Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 7

Chapter 7

Accounting Information Systems

QUESTIONS

1. The five components of an accounting system are: source documents, input

devices, information processors, information storage, and output devices.

2. Source documents contain data about business transactions or events that are put

3. The five fundamental principles of accounting information systems are: (a) control

4. An input device is used to transfer data from source documents to the information

5. Data stored “off-line” are not immediately available to the information processor(s),

6. Output devices provide the means by which information is taken from the

accounting system and made available for use.

9. The double posting does not cause the trial balance to be out of balance because

10. When copies of the sales invoices are used as a sales journal, each invoice total is

posted to the proper customer account in the subsidiary Accounts Receivable

48.5%

11. Both kinds of credits must not be placed in the same column because the sum of the

credits to the customer accounts must be posted to the Accounts Receivable

12. Immediate recording and posting of credit sales and cash receipts from customers

13. In its note 11 (Segment Information and Geographic Data), Apple discusses its

14. In its note 16 (Information about Segments and Geographic Areas), Google

discusses its reportable segments. The Company’s three reportable geographical

15.

Segment

Operating

Income

Net Sales

Operating Income /

Net Sales

Americas …………………………

$31,186

$93,864

33.2%

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 7

443

QUICK STUDIES

Quick Study 7-1 (15 minutes)

1.

B

5.

C

8.

A

Quick Study 7-2 (10 minutes)

Quick Study 7-3 (10 minutes)

a. Sales Journal

Quick Study 7-4 (15 minutes)

General Journal

Nov. 2

[In Purchases Journal]

Nov. 12

Automobiles …………………………………………………….

17,000

Nov. 16

Nov. 19

3.

E

7.

B

10.

D

444

Quick Study 7-5 (15 minutes)

a) Accounts Receivable Ledger

ACCOUNTS RECEIVABLE LEDGER

Stern Company

Date

Explanation

PR

Debit

Credit

Balance

Jan. 10

S1

4,000

4,000

2,000

Date

Explanation

PR

Debit

Credit

Balance

Jan. 19

S1

1,600

1,600

Date

Explanation

PR

Debit

Credit

Balance

Jan. 23

S1

2,500

2,500

1,200

8,100

8,100

3,200

Quick Study 7-6 (20 minutes)

PURCHASES JOURNAL

Date

Account

Date

of

Invoice

Terms

PR

Accounts

Payable

Cr.

Inventory

Dr.

Office

Supplies

Dr.

Other

Accounts

Dr.

May 1

Krause, Inc. ……………………

5/01

n/30

10,100

10,100

445

Quick Study 7-7 (10 minutes)

