CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN)

VARIABLE COSTING FOR MANAGEMENT ANALYSIS

DISCUSSION QUESTIONS

1. a. Under absorption costing, both variable and fixed manufacturing costs are included as a

part of the cost of the product manufactured.

b. Under variable costing, only the variable manufacturing costs are included as a part of

the cost of the product manufactured. The fixed manufacturing costs are treated as an

expense of the period in which they are incurred.

2. Fixed factory overhead.

3. Included as part of the cost of product manufactured: (b), (d), (g).

6. All costs are controllable by someone within the business but not necessarily by the same

level of management. For a specific level of management, noncontrollable costs are costs

for which another level of management is responsible.

9. Rewarding sales personnel on the basis of total sales will normally motivate the sales staff

to expend their efforts promoting high-volume products, which will produce a large total

amount of sales dollars. In some cases, more profit may be earned by promoting specialty

products with lower sales volume but which have higher profit margins on each product

sold. For example, grocery stores must generate a large volume of sales to earn the same

profit as a jewelry store, because the profit margin for the grocery industry is low, while

the profit margin for the jewelry industry is high. A better measure of sales performance is

the total dollar contribution margin of each salesperson (total sales less variable cost of

goods sold and variable selling expenses) to overall company profit.

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

BASIC EXERCISES

BE 21–1 (FIN MAN); BE 7–1 (MAN)

a. $438,000 = $912,000 – $474,000

BE 21–2 (FIN MAN); BE 7–2 (MAN)

a. Variable costing operating income is less than absorption costing operating income

BE 21–3 (FIN MAN); BE 7–3 (MAN)

BE 21–4 (FIN MAN); BE 7–4 (MAN)

a. $52,500 greater in producing 15,000 units. 10,000 units × ($15.75* – $10.50**),

BE 21–5 (FIN MAN); BE 7–5 (MAN)

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

EXERCISES

Ex. 21–1 (FIN MAN); Ex. 7–1 (MAN)

a. The inventory valuation under the absorption costing concept would include

the fixed factory overhead cost, as follows:

21,500 units × $84* = $1,806,000

*

Direct materials ……………………………………………………………………………………………….

$30

b. The inventory valuation under the variable costing concept would not include

the fixed factory overhead cost, as follows:

21,500 units × $62* = $1,333,000

*

Direct materials ……………………………………………………………………………………………….

$30

Total ……………………………………………………………………………………………………………….

