7-21

PROBLEM 7-36 (30 MINUTES)

1.

Break-even point in units, using the equation approach:

$24X – ($15 + $3)X – $1,800,000

=

0

300,000 units

2.

New projected sales volume

=

400,000 110%

=

$2,640,000 – $1,800,000 = $840,000

3.

Target net income = $600,000 (from original problem data)

Volume of sales dollars required:

Volume of sales dollars required

ratio margin–oncontributi

profitnet target expenses fixed

+

=

7-22

PROBLEM 7-36 (CONTINUED)

4.

Let P denote the selling price that will yield the same contribution-margin ratio:

$3 $19.50

$24

$3 $15 $24

−−

=

−−

P

P

Check: New contribution-margin ratio is:

Chapter 07 – Cost-Volume-Profit Analysis

7-23

PROBLEM 7-37 (30 MINUTES)

1. Unit contribution margin:

Sales price…………………………………

$32.00

Less variable costs:

$ 1.60

8.00

9.60

Unit contribution margin………………..

$22.40

2. Model B is more profitable when sales and production average 184,000 units.

Model A

Model B

Sales revenue (184,000 units x $32.00)………

$5,888,000

$5,888,000

Less variable costs:

$ 294,400

$ 294,400

$1,766,400

$1,472,000

Contribution margin……………………………

$4,121,600

$4,416,000

Less: Annual fixed costs……………………..

Net income………………………………………

$2,150,400

$2,188,800

3. Annual fixed costs will increase by $180,000 ($900,000 ÷ 5 years) because of

straight-line depreciation associated with the new equipment, to $2,407,200

4. Let X = volume level at which annual total costs are equal

Chapter 07 – Cost-Volume-Profit Analysis

7-24

PROBLEM 7-38 (25 MINUTES)

1. Closing of Mall store:

Loss of contribution margin at Mall Store …………………………………………….. $(108,000)

2. Promotional campaign:

3. Elimination of items sold at their variable cost:

We can restate the November 20×4 data for the Mall Store as follows:

Mall Store

Items Sold at

Their

Variable Cost

Other Items

7-25

PROBLEM 7-39 (40 MINUTES)