May 1

Purchases Journal

8

Sales Journal

Purchases Journal

Purchases Journal

Cash Receipts Journal

Cash Disbursements Journal

Cash Disbursements Journal

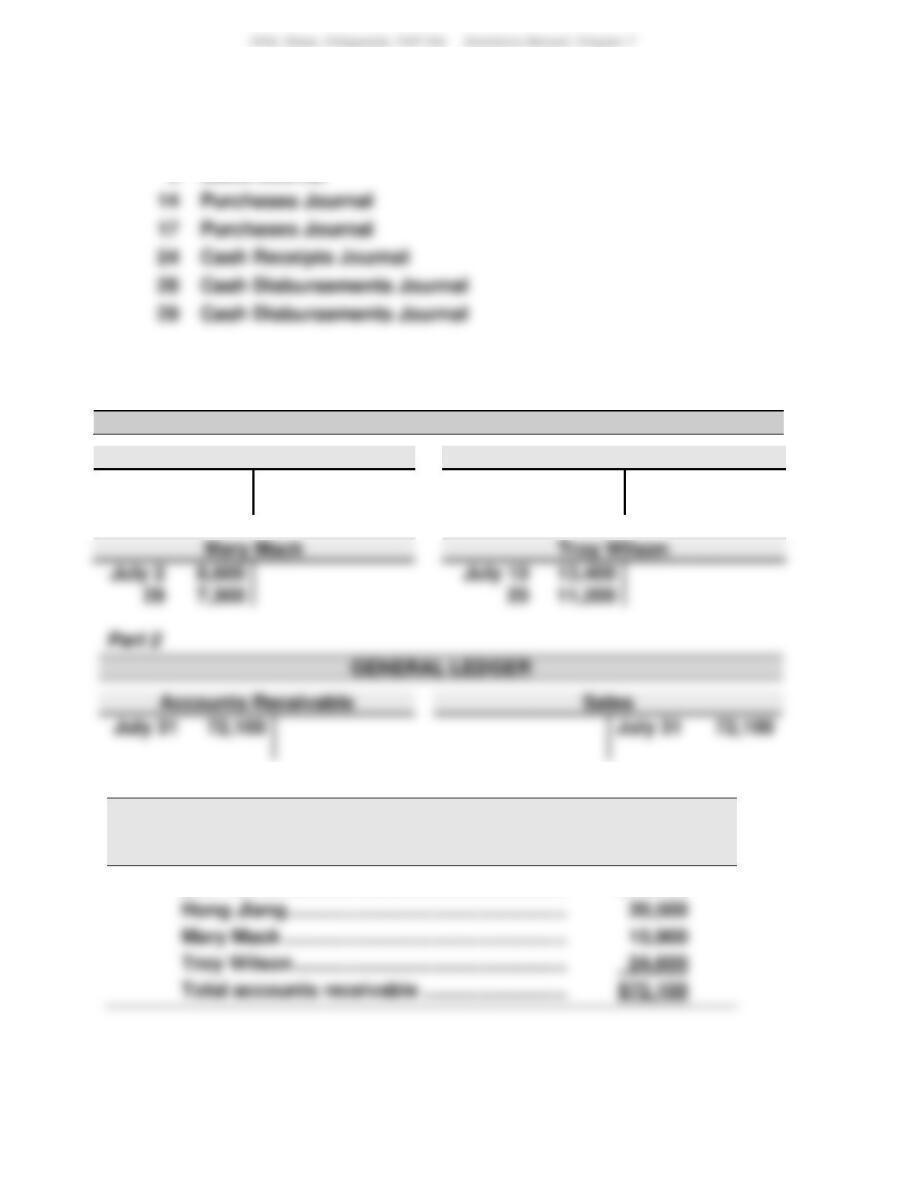

Quick Study 7-8 (30 minutes)

Part 1

ACCOUNTS RECEIVABLE LEDGER

Eric Horner

Hong Jiang

July 8

11,100

July 14

20,500

July 2

July 10

13,400

11,200

72,100

Part 3

WARTON COMPANY

Schedule of Accounts Receivable

July 31

Eric Horner …………………………………………………

$11,100

Mary Mack …………………………..……………………..

Troy Wilson ………………………………………………..

Total accounts receivable …………………………..

$72,100

446

Quick Study 7-9 (15 minutes)

Product

Product Sales

Percent of Total Sales*

iPhone ……………………………………..

$ 155,041

66.3%

Quick Study 7-10 (15 minutes)

General Journal

1.

[In Purchases Journal]

2.

3.

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 7

447

EXERCISES

Exercise 7-1 (15 minutes)

SALES JOURNAL

Date

Account Debited

Invoice

Number

PR

Accounts

Receivable Dr.

Sales Cr.

Cost of Goods

Sold Dr.

Inventory Cr.

May 7

J. Dryer …………………………..

5704

1,250

800

Exercise 7-2 (10 minutes)

May 2

Cash Receipts Journal

5

Purchases Journal

7

Sales Journal

8

Cash Receipts Journal

Sales Journal

Cash Receipts Journal

Cash Receipts Journal

T. Taylor …………………………..

5706

500

448

Exercise 7-3 (20 minutes)

CASH RECEIPTS JOURNAL

Date

Account Credited

Explanation

PR

Cash

Dr.

Sales

Discount

Dr.

Accounts

Recble.

Cr.

Sales

Cr.

Other

Accounts

Cr.

Cost of

Goods

Sold Dr.

Inventory Cr.

Nov. 9

Notes Payable ………………

Note to bank

3,750

3,750

Sales …………………………..

Cash sale

330

Exercise 7-4 (10 minutes)

