Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-1

CHAPTER 7

ACCOUNTING INFORMATION SYSTEMS

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Identify the principles and

1, 2, 3, 4,

7-1, 7-2

7-3

C2. Explain the goals and uses of

special journals.

7, 9, 10, 11,

12

7-3, 7-4,

7-7, 7-10

7-2, 7-4, 7-7,

7-9

7-4

C3. Describe the use of controlling

accounts and subsidiary ledgers.

8, 9, 12

7-5

7-5

7-1, 7-2,

7-3, GL

7-4, 7-6

Analytical objectives:

segment performance.

7-5, 7-8

Procedural objectives:

P1. Journalize and post transactions

using special journals.

7-6

7-1, 7-3, 7-6,

7-8, 7-9

7-1, 7-2, 7-3,

SP, GL

7-6, 7-7

P2. Prepare and prove the accuracy

of subsidiary ledgers.

7-8

7-10

7-1, 7-2,

7-3, GL

7-6

information systems.

5, 6

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-2

Additional Information on Related Assignment Material

Connect

Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all Exercises

and Problems Set A. Connect also provides algorithmic versions for Quick Study, Exercises and

Problems. It allows instructors to monitor, promote, and assess student learning. It can be used in

practice, homework, or exam mode.

Connect Insight

The Serial Problem (SP) for Success Systems continues in this chapter.

General Ledger

Assignable within Connect, General Ledger (GL) problems offer students the ability to see how transactions post

from the general journal all the way through the financial statements. Critical thinking and analysis components are

added to each GL problem to ensure understanding of the entire process. GL problems are auto-graded and provide

instant feedback to the student.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-3

Chapter Outline

Notes

I. System Principles—Accounting information systems (AIS) collect

and process data from transactions and events, organize them in

reports and communicate results to decision makers. The five

fundamental principles of accounting information systems are:

A. Control Principle

Prescribes that AIS has internal controls—methods and

D. Flexibility Principle

Prescribes that AIS be able to adapt to changes in the company,

business environment, and needs of decisions makers.

E. Cost-Benefit Principle

Requires that the benefits from an activity in AIS outweigh the

costs of that activity. Decisions regarding the other system

principles are affected by this principle.

II. System Components—Five components of accounting systems are:

Documents (paper and electronic) provide the information

A. Source Documents

C. Information Processors

Transform and summarize information for use in analysis and

reporting.

D. Information Storage

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-4

Chapter Outline

Notes

III. Special Journals in Accounting

3. Use allows an efficient division of labor—an effective control

A. Basics of Special Journals

2. Their use reduces recording and posting labor by grouping

similar transactions and periodically posting column totals.

b. Accounts payable ledger—stores transaction data of

B. Subsidiary Ledgers

List of individual accounts with a common characteristic. Contains

detailed information on specific general ledger accounts which are

referred to as the control account.

1. Two of the most important subsidiary ledgers are:

a. Accounts receivable ledger—stores transaction data of

2. Subsidiary ledgers are common for other general ledger

accounts such as equipment, inventory, and investments.

C. Sales Journal

Used to record sales of inventory on credit.

account in the general ledger.

1. Contains an Accounts Receivable Dr. / Sales Cr. column.

2. Contains a Cost of Goods Sold Dr. / Inventory Cr. Column.

3. A schedule (list) of accounts receivable is used to prove the

accuracy of the subsidiary ledger. The total of this schedule

D. Cash Receipts Journal

Multicolumn journal used to record all receipts of cash.

1. Every transaction increases Cash and is recorded in special

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-5

Chapter Outline

Notes

2. Credit columns are usually established for Accounts

Receivable and Sales. A special debit column is used for Sales

3. A column titled “Other Accounts – Cr.” is used to record all

4. Credits to the accounts of particular customers are individually

E. Purchases Journal

Multicolumn journal used to record all purchases on credit.

1. In addition to a special column for Inventory Dr. and Accounts

2. Only the totals of special columns are posted to the General

3. Credits to the accounts of particular creditors are individually

4. A schedule (list) of accounts payable is used to prove the

accuracy of the subsidiary ledger. The total of this schedule

F. Cash Disbursements (Cash Payments) Journal

Used to record all payments of cash.

