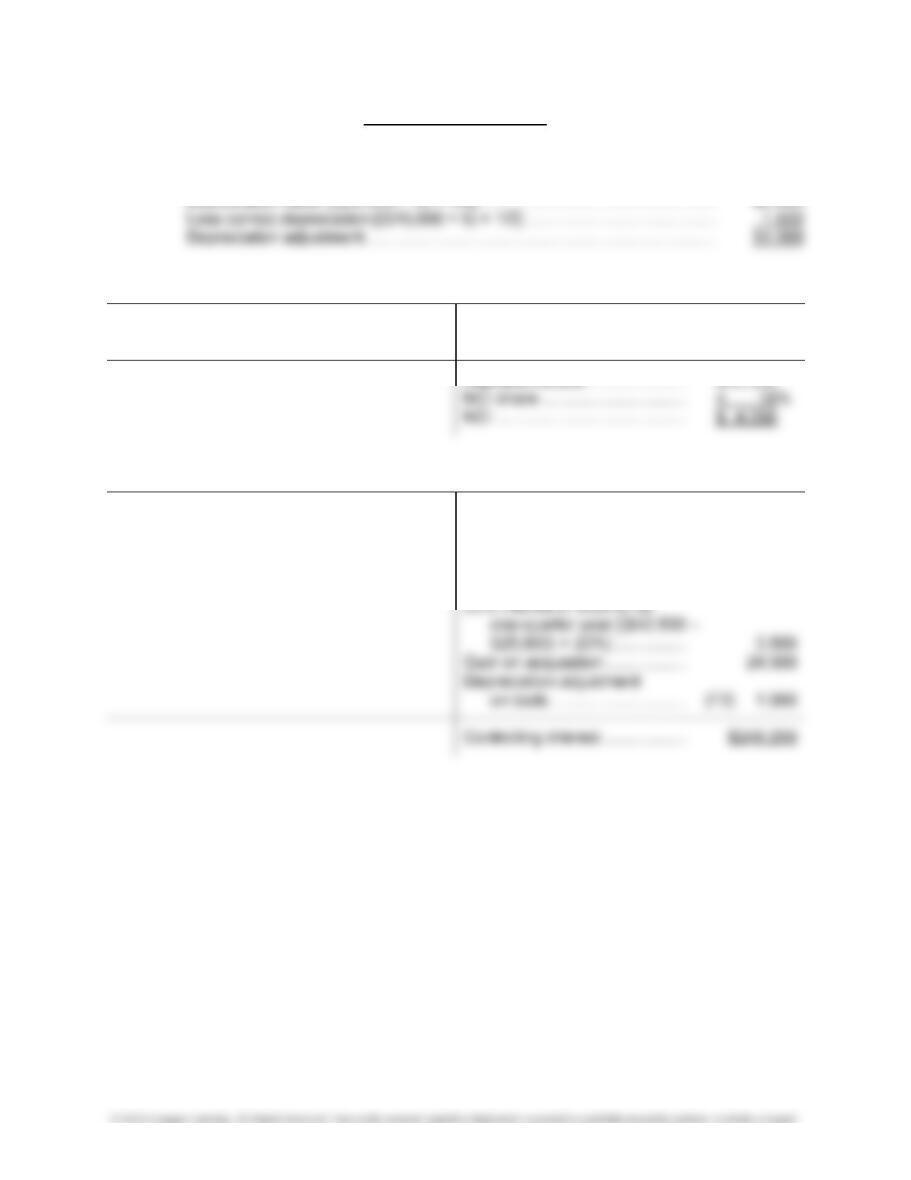

(F1) Eliminate the gain on the sale of tools.