November 3

Purchases Journal

Cash Receipts Journal

Cash Disbursements Journal

Cash Disbursements Journal

449

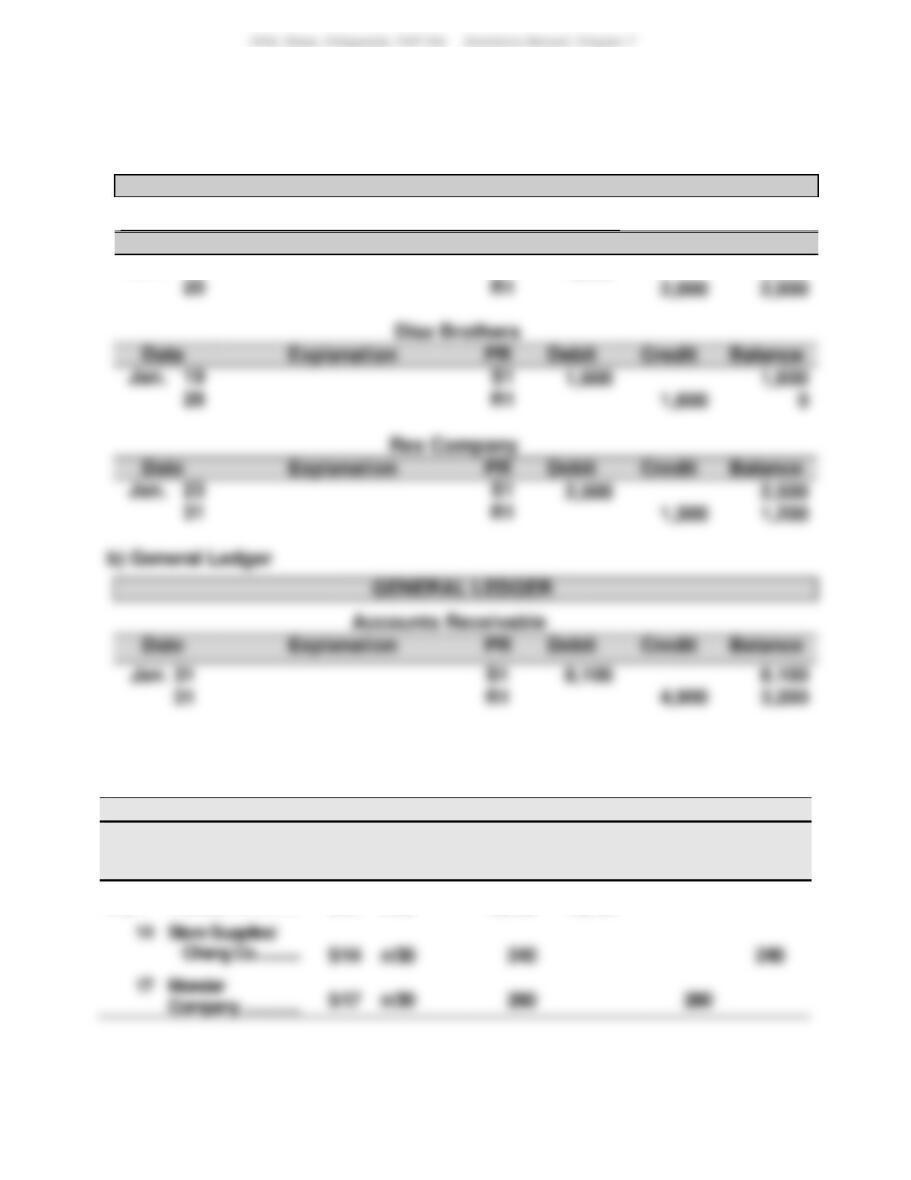

Exercise 7-5 (15 minutes)

