CHAPTER 7 Inventories

Prob. 7-2B (Concluded)

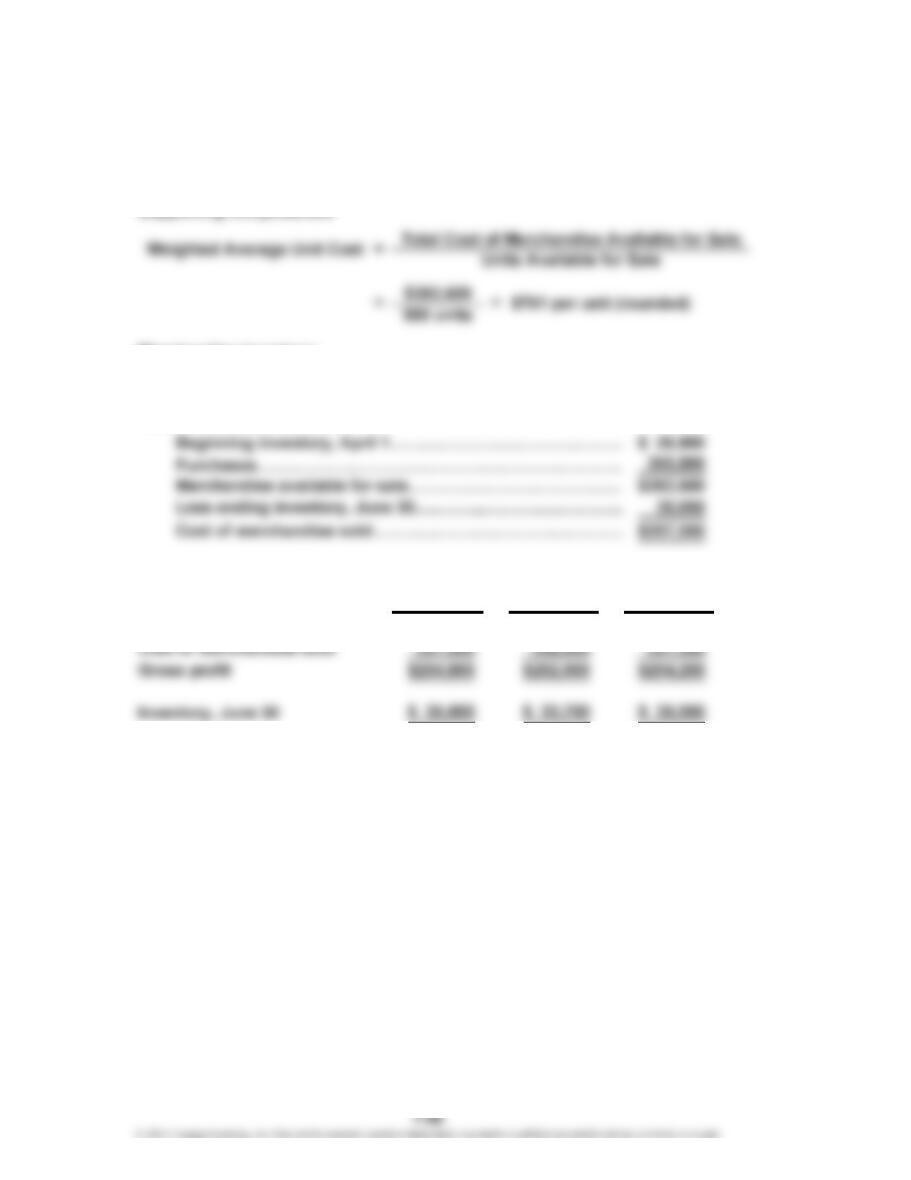

2. Total sales………………………………………………………………………

…

$611,800

Total cost of merchandise sold……………………………………………

…

358,730

Gross profit……………………………………………………………………

…

$253,070

*

CHAPTER 7 Inventories

Prob. 7-3B

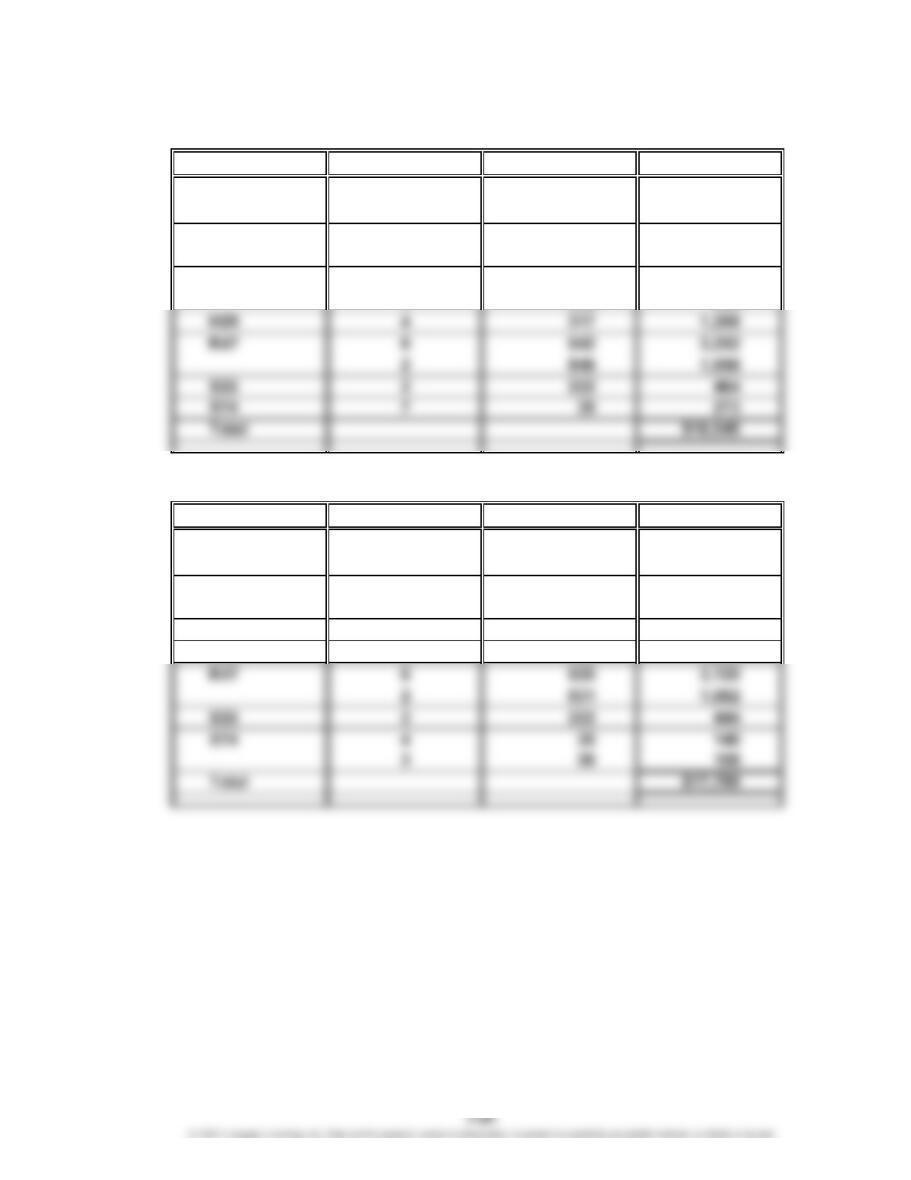

1.

Unit Total Total Total

Quantity Cost Cost Quantity Unit Cost Cost Quantity Unit Cost Cost

Apr. 3 40 670 26,800

8 120 690 82,800 160 685 109,600

11 60 685 41,100 100 685 68,500

30 50 685 34,250 50 685 34,250

May 8 100 700 70,000 150 695 104,250

10 80 695 55,600 70 695 48,650

3. $35,500 (50 units × $710)