(F2) Adjust the depreciation on tools:

Subsidiary Stallward, Inc., Income Distribution

Unrealized profit on Internally generated net

engineering services ………. (S2) $5,500 income …………………………. $48,000

Parent Away Company Income Distribution

Unrealized gain on sale Internally generated net

of tools ………………………….. (F1) $10,000 income …………………………. $202,000

Unrealized profit in ending 70% interest in income of

inventory ……………………….. (EI) 2,500 Stallward for full year

(70% × $42,500) ……………. 29,750

Problem 7-3, Continued

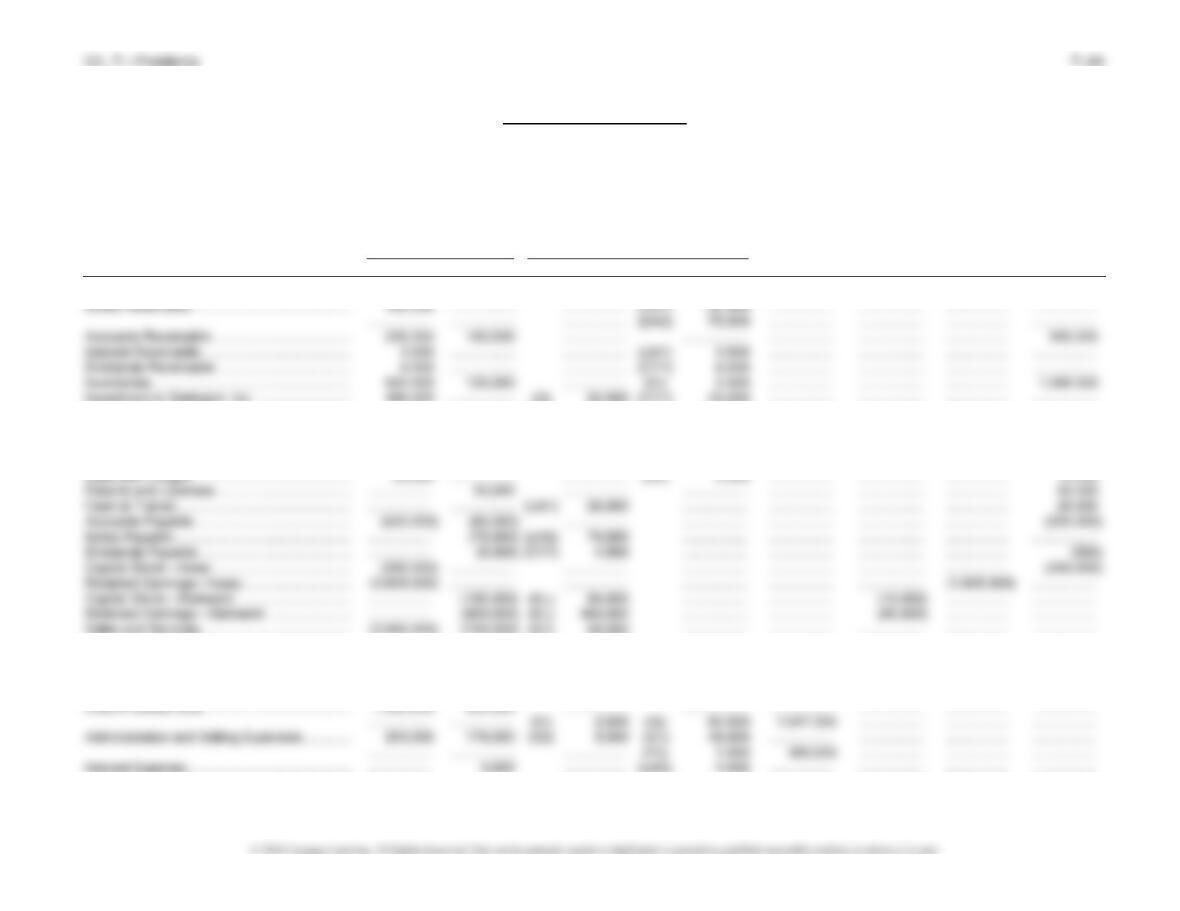

Away Company and Subsidiary Stallward, Inc.