(1) Accounts Payable Ledger

ACCOUNTS PAYABLE LEDGER

Bailey Company

Date

Explanation

PR

Debit

Credit

Balance

Jan. 9

P1

14,000

14,000

Johnson Brothers

Date

Explanation

PR

Debit

Credit

Balance

Jan. 18

P1

Date

Explanation

PR

Debit

Credit

Balance

Jan. 22

P1

(2) General Journal

GENERAL JOURNAL

Accounts Payable

Date

Explanation

PR

Debit

Credit

Balance

26,800

26,800

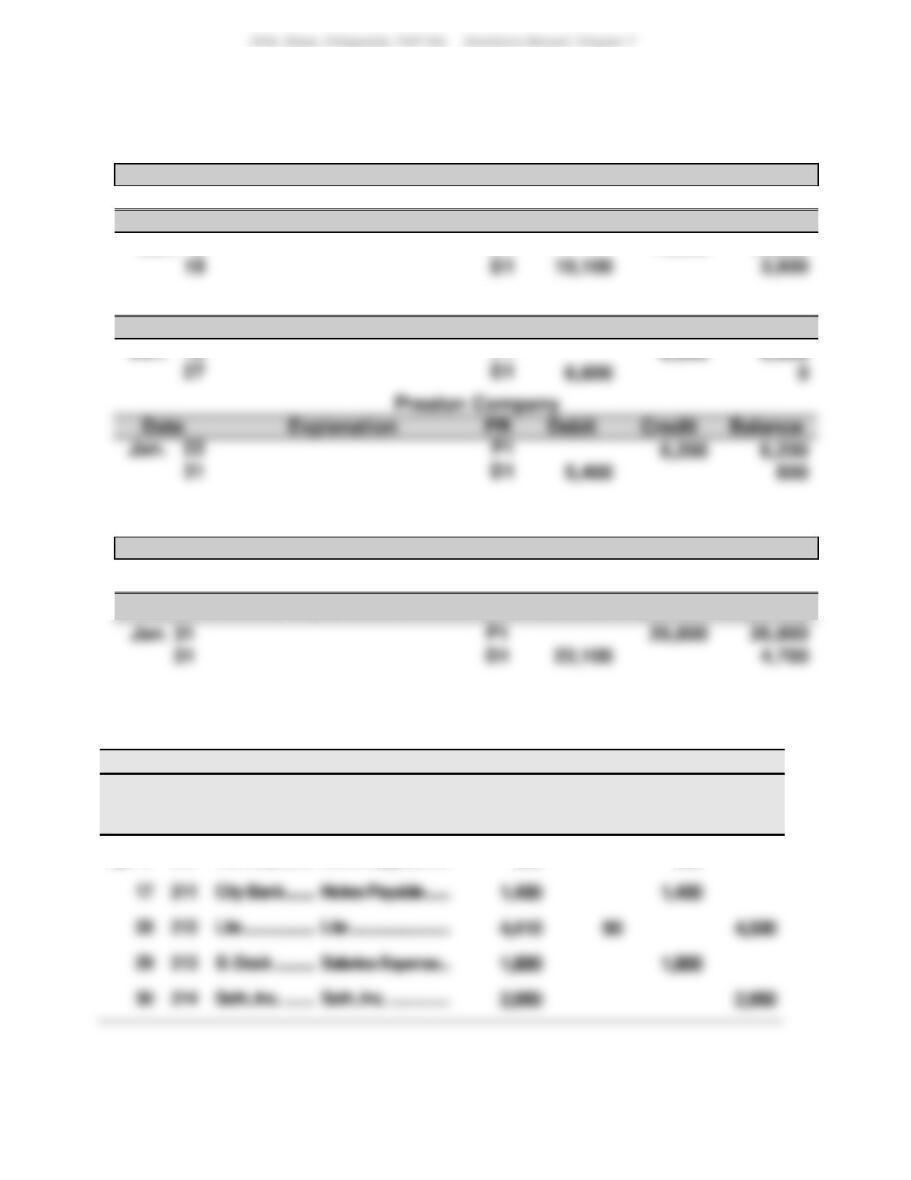

Exercise 7-6 (25 minutes)

CASH DISBURSEMENTS JOURNAL

Date

Ck.

No.

Payee

Account

Debited

PR

Cash

Cr.

Inventory

Cr.

Other

Accounts

Dr.

Accounts

Payable

Dr.

Apr. 9

210

Kitt Corp. …………………………..

Store Supplies …………………………..

650

650

212

Lite …………………………..

Lite …………………………..

Exercise 7-7 (10 minutes)

April 3

Purchases Journal

9

Cash Disbursements Journal

Cash Disbursements Journal

Purchases Journal

Cash Disbursements Journal

Cash Disbursements Journal

Cash Disbursements Journal

Exercise 7-8 (10 minutes)

1. B When crossfooting the Purchases Journal.

Exercise 7-9 (10 minutes)

a. (i) The June 5 purchase would be recorded in the Purchases Journal.

451

Exercise 7-10 (30 minutes)

Part 1

ACCOUNTS RECEIVABLE SUBSIDIARY LEDGER

Anna Page

Sara Reed

Aaron Reckers

May 17

May 10

Part 2

GENERAL LEDGER

Accounts Receivable

Sales

Sales Returns and

Allowances

May 31

Part 3

MOUNTAIN VIEW

Schedule of Accounts Receivable

May 31

Anna Page ………………………………………

$ 1,500

Aaron Reckers …………………………..

