EXERCISE 7-11

(a) Deposits in transit = $74,000 – ($71,000 – $4,800) = $7,800

(c) PERTH INC.

Bank Reconciliation

August 31, 2017

Cash balance per bank statement ………………….. $20,692*

Add: Deposits in transit ……………………………….. 7,800

28,492

(d) Aug. 31 Cash …………………………………………………… 45

Interest Revenue ………………………….. 45

EXERCISE 7-12

(a) Cash and Cash Equivalents

2. U.S. Treasury bill …………………………………………………….. 10,000

5. Checking account …………………………………………………… 2,500

(b) 4. Post-dated check—Accounts Receivable; Balance Sheet

7. Prepaid postage in postage meter—Prepaid Postage Expense; Balance

EXERCISE 7-13

Suggestions to improve cash management practices for Lance, Art and

Wayne:

2. Bill clients as work progresses.

4. Arrange a long-term loan for renovations and equipment and plan the

EXERCISE 7-14

RIGLEY COMPANY

Cash Budget

For the Two Months Ending February 28, 2017

January February

Beginning cash balance ………………………………….. $ 46,000 $ 24,000

Add: Cash receipts

Collections from customers ………………….. 71,000 146,000

Less: Cash disbursements

Payments to suppliers …………………………... 40,000 75,000

Wages ………………………………………………….. 30,000 40,000

Excess (deficiency) of available cash over

disbursements ……………………………………………… 24,000 12,000

Financing

*EXERCISE 7-15

Oct. 1 Petty Cash ………………………………………………… 150.00

Cash ………………………………………………….. 150.00

31 Petty Cash ………………………………………………… 50.00

Postage Expense …………………………..………….. 39.70

*EXERCISE 7-16

(a) Aug. 1 Petty Cash …………………………………………. 200.00

Cash …………………………………………… 200.00

15 Freight-Out ………………………………………… 74.40

16 Petty Cash …………………………………………. 200.00

Cash …………………………………………… 200.00

31 Postage Expense ……………………………….. 145.00

(b)

Petty Cash

8/31 Bal. 400

8/1 200

*EXERCISE 7-16 (Continued)

(c) The internal control features of a petty cash fund include:

(1) A custodian is responsible for the fund.

(2) A pre-numbered petty cash receipt signed by the custodian and

(3) The treasurer’s office examines all payments and stamps

(4) Surprise counts can be made at any time to determine whether

SOLUTIONS TO PROBLEMS

PROBLEM 7-1A

(a)

Principles

Application to Gary Theater

Establishment of responsibility.

Only cashiers are authorized to sell

tickets. Only the manager and cashier

can handle cash.

Segregation of duties.

The manager maintains custody of the

cash, and the company accountant

records the cash.

The duties of receiving cash and

admitting customers are assigned to

Documentation procedures.

Tickets are prenumbered. Cash count

sheets are prepared. Deposit slips are

prepared.

Physical controls.

A safe is used for the storage of cash

and a machine is used to issue tickets.

comparisons are made by the company

Human resource controls.

Cashiers are bonded.

(b) Actions by the doorperson and cashier to misappropriate cash include:

(1) Instead of tearing the tickets, the doorperson could return the

(2) The cashier could issue a lower price ticket than paid for and the

doorperson would admit the customer. The difference between the

PROBLEM 7-2A

Grant has created a situation that leaves many opportunities for

undetected theft. Here is a list of some of the weaknesses in internal

control. You may find others.

1. Documentation procedures. The tickets were unnumbered. By num-

2. Physical controls and establishment of responsibility. The tickets were

3. Documentation procedures. No record was kept of which students

took tickets to sell or how many they took. In combination with items 1

4. Documentation procedures. There was no control over unsold tickets.

This deficiency made it possible for students to sell tickets, keep the

5. Establishment of responsibility. Inadequate control over the cash box.

6. Documentation procedures. Instead of receipts, students simply wrote

PROBLEM 7-2A (Continued)