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2017

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Away Stallward Dr. Cr. Statement NCI Earnings Sheet

Cash …………………………………………………….. 99,500 78,000 …………….. …………….. …………….. …………….. …………….. 177,500

Investment in Stallward, Inc. ……………………. 469,200 …………….. (D) 24,500 (CY1) 43,200 …………..… …………….. …………….. ……………..

…………….. …………….. (CY2) 4,500 (EL) 450,000 …………….. …………….. …………….. ……………..

…………….. …………….. …………….. (PI) 5,000 …………….. …………….. …………..… ……………..

Property, Plant, and Equipment ………………… 1,250,000 500,000 …………….. (F1) 10,000 …………….. …………….. …………….. 1,740,000

Accumulated Depreciation ……………………….. (500,000) (150,000) (F2) 1,000 …………….. …………….. …………….. …………….. (649,000)

…………….. …………….. (IS) 60,000 …………….. …………….. …………….. ………….…. ……………..

…………….. …………….. (F1) 10,000 …………….. (2,440,000) …………….. …………….. ……………..

Subsidiary Income ………………………………….. (43,200) …………….. (CY1) 43,200 …………….. .……………. …………….. …………….. ……………..

Interest Income ………………………………………. (3,000) …………….. (LN3) 3,000 …………….. …………….. …………….. …………….. ……………..

