P7–5

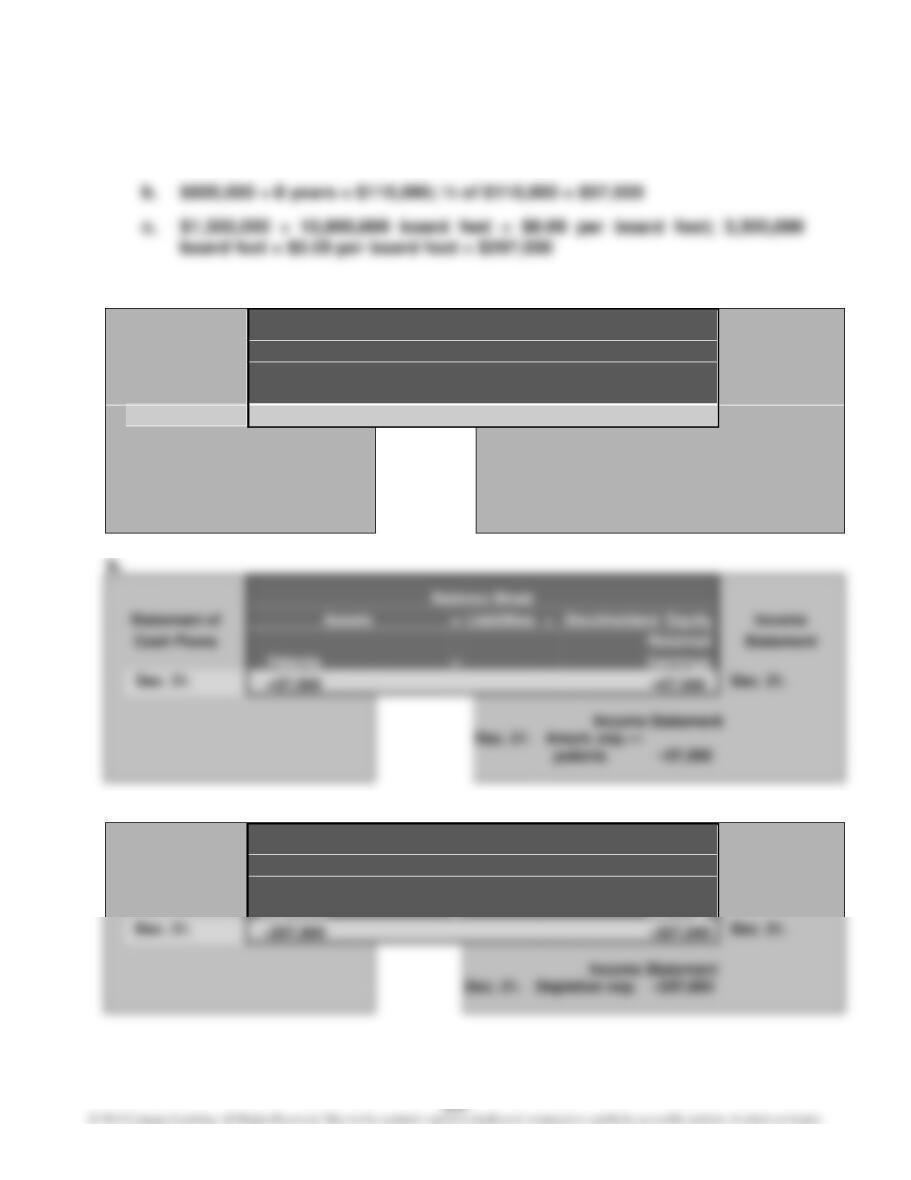

1. a. Loss on impairment of goodwill, $3,000,000

2. a.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Retained

Statement

Goodwill

=

Earnings

Dec. 31.

–3,000,000

–3,000,000

Dec. 31.

Income Statement

Dec. 31.

Loss from

impaired

goodwill

–3,000,000

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Retained

Statement

=

Earnings

–57,500

–57,500

c.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

– Acc.

Retained

Statement

=

Earnings

Dec. 31.

Depletion exp.

