1. The receiving report should be reconciled to the initial purchase order and the vendor’s invoice

b

efore recording or paying for inventory purchases. This procedure will verify that the inventory

received matches the type and quantity of inventory ordered. It also verifies that the vendor’s invoic

e

is charging the company for the actual quantity of inventory received at the agreed-upon price.

2. A physical inventory should be taken periodically to test the accuracy of the perpetual records. In

addition, a physical inventory will identify inventory shortages or shrinkage.

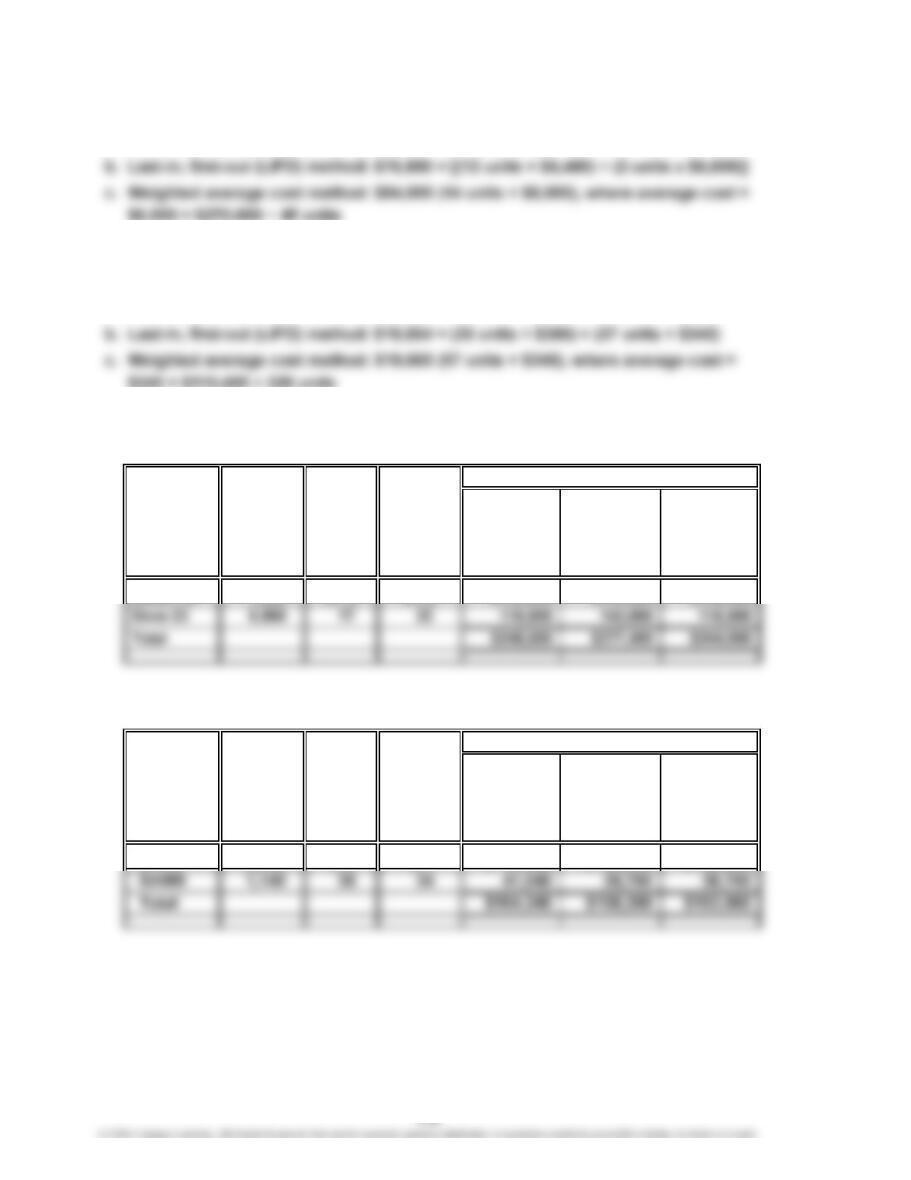

3. No, they are not techniques for determining physical quantities. The terms refer to cost flow

assumptions, which affect the determination of the cost prices assigned to items in the inventory.

4. a. LIFO c. LIFO

b. FIFO d. FIFO

5. FIFO

6. LIFO. In periods of rising prices, the use of LIFO will result in the lowest net income and thus the

lowest income tax expense.

7. The merchandise should be valued using the lower of its cost of $1,350 or its market (net realizable)

value of $1,295 ($1,475

–

$180). Thus, the merchandise should be valued at its market value of

$1,295.

8. a. Gross profit for the year was understated by $14,750.

b. Merchandise inventory and owner’s equity were understated by $14,750.