$62

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

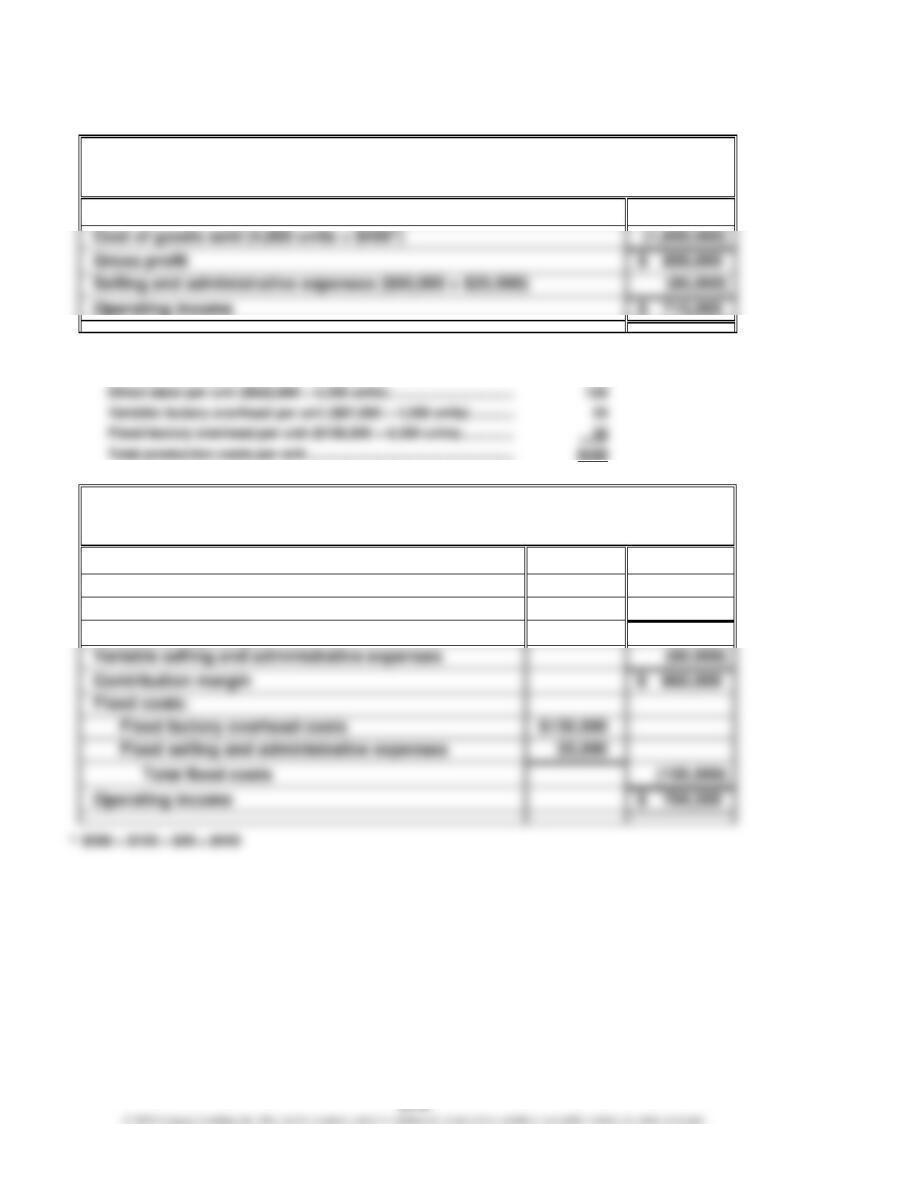

Ex. 21–2 (FIN MAN); Ex. 7–2 (MAN)

a.

Gallatin County Motors Inc.

Absorption Costing Income Statement

For the Month Ended July 31

Sales

$ 2,600,000

Gross profit

$ 800,000

Selling and administrative expenses ($60,000 + $25,000)

*

Production costs per unit:

Direct materials per unit ($1,218,000 ÷ 4,350 units) …………………..

$280

b.

Gallatin County Motors Inc.

Variable Costing Income Statement

For the Month Ended July 31

Sales

$ 2,600,000

Variable cost of goods sold

(4,000 units × $420* per unit)

(1,680,000)

Manufacturing margin

$ 920,000

Contribution margin

$ 860,000

Fixed costs:

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21–2 (FIN MAN); Ex. 7–2 (MAN) (Concluded)

c. The difference between the absorption and variable costing operating income

of $10,500 ($715,000 – $704,500) can be explained as follows:

Increase in inventory …………………………………………………………………..

350

× Fixed factory overhead per unit ………………………………………………..