1. A Check Register is a cash disbursements journal that includes

a column for entering the number of each check.

3. Special columns are usually established for Accounts Payable

4. A column titled “Other Accounts –Debit” is used to record all

special columns are posted to the General Ledger.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-6

Chapter Outline

Notes

5. Debits to the accounts of particular creditors are individually

G. General Journal Transactions

Used to record transactions that do not fit in any of the special

journals. Examples:

returns, and purchases of plant assets by issuing a note and

receipt of notes from customers.

1. Adjusting entries.

3. Correcting entries.

4. Other transactions may include sales returns, purchases

IV. Technology-Based Accounting Systems

A. Computer Technology in Accounting—provides accuracy, speed,

efficiency, and convenience in performing accounting tasks.

1. Multipurpose off-the-shelf software programs are designed to

2. Some software can operate efficiently as an integrated

3. Technology has reduced recordkeeping time and thereby

allows more time for analysis and managerial decision

making.

B. Data Processing in Accounting—systems differ with regard to

how input is entered and processed.

1. Online processing—enters and processes data as soon as

2. Batch processing accumulates source documents for a period

of time and then processes them all at once such as daily,

weekly, or monthly.

computers access to a common database and programs.

rely on modem or wireless communication.

C. Computer Networks in Accounting

Chapter Outline

Notes

D. Enterprise-Resource Planning (ERP) Software

Payable Ledger.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-7

E. Cloud Computing

1. Delivery of computing as a service rather than a product.

V. Decision Analysis—Segment Return on Assets

A. A segment is a part of a company that is separately identified by

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-8

Chapter 7 Alternate Demonstration Problem

Bedrock Company completed these transactions during February of the

current year:

Feb

1

Owner, F. Stone invested $100,000 cash in the business.

1

Sent Flint Company check No. 413 for a cash purchase of

inventory $ 75,000.

5

Purchased on credit from Best Company inventory, $1,855;

store supplies, $75; and office supplies, $35. Invoice dated

February 4, terms n/10, EOM.

7

Borrowed $5,000 by giving First National Bank a promissory

note payable.

9

Purchased office equipment on credit from More Company,

invoice dated February 6, terms n/10, EOM, $625.

Sent Able Company Check No. 414 in payment of its January

Sold inventory costing $1,000 on credit to Carl Cole for $ 1,650

Invoice No. 713.

the discount.

the discount.

Received inventory and an invoice dated February 11, terms

Feb.

14

Issued Check No. 415, payable to Payroll, in payment of sales

3

Received inventory and an invoice dated January 30, terms

4

Invoice No. 712.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-9

salaries for the first half of the month, $855. Cashed the check

and paid the employees.

14

Cash sales for the first half of the month, $18,460. Cost of this

merchandise was $ 9,500. (Normally, cash sales are recorded

18

Received a credit memorandum from More Company for office

equipment received on February 9 and returned for credit,

$130.

21

Received payment from Carl Cole for the sale of February 11

less the discount.

21

24

Invoice No. 714.

Issued Check No. 417, payable to Payroll, in payment of sales

salaries for the last half of the month, $855. Cashed the check

and paid the employees.

28

Cash sales for the last half of the month, $20,215. Cost of this

Issued Check No. 416 to Old Company in payment of its

Purchased inventory on credit from Best Company, $410;

store supplies, $45; and office supplies, $30. Invoice dated

Received a credit memorandum from Old Company for

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-10

general ledger accounts.

Required:

1. Open the following general ledger accounts: Cash, Accounts

Receivable, Inventory, Store Supplies, Office Supplies, Office

2. Open the following accounts receivable ledger accounts: Carl Cole,

3. Open the following accounts payable ledger accounts: Able

Company, Best Company, More Company, and Old Company.