9. Bibbins Company. Since the merchandise was shipped FOB shipping point, title passed to

Bibbins Company when it was shipped and should be reported in Bibbins Company’s financial

statements at May 31, the end of the fiscal year.

10. Manufacturer’s. The manufacturer retains title until the goods are sold. Thus, any unsold merchandis

at the end of the year is part of the manufacturer’s (consignor’s) inventory, even though the

merchandise is in the hands of the retailer (consignee).

CHAPTER 7

INVENTORIES

DISCUSSION QUESTIONS

CHAPTER 7 Inventories

PE 7–1A

a. First-in, first-out (FIFO)

$112 ($55 + $57)

$116 ($58 × 2)

$28 ($90 – $62)

$32 ($90 – $58)

PE 7–1B

a. First-in, first-out (FIFO)

$50 ($110 – $60)

$120 ($60 × 2)

PE 7–2A

a. Cost of merchandise sold (January 25):

25 units @ $100 $2,500

PE 7–2B

a. Cost of merchandise sold (July 24):

6 units @ $15 $ 90

$60 ($110 – $50)

$130 ($60 + $70)

June

June 30

Gross Profit Ending Inventory

PRACTICE EXERCISES

Gross Profit

November

Ending Inventory

November 30

$119 ($57 + $62)

$35 ($90 – $55)

PE 7–3A

a.

Cost of merchandise sold (April 27):

b. Inventory, April 30:

120 units @ $8 $ 960

PE 7–3B

a. Cost of merchandise sold (March 27):

b. Inventory, March 31:

45 units @ $18 $ 810

PE 7–4A

a. Weighted average unit cost: $88

Inventory total cost after purchase on May 23:

PE 7–4B

a. Weighted average unit cost: $9.50

Inventory total cost after purchase on October 22:

125 units @ $8 $1,000

CHAPTER 7 Inventories

PE 7–5A

a. First-in, first-out (FIFO) method: $90,720 = 14 units × $6,480

PE 7–5B

a. First-in, first-out (FIFO) method: $20,094 = (40 units × $357) + (17 units × $342)

PE 7–6A

Market

Value per

Cost Unit (Net

Inventory per Realizable

Commodity Quantity Unit Value) Cost Market LCM

Raven 10 1,200 $115 $112 $138,000 $134,400 $134,400

PE 7–6B

Market

Value per

Cost Unit (Net

Inventory per Realizable

Commodity Quantity Unit Value) Cost Market LCM

JFW1 6,330 $10 $11 $ 63,300 $ 69,630 $ 63,300

Total

Total

PE 7–7A

Balance Sheet:

Merchandise inventory understated*…………………

Current assets understated……………………………

Total assets understated…………………………………

Owner’s equity understated……………………………

Cost of merchandise sold overstated…………………

Gross profit understated…………………………………

Net income understated…………………………………

(11,600)

(11,600)

(11,600)

PE 7–7B

Balance Sheet:

Merchandise inventory overstated*……………………

Current assets overstated………………………………

Total assets overstated…………………………………

Owner’s equity overstated………………………………

Cost of merchandise sold understated………………

Gross profit overstated…………………………………

Net income overstated……………………………………

8,780

8,780

$8,780

$(11,600)

(11,600)

(11,600)

Overstatement (Understatement)

Amount of Misstatement

Amount of Misstatement

Overstatement (Understatement)

8,780

8,780

CHAPTER 7 Inventories

PE 7–8A

a.

Cost of merchandise sold

Inventories:

Beginning of year

End of year

$819,000

$774,000

b.

Cost of merchandise sold

Average daily cost of

merchandise sold

$819,000

$774,000

c. The increase in the inventory turnover from 4.8 to 5.5 and the decrease in the

2016 2015

$12,341.1 $10,178.6

$4,504,500

$3,715,200

Inventory Turnover

Number of Days’ Sales

in Inventory

$788,000

$760,000

$850,000

$788,000

2016 2015

$4,504,500

$3,715,200

PE 7–8B

a.

Cost of merchandise sold

Inventories:

Beginning of year

$805,000

$755,000

b.

Cost of merchandise sold

Average daily cost of

merchandise sold

$805,000

$755,000

c. The decrease in the inventory turnover from 5.3 to 4.8 and the increase in the

2016 2015

2016 2015

$770,000

$740,000

$3,864,000

$4,001,500

Inventory Turnover

Number of Days’ Sales

in Inventory

$4,001,500

$10,586.3 $10,963.0

$3,864,000

($3,864,000 ÷ 365 days) ($4,001,500 ÷ 365 days)

CHAPTER 7 Inventories

Ex. 7–1

Switching to a perpetual inventory system will strengthen Triple Creek Hardware’s

internal controls over inventory because the store managers will be able to keep

track of how much of each item is on hand. This should minimize shortages of

Ex. 7–2

a. Appropriate. The inventory tags will protect the inventory from customer theft.

b. Inappropriate. The control of using security measures to protect the inventory

is violated if the stockroom is not locked.