× $30

Difference in operating income ……………………………………………………

$10,500

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

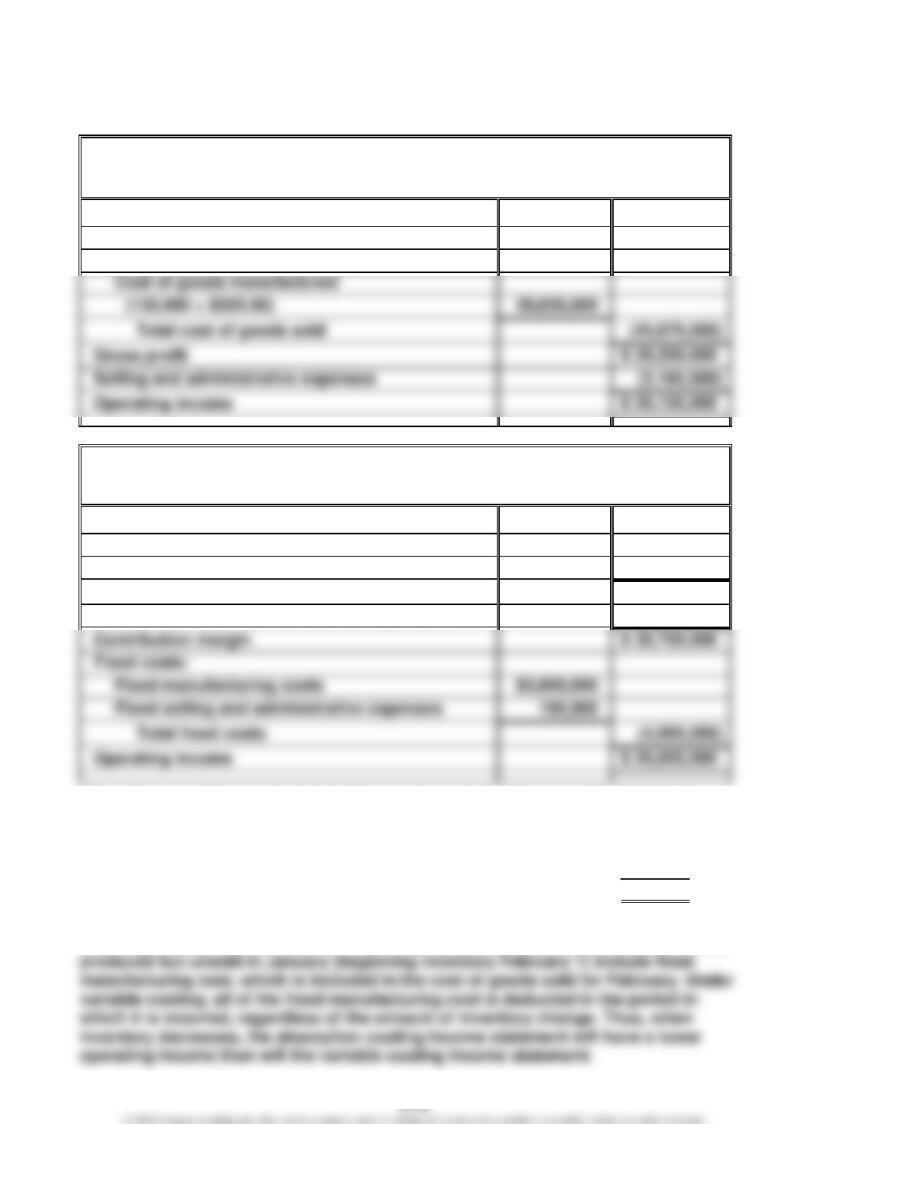

Ex. 21–3 (FIN MAN); Ex. 7–3 (MAN)

a.

Fresno Industries Inc.

Absorption Costing Income Statement

For the Month Ended February 28

Sales (150,000 × $500.00)

$ 75,000,000

Cost of goods sold:

Beginning inventory (20,000 × $301.00)

$ 6,020,000

39,650,000

(45,670,000)

Selling and administrative expenses

(3,195,000)

b.

Fresno Industries Inc.

Variable Costing Income Statement

For the Month Ended February 28

Sales

$ 75,000,000

Variable cost of goods sold

(150,000 units × $275.00 per unit)

(41,250,000)

Manufacturing margin

$ 33,750,000

Variable selling and administrative expenses

(3,000,000)

Contribution margin

Fixed costs:

Fixed manufacturing costs

$3,900,000

Operating income

c. The difference between the absorption and variable costing operating income

of $520,000 ($26,655,000 – $26,135,000) can be explained as follows:

Beginning inventory ………………………………………………………………..

20,000

Fixed manufacturing cost per unit in January …………………………...

× $26.00

Difference in operating income…………………………………………………

$520,000

Under the absorption costing concept, the fixed manufacturing cost included in the

cost of goods sold is matched with the revenues. As a result, 20,000 units that were