4. Enter the transactions in a Sales Journal, a Purchases Journal, a

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-11

Chapter 7 Solution: Alternate Demonstration Problem

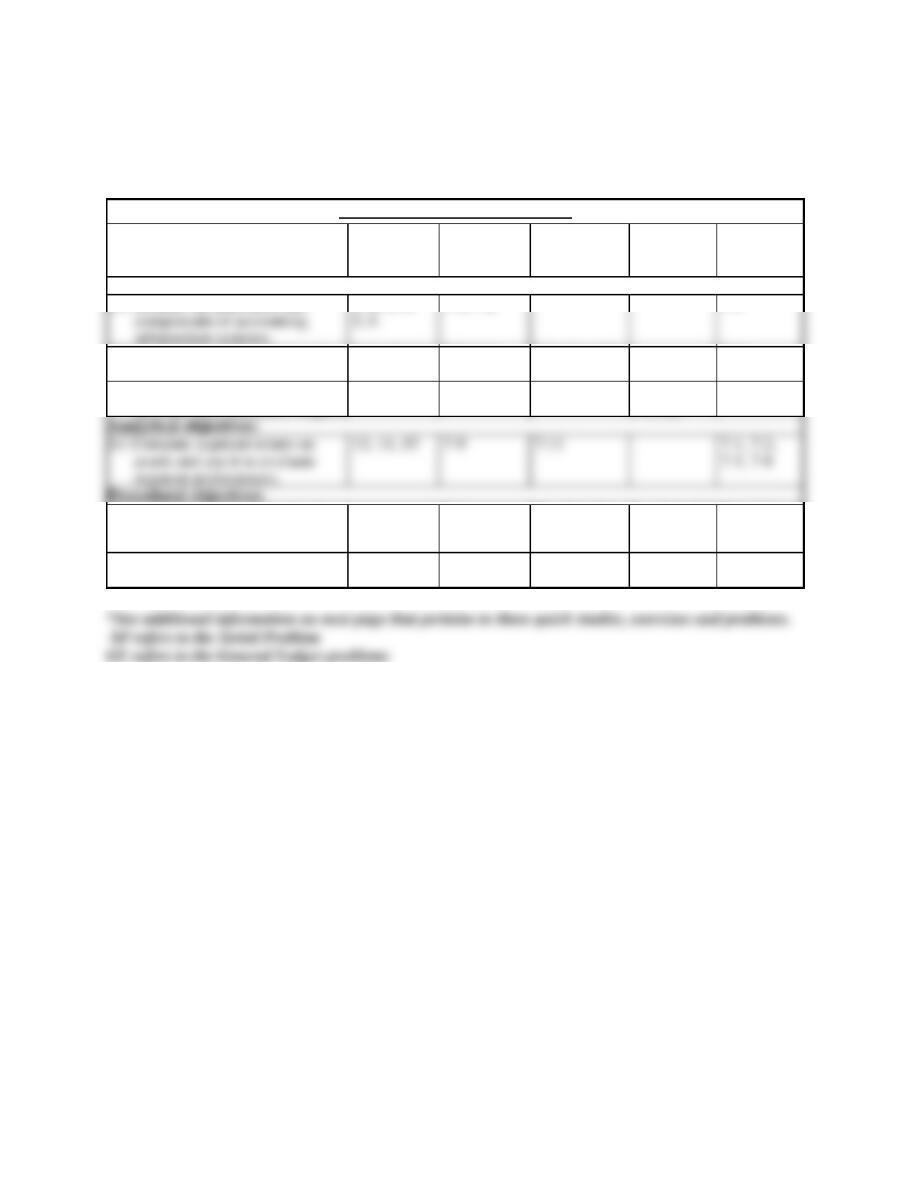

SALES JOURNAL

Date

Account Debited

Invoice

Number

PR

Accts Rec Dr

Sales Cr

Cost of Goods Sold Debit

Inventory Credit

Feb.

2

Dale Dent

711

800.00

500.00

4

Gary Glen

712

1,250.00

850.00

PURCHASES JOURNAL

Date

Amount Credited

Date of

Invoice

Terms

P

R

Accounts

Payable

Credit

Inventory

Debit

Store

Supplies

Debit

Office

Supplies

Debit

Feb.

3

Able Company

1/30

2/10, n/60

1,750.00

1,750.00

. . . . .

. . . . .

5

Best Company

2/4

n/10, EOM

1,965.00

1,855.00

75.00

35.00

Old Company

2/11

2/10, n/60

1,985.00

1,985.00

. . . . .