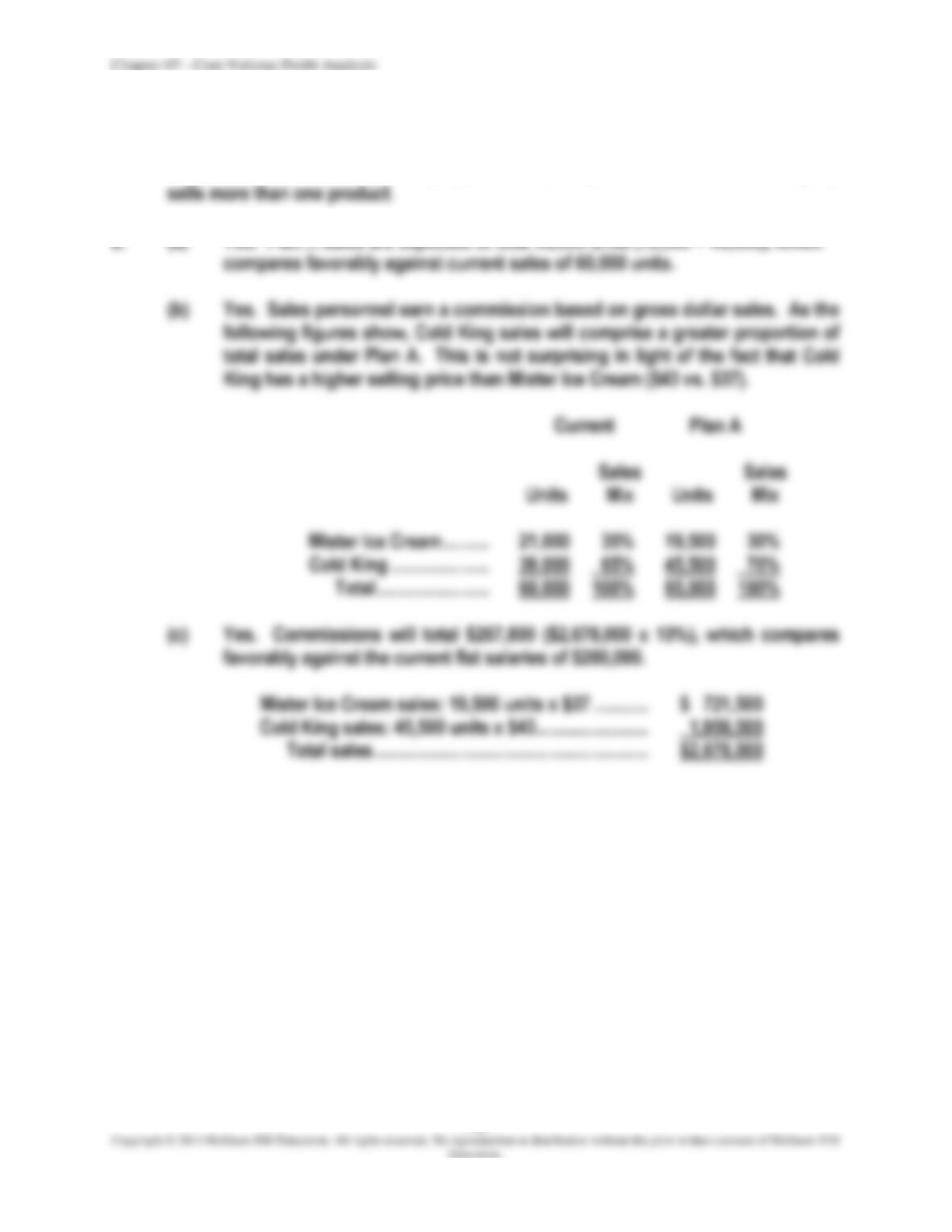

1. Sales mix refers to the relative proportion of each product sold when a company

7-26

PROBLEM 7-39 (CONTINUED)

(d) No. The company would be less profitable under the new plan.

Current

Plan A

Sales revenue:

Mister Ice Cream: 21,000 units x $37; 19,500 units x $37 …………..

$ 777,000

$ 721,500

Cold King: 39,000 units x $43; 45,500 units x $43 ……………………..

1,677,000

1,956,500

$2,454,000

$2,678,000

Less variable cost:

Mister Ice Cream: 21,000 units x $20.50; 19,500 units x $20.50 ….

$ 430,500

$ 399,750

Cold King: 39,000 units x $32.50; 45,500 units x $32.50 …………….

1,267,500

1,478,750

Sales commissions (10% of sales revenue) ……………………………..

267,800

$1,698,000

$2,146,300

Contribution margin …………………………………………………………………….

$ 756,000

$ 531,700

Less fixed cost (salaries) ……………………………………………………………..

200,000

—-___

Net income ………………………………………………………………………………….

$ 556,000

$ 531,700

3. (a) The total units sold under both plans are the same; however, the sales mix

Plan A

Plan B

Units

Sales

Mix

Units

Sales

Mix

Mister Ice Cream …………..

19,500

30%

39,000

60%

Cold King ……………………..

45,500

70%

26,000

40%

Total ………………………..

65,000

65,000

7-27

PROBLEM 7-39 (CONTINUED)

(b) Plan B is more attractive both to the sales force and to the company.

Salespeople earn more money under this arrangement ($274,950 vs.

$200,000), and the company is more profitable ($641,550 vs. $556,000).

Current

Plan B

Sales revenue:

Mister Ice Cream: 21,000 units x $37; 39,000 units x $37 …………..

$ 777,000

$1,443,000

Cold King: 39,000 units x $43; 26,000 units x $43 …………………….

$2,454,000

$2,561,000

Less variable cost:

Mister Ice Cream: 21,000 units x $20.50; 39,000 units x $20.50 ….

$ 430,500

$ 799,500

Cold King: 39,000 units x $32.50; 26,000 units x $32.50 …………….

845,000

$1,698,000

$1,644,500

Contribution margin …………………………………………………………………….

$ 756,000

$ 916,500

Less: Sales force compensation:

Flat salaries …………………………………………………………………………..

200,000

Commissions ($916,500 x 30%) ………………………………………………

274,950

Net income ………………………………………………………………………………….

$ 556,000

$ 641,550

Chapter 07 – Cost-Volume-Profit Analysis

7-28

PROBLEM 7-40 (35 MINUTES)

1. Current income:

Sales revenue………………………...

$4,032,000

Less: Variable costs…………………

$1,008,000

Net income…………………………….

$ 288,000

2. If operations are shifted to Mexico, the new unit contribution margin will be $74.40

($96.00 – $21.60). Thus:

3. (a) CompTronics desires to have a 32,000-unit break-even point with a $72 unit

contribution margin. Fixed costs must therefore drop by $432,000 ($2,736,000

– $2,304,000), as follows:

(b) As the following calculations show, CompTronics will have to generate a

contribution margin of $85.50 to produce a 32,000-unit break-even point.