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

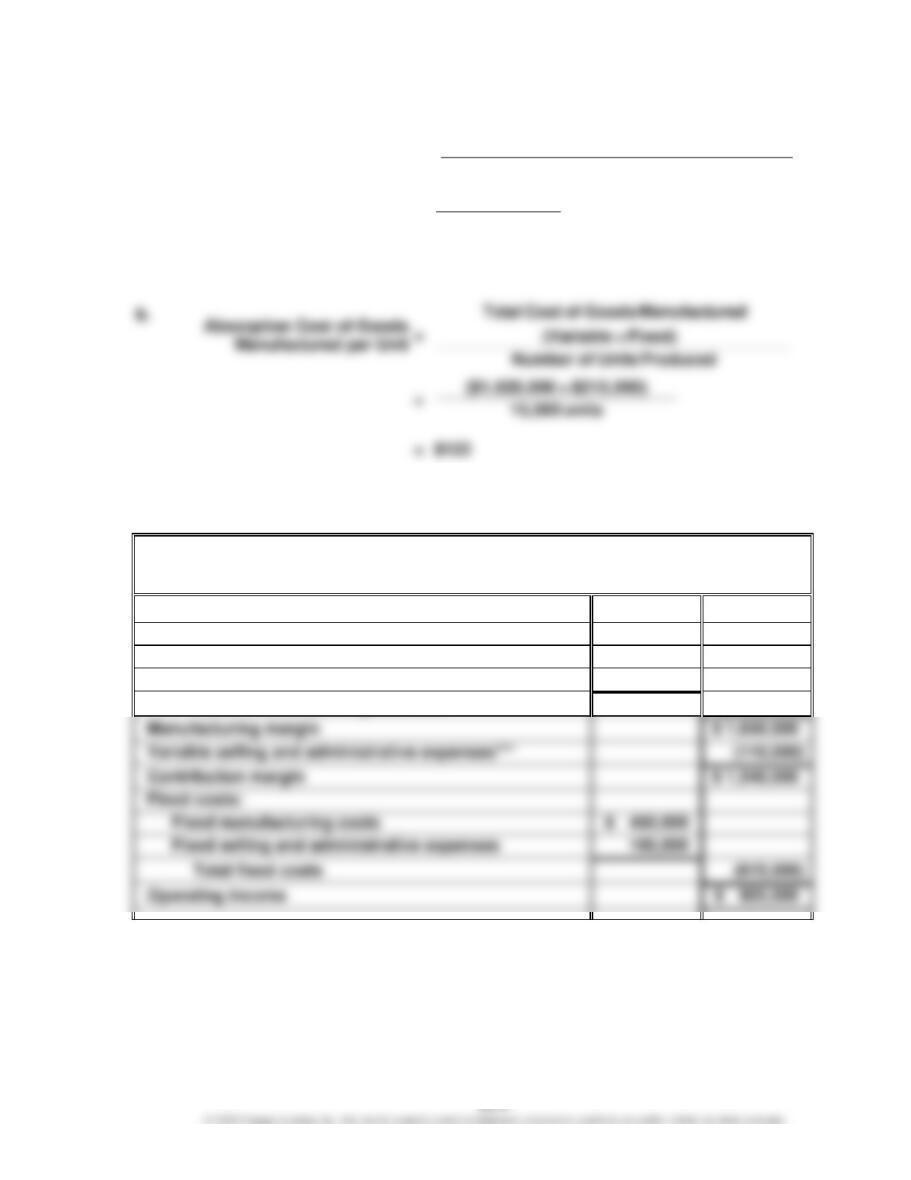

Ex. 21–4 (FIN MAN); Ex. 7–4 (MAN)

a.

Variable Cost of Goods

Manufactured per Unit

=

Variable Cost of Goods Manufactured

Number of Units Produced

=

$1,620,000

15,000 units

=

$108

Ex. 21–5 (FIN MAN); Ex. 7–5 (MAN)

Joplin Company

Variable Costing Income Statement

For the Month Ended April 30

Sales (275,000 units)

$ 4,950,000

Variable cost of goods sold:

Variable cost of goods manufactured*

$3,600,000

Inventory, April 30 (25,000 units)**

(300,000)

Total variable cost of goods sold

(3,300,000)

Variable selling and administrative expenses***

(615,000)

*

$4,050,000 – $450,000 (total manufacturing cost less fixed manufacturing cost)

**

$3,600,000 ÷ 300,000 units manufactured = $12.00;

$12.00 × 25,000 units = $300,000

***

$275,000 – $165,000 = $110,000

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21–6 (FIN MAN); Ex. 7–6 (MAN)

Maryville Equipment Company

Absorption Costing Income Statement

For the Month Ended October 31

Sales (220,000 units)

$ 7,920,000

Cost of goods sold:

Cost of goods manufactured*

$ 6,890,000

Gross profit

$ 2,200,000

Operating income

*

$6,360,000 + $530,000 (total variable plus fixed manufacturing cost)

**

$6,890,000 ÷ 265,000 units manufactured = $26 per unit; $26 × 45,000 units = $1,170,000

Ex. 21–7 (FIN MAN); Ex. 7–7 (MAN)

a.

The Procter & Gamble Company

Variable Costing Income Statement (assumed)

(in millions)

Sales

$ 65,058

Variable cost of products sold

(19,500)

Manufacturing margin

$ 45,558

Variable marketing, administrative, and other

Contribution margin

$ 31,558

Fixed costs:

(17,603)

*

$32,535 – $19,500

**

$18,568 – $14,000

b. If The Procter & Gamble Company reduced its inventories during the period, then