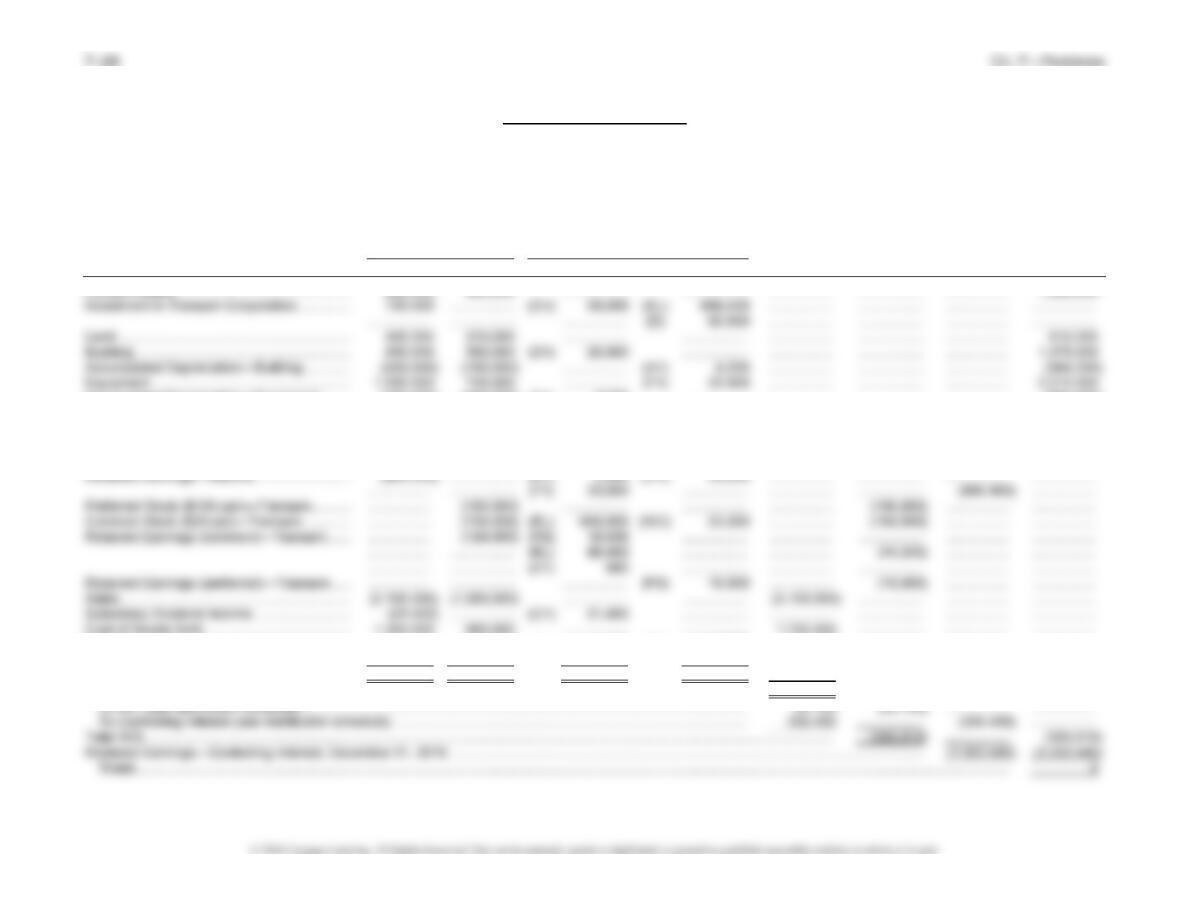

Problem 7-3, Concluded

Away Company and Subsidiary Stallward, Inc.

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2017

(Concluded)

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Away Stallward Dr. Cr. Statement NCI Earnings Sheet

Gain on Acquisition …………………………………. …………….. …………….. …………….. (D) 24,500 (24,500) …………….. …………….. ……………..

Dividends Declared …………………………………. …………….. 5,000 …………….. (CY2) 4,500 …..………… 500 …………….. ……………..

PROBLEM 7-4

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (90%) (10%)

Fair value of subsidiary …………………… $560,000 $504,000 $ 56,000

Less book value of interest acquired:

Common stock ($5 par) ……………… $100,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Buildings ………………………………………. $ 60,000 debit D 20 $3,000

Entries of July 1, 2017:

Investment in Dower [10% × ($30,000 income – $10,000 dividends)

– (10% × $3,000 amortization × 1/2 year)] …………………………… 1,850

Investment Income ………………………………………………………. 1,850

Cash ……………………………………………………………………………………. 100,000

Investment in Dower [(1/9 × $504,000) + $1,850 + $8,800] ……. 66,650

Paid-In Capital in Excess of Par—Carlos …………………………….. 33,350

To record sale of 10% interest.

Entries on December 31, 2017:

7–27 Ch. 7—Problems

Problem 7-4, Concluded

Investment in Dower (80% × $100,000 change) –

(80% × 4 years × $3,000 amortization) ……………………………….. 70,400

Retained Earnings ……………………………………………………….. 70,400

To convert the portion of the investment sold to equity by

PROBLEM 7-5

Adjustments for investment in preferred stock:

Investment in Channel Preferred Stock ……………………………………. 1,800

Subsidiary Income—Preferred Stock ………………………………….. 1,800

To record dividend preference for 2015.

Adjustments for investment in common stock:

From cost to fair value on January 1, 2013

Fair value, 1,000 shares ($140,000 purchase cost/5,000 shares) $28,000

Adjustment for 2013–2014:

Retained Earnings ………………………………………………………………… 3,600

Investment in Channel Common Stock ……………………………….. 3,600

Net correction for equity adjustments on common:

2013–2014:

Failure to deduct preferred dividend claims from

net income to arrive at income available to

Problem 7-5, Concluded

Adjustment for sale of 10% interest:

Adjusted cost of shares, January 1, 2013, 1,000 shares × $28 …. $28,000

Share of income (10% × $75,000) ………………………………………… 7,500

Common dividends (10% × $5,000) ………………………………………. (500)

PROBLEM 7-6

Determination and Distribution of Excess Schedule, December 31, 2013

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary …………………… $900,000 $720,000 $180,000

Less book value of interest acquired:

Common stock ($20 par) ……………. $750,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Building ………………………………………… $ 28,000 debit D1 20 $1,400

