205

CHAPTER 7

FIXED ASSETS, NATURAL RESOURCES,

AND INTANGIBLE ASSETS

CLASS DISCUSSION QUESTIONS

1. Fixed assets have the following

characteristics:

(a) They exist physically and, thus, are tan-

gible assets.

(b) They are owned and used by the com-

pany in its normal operations.

(c) They are not offered for sale as part of

normal operations.

4. $475,000

5. Ordinarily not; if the book values closely

approximate the market values of fixed as-

sets, it is coincidental. Depreciation does not

measure a decline in the market value of a

fixed asset. Instead, depreciation is an allo-

cation of a fixed asset’s cost to expense

over the asset’s useful life. Thus, the book

value of a fixed asset (cost less accumulat-

ed depreciation) usually does not agree with

9. Capital expenditures include the cost of ac-

quiring fixed assets and the cost of improv-

ing an asset. These costs are recorded by

increasing the fixed asset account. Capital

expenditures also include the costs of ex-

traordinary repairs, which are recorded by

decreasing the asset’s accumulated depre-

ciation account. Revenue expenditures are

recorded as expenses that benefit only the

current period and are incurred for normal

maintenance and repairs of fixed assets.

10. Capital expenditure

11. a. Capital expenditure

b. Revenue expenditure (Note: Changing oil

b. An accelerated depreciation method

reduces income tax payable to the IRS in

the earlier periods of an asset’s life.

Thus, cash is freed up in the earlier peri-

ods to be used for other business

purposes.

c. MACRS is a modified form of accelerat-

ed depreciation provided by the Internal

Revenue Code. It is used in computing

depreciation for tax purposes. To simpli–

discarded.

14. Depletion is determined by multiplying the

quantity extracted and sold during the period

by the depletion rate. The depletion rate is

computed by dividing the cost of the mineral

deposit by its estimated size.

206

EXERCISES

E7–1

a. New printing press: 1, 2, 3, 5, 6

b. Used printing press: 7, 8, 9, 11

E7–2

E7–3

Initial cost of land ($100,000 + $187,500) ……………… $287,500

Plus: Legal fees …………………………………………………. $3,000

Delinquent taxes ………………………………………. 2,050

E7–4

a. No. The $8,300,000 represents the original cost of the equipment. Its replace-

ment cost, which may be more or less than $8,300,000, is not reported in the

financial statements.

E7–5

(a) 25% (1/4); (b) 12.5% (1/8); (c) 10% (1/10); (d) 5% (1/20); (e) 4% (1/25); (f) 2.5%

(1/40); (g) 2% (1/50)

207

E7–6

$2,500 = ($45,000 – $7,500) ÷ 15 years

E7–7

E7–8

a. 5% of ($160,000 – $4,500) = $7,775, or [($160,000 – $4,500) ÷ 20 years]

b. Year 1: 10% of $160,000 = $16,000

Year 2: 10% of ($160,000 – $16,000) = $14,400

E7–9

E7–10

Capital expenditures: 3, 4, 5, 6, 7, 9, 10

Revenue expenditures: 1, 2, 8

E7–11

208

E7–12

a.

Year 2 Year 1

Vehicles ……………………………………….. $ 7,542 $ 6,762

Aircraft …………………………………………. 15,801 15,772

b. A comparison of Years 1 and 2 reveals that each category of asset except

land increased during Year 2. UPS expanded its operations during Year 2 by

$1,469 ($40,620 – $39,151) with purchases of property, plant, and equipment.

209

E7–13

a.

Cost of equipment ………………………………………………………….. $ 560,000

Accumulated depreciation at December 31, 20Y7

(5 years at $26,000* per year) ……………………………………… (130,000)

Book value at December 31, 20Y7 …………………………………… $ 430,000

*($560,000 – $40,000) ÷ 20 = $26,000

b. 1. Update Depreciation

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Acc. Depr.— Retained

–

g

y

(

)

(

)

y

r

(

)

2. Sale of Equipment

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Acc.

Depr.— Retained

Cash +Equip.