Total debit……………………………………………

452

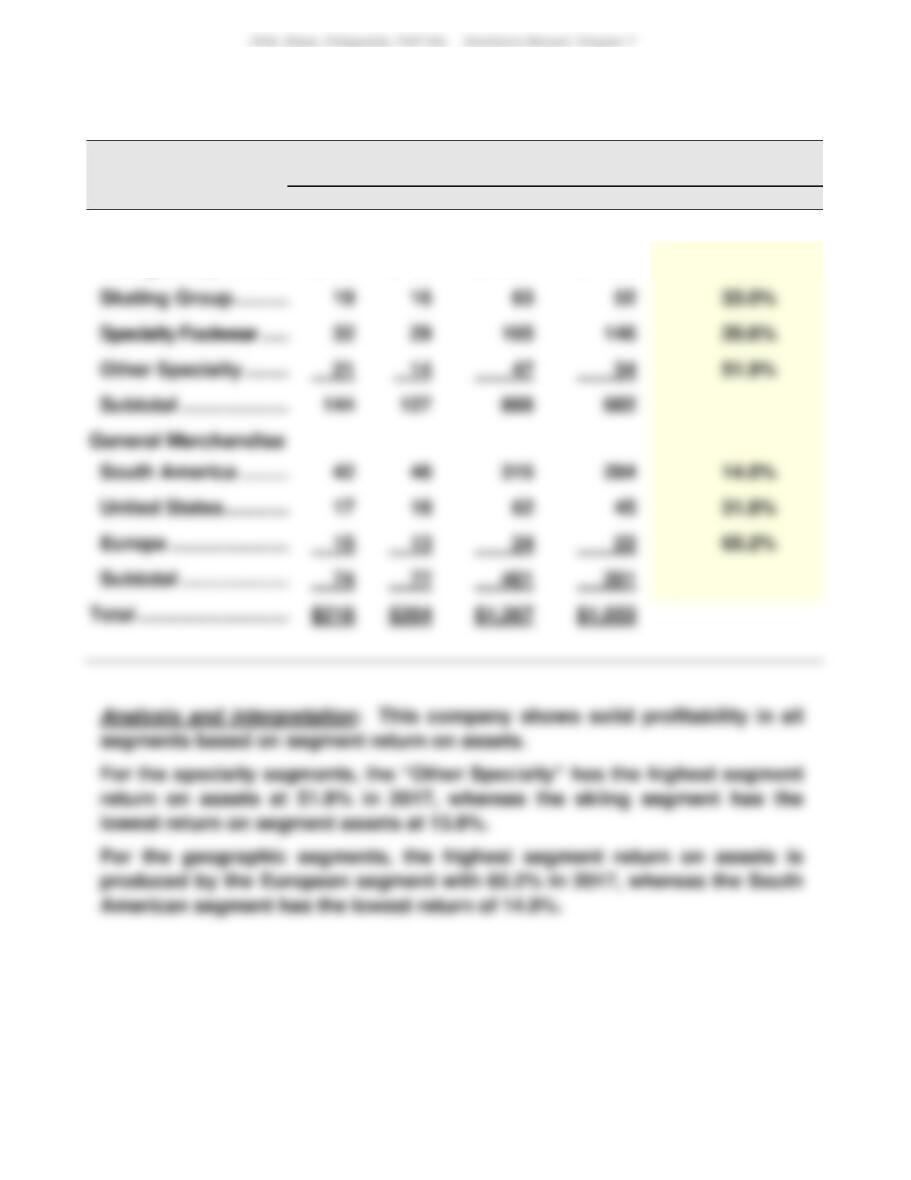

Exercise 7-11 (20 minutes)

Segment Income

(in $ mil.)

Segment Assets

(in $ mil.)

Segment Return

on Assets

Segment

2017

2016

2017

2016

2017

Specialty

Skiing Group …………..

$ 72

$ 68

$ 591

$ 450

13.8%

31.8%

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 7

453

PROBLEM SET A

Problem 7-1A (100 minutes)

Parts 1 and 2

SALES JOURNAL

Page 2

Date

Account Debited

Invoice

Number

PR

Accounts Receivable Dr.

Sales Cr.

Cost of Goods Sold Dr.

Inventory Cr.

Mar. 2

Min Cho ……………………………………………..

854

✓

16,800

8,400

3

Linda Witt …………………………………………..

855

✓

10,200

5,800

PURCHASES JOURNAL

Page 2

Date

Account

Date of

Invoice

Terms

PR

Accounts

Payable

Cr.

Inventory

Dr.

Office

Supplies

Dr.

Other

Accounts

Dr.

Mar. 1

Van Industries …………………………..

3/1

2/15, n/30

✓

43,600

43,600

Gabel Company …………………………..

3/3

✓

Office Equip./Spell Supply …………………….

3/9

21,850

The CD Company …………………………..

2/10, n/30

✓

32,625

32,625

Totals …………………………………………………….

76,225

Jovita Albany …………………………..

856

✓

5,600

2,900

Jovita Albany …………………………..

857

✓

14,910

7,220

Linda Witt …………………………………………..

858

✓

Totals …………………………………………………

51,825

27,600

454

Problem 7-1A (Continued)

Parts 1 and 2—continued

CASH RECEIPTS JOURNAL

Page 2

Date

Account Credited

Explanation

PR

Cash

Dr.

Sales

Discount

Dr.

Accounts

Receivable

Cr.

Sales

Cr.

Other

Accts.

Cr.

Cost of Goods

Sold Dr.

Inventory Cr.

Mar. 6

L.T. Notes Pay. …………………………..

Note to bank…………………………..

251

82,000

82,000

Min Cho …………………………..

Invoice, 3/2 …………………………..

16,464

Linda Witt …………………………..

Invoice 3/3 …………………………..

Sales …………………………..

Cash sales …………………………..

34,680

34,680

Jovita Albany …………………………..

Invoice, 3/10 …………………………..

5,600

Sales …………………………..

Cash sales …………………………..