. . . . .

Best Company

2/12

n/10, EOM

45.00

30.00

Totals

65.00

Carl Cole

714

475.00

Gary Glen

715

375.00

Totals

5,310.00

(112/411)

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-13

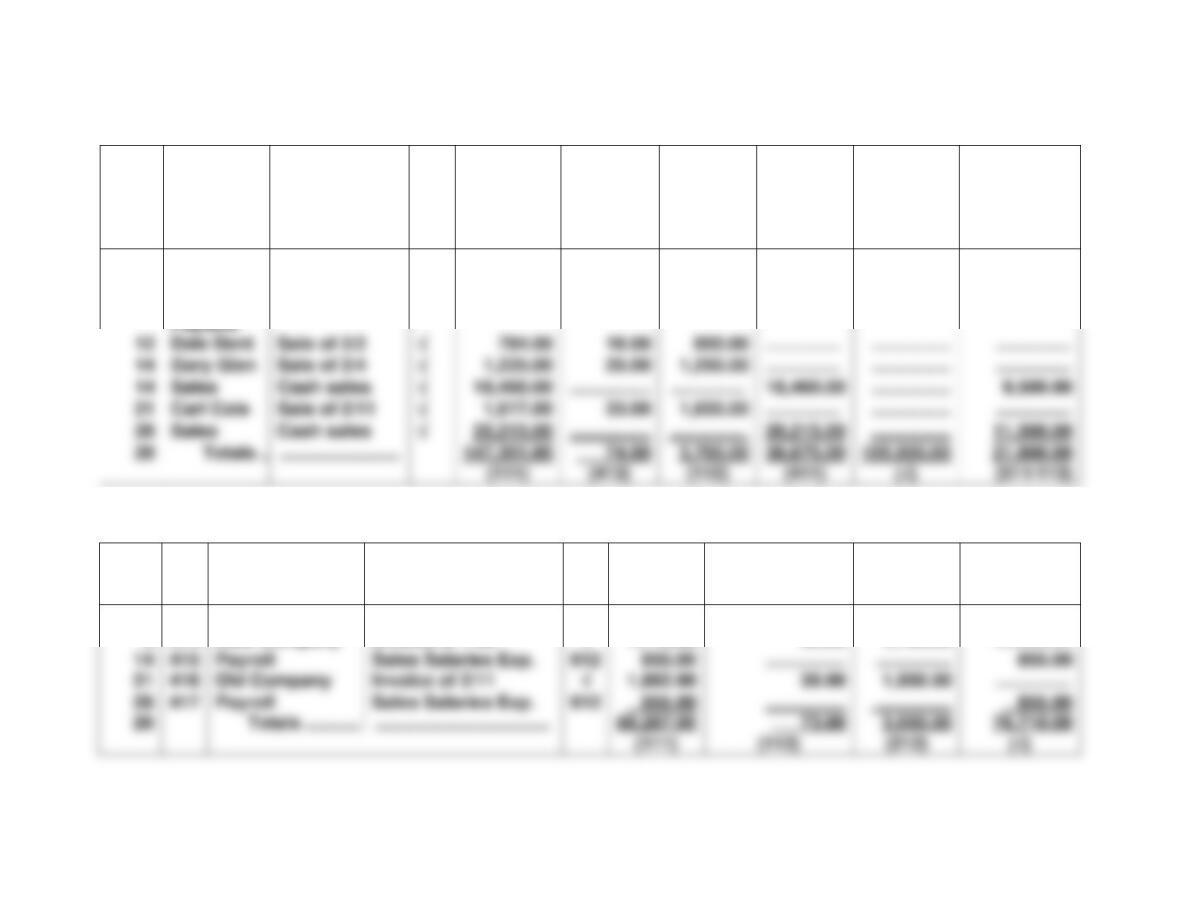

CASH RECEIPTS JOURNAL

Date

Account

Credited

Explanation

PR

Cash

Debit

Sales

Disc.

Debit

Accts.

Rec.

Credit

Sales

Credit

Other

Accts.