Based on a $96.00 selling price, this means that the company can incur

variable costs of only $10.50 per unit. Given the current variable cost of

$24.00 ($96.00 – $72.00), a decrease of $13.50 per unit ($24.00 – $10.50) is

needed.

7-29

PROBLEM 7-40 (CONTINUED)

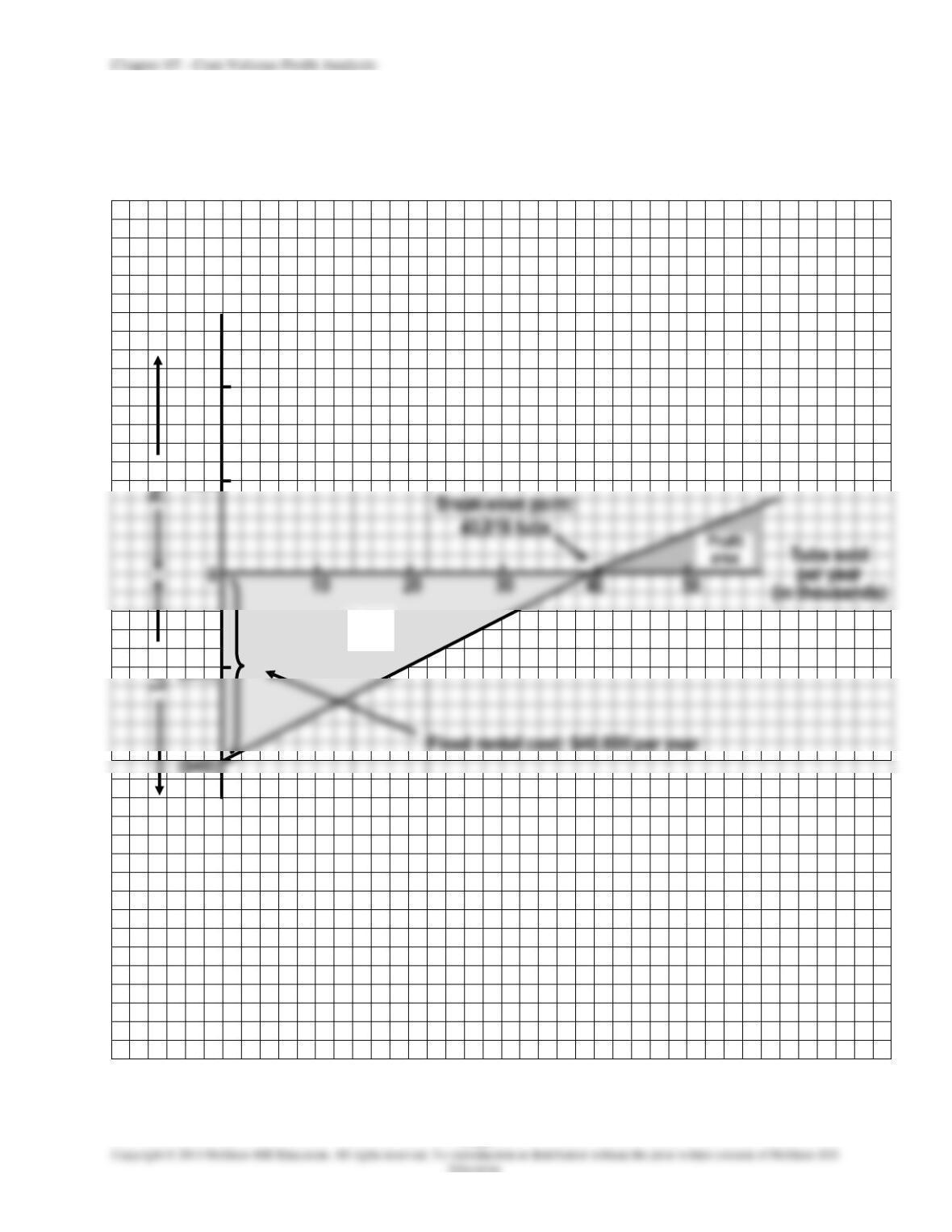

PROBLEM 7-41 (45 MINUTES)

1.

Break-even sales volume for each model:

(a)

Standard model:

(b)

Super model:

(c)

Giant model:

7-30

PROBLEM 7-41 (CONTINUED)

2. Profit-volume graph:

Dollars per year (in

thousands)

$40

$20

($20)

($40)

Loss

area

Chapter 07 – Cost-Volume-Profit Analysis

7-31

PROBLEM 7-41 (CONTINUED)

3. The sales price per tub is the same regardless of the type of machine selected.

Therefore, the same profit (or loss) will be achieved with the Standard and Super

models at the sales volume, X, where the total costs are the same.