EXERCISES

CHAPTER 7 Inventories

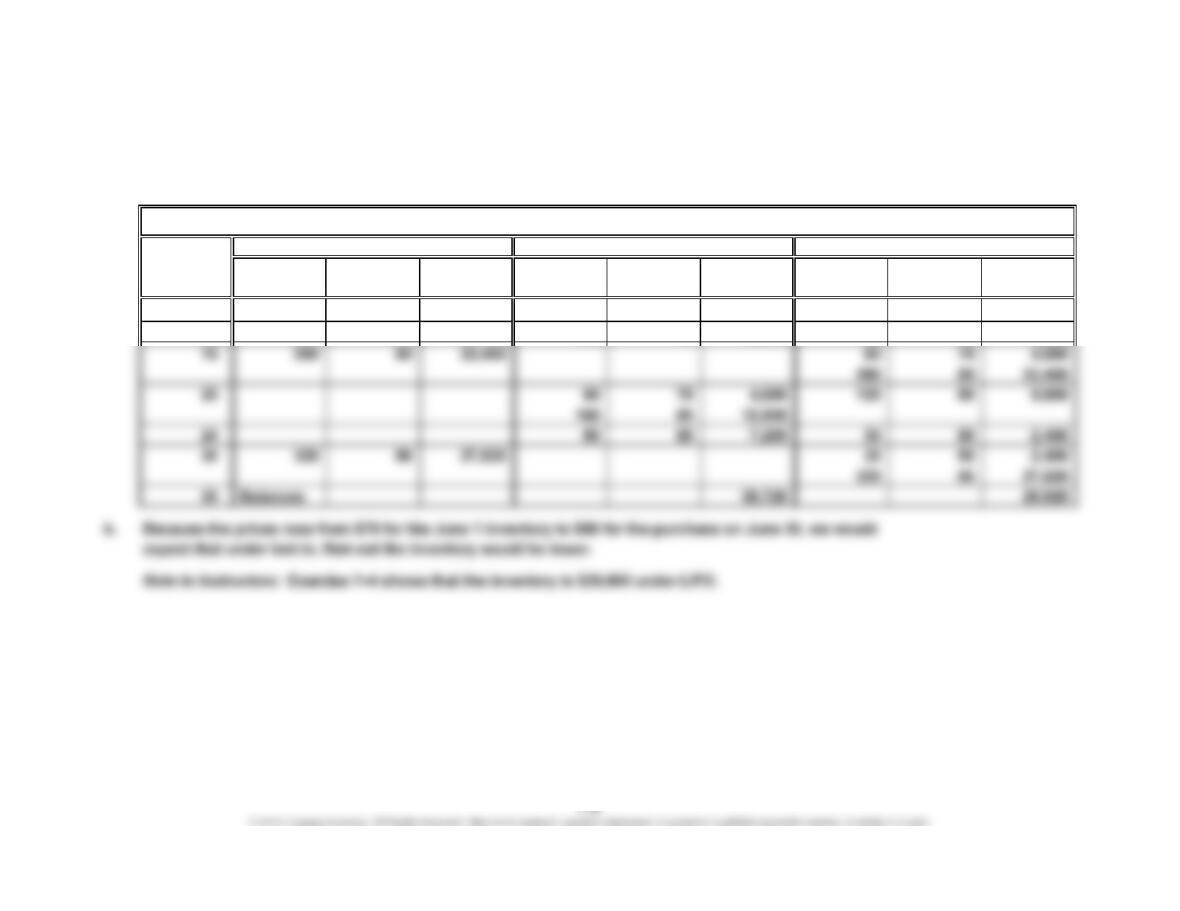

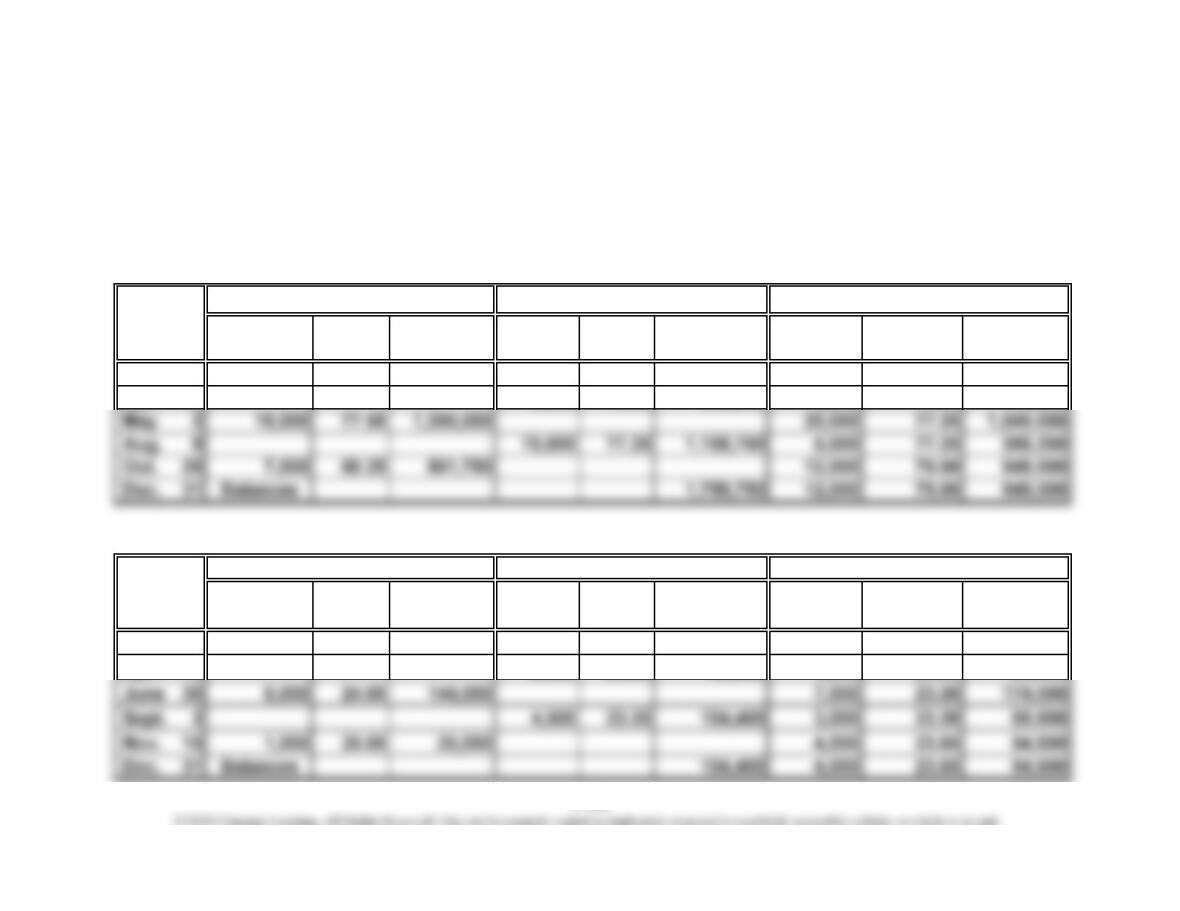

Ex. 7–3

a.

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

June 1240 78 18,720

10 180 78 14,040 60 78 4,680

Date

Portable DVD Players

Purchases Cost of Merchandise Sold Inventory

CHAPTER 7 Inventories

Ex. 7–4

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

Jun. 1240 78 18,720

10 180 78 14,040 60 78 4,680

15 280 80 22,400 60 78 4,680

Date

Portable DVD Players

Purchases Cost of Merchandise Sold Inventory

CHAPTER 7 Inventories

Ex. 7–5

a.

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

May 11,550 44 68,200

10 720 45 32,400 1,550 44 68,200

720 45 32,400

Date

Prepaid Cell Phones

Purchases Cost of Merchandise Sold Inventory

CHAPTER 7 Inventories

Ex. 7–6

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

May 11,550 44 68,200

10 720 45 32,400 1,550 44 68,200

720 45 32,400

Date

Prepaid Cell Phones

Purchases Cost of Merchandise Sold Inventory

CHAPTER 7 Inventories

Ex. 7–7

a. $22,880 ($4.40 × 5,200 units)

b. $22,000 [($4.00 × 1,200 units) + ($4.20 × 2,000 units) + ($4.40 × 2,000 units)] = $4,800 + $8,400 + $8,800