Credit

Cost of

Goods Sold

Debit

Inventory

Credit

Feb.1

F.Stone,

Capital

Investment

311

100,000.00

…………….

……………

……………

100,000.00

……………

7

Notes

Note to bank

211

5,000.00

…………….

……………

……………

5,000.00

……………

CASH DISBURSEMENTS JOURNAL

Date

Ch.

No.

Payee

Account Debited

PR

Cash

Credit

Inventory

Credit

Accts.

Pay

Debit

Other

Accts.

Debit

Feb.1

413

Flint Company

Inventory

113

75,000.00

…………….

……………

75,000.00

9

414

Able Company

Invoice of 1/30

1,715.00

35.00

1,750.00

……………

415

Payroll

Sales Salaries Exp.

612

…………….

……………

417

Payroll

Sales Salaries Exp.

612

…………….

……………

Totals ………..

……………………………..

80,287.00

76,710.00

(212)

Payable

Dale Dent

Sale of 2/2

16.00

……………

Sales

Cash sales

18,460.00

Sales

Cash sales

20,215.00

Totals ………..

……………………

147,301.00

105,000.00

21,000.00

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-14

GENERAL JOURNAL

Feb 9

Office Equipment

133

625.00

Accounts Payable/ More Company

212/

625.00

GENERAL LEDGER

Cash Acct. No. 111

Date

Explanation

PR

Debit

Credit

Balance

Feb.

28

28

R2

D2

147,301

80,287

147,301

67,014

Accounts Receivable Acct. No. 112

Date

Explanation

PR

Debit

Credit

Balance

Feb.

28

28

S2

R2

5,310

3,700

5,310

1,610

Inventory Acct. No. 113

Date

Explanation

PR

Debit

Credit

Balance

Feb.

28

D2

2

D2

75,000

75,000

Store Supplies Acct. No. 115

Date

Explanation

PR

Debit

Credit

Balance

Feb.

28

P2

120

120

Office Supplies Acct. No. 116

Date

Explanation

PR

Debit

Credit

Balance

Feb.