the cost of products sold would include fixed costs allocated to the beginning

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

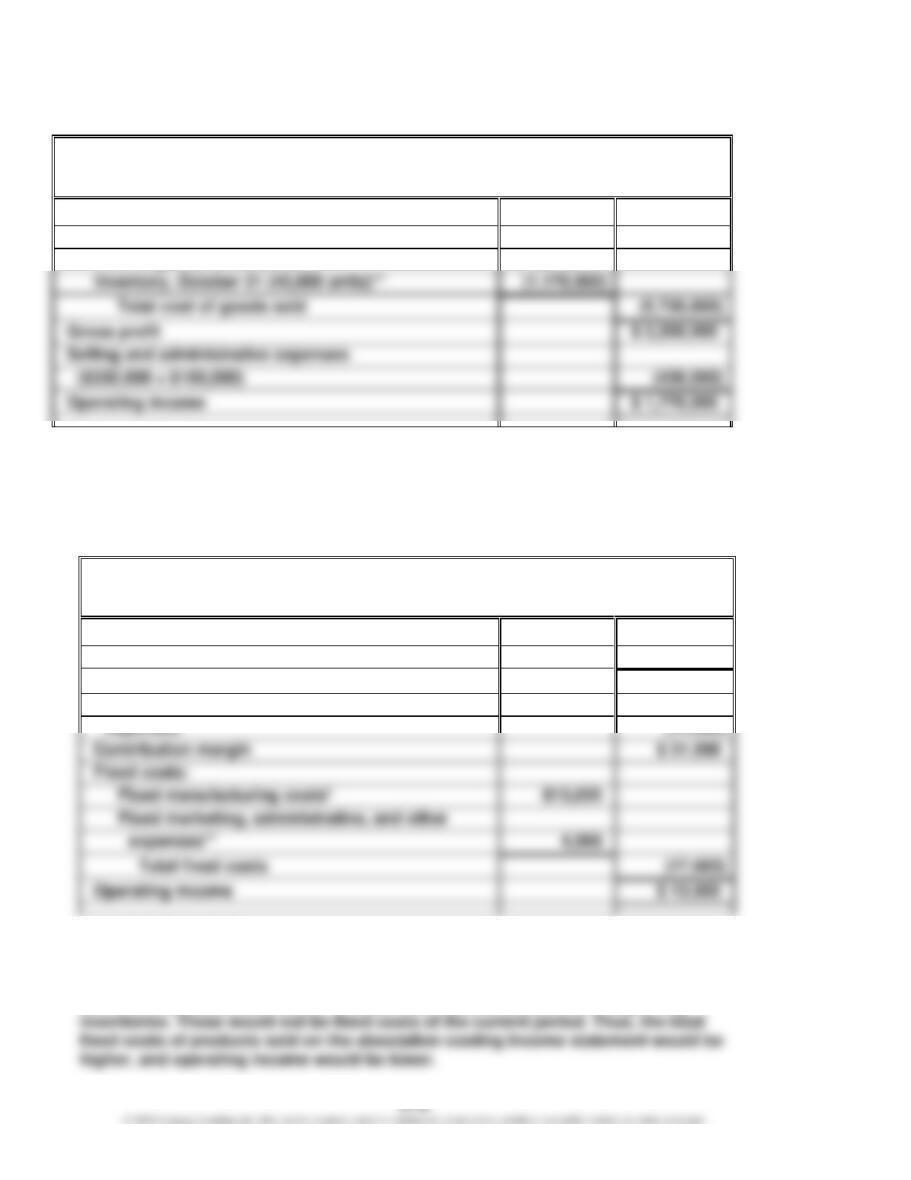

Ex. 21–8 (FIN MAN); Ex. 7–8 (MAN)

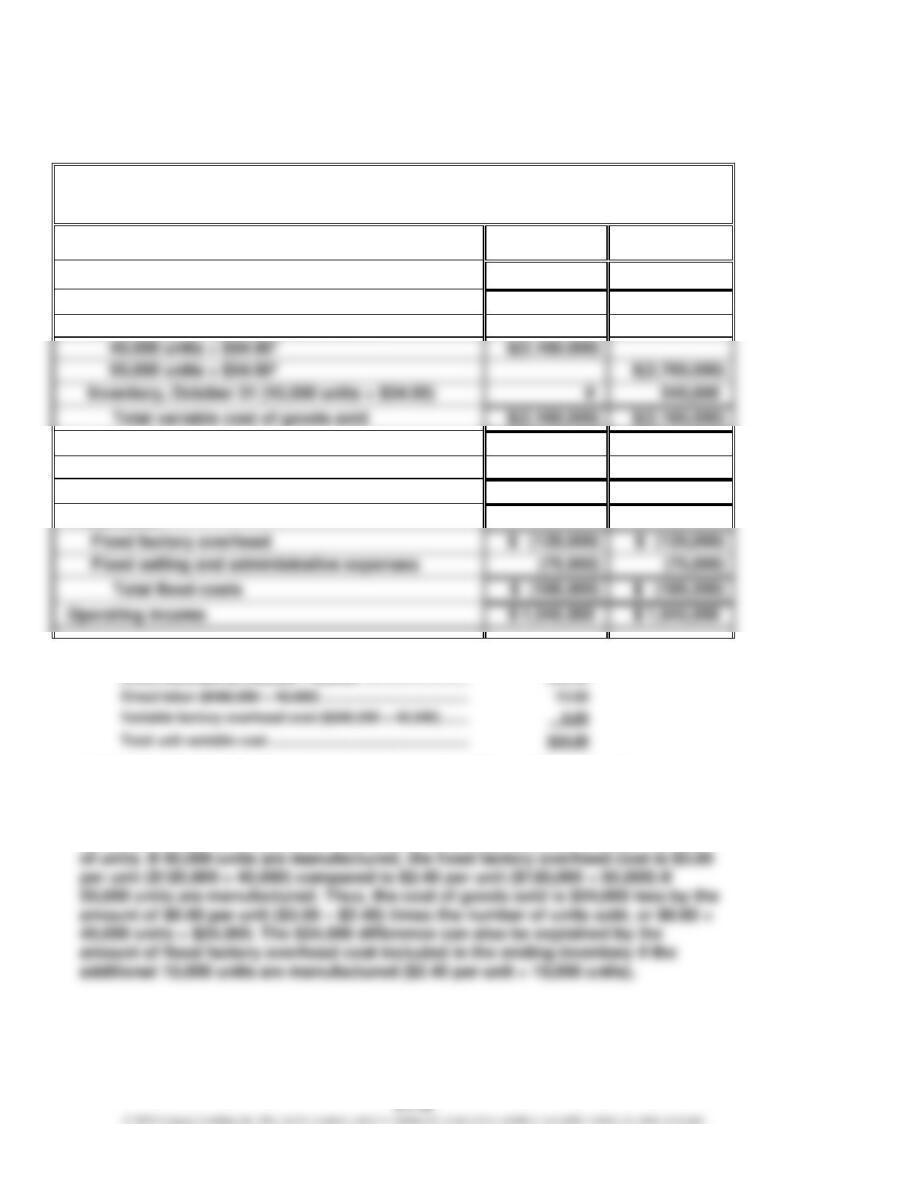

a. 1.