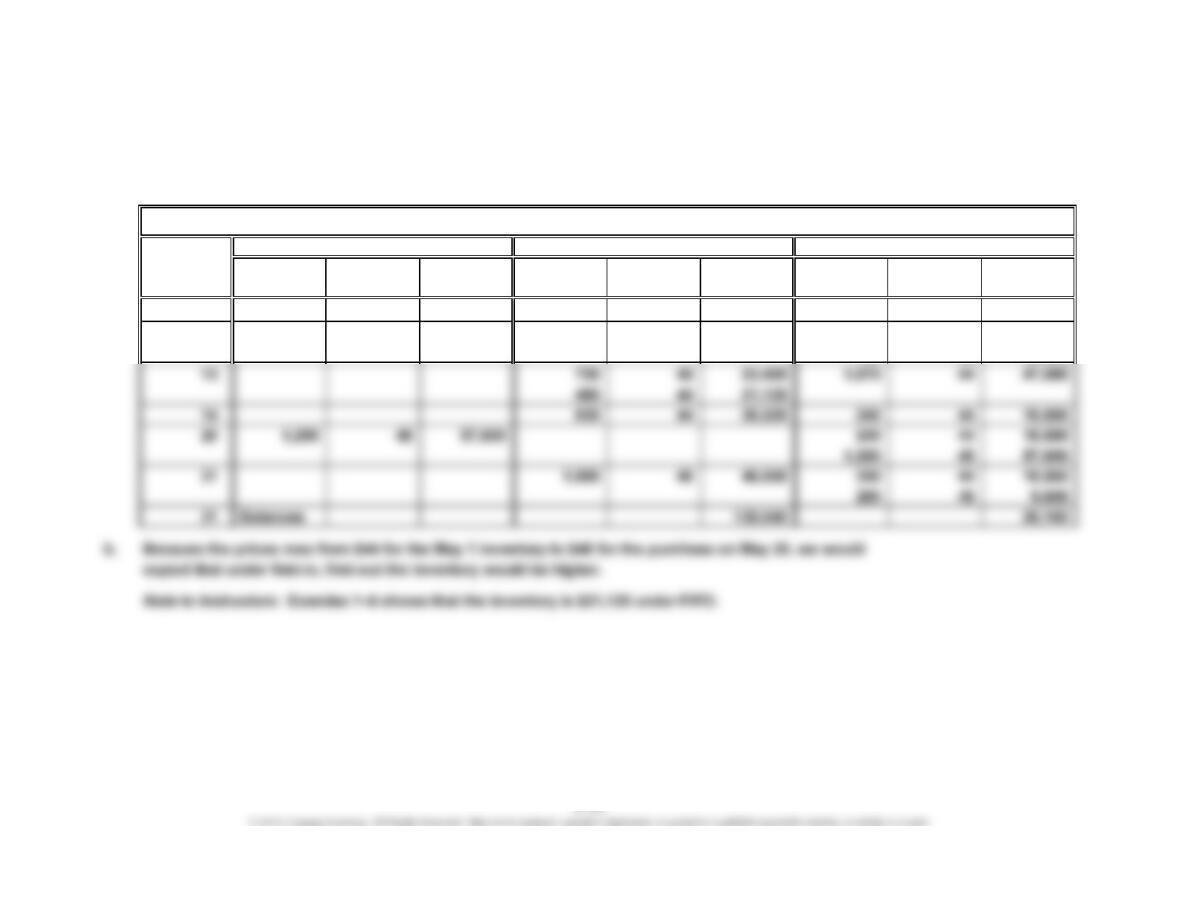

Ex. 7–8

Cost of Merchandise Sold

Unit Total Unit Total Total

Quantity Cost Cost Quantity Cost Cost Quantity Unit Cost Cost

Jan. 1 10,000 75.00 750,000

Mar. 18 8,000 75.00 600,000 2,000 75.00 150,000

Ex. 7–9

Cost of Merchandise Sold

Unit Total Unit Total Total

Quantity Cost Cost Quantity Cost Cost Quantity Unit Cost Cost

Jan. 1 4,000 20.00 80,000

Apr. 19 2,500 20.00 50,000 1,500 20.00 30,000

Date

Inventory

Inventory

Date

Purchases

Purchases

7-13

CHAPTER 7 Inventories

7-14

Ex. 7–10

Cost of Merchandise Sold

Unit Total Unit Total Total

Quantity Cost Cost Quantity Cost Cost Quantity Unit Cost Cost

Jan. 14,000 20.00 80,000

Apr. 19 2,500 20.00 50,000 1,500 20.00 30,000

June 30 6,000 24.00 144,000 1,500 20.00 30,000

Date

InventoryPurchases

CHAPTER 7 Inventories

Ex. 7–11

Inventory

Unit Total Unit Total Total

Quantity Cost Cost Quantity Cost Cost Quantity Unit Cost Cost

Jan. 1 4,000 20.00 80,000

Apr. 19 2,500 20.00 50,000 1,500 20.00 30,000

June 30 6,000 24.00 144,000 1,500 20.00 30,000

Ex. 7–12

a. $15,400 (220 units at $70)