7. Segregation of duties. Lynn Dandi counted the funds, made out the

deposit slip, and took the funds to the bank. This made it possible for

8. Documentation procedures. Grant did not receive a receipt from Kray

9. Segregation of duties. Dana Uhler was collecting tickets and receiving

PROBLEM 7-3A

(a) KEEDS COMPANY

Bank Reconciliation

July 31, 2017

Cash balance per bank statement ………………… $7,690.80

Add: Deposits in transit …………………………….. 1,193.30

8,884.10

Less: NSF check ………………………………………… $575.00

Error in recording check No. 2480 ……… 36.00

(b) July 31 Cash ……………………………………………. 1,520

Accounts Receivable …………….. 1,520

31 Accounts Receivable—W. Krueger … 575

Cash …………………………………….. 575

PROBLEM 7-4A

(a) BOGALUSA COMPANY

Bank Reconciliation

November 30, 2017

Cash Balance per bank statement ……………. $17,712.50

Add: Deposits in transit ………………………… 1,304.00

19,016.50

Less: Outstanding checks

No. 2451 ……………………………………. $1,260.40

No. 2472 ……………………………………. 426.80

No. 2478 ……………………………………. 538.20

Cash Balance per books………………………….. $11,073.80

Add: Electronic funds

PROBLEM 7-4A (Continued)

(b) Nov. 30 Cash ………………………………………………… 2,242

Accounts Receivable …………………. 2,242

PROBLEM 7-5A

(a) TIMMINS COMPANY

Bank Reconciliation

May 31, 2017

Cash balance per bank statement ……………….. $6,968.00

Add: Deposits in transit ……………………………. $1,880.15

Bank error—Tomins …………………………. 360.00 2,240.15

9,208.15

Less: Outstanding checks ………………………….. 276.25

Less: NSF check ……………………………………….. $ 380.00

Error in May 12 deposit …………………….. 50.00

(b) May 31 Cash …………………………………………… 2,690

Notes Receivable ………………….. 2,690

31 Accounts Receivable—

S. Ballard ………………………………….. 380

Cash …………………………………….. 380

PROBLEM 7-6A

(a) DAISEY COMPANY

Bank Reconciliation

October 31, 2017

Balance per bank statement ……………………………………….. $18,380.00

Less: Outstanding checks

No.

Amount

No.

Amount

62

$140.75

862

$190.71

(b) The cashier attempted to cover the theft of $1,044.00 by:

$140.75; No. 183, $180.00; and No. 284, $253.25).

3. Subtracting the $185 credit from the bank balance instead of adding

(c) 1. The principle of independent internal verification has been violated

because the cashier prepared the bank reconciliation.

2. The principle of segregation of duties has been violated because

PROBLEM 7-7A

MOTNAHAN INC.

Cash Budget

For the Month Ending April 30, 2017

Beginning cash balance ………………………………………. $11,000

Add: Cash receipts

Cash sales ……………………………………………….. 42,000

Collections from customers ………………………. 18,400

Less: Cash disbursements

Payment of March purchases ……………………. 22,400

April cash purchases ………………………………… 28,100

PROBLEM 7-8A

BASTILLE CORPORATION

Cash Budget

For the Two Months Ending February 28, 2017

January February

Beginning cash balance …………………………………. $ 46,000 $ 43,000

Add: Cash receipts

Collections from customers ………………….. 326,000 378,000

Less: Cash disbursements

Purchases ……………………………………………. 110,000 135,000

Salaries ………………………………………………… 84,000 81,000

Administrative expenses (Jan. $72,000 –

$1,000; Feb. $75,000 – $1,000) …………….. 71,000 74,000

ACCOUNTING CYCLE REVIEW

(a)