30,180

Totals …………………………..

64,860

82,000

(101)

(413)

(502/119)

CASH DISBURSEMENTS JOURNAL

Page 2

Date

Ck.

No.

Payee

Account Debited

PR

Cash

Cr.

Inventory

Cr.

Other

Accounts

Dr.

Accounts

Payable

Dr.

Mar. 13

416

Van Industries …………………………..

Van Industries …………………………..

✓

42,728

872

43,600

417

Payroll …………………………..

18,300

418

The CD Co. …………………………..

The CD Company …………………………..

✓

29,596

604

30,200

419

Payroll …………………………..

Totals …………………………..

73,800

455

Problem 7-1A (Continued)

Parts 1 and 2—continued

GENERAL JOURNAL

Page 2

Mar. 17

Accounts Payable—CD Co. …………………………..

201/✓

2,425

Accounts Payable—Spell Supply ………………………..

201/✓

GENERAL LEDGER

Cash

Acct. No. 101

Date

Explanation

PR

Debit

Credit

Balance

Mar. 31

R2

178,808

178,808

D2

69,884

Accounts Receivable

Acct. No. 106

Date

Explanation

PR

Debit

Credit

Balance

Mar. 31

S2

51,825

51,825

R2

19,225

Inventory

Acct. No. 119

Date

Explanation

PR

Debit

Credit

Balance

Mar. 1

10,000

17

G2

2,425

7,575

31

1,476

31

Date

Explanation

PR

Debit

Credit

Balance

Mar. 3

P2

456

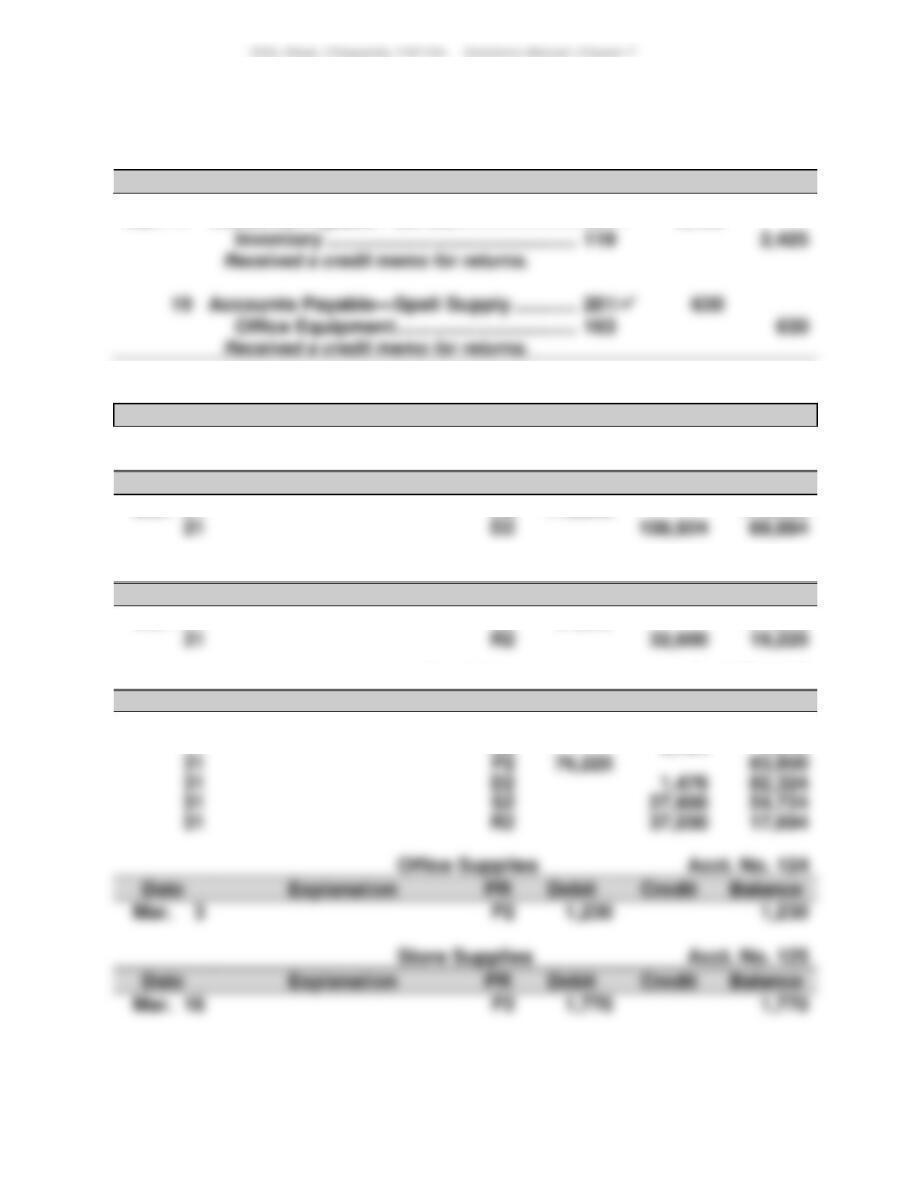

Problem 7-1A (Continued)

