CHAPTER 7 Inventories

Ex. 7-21 (Concluded)

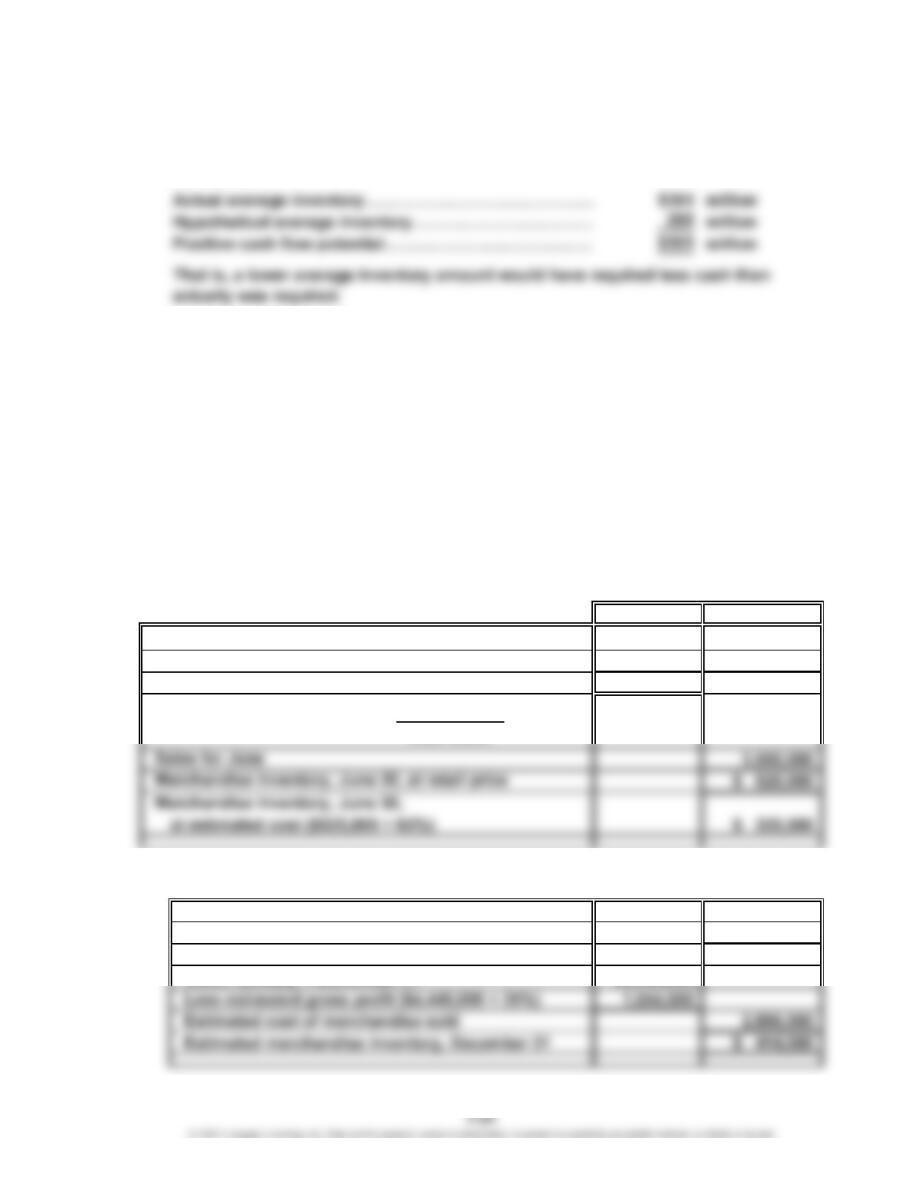

Thus, the additional cash flow that would have been generated is the difference

between the actual average inventory and the hypothetical average inventory,

as follows:

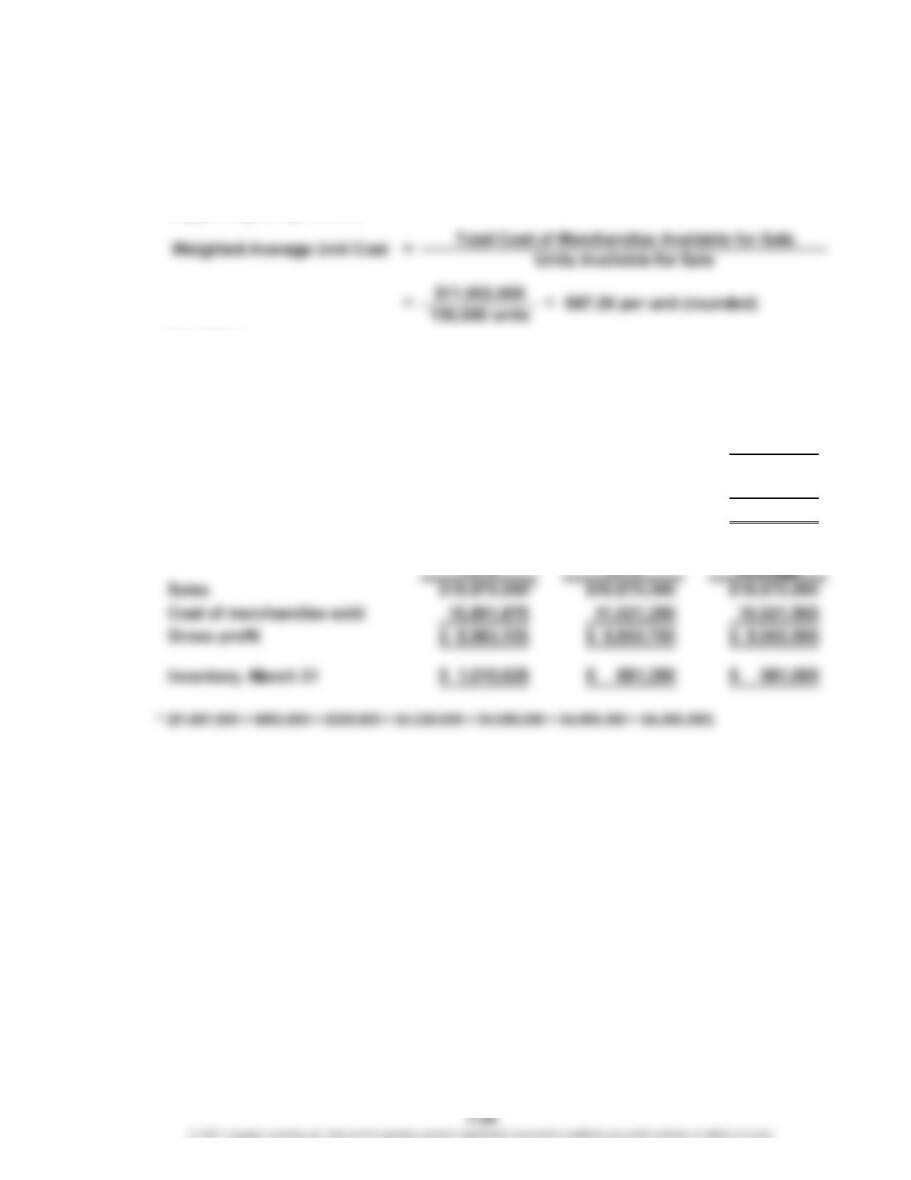

Appendix Ex. 7-22

$666,900 ($1,235,000 × 54%)

Appendix Ex. 7-23

$241,804 ($396,400 × 61%)

Appendix Ex. 7-24

$511,500 ($775,000 × 66%)

Appendix Ex. 7-25

Cost Retail

Merchandise inventory, June 1 $ 165,000 $ 275,000

Purchases in June (net) 2,361,500 3,800,000

Merchandise available for sale $2,526,500 $4,075,000

$2,526,500

Appendix Ex. 7-26

a. Merchandise inventory, January 1 $ 350,000

Purchases (net), January 1–December 31 2,950,000

Merchandise available for sale $3,300,000

Ratio of cost to retail price: = 62%

CHAPTER 7 Inventories

Appendix Ex. 7-26 (Concluded)

b. The gross profit method is useful for estimating inventories for monthly or

quarterly financial statements. It is also useful in estimating the cost of

merchandise destroyed by fire or other disasters.