Goodwill ……………………………………….. 88,000 debit D2

Total ……………………………………….. $116,000

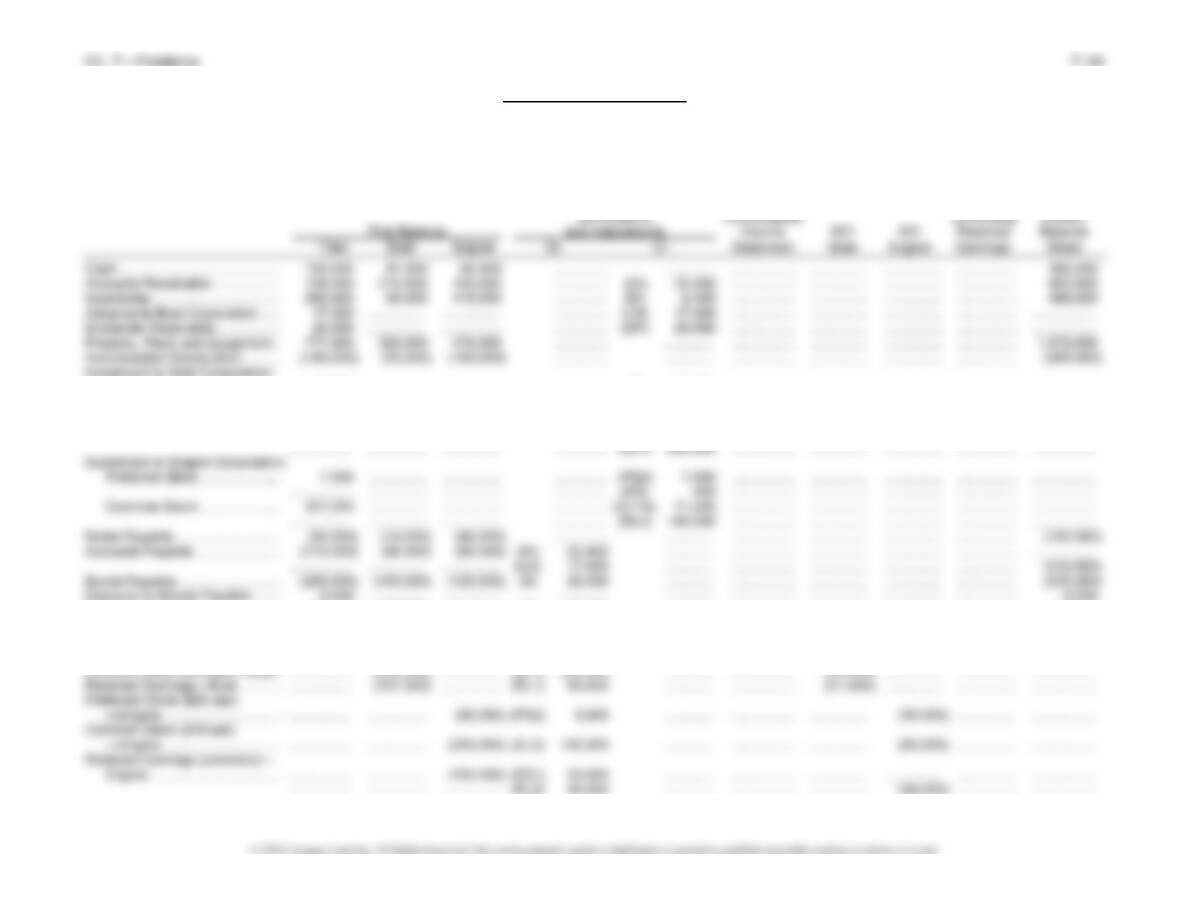

Problem 7-6, Continued

Marsha Corporation and Subsidiary Transam Corporation

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Marsha Transam Dr. Cr. Statement NCI Earnings Sheet

Current Assets ……………………………………….. 806,400 463,250 …………….. …………….. …………….. …………….. …………….. 1,269,650

Accumulated Depreciation—Equipment …….. (400,000) (200,000) (F1) 5,000 …………….. …………….. …….………. …………….. (590,000)

…………….. …………….. (F2) 5,000 …………….. …………….. …………….. ………….…. ……………..