Marshall Inc.

Absorption Costing Income Statement

For the Month Ending October 31

40,000 Units

Manufactured

50,000 Units

Manufactured

Sales

$ 3,600,000

$ 3,600,000

Cost of goods sold:

Cost of goods manufactured:

40,000 units × $57.00*

$(2,280,000)

Inventory, October 31 (10,000 units × $56.40)

Total cost of goods sold

$(2,280,000)

Gross profit

Selling and administrative expenses

*

Unit cost of goods manufactured:

Direct materials ($1,440,000 ÷ 40,000) ………………………………

$36.00

Direct labor ($480,000 ÷ 40,000) ……………………………………….

12.00

Variable factory overhead cost ($240,000 ÷ 40,000) …………..

6.00

Fixed factory overhead cost ($120,000 ÷ 40,000) ………………

3.00

Unit cost of goods manufactured:

Direct materials ………………………………………………………………

Direct labor …………………………..………………………………………..

Fixed factory overhead cost ($120,000 ÷ 50,000) ………………

Total unit cost …………………………………………………………………

$57.00

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21–8 (FIN MAN); Ex. 7–8 (MAN) (Concluded)

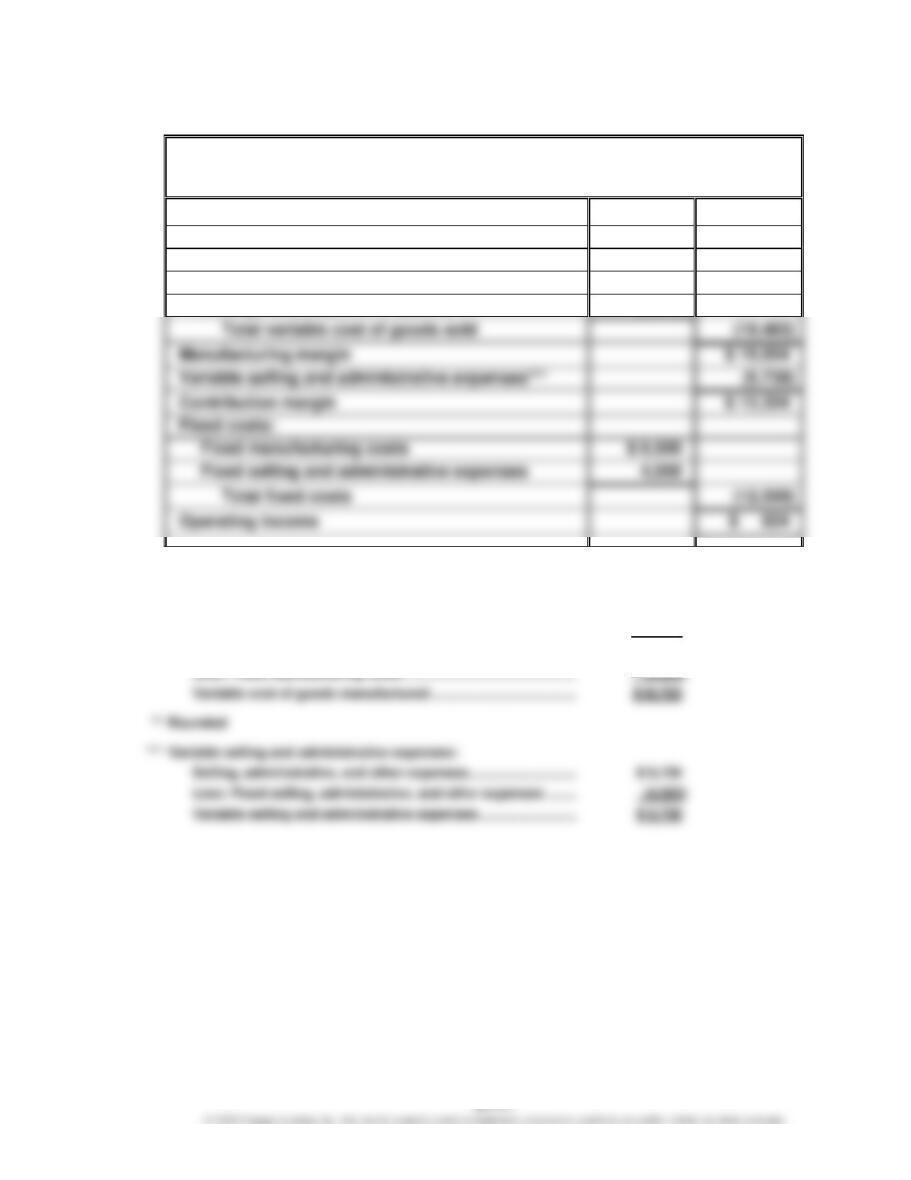

2.

