7-41

PROBLEM 7-46 (35 MINUTES)

1.

units 25,000

$750,000 $1,250,000

margin oncontributiUnit

−

=

2.

Number of sales units required

to earn target net profit

margin oncontributiunit

profitnet target costs fixed

+

=

3.

margin oncontributiunit new

costs fixed new

units) (inpoint even–break New

=

4.

Number of sales units required

*Last year’s profit: ($50)(25,000) – $1,050,000 = $200,000

margin oncontributiunit new

profitnet target costs fixed new

+

=

to earn target net profit, given

Chapter 07 – Cost-Volume-Profit Analysis

7-42

PROBLEM 7-46 (CONTINUED)

5.

margin oncontributiunit

ratio margin–onContributi

=

*Sales price, given in problem.

Let P denote the price required to cover increased direct-material cost and maintain

the same contribution-margin ratio:

Check:

7-43

PROBLEM 7-47 (40 MINUTES)

1.

Memorandum

Date: Today

To: Vice President for Manufacturing, Saturn Game Company

2. New break-even point if automated manufacturing equipment is installed:

Sales price ……………………………………………………………………………………….. $52

Costs that are variable (with respect to sales volume):

PROBLEM 7-47 (CONTINUED)

3.

Sales (in units) required to show a profit of $280,000:

Number of sales units required

profitnet target cost fixed

+

4.

If management adopts the new manufacturing technology:

(a)

Its break-even point will be higher (17,000 units instead of 15,000 units).

PROBLEM 7-47 (CONTINUED)

5.

The controller should include the break-even analysis in the report. The Board of

Directors needs a complete picture of the financial implications of the proposed

equipment acquisition. The break-even point is a relevant piece of information. The

controller should accompany the break-even analysis with an explanation as to

7-46

PROBLEM 7-48 (45 MINUTES)

1.

tonper $450

1,800

$810,000

margin oncontributiUnit

==

2.

Projected net income for sales of 2,100 tons:

Projected fixed costs ……………………………………………………………………

Projected net income ……………………………………………………………………

3.

Projected net income including foreign order:

Foreign

Order

Regular

Sales

Sales in tons ……………………………………………………………

1,500

1,500

Contribution margin per ton:

7-47

PROBLEM 7-48 (CONTINUED)

4.

New sales territory:

To maintain its current net income, Central Pennsylvania Limestone Company just

needs to break even on sales in the new territory.

5.

Automated production process:

$50 $450

$117,000 $495,000

tonsinpoint even–Break

+

+

=

6.

Changes in selling price and unit variable cost:

$80) ($550 0%)($1,000)(9 margin oncontributiunit New

+−=

Chapter 07 – Cost-Volume-Profit Analysis

7-48

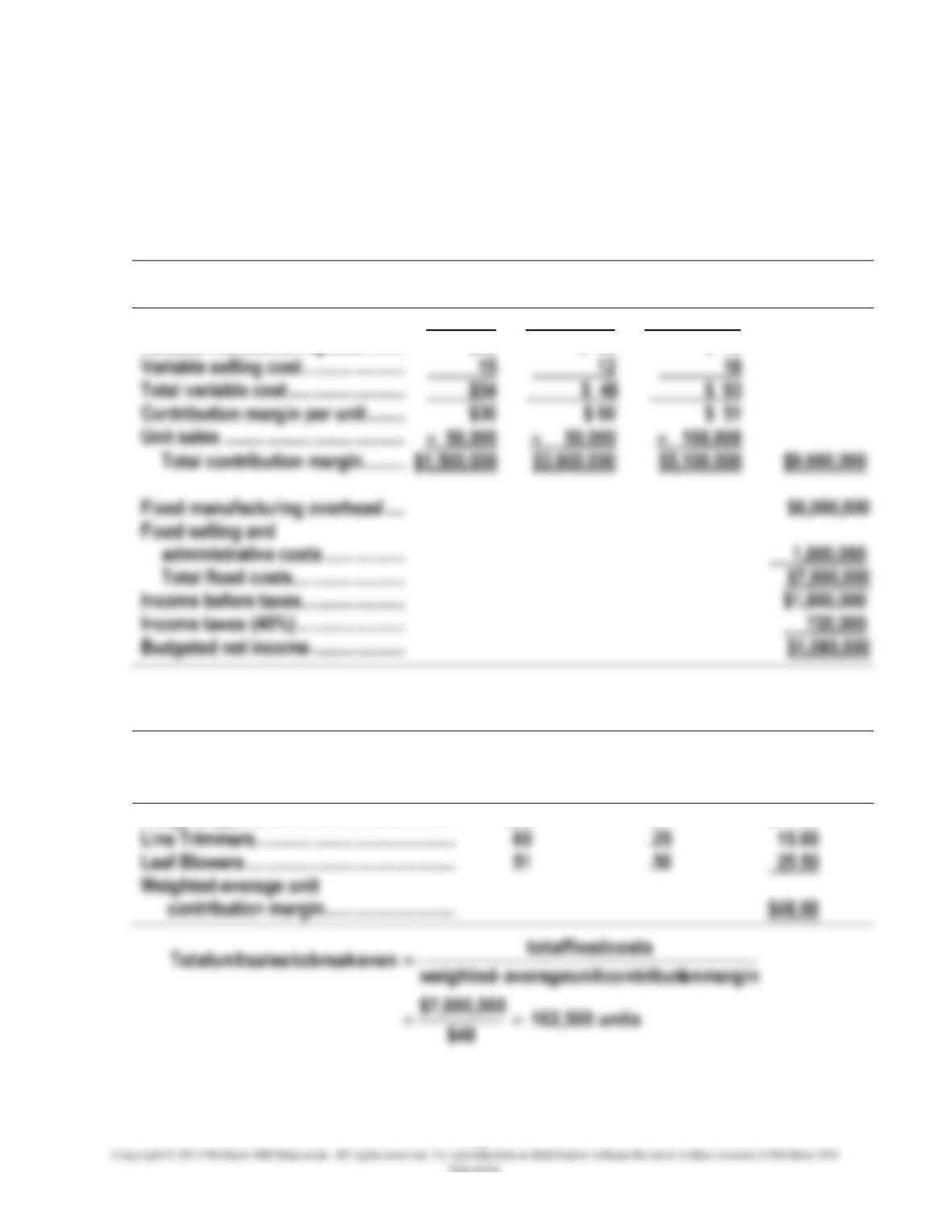

PROBLEM 7-49 (45 MINUTES)

1.

TOLEDO TOOL COMPANY

BUDGETED INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 20X4

Hedge

Clippers

Line

Trimmers

Leaf Blowers

Total

Unit selling price ………………………….

$84

$108

$144

Variable manufacturing cost ………..

$39

$ 36

$ 75

Variable selling cost …………………….

15

12

18

Total variable cost ……………………….

$54

$ 48

$ 93

Contribution margin per unit ………..

$30

$ 60

$ 51

Total contribution margin …………

$1,500,000

$3,000,000

$5,100,000

Fixed manufacturing overhead …….

Fixed selling and

Total fixed costs ………………………

Income before taxes …………………….

Income taxes (40%) ……………………..

2.

(a)

Unit

Contribution

(b)

Sales

Proportion

(a) (b)

Hedge Clippers …………………………………….

$30

.25

$ 7.50

Line Trimmers ………………………………………

.25

15.00

Leaf Blowers ………………………………………..

.50

Chapter 07 – Cost-Volume-Profit Analysis

7-49

PROBLEM 7-49 (CONTINUED)

Sales proportions:

Sales

Proportion

Total Unit

Sales

Product Line

Sales

Hedge Clippers ………………………………………

.25

162,500

40,625

Line Trimmers ………………………………………..

.25

162,500

40,625

Leaf Blowers ………………………………………….

.50

162,500

3.

(a)

Unit

Contribution

(b)

Sales

Proportion

(a) (b)

Hedge Clippers ………………………………………………..

$30

.20

$ 6.00

Line Trimmers* ………………………………………………..

.20

11.40

Leaf Blowers† ………………………………………………….

.60

*Variable selling cost increases. Thus, the unit contribution decreases to

margin oncontributiunit average–weighted

costs fixed total

evenbreak tosalesunit Total

=

Sales proportions:

Sales

Proportions

Total Unit

Sales

Product Line

Sales

Hedge Clippers ……………………………………………

.20

200,000

40,000

Line Trimmers ……………………………………………..

.20

200,000

40,000

Leaf Blowers ……………………………………………….