Model

Variable Cost

per Tub

Total

Fixed Cost

Standard …………………………………………….

$2.86

$16,000

Super ………………………………………………….

2.70

22,000

Or, stated slightly differently:

Volume at which both machines

produce the same profit

aldifferenticost variable

aldifferenticost fixed

=

Check: the total cost is the same with either model if 37,500 tubs are sold.

Standard

Super

Variable cost:

Standard, 37,500 $2.86………………………

$107,250

$101,250

Fixed cost:

Standard, $16,000 ………………………………..

16,000

Super, $22,000 …………………………………….

Chapter 07 – Cost-Volume-Profit Analysis

7-32

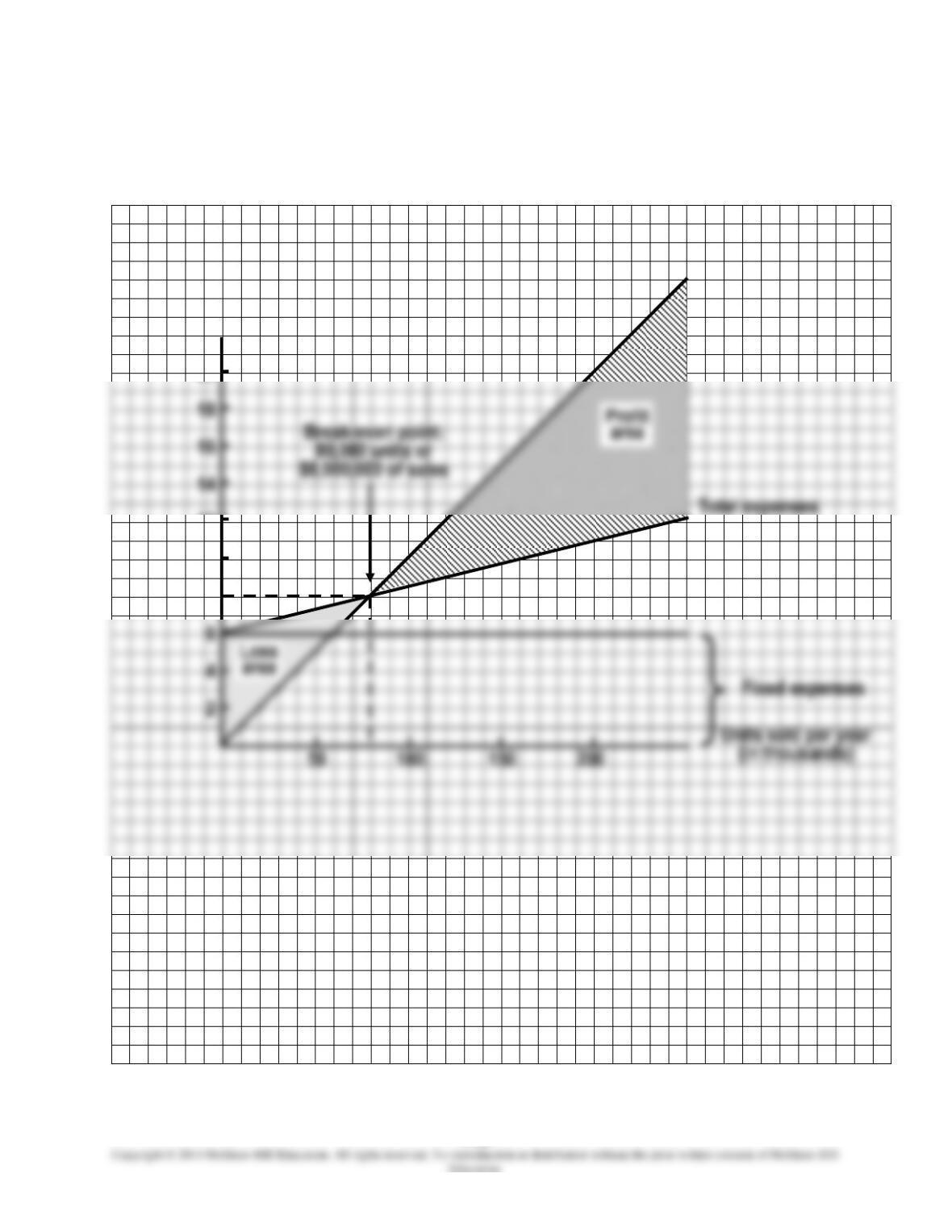

PROBLEM 7-42 (40 MINUTES)

1. CVP graph:

Total expenses

Total revenue

Fixed expenses

Units sold per year

Dollars per year

(in millions)

20

12

10

8

Chapter 07 – Cost-Volume-Profit Analysis

7-33

PROBLEM 7-42 (CONTINUED)

2.