–

Equip. = Earnin

g

s

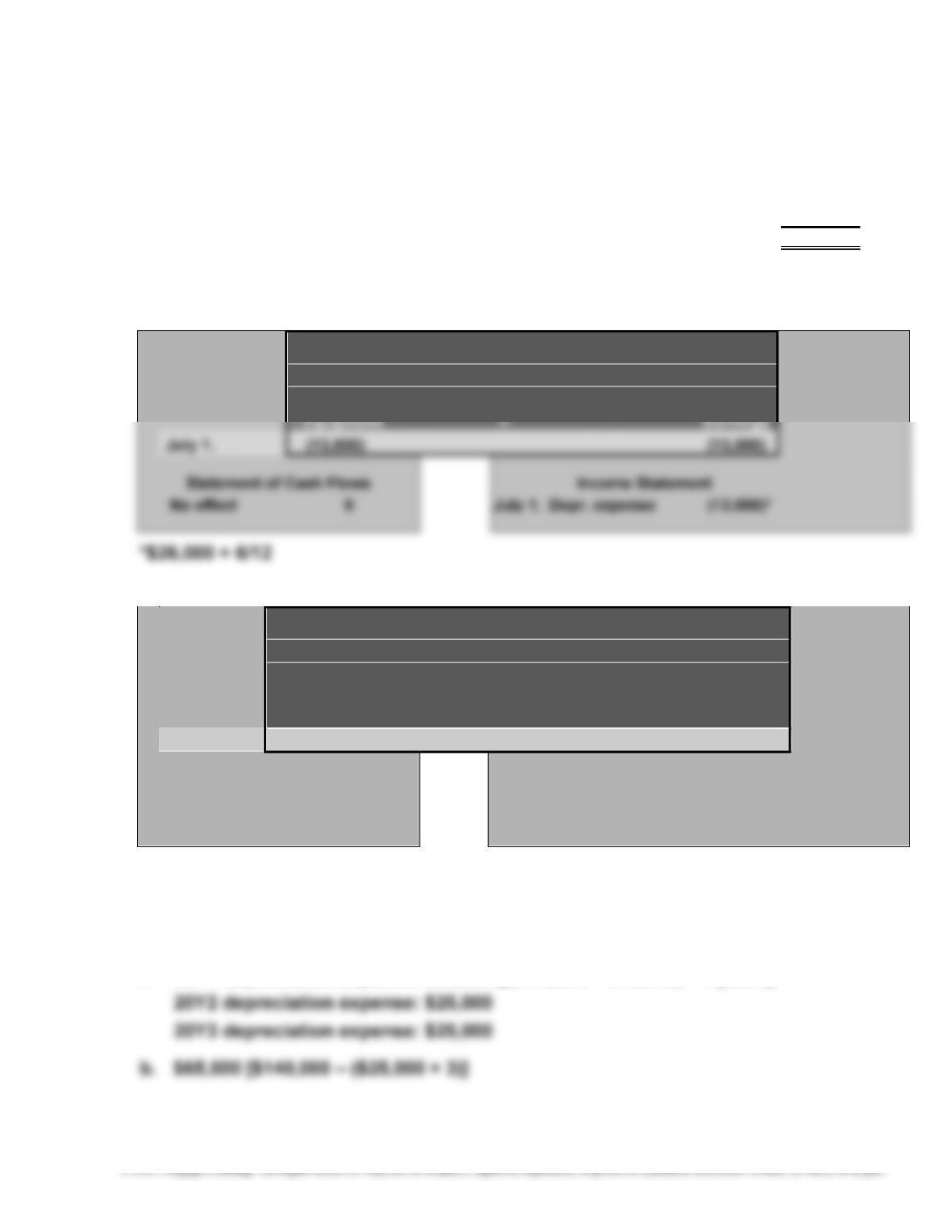

Jul

y

1. 400,000

(

560,000

)

143,000*

(

17,000

)

Statement of Cash Flows Income Statement

July 1. Investing 400,000 July 1. Loss on disposal

of fixed assets

(

17,000

)

*$130,000 + $13,000

E7–14

a. 20Y1 depreciation expense: $25,000 [($140,000 – $15,000) ÷ 5 years]

210

E7–14, Concluded

c.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Acc.

Dep

r

.— Retained

–

g

(

)

(

)

(

)

d.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Acc.

Dep

r

.— Retained

Cash + Equip.

