Ex. 7.3 a.

b.

Employee theft is never ethical, even if it is committed to pay for medical bills.

There were several controls lacking at White Electric Supply which made it

possible for the bookkeeper to embezzle nearly $416,000 in less than five years.

Ex. 7.4 a.

b.

c. (1)

(2)

(3)

The fraudulent actions by D. J. Fletcher would not cause the general ledger to be

If Bluestem Products bonds its employees, it may be able to collect the $3,000

In the income statement, the Sales Returns and Allowances account would be

restitution.

Cash receipts should be deposited daily in the bank. The $3,000 of currency

The function of handling cash should be separate from the maintenance of

The employee who opens the mail should prepare a list of amounts

(4)

Ex 7.5 a. $ 15,200

Add: Undeposited receipts of December 31 ………………………………………..

10,000

$ 25,200

25

775

Cash …………………………………………………………..

Accounts Receivable (Jane Jones) …………………………………..

Bank Service Charges ………………………………………………..

b.

Balance per bank statement ……………………………………………………

Adjusted cash balance ……………………………………………………………..

$ 16,700

Balance per depositor’s records …………………………………………………..

$ 17,500

Adjusted cash balance, as above ………………………………………………….

$ 16,700

Jane Jones check returned NSF …………………………….

Service charges …………………………………………………….

Ex. 7.6

Ex. 7.7 a.

b.

d. (1)

Valuation at market value is not a departure from the principle of

e.

Fair value accounting benefits users of financial statements by showing

marketable securities at the amount of cash those securities represent under

The highest interest rates are offered by Citizens Trust Bank and Commerce Bank,

both are offering 0.05%. The benefit of investing with Citizens Trust is that there is

Marketable securities are either equity or debt instruments that are readily

cash at quoted market prices.

Cash generates little or no revenue. Marketable securities, on the other hand,

produce revenue in the form of dividends, interest, and perhaps increases in their

The valuation of marketable securities at market value is a departure from

c.

Ex. 7.8 a. 200,000

b. 155,000

155,000

Required year-end credit balance ………….………….….

Temporary debit balance……………………………….

Credit balance at beginning of year…………………………

Required adjustment for year……………………………….

Write-offs during year……………………………………..

c. 96,000

Accounts Receivable…………….……………………………….

d.

Ex. 7.9 a.

b.

c.

Adjusting the balance in the Allowance for Doubtful Accounts account based upon

Uncollectible Accounts Expense………………………………. ……..

The reason it takes Goodyear 17 days longer than PPL to collect its receivables is

due, in large part, to industry characteristics of each company. Customers of

Uncollectible Accounts Expense ………………………………………………………………………

Uncollectible Accounts Expense ……………………………………………………

Allowance for Doubtful Accounts…………………………………..

Allowance for Doubtful Accounts…………………………………..

Total Net Operating Non Operating

Transaction Assets Income Cash Flow Cash Flow

a. NE NE NE D*

b. NE NE INE

Ex. 7.10

d. NE NE NE NE

a.

b.

c.

d.

f.

g.

h.

Cash earmarked for a special purpose is not available to pay current liabilities and,

Compensating balances are included in the amount of cash listed in the balance sheet, and

Ex. 7.11

Cash equivalents normally are not shown separately in financial statements. Rather, they

The difference between the cost and current market value of securities owned is shown in

The accounts receivable turnover rate is equal to net sales divided by average accounts

Realized gains and losses on investments sold during the year are reported in the income

Transfers between cash and cash equivalents are not reported in financial statements. For

e.

Receivables

Gross

Curren

Turnover Net Retained Working

Transaction Profit Ratio Rate Income Earnings Capital

a. U NE UNE NE NE

Ex. 7.12

Ex. 7.13 a.

b.

c. Jan. 4 520,000

Marketable Securities ……………………………………

180,000

d.

The sale of securities on January 4, Year 2, will increase Wharton’s taxable

The amount of unrealized holding gain included in the securities’ current market

As of December 31, Year 1, Wharton Inc. still owns the marketable securities.

investments.

Cash …………………………………………………………

Gain on Sale of Investments ……………………

340,000

a.

Year 1

Aug. 1

1.

Year 2

Jan. 31

3.

Year 2

Jan. 31

4.

Interest Receivable ………………………………………………………

Interest Revenue …………………………………………………………

Interest Revenue ……………………………………………………..

Interest Receivable …………………………………………………..

43,200

Accounts Receivable (Dusty Roads) ……………………………………….

45,144

Notes Receivable ……………………………………………………..

Net

Revenue –Expenses = Income Assets = Equity

NE NE NE NE NE

INE I I I

INE I I I

INE I I I

4.

NE

3.

NE

Ex. 7.14

Notes Receivable ……………………………………………………..

43,200

Accounts Receivable (Dusty Roads) ………………………………

43,200

Cash ………………………………………………………………………….

45,144

Notes Receivable ………………………………………………………….

43,200

2.

NE

b.

Transaction

1.

NE

Liabilities +

Dec. 31

2.

Interest Revenue ……………………………………………………..