Marshall Inc.

Variable Costing Income Statement

For the Month Ending October 31

40,000 Units

Manufactured

50,000 Units

Manufactured

Sales

$ 3,600,000

$ 3,600,000

Variable cost of goods sold:

Variable cost of goods manufactured:

Inventory, October 31 (10,000 units × $54.00)

Manufacturing margin

$ 1,440,000

$ 1,440,000

Variable selling and administrative expenses**

(200,000)

(200,000)

Contribution margin

$ 1,240,000

$ 1,240,000

Fixed costs:

*

Unit variable cost of goods manufactured:

**

Variable selling and administrative expenses are constant with constant sales levels.

b. If 50,000 units rather than 40,000 units are manufactured, the increase in operating

income of $24,000 ($1,069,000 – $1,045,000) under absorption costing is caused

by the allocation of $120,000 of fixed factory overhead cost over a larger number

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21–9 (FIN MAN); Ex. 7–9 (MAN)

a.

Caterpillar Inc.

Variable Costing Income Statement (assumed)

For Year Ended December 31

Sales

$ 38,537

Variable cost of goods sold:

Beginning inventory (70% × $9,700)

$ 6,790

Variable cost of goods manufactured*

18,723

Ending inventory (70% × $8,614)**

(6,030)

Contribution margin

Fixed costs:

Fixed manufacturing costs

$ 8,500

Fixed selling and administrative expenses

*

Variable cost of goods manufactured:

Cost of goods sold …………………………………………………………….

$28,309

Plus: Ending inventory ………………………………………………………

8,614

Less: Beginning inventory …………………………………………………

(9,700)

Cost of goods manufactured ……………………………………………..

$27,223

Variable cost of goods manufactured …………………………………

Variable selling and administrative expenses:

Selling, administrative, and other expenses ………………………..

Less: Fixed selling, administrative, and other expenses ……..

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21–9 (FIN MAN); Ex. 7–9 (MAN) (Concluded)

b. The operating income under the variable costing concept will not be the same as

the operating income under the absorption costing concept when the inventories

either increase or decrease during the year. In this case, Caterpillar’s inventory

decreased, meaning it sold more than it manufactured. As a result, the operating

income under the variable costing concept will be more than the operating income

The difference between the operating income under the two concepts can be shown

as follows (rounded):

Fixed cost portion of January 1 inventory (30% × $9,700) …………………..

$ 2,910

Less: Fixed cost portion of December 31 inventory (30% × $8,614)* ……

(2,584)

Operating income—absorption costing …………………………………………….

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21–10 (FIN MAN); Ex. 7–10 (MAN)

a. Management’s decision and conclusion are incorrect. The profit will not be improved

by $756,000 because the fixed costs used in manufacturing and selling running shoes

will not be avoided if the line is eliminated. These fixed costs total $1,386,000 for the

used for making this type of decision.

b.

Winslow Inc.

Variable Costing Income Statements—Three Product Lines

For the Year Ended December 31

Cross Training

Shoes

Golf

Shoes

Running

Shoes

Revenues

$ 5,800,000

$ 6,900,000

$ 4,200,000

Variable cost of goods sold*

(2,088,000)

(2,484,000)

(2,016,000)

Manufacturing margin

$ 3,712,000

$ 4,416,000

$ 2,184,000

Variable selling and administrative

Contribution margin

Fixed costs:

expenses**

(1,740,000)

(1,656,000)

(1,554,000)

*

Cross Training: $3,016,000 – $928,000; Golf Shoes: $3,381,000 – $897,000;

Running Shoes: $2,814,000 – $798,000

**

Cross Training: $2,436,000 – $696,000; Golf Shoes: $2,484,000 – $828,000;

Running Shoes: $2,142,000 – $588,000

c. If the running shoe line were eliminated, then the contribution margin of the product

line also would be eliminated. The fixed costs would not be eliminated. Thus, the

profit of the company would actually decline by $630,000. Management should keep

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21–11 (FIN MAN); Ex. 7–11 (MAN)

Sun Sound

Headphones

Ear Bling

Headphones

Unit volume increase ……………………………………………………….

28,000

30,000

× Contribution margin per unit………………………………………….

× $33.60

× $30.00

Increase in profitability …………………………………………………….

$940,800

$900,000

The increase in total profitability would be $1,840,800 ($940,800 + $900,000). Note that

Ex. 21–12 (FIN MAN); Ex. 7–12 (MAN)

a.

Galaxy Sports Inc.

Contribution Margin by Product

Conquistador

Hurricane

Sales

$ 60,000,000

$ 46,000,000

$ 15,000,000

$ 18,400,000

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21–13 (FIN MAN); Ex. 7–13 (MAN)

a.

Coast to Coast Surfboards Inc.