–

Equip. = Earnin

g

s

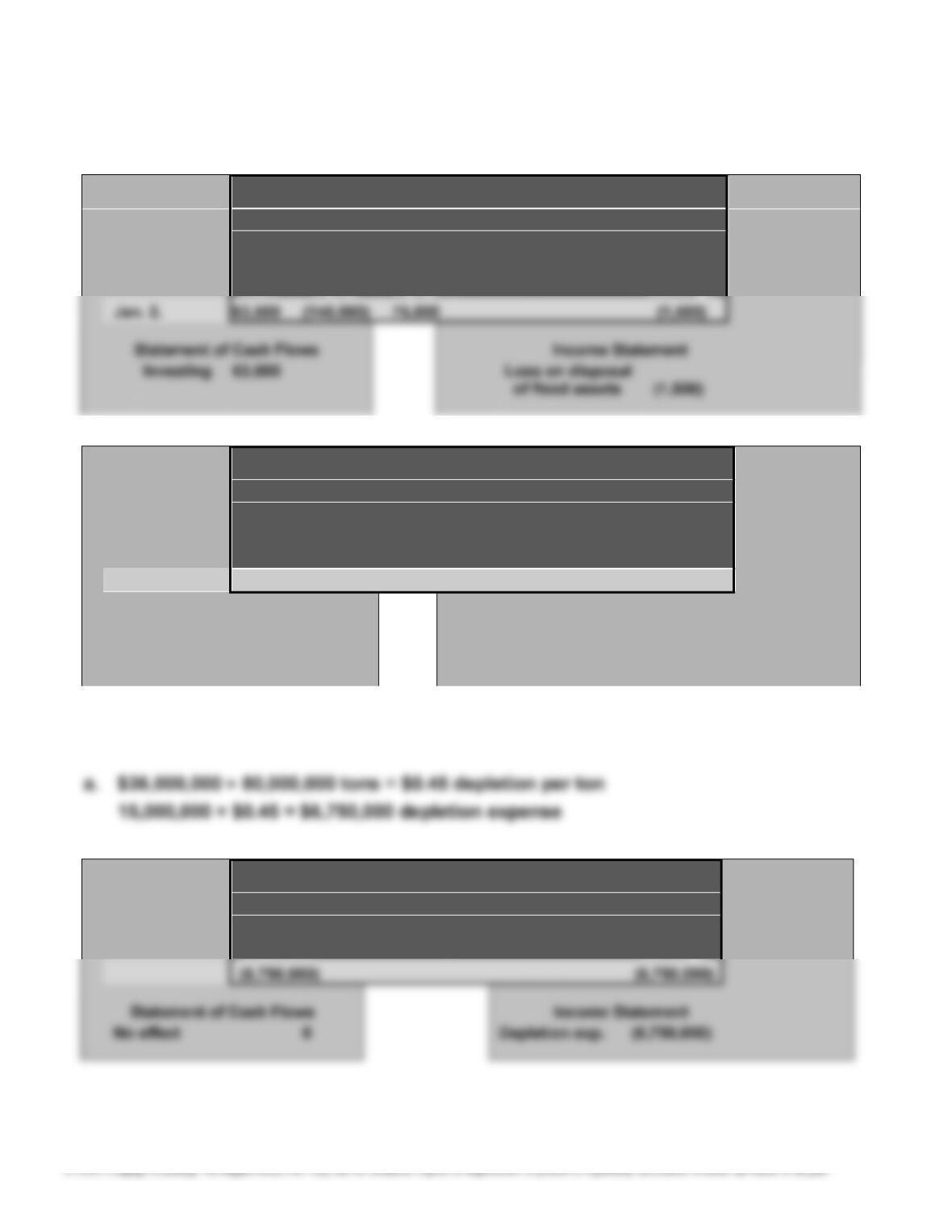

Jan. 2. 71,000

(

140,000

)

75,000 6,000

Statement of Cash Flows Income Statement

Investing 71,000 Gain on disposal

of fixed assets

6,000

E7–15

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

–

Acc. Retained

(

)