Date

Purchases Cost of Merchandise Sold Inventory

CHAPTER 7 Inventories

Prob. 7-4B

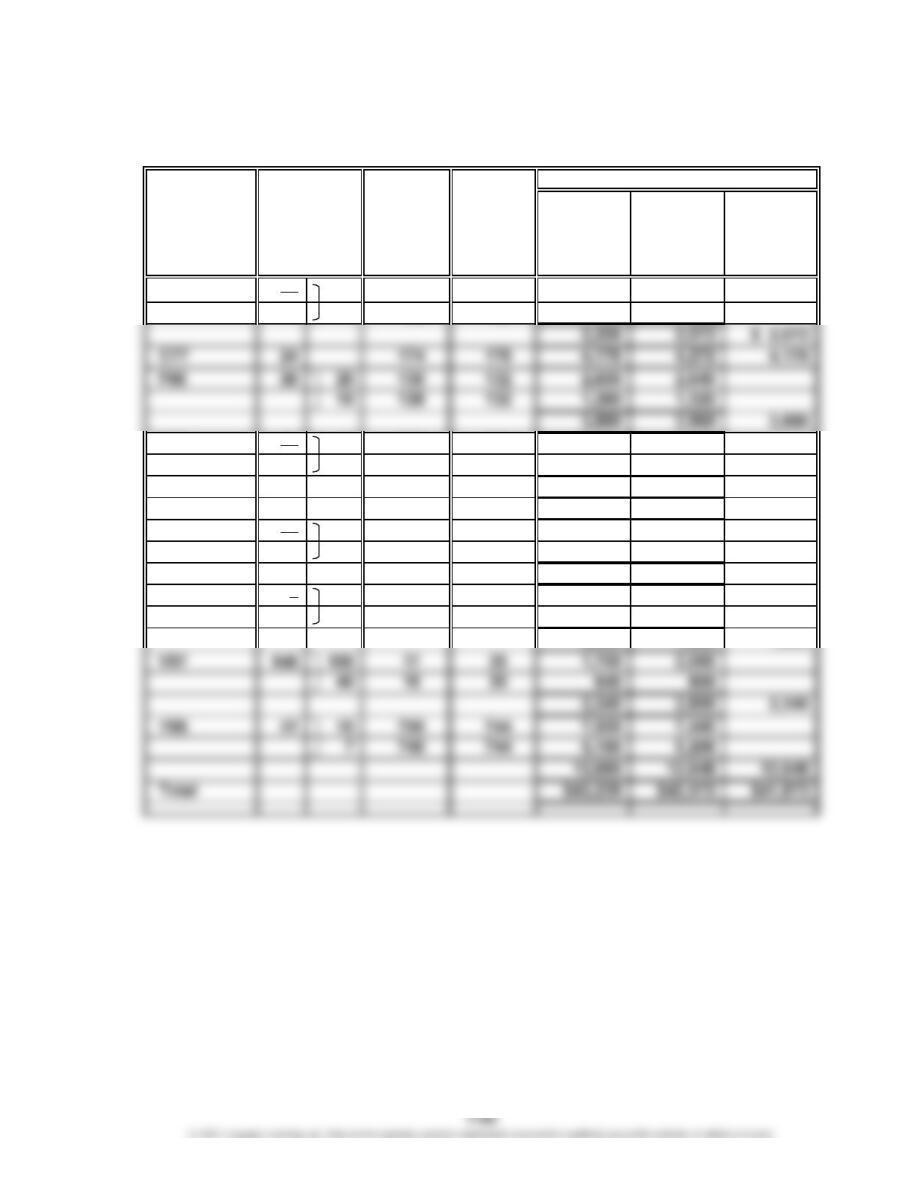

1. First-In, First-Out Method

Merchandise inventory, June 30……………………………………….

…

$ 35,600

Cost of merchandise sold………………………………………..………

…

357,000

Supporting computations

Merchandise inventory:

50 units @ $712………………………………………………………

…

$ 35,600

2. Last-In, First-Out Method

Merchandise inventory, June 30………………………………………… $ 33,700

Cost of merchandise sold…………………………………….…………

…

358,900

Supporting computations

Merchandise inventory:

40 units @ $670………………………………………………………

…

$26,800

10 unit @ $690………………………………………………………

…

6,900

50 units………………………………………………………………… $33,700

…

…

…

CHAPTER 7 Inventories

Prob. 7-4B (Continued)