–297,000

FINANCIAL ANALYSIS

FA7–1

1. Net sales …………………………………………… $37,110

Average net property, plant, and equipment:

2. United’s fixed asset turnover is 2.22 compared to Delta’s 1.73. United is gen-

erating $0.49 ($2.22 – $1.73) more sales per average dollar of invested fixed

FA7–2

1. Net sales …………………………………………… $15,658

Average net property, plant, and equipment:

($10,578 + $12,127) ÷ 2 …………………. $11,353

Fixed asset turnover:

($15,658 ÷ $11,353) ………………………. 1.38

FA7–3

1. Year 2 Year 1

Net sales …………………………………………… $4,504 $3,779

2. JetBlue increased its fixed asset turnover by 0.14 from 0.81 in Year 1 to 0.95

in Year 2. This is a favorable trend and implies that JetBlue is more efficiently

using its fixed asset to generate sales in Year 2.

FA7–4

1. The fixed asset turnovers are summarized below from highest to lowest.

Fixed Asset

2. As shown above, United has the highest fixed asset turnover followed by Del-

ta, Southwest, and JetBlue. These differences are significant and a review of

FA7–5

1. Marriott Intercontinental

Net sales ……………………………………………. $12,317 $1,768

2. Marriott’s fixed asset turnover of 9.95 is significantly higher than Interconti-

nental’s fixed asset turnover of 1.08. The reasons for these significant differ-

ences could be due to how each company manages its properties. For exam-

ple, these differences could be due to how each company handles its

CASES

Case 7–1

It is considered unprofessional for employees to use company assets for

personal reasons, because such use reduces the useful life of the assets for

normal business purposes. Thus, it is unethical for Rowel Baylon to use Arches

Case 7–2

You should explain to Don and Rita that it is acceptable to maintain two sets

of records for tax and financial reporting purposes. This can happen when a

company uses one method for financial statement purposes, such as straight-line

depreciation, and another method for tax purposes, such as MACRS depreciation.

Case 7–3

1. a. Straight-line method:

20Y2: ($300,000 ÷ 5) × 1/2 ………………………………………………………….. $30,000

20Y3: ($300,000 ÷ 5) ………………………………………………………………….. 60,000

20Y4: ($300,000 ÷ 5) ………………………………………………………………….. 60,000

b. MACRS:

20Y2: ($300,000 × 20%) …………………………………………………………….. $60,000

Case 7–3, Continued

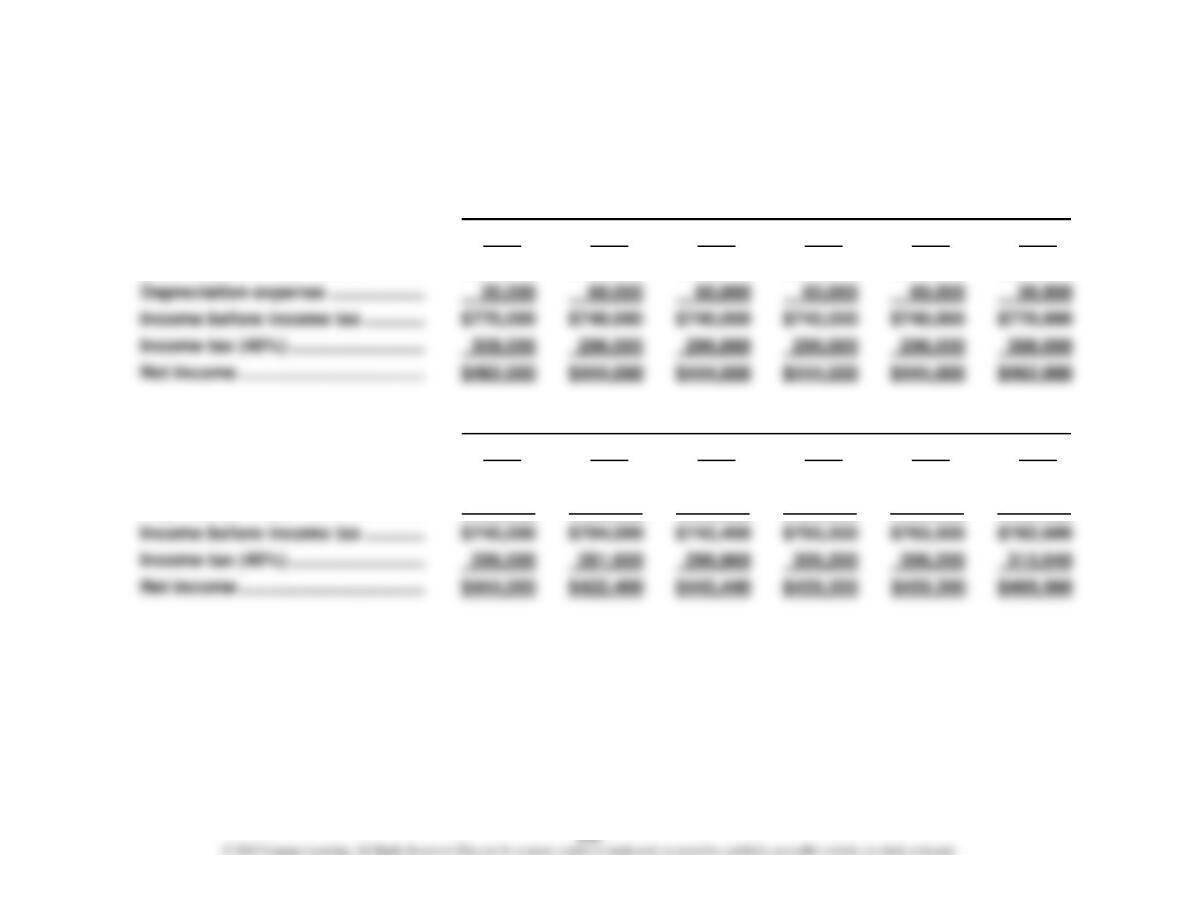

2.

a. Straight-line method Year

20Y2 20Y3 20Y4 20Y5 20Y6 20Y7

Income before depreciation ………. $800,000 $800,000 $800,000 $800,000 $800,000 $800,000

b. MACRS Year

20Y2 20Y3 20Y4 20Y5 20Y6 20Y7

Income before depreciation ………. $800,000 $800,000 $800,000 $800,000 $800,000 $800,000

Depreciation expense ………………. 60,000 96,000 57,600 34,500 34,500 17,400

Case 7–3, Concluded

3. For financial reporting purposes, Bree should select the method that provides

the net income figure that best represents the results of operations. (Note to

Instructors: The concept of matching revenues and expenses was discussed

in Chapter 3.) However, for income tax purposes, Bree should consider se-

lecting the method that will minimize current taxes. Based on the analyses in

(2), both methods of depreciation will yield the same total amount of taxes

over the useful life of the equipment. MACRS results in fewer taxes paid in the

early years of useful life and more in the later years. For example, in 20Y2 the

Case 7–4

Note to Instructors: The purpose of this activity is to familiarize students with the

considerations in leasing and buying a business asset. A couple of Internet sites

that your students might find useful in deciding whether to purchase or lease an

asset are:

Some considerations on deciding whether to purchase or lease an asset include

the following:

• The amount of time the business will be using the asset. If the business

needs the asset for a short time only, then leasing may be more advanta-

geous.

• How quickly will the asset become obsolete? Leasing may be more advan-

tageous if the asset is expected to become obsolete relatively quickly.

Case 7–4, Concluded

• Are there any limitations on use of the leased asset? For example, leased

automobiles often have a mileage limit per year. Miles driven beyond the

limit incur additional charges.

Students may want to experiment with different assumptions and assets (such as

an automobile) using the lease versus buy calculator at http://lease-vs-buy.com/.

Case 7–5

Note to Instructors: The purpose of this activity is to familiarize students with the

procedures involved in acquiring a patent, a copyright, and a trademark. You may

want to divide the class into three groups to report back on patents, copyrights,

and trademarks separately.

The following is some information on patents, copyrights, and trademarks that

you may find helpful in your discussions.

Patent

A patent is requested by filing a written application at the relevant patent office.

The person or company filing the application is referred to as “the applicant.” The

applicant may be the inventor or its assignee. The application contains a descrip-

tion of how to make and use the invention and provides sufficient detail for a per-

son skilled in the art (i.e., the relevant area of technology) to make and use the

Case 7–5, Concluded

Copyright

While copyright in the United States automatically attaches upon the creation of

an original work of authorship, registration with the Copyright Office puts a copy-

right holder in a better position if litigation arises over the copyright. A copyright

holder desiring to register his or her copyright should do the following:

1. Obtain and complete appropriate form.

2. Prepare clear rendition of material being submitted for copyright.

3. Send both documents to U.S. Copyright Office in Washington, D.C.

Trademark

The law considers a trademark to be a form of property. Proprietary rights in rela-

tion to a trademark may be established through actual use in the marketplace, or

through registration of the mark with the trademarks office (or “trademarks regis-

try”) of a particular jurisdiction. In some jurisdictions, trademark rights can be

Case 7–6

Both Kim Jenkins (CEO) and Steve Mueller (CFO) have a responsibility for fair

and accurate reporting of financial results. Steve should remind Kim of this fact.