211

E7–16

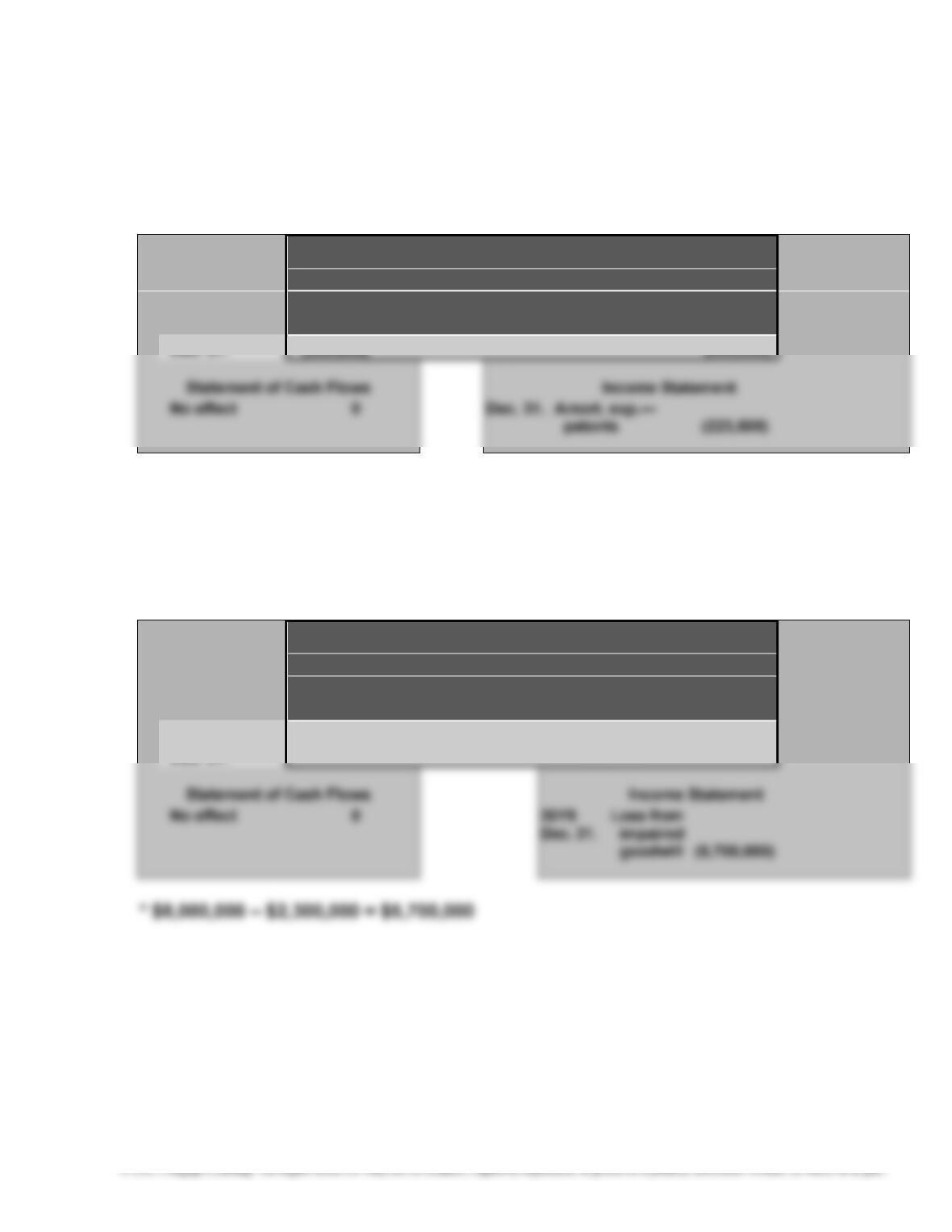

a. ($1,500,000 ÷ 8 years) + ($252,000 ÷ 7 years) = $187,500 + $36,000 = $223,500

total patent amortization expense

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Retained

Patents = Earnin

g

s

E7–17

a. $8,000,000. The goodwill is not amortized; thus, the book value of goodwill

has remained unchanged since originally recognized on January 1, 20Y3.

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Retained

Goodwill = Earnings

20Y9

(5,700,000)* (5,700,000)

212

E7–18

a. Property, Plant, and Equipment (in millions):

Year 2 Year 1

Land and buildings ……………………………………………. $16,216 $13,587

Machinery, equipment, and internal-use software .. 65,982 54,210

Leasehold improvements …………………………………… 8,205 7,279

$90,403 $75,076

Less accumulated depreciation and amortization .. (49,099) (41,293)

Book value ………………………………………………………… $41,304 $33,783

A comparison of the book values of Years 1 and 2 indicates they increased. A

comparison of the total cost and accumulated depreciation reveals that Apple

E7–19

1. Fixed assets should be reported at cost and not replacement cost.

2. Land does not depreciate.

213

PROBLEMS

P7–1

1.