3. Weighted Average Cost Method

Merchandise inventory, June 30………………………………

…

$ 35,050

Cost of merchandise sold………………………………………

…

357,550

Merchandise inventory:

50 units × $701 = $35,050 (rounded)

Cost of merchandise sold:

…

4. Weighted

FIFO LIFO Average

Sales $611,800 $611,800 $611,800

CHAPTER 7 Inventories

Prob. 7-5B

1. First-In, First-Out Method

Model Quantity Unit Cost Total Cost

C55 3 $1,070 $ 3,210

1 1,060 1,060

D11 6 675 4,050

5 666 3,330

F32 1 280 280

2. Last-In, First-Out Method

Model Quantity Unit Cost Total Cost

C55 3 $1,040 $ 3,120

1 1,054 1,054

D11 9 639 5,751

2 645 1,290

F32 2 240 480

H29 4 305 1,220

CHAPTER 7 Inventories

Prob. 7-5B (Concluded)

3. Weighted Average Cost Method

Quantity Unit Cost*Total Cost

4 $1,056 $ 4,224

11 654 7,194

2 252 504

*Computations of unit costs:

C55: $1,056 = [(3 × $1,040) + (3 × $1,054) + (3 × $1,060) + (3 × $1,070)] ÷ (3 + 3 + 3 + 3)

D11: $654 = [(9 × $639) + (7 × $645) + (6 × $666) + (6 × $675)] ÷ (9 + 7 + 6 + 6)

F32: $252 = [(5 × $240) + (3 × $260) + (1 × $260) + (1 × $280)] ÷ (5 + 3 + 1 + 1)

H29: $311 = [(6 × $305) + (3 × $310) + (3 × $316) + (4 × $317)] ÷ (6 + 3 + 3 + 4)

K47: $534 = [(6 × $520) + (8 × $531) + (4 × $549) + (6 × $542)] ÷ (6 + 8 + 4 + 6)

S33: $227 = [(4 × $222) + (4 × $232)] ÷ (4 + 4)

X74: $37 = [(4 × $35) + (6 × $36) + (8 × $37) + (7 × $39)] ÷ (4 + 6 + 8 + 7)

4. a. During periods of rising prices, the LIFO method will result in a lower cost