Contribution Margin by Territory

East Coast

West Coast

Sales

$ 8,000,000

$ 8,000,000

Variable cost of goods sold

(6,000,000)

(6,000,000)

Contribution margin

b. The total contribution margin is slightly lower for the East Coast, while the

contribution margin ratio is slightly higher for the West Coast. This is because East

Coast sells only Atlantic Waves, which have a lower contribution margin ratio (8.0%

vs. 11.7%)* but a higher contribution margin per unit ($16 vs. $14). In attempting to

improve the company’s profitability, it is unlikely that changing the mix of products

to the two territories will have much effect. East Coast will sell very few Pacific

* 8.0% = $16 ÷ $200

11.7% = $14 ÷ $120, rounded to one decimal place

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21–14 (FIN MAN); Ex. 7–14 (MAN)

a.

1.

Havasu Off-Road Inc.

Contribution Margin by Salesperson

Rene

Steve

Colleen

Paul

Sales

$ 558,000

$ 384,000

$ 560,000

$1,080,000

Variable cost of goods sold

(334,800)

(192,000)

(336,000)

(540,000)

Variable commission

Manufacturing margin

$ 223,200

$ 192,000

$ 224,000

$ 540,000

2. Paul earns the highest contribution margin and has the highest contribution margin

ratio. This is because he sells the most units, has a low commission rate, and sells a

product mix with a high manufacturing margin (50% of sales, $540,000 ÷ $1,080,000).

Steve also sells products with a high average manufacturing margin (50% of sales,

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21–14 (FIN MAN); Ex. 7–14 (MAN) (Concluded)

b.

1.

Havasu Off-Road Inc.

Contribution Margin by Territory

Northeast

Southwest

Sales

$ 942,000

$1,640,000

Variable cost of goods sold

(526,800)

(876,000)

Contribution margin

2. The Southwest Region has $698,000 more sales and $297,120 more contribution

margin. In addition, the Southwest Region has the largest contribution margin

ratio. In the Southwest Region, the salesperson with the highest sales unit

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21-15 (FIN MAN); Ex. 7-15 (MAN)

a.

Caterpillar Inc.

Contribution Margin by Segment (assumed)

(in millions, except ratio figures)

Building

Construction

Products

Cat Japan

Core

Components

Earth moving

Electric

Power

Excavation

Large

Power

Systems

Logistics

Marine &

Petroleum

Power

Mining

Turbines

Sales

$2,217.00

$1,225.00

$1,234.00

$ 5,045.00

$ 2,847.00

$ 4,562.00

$ 2,885.00

$ 659.00

$2,132.00

$ 3,975.00

$3,321.00

Variable cost of goods sold

(997.65)

(673.75)

(604.66)

(2,572.95)

(1,537.38)

(2,372.24)

(1,529.05)

(329.50)

(1,066.00)

(2,067.00)

(1,594.08)

Manufacturing margin

$1,219.35

$ 551.25

$ 629.34

$ 2,472.05

$ 1,309.62

$ 2,189.76

$ 1,355.95

$ 329.50

$1,066.00

$ 1,908.00

$ 1,726.92

Variable promotion expenses

(310.00)

(120.00)

(150.00)

(600.00)

(600.00)

(270.00)

(480.00)

Variable selling expenses

$ (509.53)

$ (254.75)

$(1,003.60)

$ (484.70)

$ (873.72)

$ (461.88)

$ (758.25)

$ (698.89)

Contribution margin

$ 709.82

$ 296.50

$ 1,468.45

$ 824.92

$ 1,316.04

$ 188.60

$ 1,149.75

$ 1,028.03

Contribution margin ratio

Building

Construction

Products

Cat Japan

Core

Components

Earth moving

Electric

Power

Excavation

Large

Power

Systems

Logistics

Marine &

Power

Mining

Turbines

Manufacturing margin

47.0%

Dealer commissions

Variable promotion

(10.4)%

Contribution margin ratio

31.6%

Dealer commissions

$ (199.53)

$ (134.75)

$ (98.72)

$ (403.60)

$ (284.70)

$ (273.72)

$ (144.25)

$ (65.90)

$ (191.88)

$ (278.25)

$ (298.89)

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21–15 (FIN MAN); Ex. 7–15 (MAN) (Concluded)

c. The Building Construction Products segment has the highest contribution margin

ratio. The manufacturing margin is high, while the dealer commission rate is average.

The variable promotion expenses as a percent of sales is higher than average. Cat

Japan is the poorest performing segment in terms of contribution margin ratio. This

is because the manufacturing margin is the lowest and dealer commissions are the

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21–16 (FIN MAN); Ex. 7–16 (MAN)

a.

Turner

Home Box Office

Warner Bros.

Revenues ……………………………….

$11,364

$ 5,890

$13,037

Variable costs …………………………

(4,546)

(2,062)

(3,259)

b. The higher contribution margin ratio of Warner Bros. segment of 75% in part (a)

should not be interpreted that it is the most profitable segment. The fixed costs