Land Other

Item Land Improvements Building Accounts

a. $ 80,000

b. $ 30,000

c. 10,000

d. $ 25,000

e. 400,000

f. $ 5,000

s. 10,500

2. $ 473,500 $ 37,000 $ 876,250

*Receipt

3. Since land used as a plant site does not lose its ability to provide services, it

214

P7–2

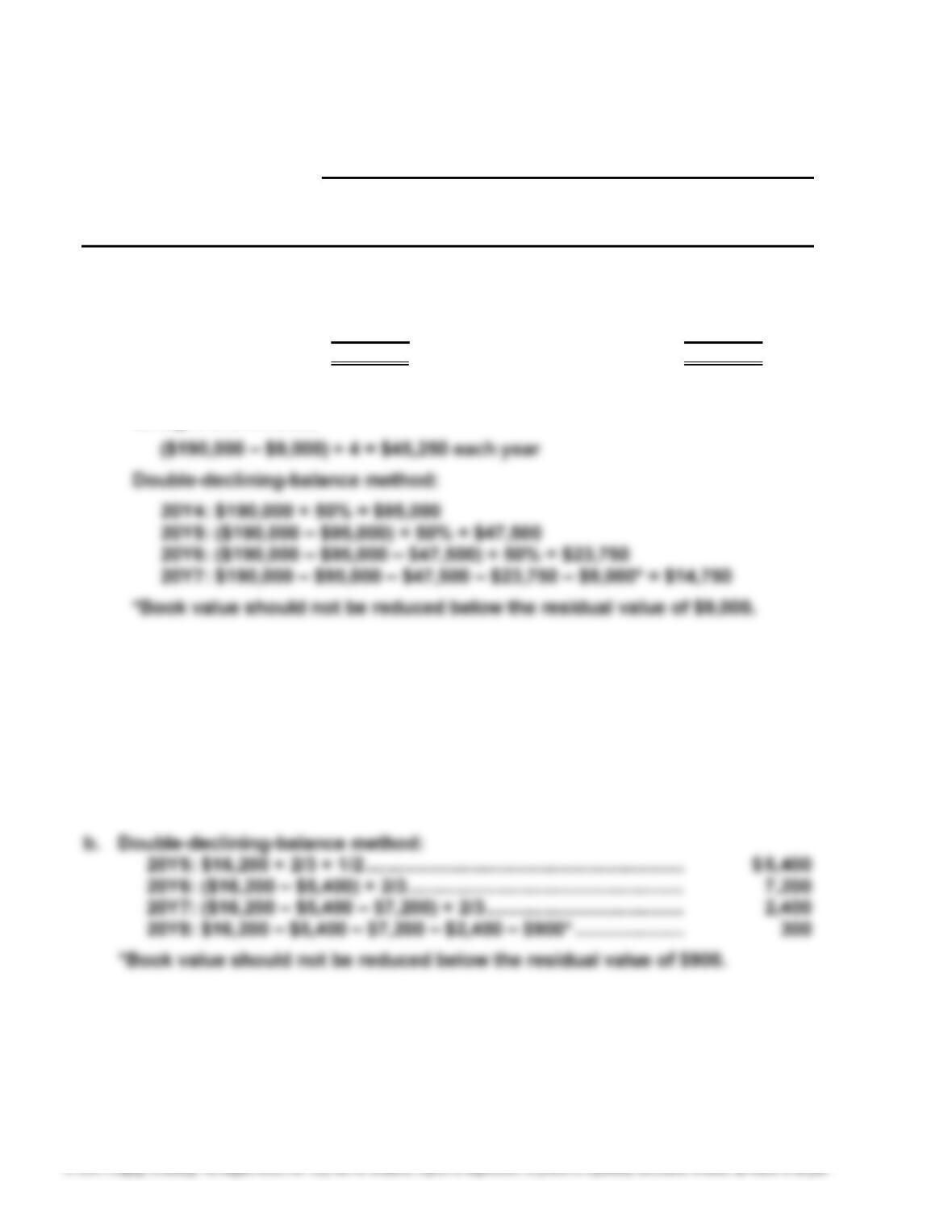

Depreciation Expense

a. Straight- b. Double-

Line Declining-Balance

Year Method Method

20Y4 $ 45,250 $ 95,000

20Y5 45,250 47,500

20Y6 45,250 23,750

20Y7 45,250 14,750*

Total $181,000 $ 181,000

Calculations:

Straight-line method:

P7–3

a. Straight-line method:

20Y5: [($16,200 – $900) ÷ 3] × 1/2 ……………………………………….. $ 2,550

20Y6: ($16,200 – $900) ÷ 3 ………………………………………………….. 5,100

20Y7: ($16,200 – $900) ÷ 3 ………………………………………………….. 5,100

20Y8: [($16,200 – $900) ÷ 3] × 1/2 ……………………………………….. 2,550

215

1.

Accumulated

Depreciation Depreciation, Book Value,

Year Expense End of Year End of Year

a. 1 $32,500* $ 32,500 $ 107,500

2 32,500 65,000 75,000

3 32,500 97,500 42,500

4 32,500 130,000 10,000

2.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Acc.

Dep

r

.— Retained

Cash + Equip.

–

Equip. = Earnin

g

s

23,300

(

140,000

)

122,500 5,800*

Statement of Cash Flows Income Statement

Investing 23,300 Gain on disposal

of equipment

5,800

*[$23,300 – ($140,000 – $122,500)]

3.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Acc.

Dep

r

.— Retained

Cash + Equip. – Equip. = Earnings

(

)