of inventory, a greater amount of cost of merchandise sold, and less net

Model

C55

D11

F32

CHAPTER 7 Inventories

Prob. 7-6B

Market

Value per

Cost Unit (Net

Inventory per Realizable

Item Unit Value) Cost Market LCM

A54 37 30 $ 60 $ 56 $ 1,800 $ 1,680

7 58 56 406 392

H83 21 6 547 545 3,282 3,270

15 540 545 8,100 8,175

11,382 11,445 11,382

K12 375 6 5 2,250 1,875 1,875

Q58 90 75 25 18 1,875 1,350

15 26 18 390 270

2,265 1,620 1,620

S36 8 5 256 235 1,280 1,175

3 260 235 780 705

Quantity

Inventory Sheet

December 31

Inventory

Total

CHAPTER 7 Inventories

Appendix Prob. 7-7B

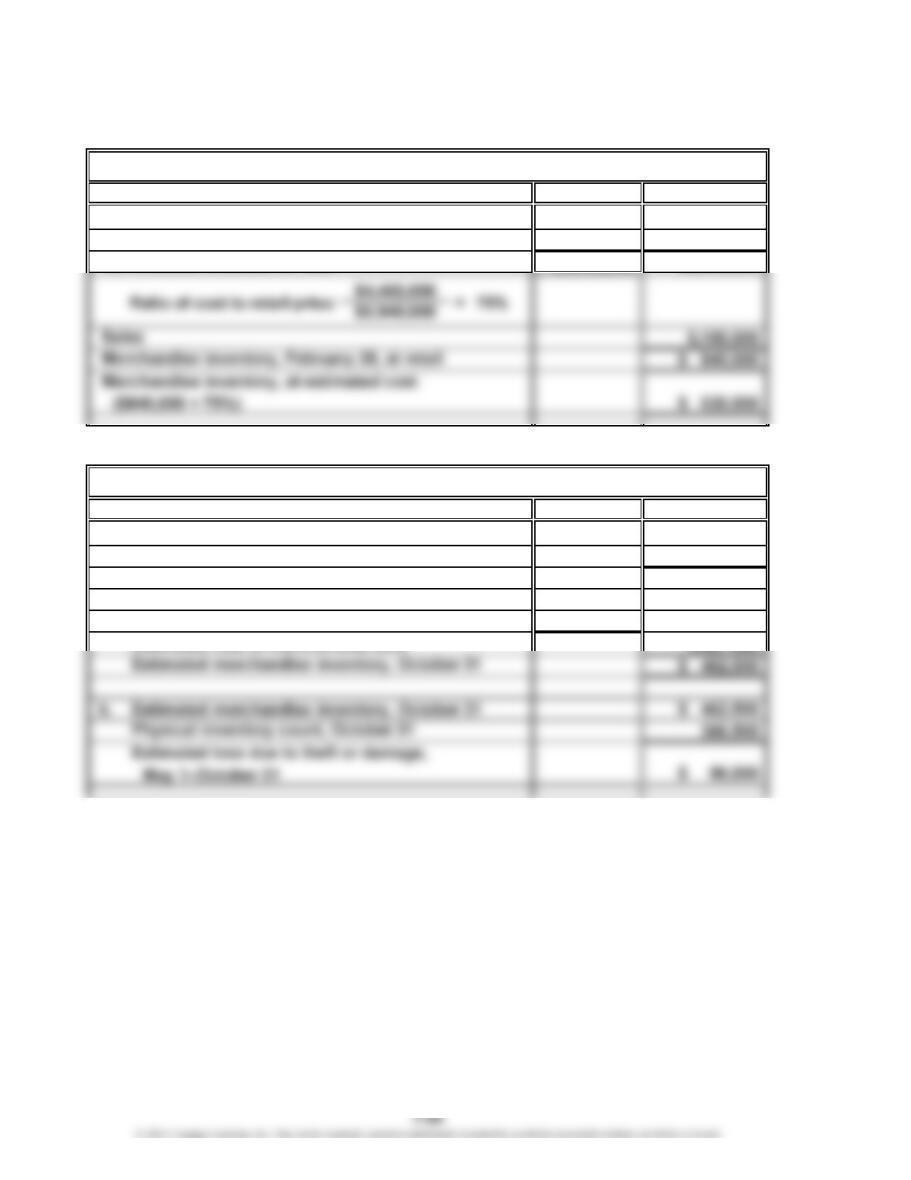

1.

Cost Retail

Merchandise inventory, February 1 $ 400,000 $ 615,000

Net purchases 4,055,000 5,325,000

Merchandise available for sale $4,455,000 $5,940,000

2.

Cost

a. Merchandise inventory, May 1 $ 400,000

Net purchases 3,150,000

Merchandise available for sale $3,550,000

Sales $4,750,000

Less estimated gross profit ($4,750,000 × 35%) 1,662,500

Jaffe Co.

Coronado Co.

CHAPTER 7 Inventories

CP 7-1

1. In the short run, Sizemo Electroniks may benefit slightly from the inflated inventory

values and higher earnings. However, at some point in the future, the inventory

2. The users of Sizemo’s financial statements are harmed by this decision, as it does

not result in financial statements that fairly present the company’s financial results.

3. No. Tina is acting unethically by instructing Jay to ignore a lower-of-cost-or-market

adjustment intentionally. As Jay’s supervisor, Tina has a responsibility to ensure

her employees behave ethically and apply GAAP correctly. Jay is behaving

unethically by knowingly applying GAAP incorrectly. He should have reported the

incident to Tina’s supervisor.

CP 7-2

Because the title to merchandise shipped FOB shipping point passes to the buyer

when the merchandise is shipped, the shipments made before midnight, October 31,

CASES & PROJECTS

CHAPTER 7 Inventories

CP 7-3

A sample solution based on Nike Inc.’s Form 10-K for the fiscal year ended May 31,

2018, follows:

1. a. Inventory costs consist primarily of product cost from the company’s suppliers,

as well as inbound freight, import duties, taxes, insurance and logistics, and

other handling fees.

b. Inventories are stated at lower of cost and net realizable value, and valued on

either an average or specific identification cost basis.