Office Equipment

Acct. No. 163

Date

Explanation

PR

Debit

Credit

Balance

Mar. 9

P2

21,850

21,850

G2

21,220

Accounts Payable

Acct. No. 201

Date

Explanation

PR

Debit

Credit

Balance

Mar. 17

G2

2,425

(2,425)

G2

(3,055)

P2

98,020

73,800

24,220

Long-Term Notes Payable

Acct. No. 251

Date

Explanation

PR

Debit

Credit

Balance

Mar. 6

82,000

82,000

Z. Church, Capital

Acct. No. 301

Date

Explanation

PR

Debit

Credit

Balance

Mar. 1

10,000

Sales

Acct. No. 413

Date

Explanation

PR

Debit

Credit

Balance

Mar. 31

S2

51,825

51,825

64,860

Sales Discounts

Acct. No. 415

Date

Explanation

PR

Debit

Credit

Balance

Mar. 31

Cost of Goods Sold

Acct. No. 502

Date

Explanation

PR

Debit

Credit

Balance

Mar. 31

37,030

37,030

Mar. 31

S2

27,600

64,630

Sales Salaries Expense

Acct. No. 621

Date

Explanation

PR

Debit

Credit

Balance

Mar. 15

18,300

18,300

18,300

36,600

457

Problem 7-1A (Continued)