b. $13,280 (200 units at $60 plus 20 units at $64) = $12,000 + $1,280

Date

Cost of Merchandise SoldPurchases

CHAPTER 7 Inventories

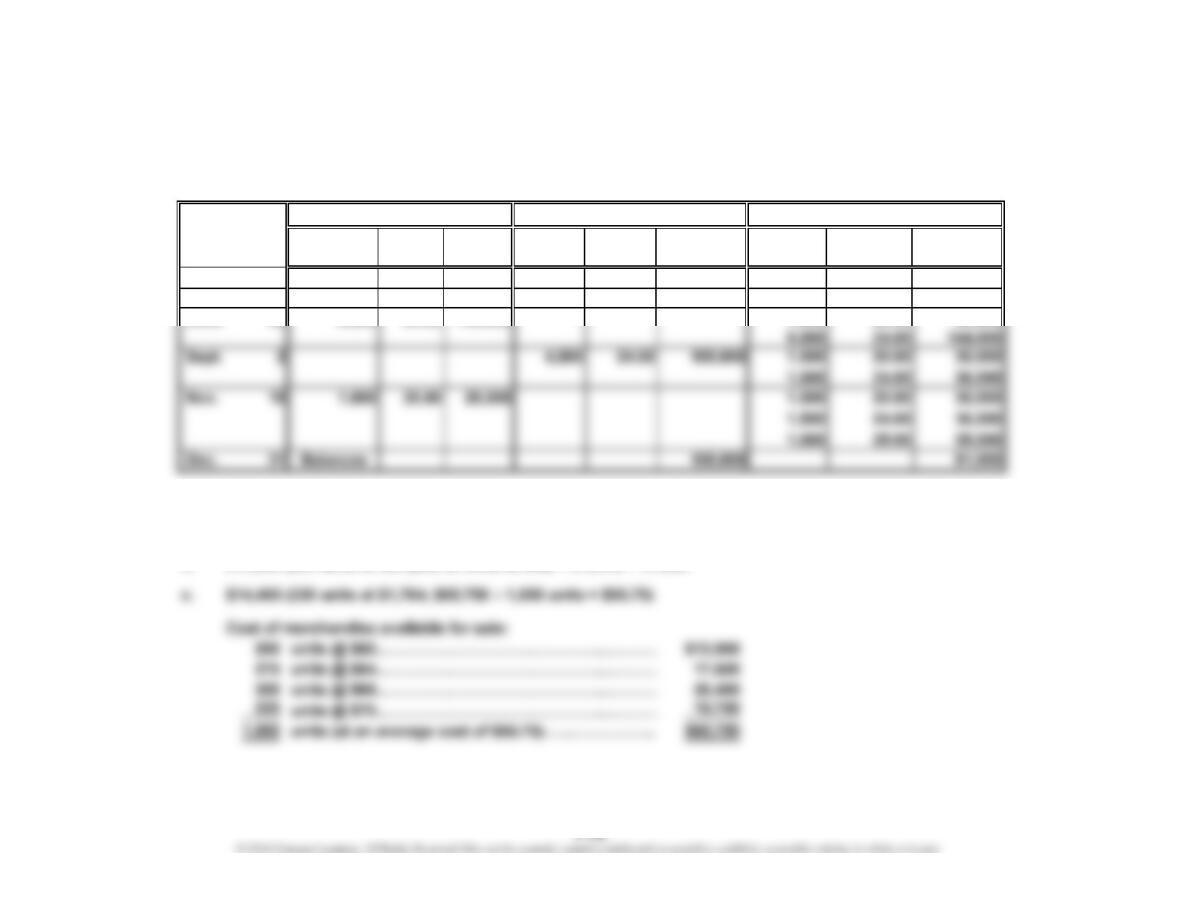

Ex. 7–13

Merchandise Merchandise

Inventory Method Inventory Sold

a. FIFO $6,228 $16,472

a. First-in, first-out:

Merchandise inventory:

98 units at $60…………………………………………………..…………… $ 5,880

units……………………………………………………..……………………

$22,700 – $6,228…………………………………….……………………………

104

units…………………………………………………………………………

$5,630

Merchandise sold:

$22,700 – $5,630……………………………………………..……………………

$17,070

c. Weighted average cost:

104 units at $56.75 ($22,700 ÷ 400 units)……………………………………

$22,700 – $5,902…………………………………………………………………

Cost

CHAPTER 7 Inventories

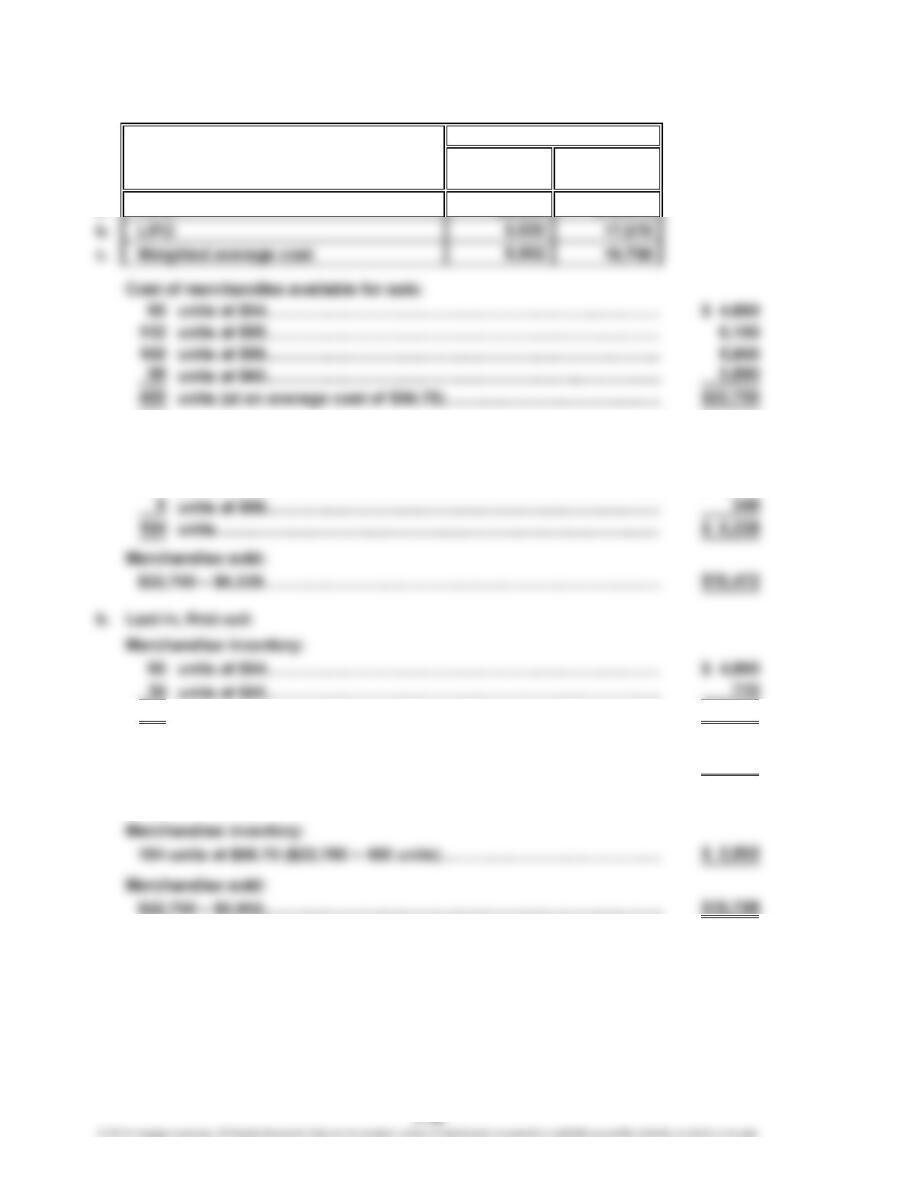

Ex. 7–14

a. 1. FIFO inventory > (greater than) LIFO inventory

3. FIFO net income > (greater than) LIFO net income

b. In periods of rising prices, the income shown on the company’s tax return

would be lower if LIFO rather than FIFO were used; thus, there is a tax advantage

of using LIFO.

Note to Instructors: The federal tax laws require that if LIFO is used for tax

purposes, LIFO must also be used for financial reporting purposes. This is

Ex. 7–15

Market

Value per

Cost Unit (Net

Inventory per Realizable

Quantity Unit Value) Cost Market LCM

80 $140 $125 $11,200 $10,000 $10,000

120 90 112 10,800 13,440 10,800

Ex. 7–16

The merchandise inventory would appear in the Current Assets section, as

follows:

Commodity

Aspen

Ash

Total

CHAPTER 7 Inventories

Ex. 7–17

a.

Merchandise inventory*…………………………………………

$5,200 understated

Current assets……………………………………………………

Total assets………………………………………………………

Owner’s equity……………………………………………………

b.

Cost of merchandise sold………………………………………

$5,200 overstated

Gross profit………………………………………………………

Net income………………………………………………………

c.

Cost of merchandise sold………………………………………

$5,200 understated

Gross profit………………………………………………………

Net income………………………………………………………

d. The December 31, 2017, balance sheet would be correct, since the 2016

Ex. 7–18

a.

Merchandise inventory*…………………………………………

$8,650 overstated

Current assets……………………………………………………

Total assets………………………………………………………

Owner’s equity……………………………………………………

b.

Cost of merchandise sold………………………………………

$8,650 understated

Gross profit………………………………………………………

Net income………………………………………………………

c.