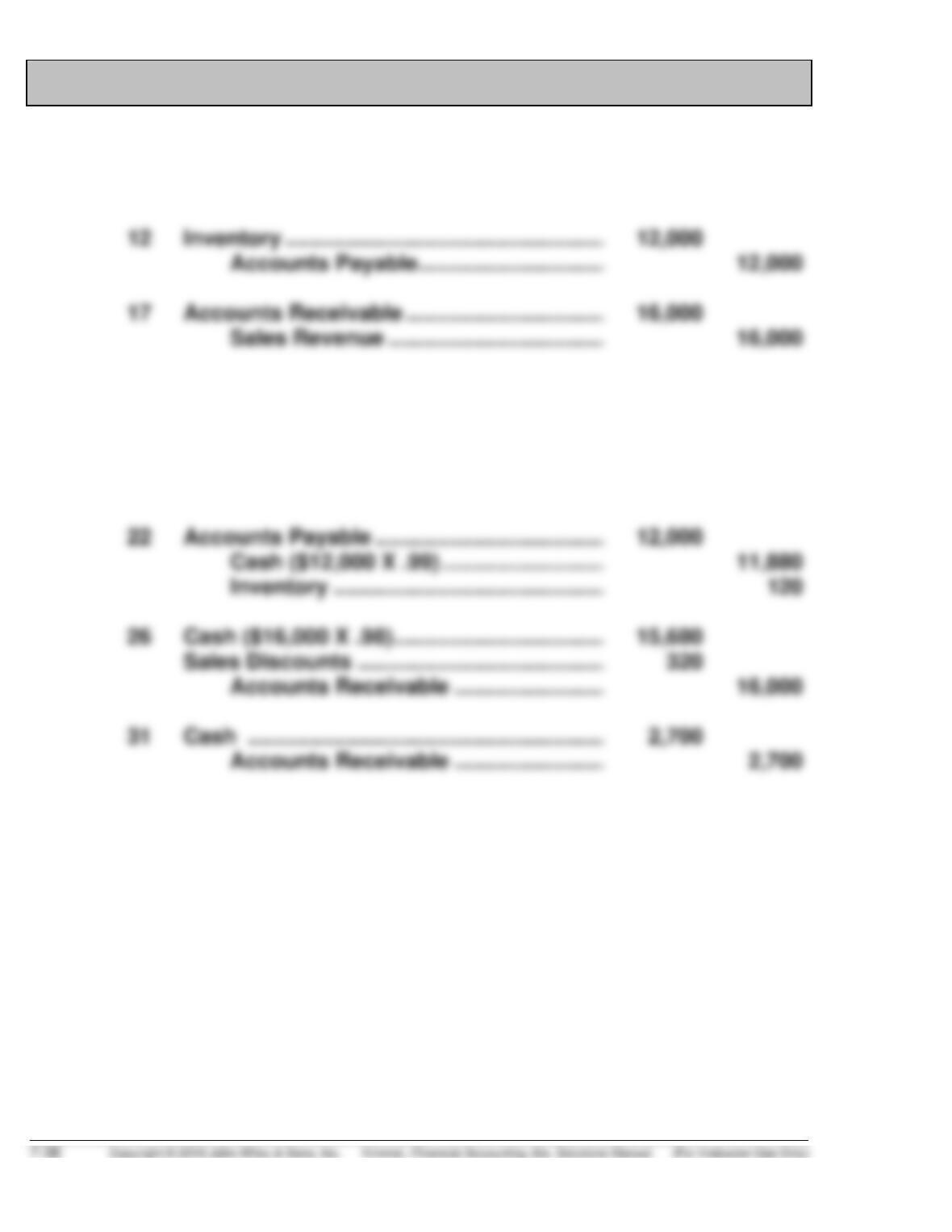

Dec. 7

Cash …………………………………………………….

Accounts Receivable ……………………..

3,600

3,600

12

Inventory ………………………………………………

Accounts Payable …………………………..

12,000

12,000

Cost of Goods Sold ……………………………….

Inventory ……………………………………….