Break-even point:

0$12,000,00

margin oncontributi

3.

Margin of safety

=

budgeted sales revenue – break-even sales revenue

=

$16,000,000 – $8,000,000 = $8,000,000

4.

Operating leverage factor

(at budgeted sales)

sales) budgeted(at incomenet

sales) budgeted(at margin oncontributi

=

5.

Dollar sales required to

earn target net profit

ratio margin–oncontributi

profitnet target expenses fixed

+

=

6.

Cost structure:

Amount

Percent

Sales revenue ……………………………………………….

$16,000,000

100.0

Variable expenses …………………………………………

4,000,000

Contribution margin ………………………………………

$12,000,000

Fixed expenses …………………………………………….

6,000,000

Chapter 07 – Cost-Volume-Profit Analysis

7-34

PROBLEM 7-43 (35 MINUTES)

1. Plan A break-even point = fixed costs ÷ unit contribution margin

Plan B break-even point = fixed costs ÷ unit contribution margin

Chapter 07 – Cost-Volume-Profit Analysis

7-35

PROBLEM 7-43 (CONTINUED)

3. Calculation of contribution margin and profit at 6,000 units of sales:

Plan A

Plan B

Sales revenue: 6,000 units x $120……………….

$720,000

$720,000

Less variable costs:

72,000

—-__

$522,000

$450,000

Contribution margin………………………………

$198,000

$270,000

Fixed costs………………………………………….

33,000

99,000

Net income………………………………………….

$165,000

$171,000

Operating leverage factor = contribution margin ÷ net income

4 & 5. Calculation of profit at 5,000 units:

Plan A

Plan B

Sales revenue: 5,000 units x $120……………….

$600,000

Less variable costs:

60,000

—- __

$435,000

$375,000

Contribution margin………………………………

$165,000

$225,000

Fixed costs…………………………………………

33,000

99,000

Net income………………………………………….

$132,000

$126,000

Cost of purchasing product:

Chapter 07 – Cost-Volume-Profit Analysis

7-36

PROBLEM 7-43 (CONTINUED)

Plan A profitability decrease:

Plan B profitability decrease:

PneumoTech would experience a larger percentage decrease in income if it adopts

6. Heavily automated manufacturers have sizable investments in plant and equipment,

along with a high percentage of fixed costs in their cost structures. As a result,

7-37

PROBLEM 7-44 (45 MINUTES)

1.

Break-even point in units:

margin oncontributiunit

costs fixed

point even–Break =

Calculation of contribution margins:

Labor-

Intensive

Production

System

Computer-

Assisted

Manufacturing

System

Selling price ………………………………..

$45.00

$45.00

Variable costs:

Direct material…………………………

$8.40

$7.50

Direct labor …………………………….

10.80

9.00

Variable overhead ……………………

7.20

4.50

Variable selling cost ………………..

3.00

(a)

Labor-intensive production system:

$750,000 $1,980,000

+

(b)

Computer-assisted manufacturing system:

$750,000 $3,660,000

+

Chapter 07 – Cost-Volume-Profit Analysis

7-38

PROBLEM 7-44 (CONTINUED)

2.

Zodiac’s management would be indifferent between the two manufacturing methods

at the volume (X) where total costs are equal.

$29.40X + $2,730,000

=

$24X + $4,410,000

=

3.

Operating leverage is the extent to which a firm’s operations employ fixed operating

costs. The greater the proportion of fixed costs used to produce a product, the

4.

Management should employ the computer-assisted manufacturing method if annual

5.

Zodiac’s management should consider many other business factors other than

operating leverage before selecting a manufacturing method. Among these are:

Chapter 07 – Cost-Volume-Profit Analysis

7-39

PROBLEM 7-45 (40 MINUTES)

1. In order to break even, during the first year of operations, 10,220 clients must visit the

law office being considered by Steven Clark and his colleagues, as the following

calculations show.

Fixed expenses:

Advertising ……………………………………………………………………. $ 980,000

Chapter 07 – Cost-Volume-Profit Analysis

7-40

PROBLEM 7-45 (CONTINUED)

Break-even point:

0 = revenue – variable cost – fixed cost

2. Safety margin:

Safety margin = budgeted sales revenue − break-even sales revenue