Interest Receivable ………………………………………………………..

b.

d. 88.519 billion

Accounts receivable 02/03/13

Average days outstanding (rounded)

Note to instructor: The notes accompanying the financial statements reveal that the company has an

The company does not report any investments in marketable securities. If Home Depot had

Net sales

Financial (current) assets = $4.106 billion (2.216 billion + 1.890 billion)

25 Minutes, Medium

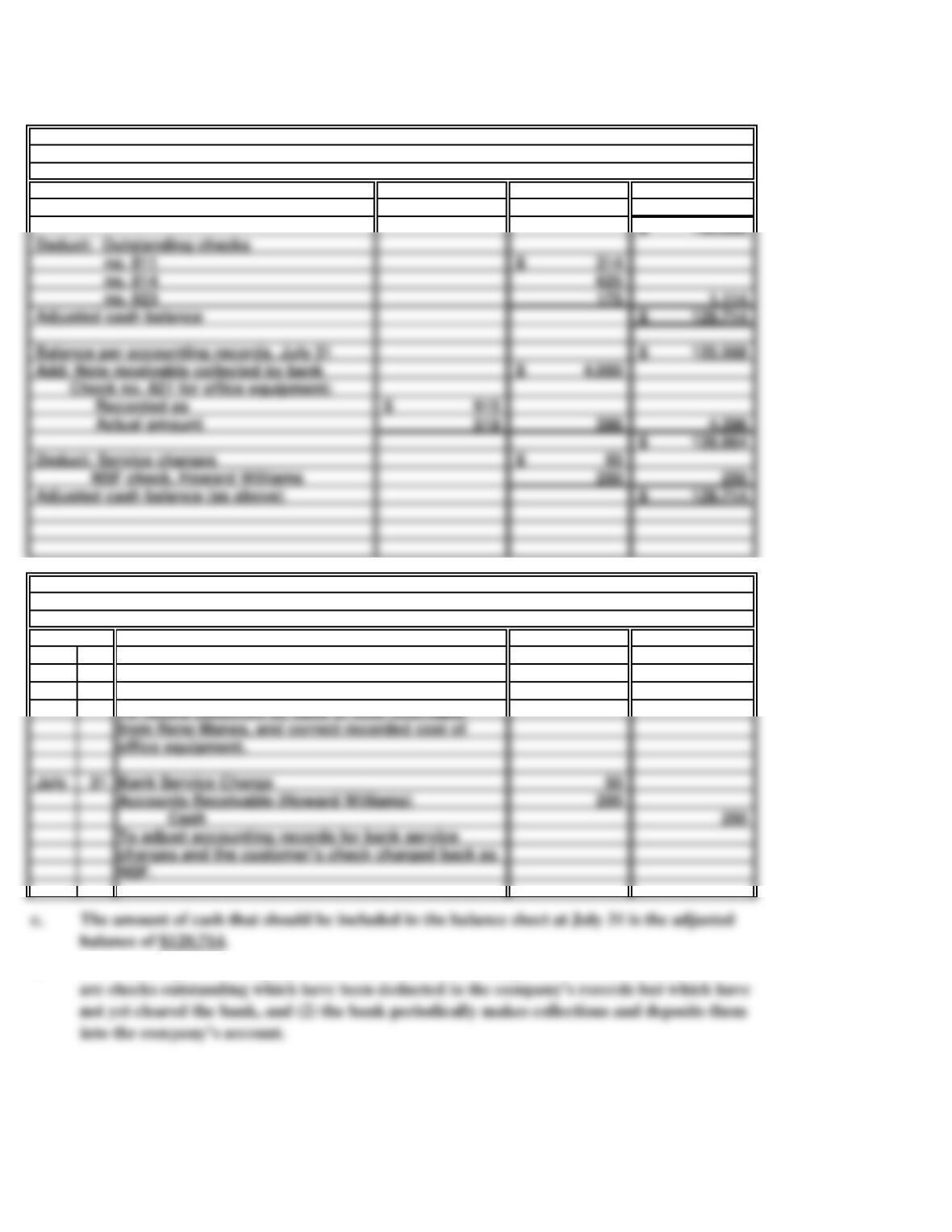

a.

114,828$

16,000

b.

July 31 4,396

Notes Receivable 4,000

Office Equipment 396

July 31 50

Cash 250

To record collection by bank of note receivable

Accounts Receivable (Howard Williams)

charges and the customer’s check charged back as

office equipment.

from Rene Manes, and correct recorded cost of

Bank Service Charge

To adjust accounting records for bank service

d.

Add: Deposit in transit

General Journal

SOLUTIONS TO PROBLEMS SET A

PROBLEM 7.1A

BANNER, INC.

July 31

Bank Reconciliation

BANNER, INC.