10,000

10,000

19

Salaries and Wages Expense …………………

Cash ………………………………………………

2,200

2,200

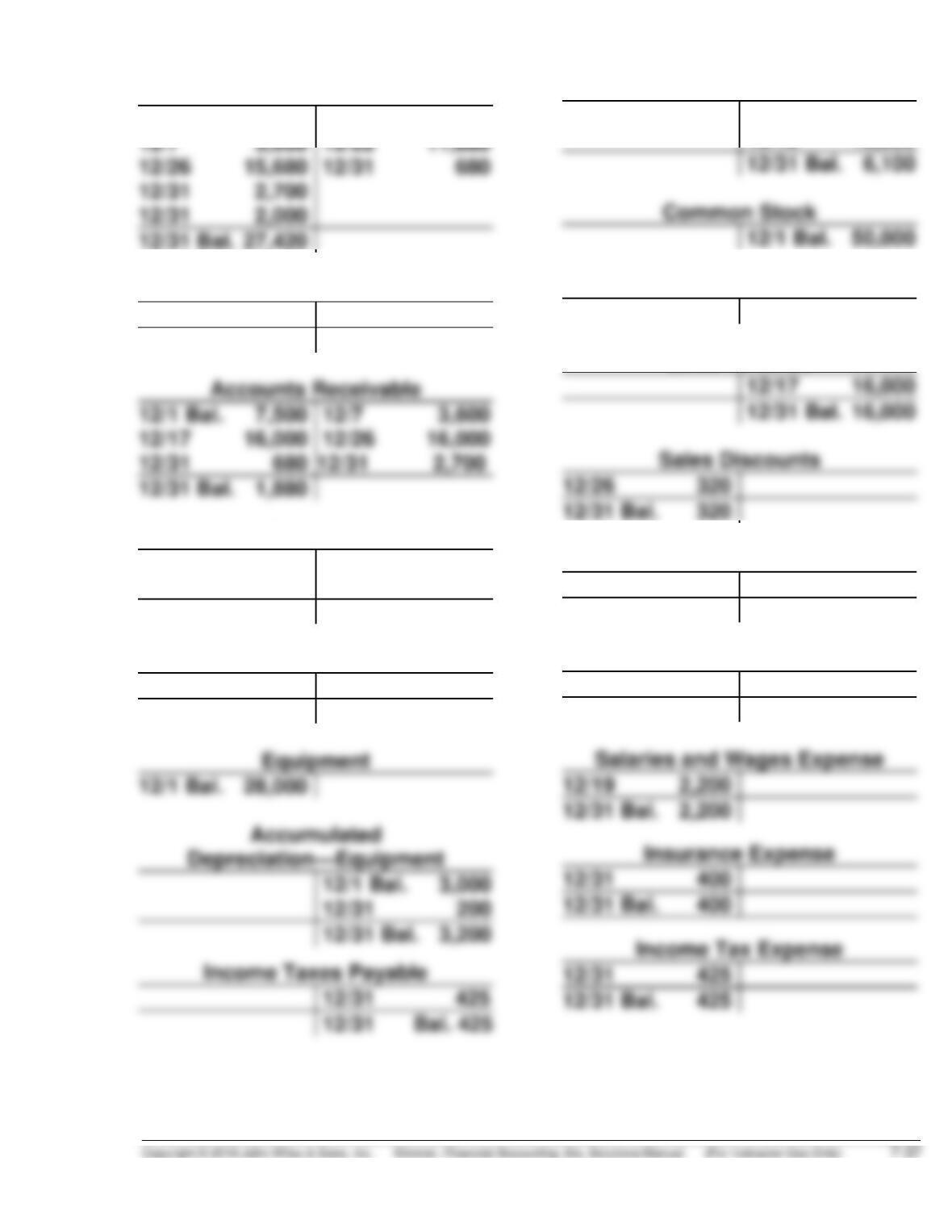

Accounts Receivable ……………………..

Cash

12/31 Bal. 27,420

12/31 Bal. 6,100

12/1 Bal. 50,000

12/1 Bal. 18,200

12/19 2,200

Notes Receivable

12/1 Bal. 2,000

12/31 2,000

12/31 Bal. – 0 –

12/31 Bal. 1,880

12/17 16,000

12/31 Bal. 16,000

12/26 320

12/31 Bal. 320

Inventory

12/1 Bal. 16,000

12/12 12,000

12/17 10,000

12/22 120

12/31 Bal. 17,880

Prepaid Insurance

12/1 Bal. 1,600

12/31 400

12/31 Bal. 1,200

12/1 Bal. 28,000

12/31 Bal. 3,200

12/31 425

12/19 2,200

12/31 Bal. 2,200

12/31 400

12/31 Bal. 400

12/31 425

12/31 Bal. 425

Accounts Payable

12/22 12,000

12/1 Bal. 6,100

12/12 12,000

Retained Earnings

12/1 Bal. 14,200

Sales Revenue

Cost of Goods Sold

12/17 10,000

12/31 Bal. 10,000

Depreciation Expense

12/31 200

12/31 Bal. 200

ACR SOLUTION (Continued)