Goodwill ………………………………………………… …………….. …………….. (D2) 88,000 ….…………. …………….. …………….. …………….. 88,000

Liabilities ……………………………………………….. (800,000) (550,000) …………….. …………….. …………….. …………….. …………….. (1,350,000)

Common Stock ($20 par)—Marsha …………… (2,000,000) …………….. …………….. …………….. …..………… …………….. …………….. (2,000,000)

Other Expenses ……………………………………… 650,000 320,000 (A1) 1,400 (F2) 5,000 966,400 ………….…. …………….. ……………..

Dividends Declared …………………………………. 200,000 50,750 …………….. (CY) 21,400 …………….. 29,350 200,000 ……………..

0

0 933,200 933,200 …………….. …………….. …………….. ……………..

Consolidated Net Income ……………………………………………………………………………………………………………….……… (378,600) …………….. …………….. ……………..

Problem 7-6, Continued

Eliminations and Adjustments:

(CV) Convert the investment to the equity method as of January 1:

Retained earnings applicable to common stock

on January 1, 2016 ($124,000 – $16,000 arrearage

for 2014 and 2015) ……………………………………………………… $108,000

from the retained earnings of Transam Corporation, 2 years × $8,000.

(EL) Eliminate the parent’s 80% share of subsidiary common stock equity.

(D)/(NCI) Distribute the excess and NCI adjustment according to the determination and

distribution of excess schedule.

(D1) Building.

(A1) Adjust the depreciation on the building—two past years and one current year.

(F2) Reduce current depreciation by $5,000 for 1/5 of current gain on sale.

Problem 7-6, Concluded

Subsidiary Transam Corporation Income Distribution

Building depreciation ……………. (A1) $1,400 Internally generated net

income …………………………. $80,000

Less preferred claim to

NCI (2016 dividends) ……… 8,000

Adjusted income …………………. $70,600

Parent Marsha Corporation Income Distribution

Internally generated

income …………………………. $295,000

Share of Transam adjusted

PROBLEM 7-7

(1)

Adjustment of investment account:

July 1, 2018

Implied fair value of 5,000 shares [($226,200/15,000 shares) × 5,000] ……………. $ 75,400

(2) Supporting schedules for worksheet:

Determination and Distribution of Excess Schedule, July 31, 2018

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary …………………… $377,000 $301,600* $ 75,400

Less book value of interest acquired:

Common stock ($10 par) ……………. $250,000

Retained earnings …………………….. 107,000

January 1–June 20 income ………… 20,000

January 2, 2018, Engine Corporation preferred, 250 shares:

Price paid ……………………………………………………………………….. $7,000

Less interest acquired:

Preferred stock …………………………………………………………. $ 50,000

Retained earnings, preferred stock,

Problem 7-7, Continued

January 2, 2018, Engine Corporation common, 14,000 shares (14,000 shares/20,000 shares =

70%):

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (70%) (30%)

Fair value of subsidiary …………………… $280,000 $196,000 $ 84,000

Less book value of interest acquired:

Common stock ($10 par) ……………. $200,000

Problem 7-7, Continued

Titan Corporation and Subsidiaries Boat Corporation and Engine Corporation

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2018

6% Bonds ………………………… 23,800 ……………. …………… ………….. (B) 23,800 ……….……. …………… …………… ……………. ……………..

Common Stock …………………. 293,600 ……………. …………… ………….. …………. ……..……… …………… …………… ……………. ……………..

…………….. ……………. …………… (CY2) 24,000 (CY1a) 16,000 …………….. …………… .………….. ……………. ……………..

…………….. ……………. …………… ………….. (PI) 16,000 …………….. …………… …………… ……………. ……………..

Dividends Payable …………………. (22,000) (30,000) …………… (DP) 24,000 …………. …………….. …………… …………… ……………. (28,000)

Preferred Stock ($20 par)—Titan (400,000) …………… …………… ………….. …………. ………..…… …………… …………… ……………. (400,000)

Common Stock ($10 par)—Titan (600,000) …………… …………… ………….. …………. …………..… …………… …………… ……………. (600,000)

Retained Earnings—Titan ……….. (154,600) …………… …………… ………….. …………. …….………. …………… …………… (154,600) ……………..