CCC7 CONTINUING COOKIE CHRONICLE

Part 1

The weaknesses in internal accounting controls in the system recommended by

John are:

(2) John could potentially steal from the company and then cover the

(3) The accounting information for the business could be lost or stolen if

it is all stored on John’s laptop.

(4) John should not be able to write checks to himself as this leaves the

company vulnerable to theft.

Improvements should include the following:

(2) John should be responsible for the accounting function only. Natalie

(or some other independent person) should sign all checks and make

(3) Bank reconciliations should be prepared by a person independent

of the handling and recording of cash. However, this may not be

(4) The accounting records should be maintained on site and regular

back–ups should be prepared. It would be best if John used a com–

(5) John should submit a monthly invoice for the work he has done to

Natalie for her approval. Natalie should then write and sign the check.

CONTINUING COOKIE CHRONICLE (Continued)

Part 2

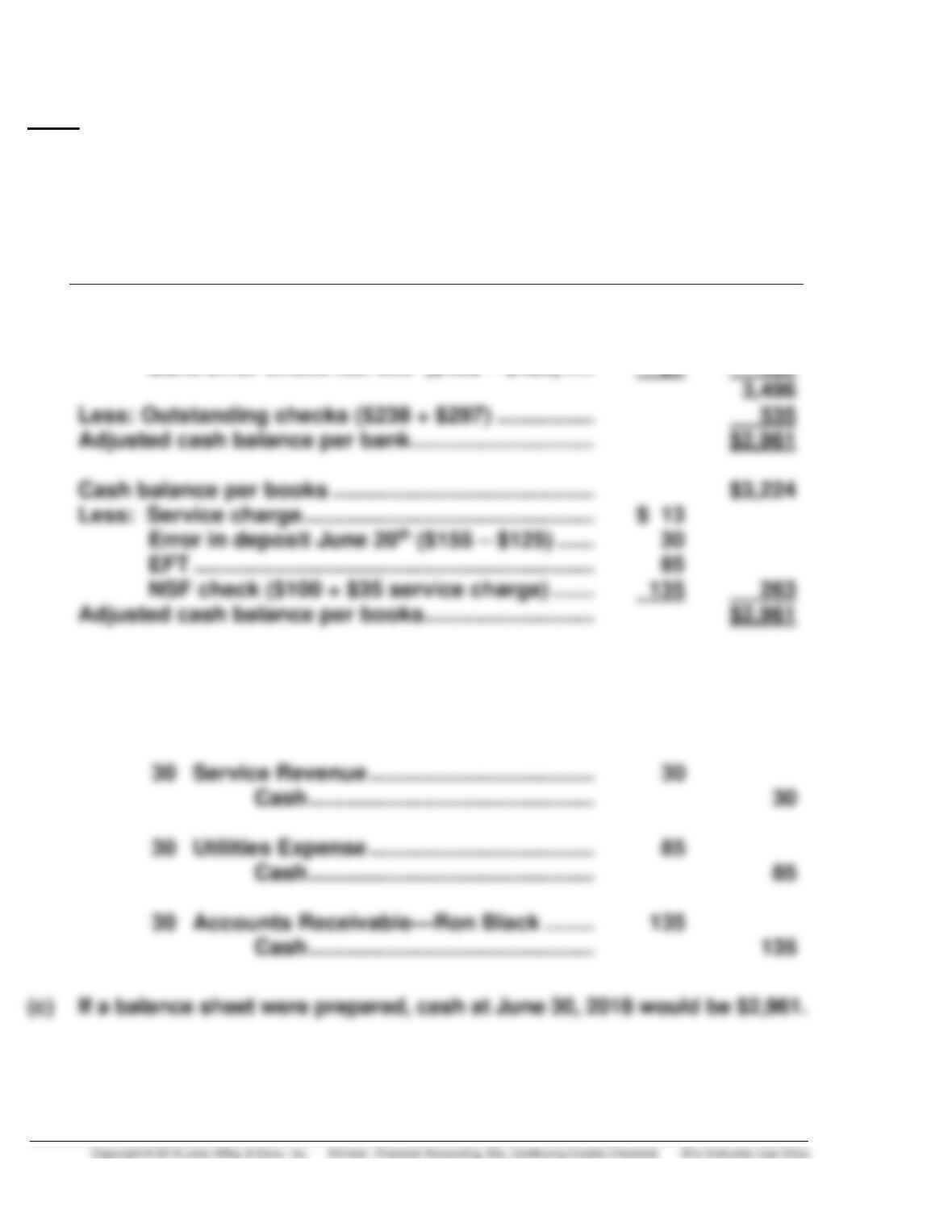

(a) COOKIE CREATIONS INC.

Bank Reconciliation

June 30, 2018

Cash balance per bank statement ……………………….

$3,359

Add: Deposit in transit ……………………………………..

$110

Bank error Check No. 603 ($452 – $425) …..

27

137

Less: Outstanding checks ($238 + $297) …………….

535

Adjusted cash balance per bank …………………………

Cash balance per books …………………………………….

Less: Service charge …………………………………………

Error in deposit June 20th ($155 – $125) ……

30

85

NSF check ($100 + $35 service charge) …….

263

Adjusted cash balance per books ……………………….

(b)

June 30

Miscellaneous Expense …………………….

13

Cash………………………………………..

13

Service Revenue ……………………………….

30

Cash ………………………………………..

30

Utilities Expense ……………………………….

85

Cash ………………………………………..

85

Accounts Receivable—Ron Black ……..

Cash ………………………………………..