Cost of merchandise sold………………………………………

$8,650 overstated

Gross profit………………………………………………………

Net income………………………………………………………

d. The December 31, 2017, balance sheet would be correct, since the 2016

Balance Sheet

Income Statement

Income Statement

Income Statement

Balance Sheet

Income Statement

CHAPTER 7 Inventories

Ex. 7–19

When an error is discovered affecting the prior period, it should be corrected. In

this case, the merchandise inventory account should be debited and the owner’s

Ex. 7–20

a. Apple: 112.1 {$87,846,000 ÷

[($776,000 + $791,000) ÷ 2]}

American Greetings: 3.8 {$741,645 ÷

[($179,730 + $208,945) ÷

2]}

CHAPTER 7 Inventories

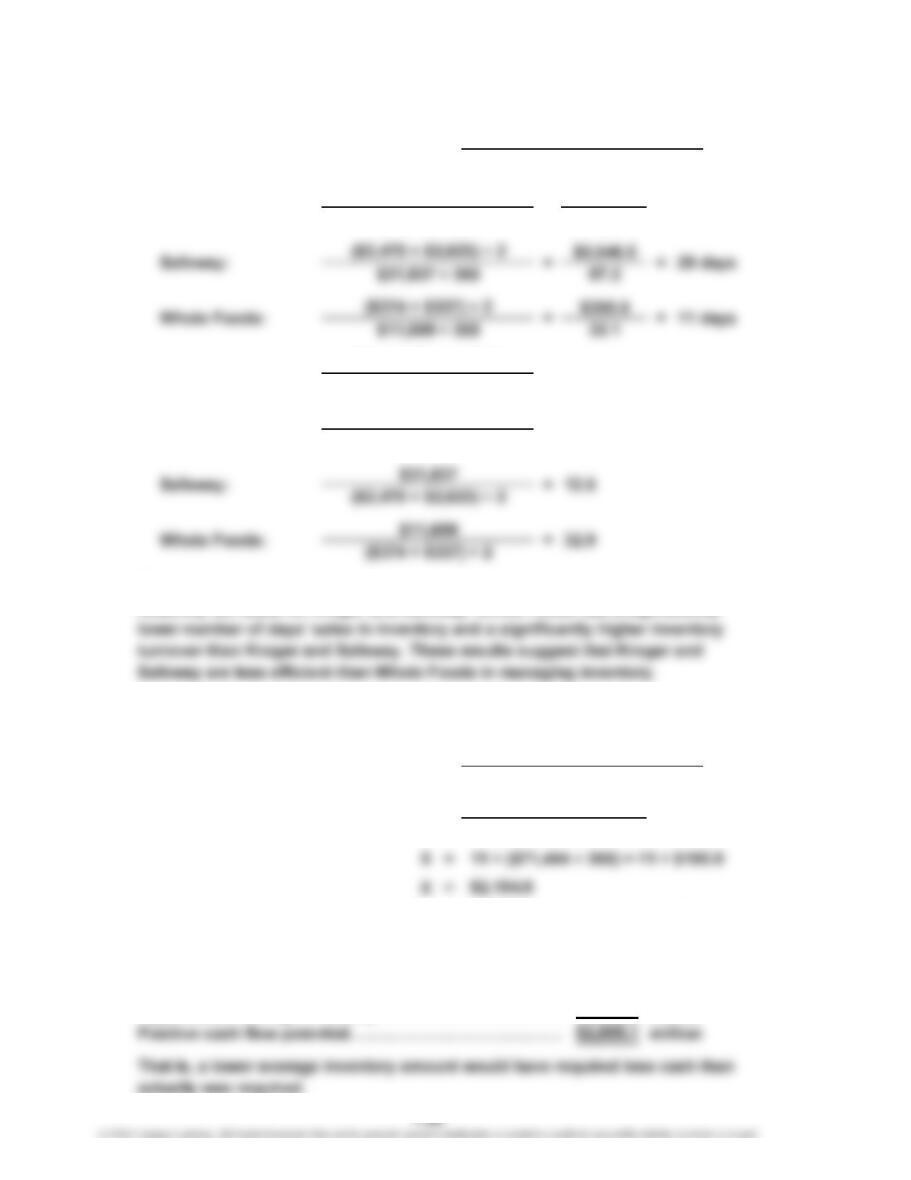

Ex. 7–21

$5,040.0

195.9

b. The number of days’ sales in inventory and the inventory turnover ratios are

relatively the same for Kroger and Safeway. Whole Foods has a significantly

c. If Kroger matched Whole Foods days’ sales in inventory, then its hypothetical

ending inventory would be determined as follows,

Thus, the additional cash flow that would have been generated is the difference

between the actual average inventory and the hypothetical average inventory,

as follows:

Actual average inventory……………………………………

…

$5,040.0 million

Hypothetical average inventory……………………………

…

2,154.9 million

($71,494 ÷ 365)

($5,114 + $4,966) ÷ 2

Inventory Turnover =

Average Inventory

11 days

Kroger: $71,494

=X

Number of Days’ Sales in Inventory

=

14.2

=

Cost of Goods Sold

= 26 days=

a.

Kroger: ($5,114 + $4,966) ÷ 2

$71,494 ÷ 365

Cost of Goods Sold ÷ 365

Average Inventory

Number of Days’ Sales in Inventory = Average Inventory

Cost of Goods Sold ÷ 365