.60

200,000

7-50

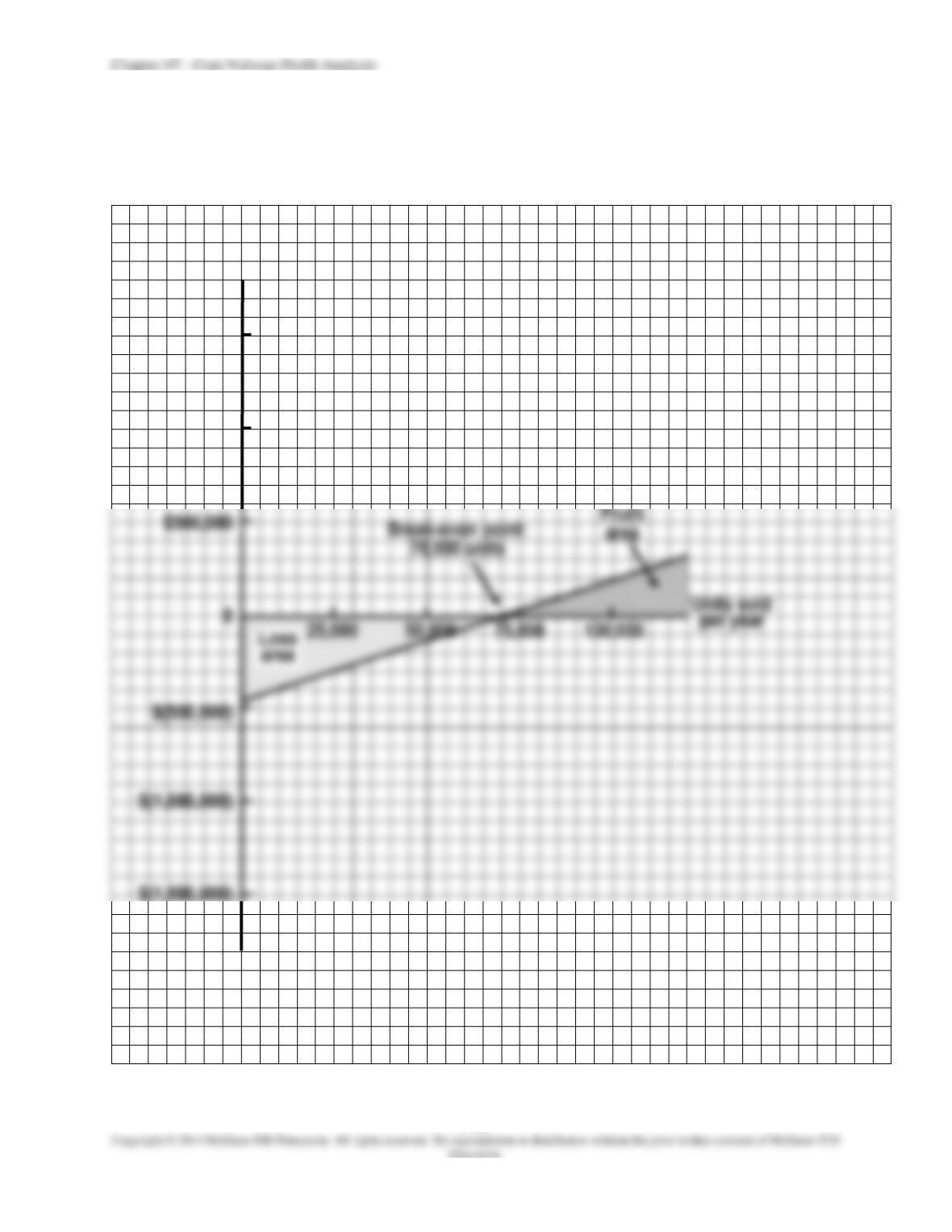

PROBLEM 7-50 (35 MINUTES)

1.

(a)

$6

sold units

costs variable sales

margin oncontributiUnit

−

=

(b)

revenue sales

margin oncontributi

ratio margin–onContributi

=

2.

Number of units of sales required

to earn target after-tax net income

margin oncontributiunit

) (1

incomenet tax–aftertarget

costs fixed

−

+

=t

3.

If fixed costs increase by $63,000:

7-51

PROBLEM 7-50 (CONTINUED)

4. Profit-volume graph:

Dollars per year

$1,500,000

$1,000,000

7-52

PROBLEM 7-50 (CONTINUED)

5.

Number of units of sales

) (1

incomenet tax–aftertarget

costs fixed

−

+

=t