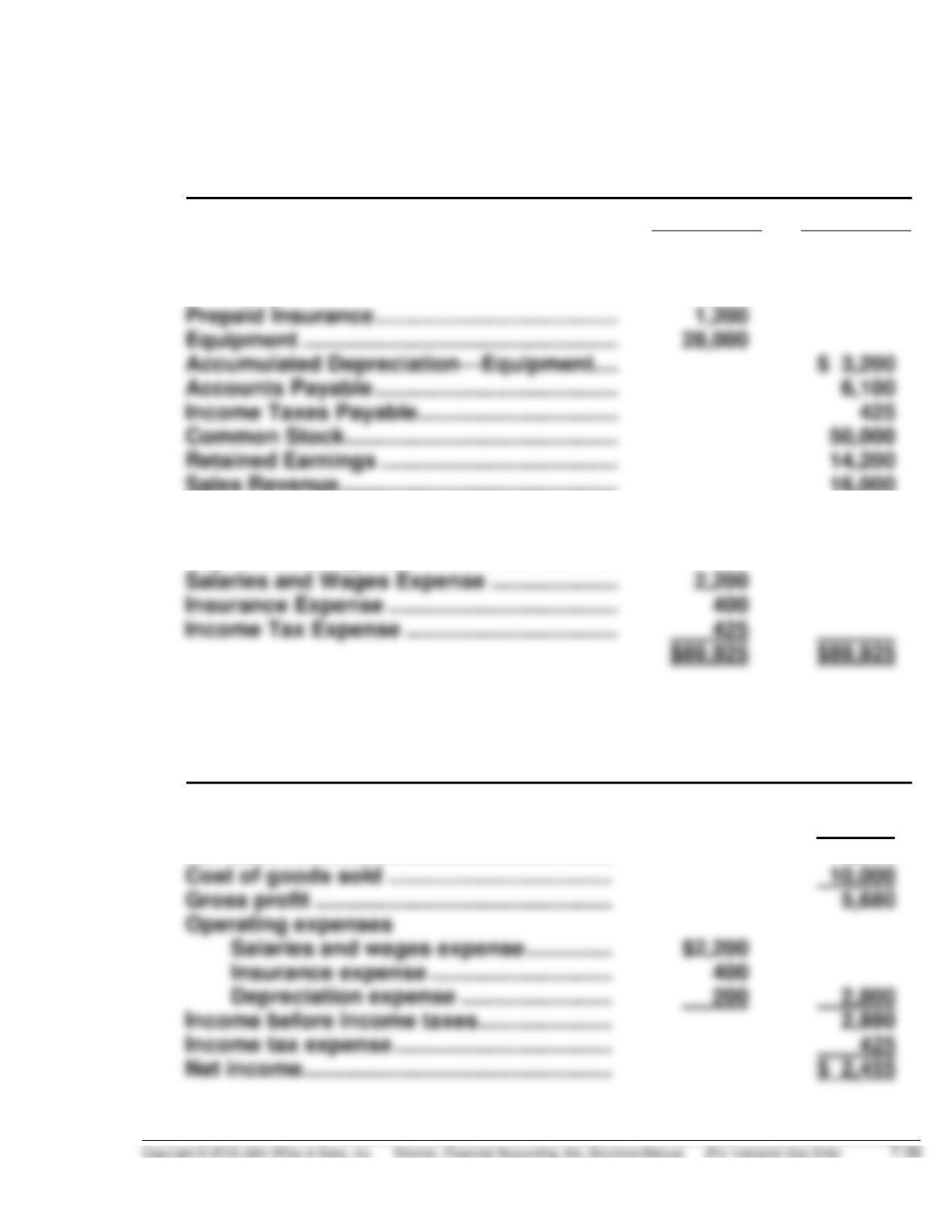

(c) HAVENHILL COMPANY

Bank Reconciliation

December 31, 2017

Cash balance per bank statement …………………….. $25,930

Add: Deposits in transit ……………………………………. 2,700

28,630

(d) Dec. 31 Cash ………………………………………………….. 2,000

Notes Receivable …………………………. 2,000

31 Accounts Receivable ………………………….. 680

Cash ……………………………………………. 680

31 Depreciation Expense ………………………… 200

ACR SOLUTION (Continued)

(f) HAVENHILL COMPANY

Adjusted Trial Balance

December 31, 2017

DR.

CR.

Cash ……………………………………………………..

$27,420

Accounts Receivable ……………………………..

1,880

Inventory ……………………………………………….

17,880

Prepaid Insurance ………………………………….

Equipment …………………………………………….

28,000

Accumulated Depreciation—Equipment ….

Accounts Payable ………………………………….

Income Taxes Payable …………………………...

Common Stock ………………………………………

50,000

Retained Earnings …………………………………

Sales Revenue ……………………………………….

16,000

Sales Discounts …………………………………….

320

Cost of Goods Sold ……………………………….

10,000

Depreciation Expense …………………………...

200

Salaries and Wages Expense …………………

2,200

Insurance Expense ………………………………..

Income Tax Expense ……………………………..

(g) HAVENHILL COMPANY

Income Statement

For the Month Ending December 31, 2017

Sales revenue ………………………………………..

$16,000

Less: Sales discounts …………………………..

320

Net sales ……………………………………………….

15,680

Cost of goods sold ………………………………..

Gross profit …………………………………………..

Operating expenses

Salaries and wages expense ……………

Insurance expense ………………………….

400

Depreciation expense ……………………..

2,800

Income before income taxes …………………..

Income tax expense ……………………………….

425