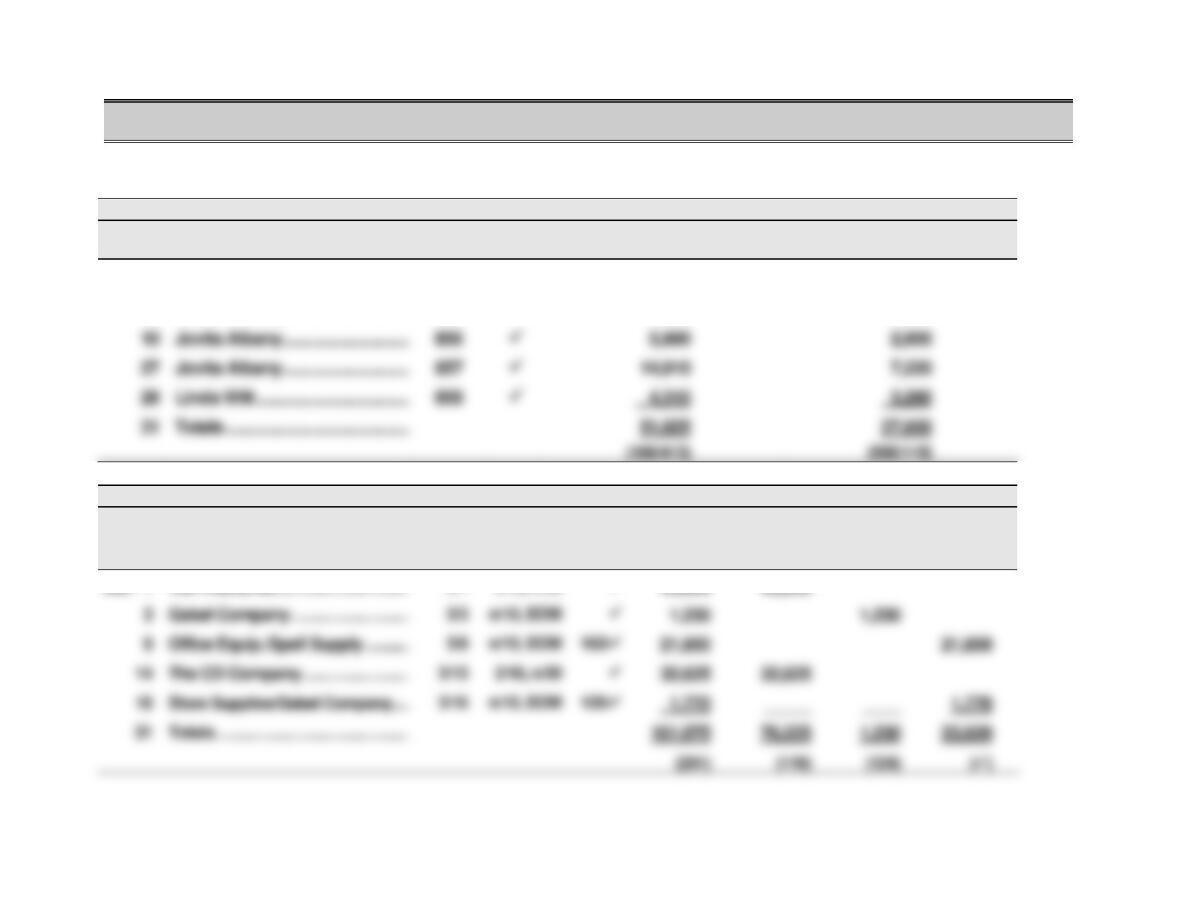

ACCOUNTS RECEIVABLE LEDGER

Jovita Albany

Date

Explanation

PR

Debit

Credit

Balance

Mar. 10

S2

5,600

5,600

S2

Min Cho

Date

Explanation

PR

Debit

Credit

Balance

Mar. 2

S2

Linda Witt

Date

Explanation

PR

Debit

Credit

Balance

Mar. 3

S2

S2

4,315

4,315

ACCOUNTS PAYABLE LEDGER

CD Company

Date

Explanation

PR

Debit

Credit

Balance

Mar. 14

P2

32,625

32,625

30,200

Date

Explanation

PR

Debit

Credit

Balance

Mar. 3

P2

P2

Mar. 9

P2

21,850

21,850

21,220

Date

Explanation

PR

Debit

Credit

Balance

Mar. 1

P2

43,600

43,600

458

Problem 7-1A (Concluded)

Part 3

CHURCH COMPANY

Trial Balance

March 31

Debit

Credit

Cash ……………………………………………………….

$ 69,884

Accounts receivable ……………………………………..

Accounts payable …………………………………………

Sales discounts…………………………………………….

Sales salaries expense …………………………..

36,600

CHURCH COMPANY

Schedule of Accounts Receivable

March 31

Jovita Albany ………………………………………………….

$14,910

CHURCH COMPANY

Schedule of Accounts Payable

March 31

Gabel Company ………………………………………………

$ 3,000

459

Problem 7-2A (70 minutes)

Parts 1, 2 and 3

SALES JOURNAL

Page 3

Date

Account Debited

Invoice

Number

PR

Accounts Receivable Dr.

Sales Cr.

Cost of Goods Sold Dr.

Inventory Cr.

Apr. 3

Page Alistair …………………………..

760

✓

4,000

3,000

5

Paula Kohr …………………………………………

761

✓

8,000

6,500

Nic Nelson ………………………………………….

7,000

Page Alistair …………………………..

763

✓

5,100

3,600

Paula Kohr …………………………………………

764

✓

3,170

2,520

Nic Nelson ………………………………………….

765

✓

Totals …………………………………………………

CASH RECEIPTS JOURNAL

Page 3

Date

Account Credited

Explanation

PR

Cash

Dr.

Sales

Discount

Dr.

Accounts

Receivable

Cr.

Sales

Cr.

Other

Accts.

Cr.

Cost of Goods

Sold Dr.

Inventory Cr.

Apr.13

Page Alistair …………………………..

Sale of 4/3

✓

3,920

80

4,000

Paula Kohr …………………………..

Sale of 4/5

✓

7,840

8,000

Sales …………………………..

Cash Sales

✓

Note to bank

Nic Nelson …………………………..

Sale of 4/11

✓

Page Alistair …………………………..

Sale of 4/13

✓

4,998

5,100

Sales …………………………..

Cash sales

Totals …………………………..

126,815

460

Problem 7-2A (Continued)

Parts 2 and 3

GENERAL LEDGER

Cash

Acct. No. 101

Date

Explanation

PR

Debit

Credit

Balance

Mar. 31

85,000

298,863

Accounts Receivable

Acct. No. 106

Date

Explanation

PR

Debit

Credit

Balance

Apr. 30

S3

37,470

37,470

Inventory

Acct. No. 119

Date

Explanation

PR

Debit

Credit

Balance

Mar. 31

125,000

Apr. 30

S3

98,075

Long-Term Notes Payable

Acct. No. 251

Date

Explanation

PR

Debit

Credit

Balance

Mar. 31

110,000

Apr. 18

170,000

B. Wiset, Capital

Acct. No. 301

Date

Explanation

PR

Debit

Credit

Balance

Mar. 31

100,000

Acct. No. 413

Date

Explanation

PR

Debit

Credit

Balance

Apr. 30

S3

37,470

164,285

Acct. No. 415

Date

Explanation

PR

Debit

Credit

Balance

Apr. 30

Acct. No. 502

Date

Explanation

PR

Debit

Credit

Balance

Apr. 30

S3

26,925

26,925

94,780

121,705