Balance per bank statement, July 31

The balance per the company’s bank statement is often larger for two reasons: (1) There

Cash

Deduct: Outstanding checks

Deduct: Service charges

Adjusted cash balance

Balance per accounting records, July 31

Add: Note receivable collected by bank

Adjusted cash balance (as above)

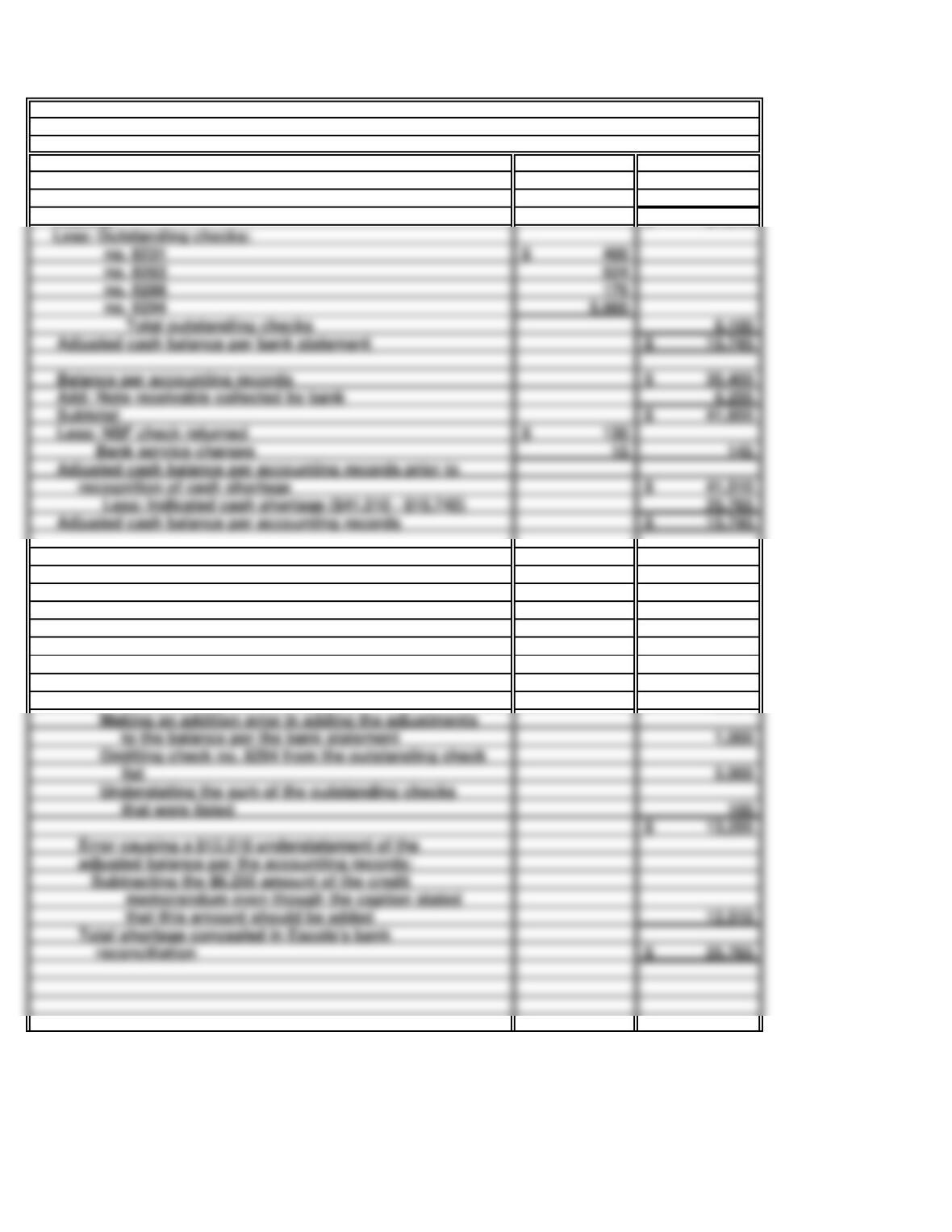

45 Minutes, Strong

a. Corrected bank reconciliation for November:

Balance per bank statement, November 30 20,600$

1,245

21,845$

900$

6,255

1,000

5,000

13,255$

25,765$

reconciliation

Understating the sum of the outstanding checks

Error causing a $12,510 understatement of the

memorandum even though the caption stated

that this amount should be added

Total shortage concealed in Escola’s bank

Subtracting the $6,255 amount of the credit

adjusted balance per the accounting records:

that were listed

Omitting check no. 8294 from the outstanding check

list

to the balance per the bank statement

Making an addition error in adding the adjustments

the following intentional errors in her reconciliation:

Errors leading to a $13,255 overstatement of the

b. Escola attempted to conceal the shortage by making

by the bank to the bank balance

adjusted balance per the bank statement:

Overstating the deposit in transit with a

transposition error

Add: Deposit in transit

Subtotal

Improperly adding the amount of the note collected

PROBLEM 7.2A

OSAGE FARM SUPPLY

November 30

BANK RECONCILIATION

OSAGE FARM SUPPLY

6,100

15,745$

35,400$

6,255

41,655$

15,745$

recognition of cash shortage

Balance per accounting records

Add: Note receivable collected by bank

Subtotal

Less: NSF check returned

Adjusted cash balance per accounting records

Bank service charges

Adjusted cash balance per accounting records prior to

Less: Outstanding checks:

no. 8231

no. 8263

Adjusted cash balance per bank statement

no. 8288

no. 8294

Total outstanding checks