28

P2

Date

Explanation

PR

Debit

Credit

Balance

18

130

495

Accounts Payable/ Old Company

212/

113

Accounts Payable/ More Company

212/

130.00

133

130.00

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-15

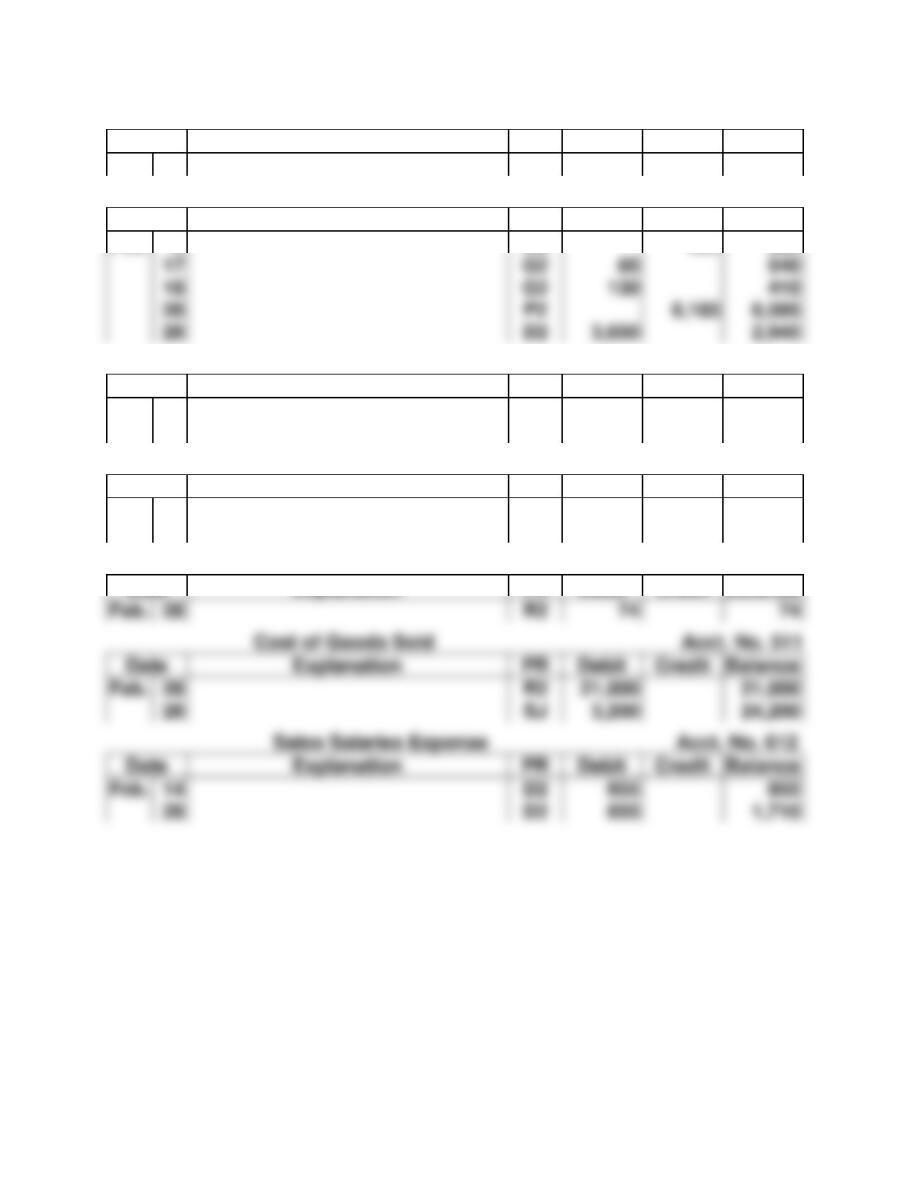

Notes Payable Acct. No. 211

Date

Explanation

PR

Debit

Credit

Balance

Feb.

7

R2

5,000

5,000

Accounts Payable Acct. No. 212

Date

Explanation

PR

Debit

Credit

Balance

Feb.

9

G2

625

625

F. Stone, Capital Acct. No. 311

Date

Explanation

PR

Debit

Credit

Balance

Feb.

1

R2

100,000

100,000

Sales Acct. No. 411

Date

Explanation

PR

Debit

Credit

Balance

Feb.

28

28

S2

R2

5,310

38,675

5,310

43,985

Sales Discounts Acct. No. 413

Date

Explanation

PR

Debit

Credit

Balance

Feb.

28

R2

Date

Explanation

PR

Debit

Credit

Balance

Feb.

28

28

3,200

24,200

Date

Explanation

PR

Debit

Credit

Balance

Feb.

14

28

D2

1,710

28

D2

3,650

2,945

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-16

ACCOUNTS RECEIVABLE LEDGER

Carl Cole

Date

Explanation

PR

Debit

Credit

Balance

Gary Glen

Date

Explanation

PR

Debit

Credit

Balance

Feb.

4

14

26

S2

R2

S2

1,250

775

1,250

1,250

-0-

775

ACCOUNTS PAYABLE LEDGER

Able Company

Date

Explanation

PR

Debit

Credit

Balance

Feb.

Date

Explanation

PR

Debit

Credit

Balance

16

P2

1,965

485

Date

Explanation

PR

Debit

Credit

Balance

Date

Explanation

PR

Debit

Credit

Balance

Feb.

21

P2

1,985

3

P2

1,750

1,750

Feb.

24

S2

S2

1,650

835

1,650

835

Date

Explanation

PR

Debit

Credit

Balance

12

800

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

7-17

BEDROCK COMPANY

Trial Balance

February 28, 2017

Cash …………………………………………………………………

$67,014

Accounts Receivable …………………………………………

1,610

Inventory …………………………………………………………..

56,642

Gary Glen ………………………………………………………….

Total ………………………………………………………...

$1,610

Best Company …………………………………………………..

$2,450

More Company ………………………………………………….

Total ………………………………………………………..

$2,945

BEDROCK COMPANY

Schedule of Accounts Receivable

February 28, 2017

Notes payable …………………………..……………………….

$ 5,000

100,000

43,985

Sales discounts …………………………..…………………….

24,200

Totals ……………………………………………………….