2. The company’s inventory turnover has improved between 2017 and 2018.

2018 2017

Cost of merchandise sold…………………………… $20,441 $19,038

CP 7-4

Memo

To: Ms. Connie Kilmer

President, Golden Eagle Company

From: A+ Student

Re: Comparison of LIFO and FIFO inventory methods

LIFO and FIFO are alternative methods of applying unit cost to the units that are sold

during the year and those units that remain in ending inventory at the end of the

year. The LIFO method is often viewed as the best basis for reflecting income from

operations. This is because the LIFO method matches the most current cost of

During periods of rising prices, such as for Golden Eagle Company, the LIFO method

will also result in less net income than FIFO. Because taxes are levied as a

percentage of net income, Golden Eagle Company would pay a lower income tax

under the LIFO method.

While the LIFO method is often viewed as the best method for matching revenues and

expenses, the FIFO method is often consistent with the physical movement of

merchandise in a business, since most businesses tend to dispose of commodities in

the order of their acquisition. To the extent that this is the case, the FIFO method

approximates the results that will be attained by a specific identification of costs.

CHAPTER 7 Inventories

CP 7-4 (Concluded)

Supporting computations:

The cost of ending inventory under the last-in, first-out and first-in, first-out methods

is as follows:

Last-in, first-out method:

31,000 units at $36.60………………………………………………

…

$1,134,600

1,000 units at $39.00………………………………………………

…

39,000

32,000 units…………………………………………………………

…

$1,173,600

The cost of merchandise sold and gross profit under each method are as follows:

FIFO LIFO

Sales…………………………………………………………

.

$10,000,000 $10,000,000

Cost of merchandise sold (see below)………………

…

6,974,400 6,711,600

Gross profit………………………………………………… $ 3,025,600 $ 3,288,400

…

…

…

…

…

CHAPTER 7 Inventories

CP 7-5

In developing a response to Paula’s concerns, you should probably emphasize

the practical need for an assumption concerning the flow of cost of merchandise

purchased and sold. That is, when identical goods are frequently purchased, it may

not be practical to specifically identify each item of inventory. If all the identical goods

were purchased at the same price, it wouldn’t make any difference for financial

reporting purposes which goods Musick Foods assumed were sold first, second, etc.

However, in most cases, goods are purchased over time at different prices, and hence,

a need arises to determine which goods are sold so that the price (cost) of those

CHAPTER 7 Inventories

CP 7-6

a. Target Corp.

b. Target Corp.

Amazon.com

=Inventory Turnover Cost of Merchandise Sold

Average Inventory

5.89= $53,299

($9,497 + $8,597) ÷ 2 =

=Days’ Sales in Inventory

Average Inventory

Cost of Merchandise Sold ÷ 365

62.0 days

($9,497 + $8,597) ÷ 2

$53,299 ÷ 365

=($17,174 + $16,047) ÷ 2 = 43.6 days

$139,156 ÷ 365

==

Days’ Sales in Inventory = Average Inventory

Cost of Merchandise Sold ÷ 365

CHAPTER 7 Inventories

CP 7-7

a.

Costco Wal-Mart JCPenney

Cost of merchandise sold………………………. $123,152 $385,301 $7,870

b. Costco Wal-Mart JCPenney

Average merchandise inventory

[from part (a)]………………………………………. $10,437 $44,026 $2,620

Cost of merchandise sold………………………. $123,152 $385,301 $7,870

Average daily cost of merchandise sold….

.

$337.4 $1,055.6 $21.6

Days’ sales in inventory…………………………. 30.9 41.7 121.3

c. Both the inventory turnover ratio and the days’ sales in inventory reflect the

merchandising approaches of the three companies.

Costco is a club warehouse. Its approach is to hold only mass appeal items that are

sold quickly off the shelf. Most items are sold in bulk quantities at very attractive

prices. Costco couples thin margins with very fast inventory turnover.

.

.