CHAPTER 7 Inventories

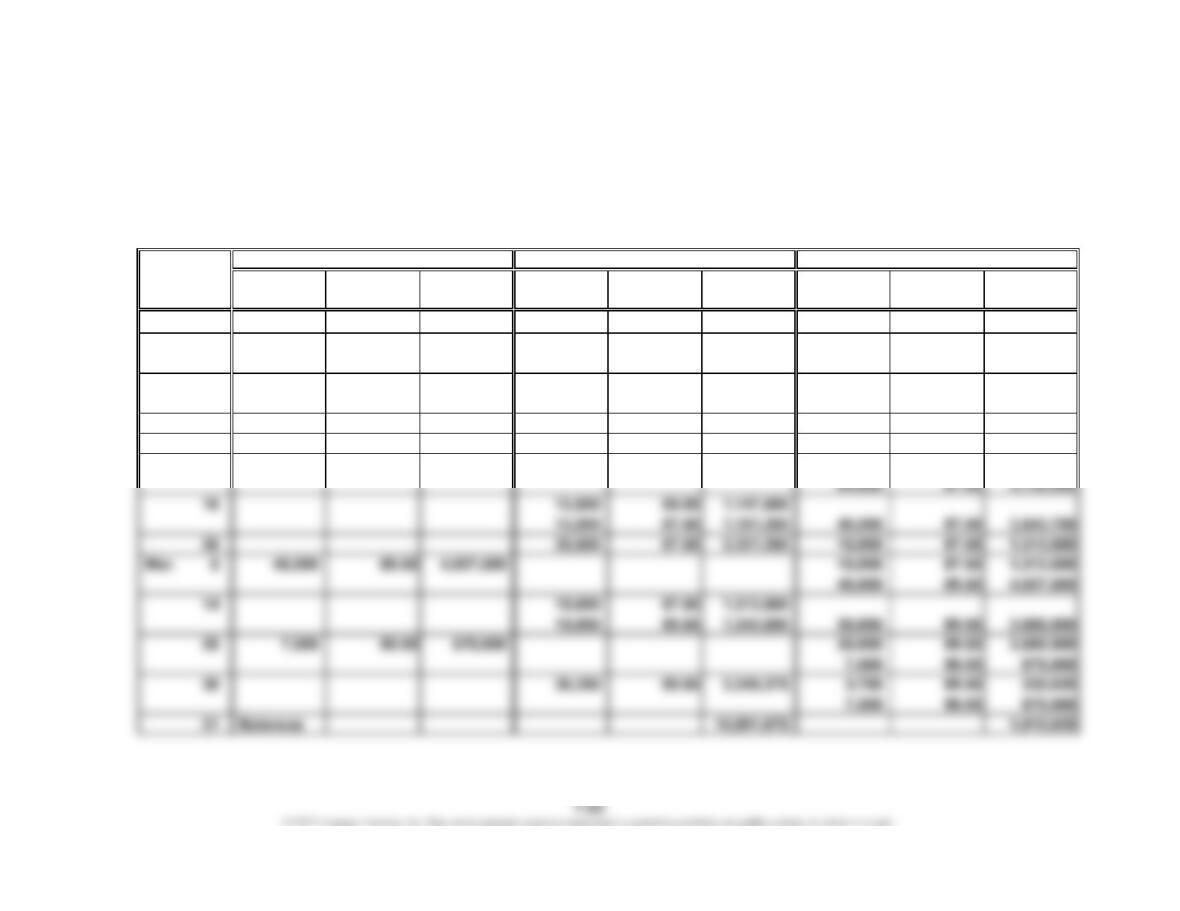

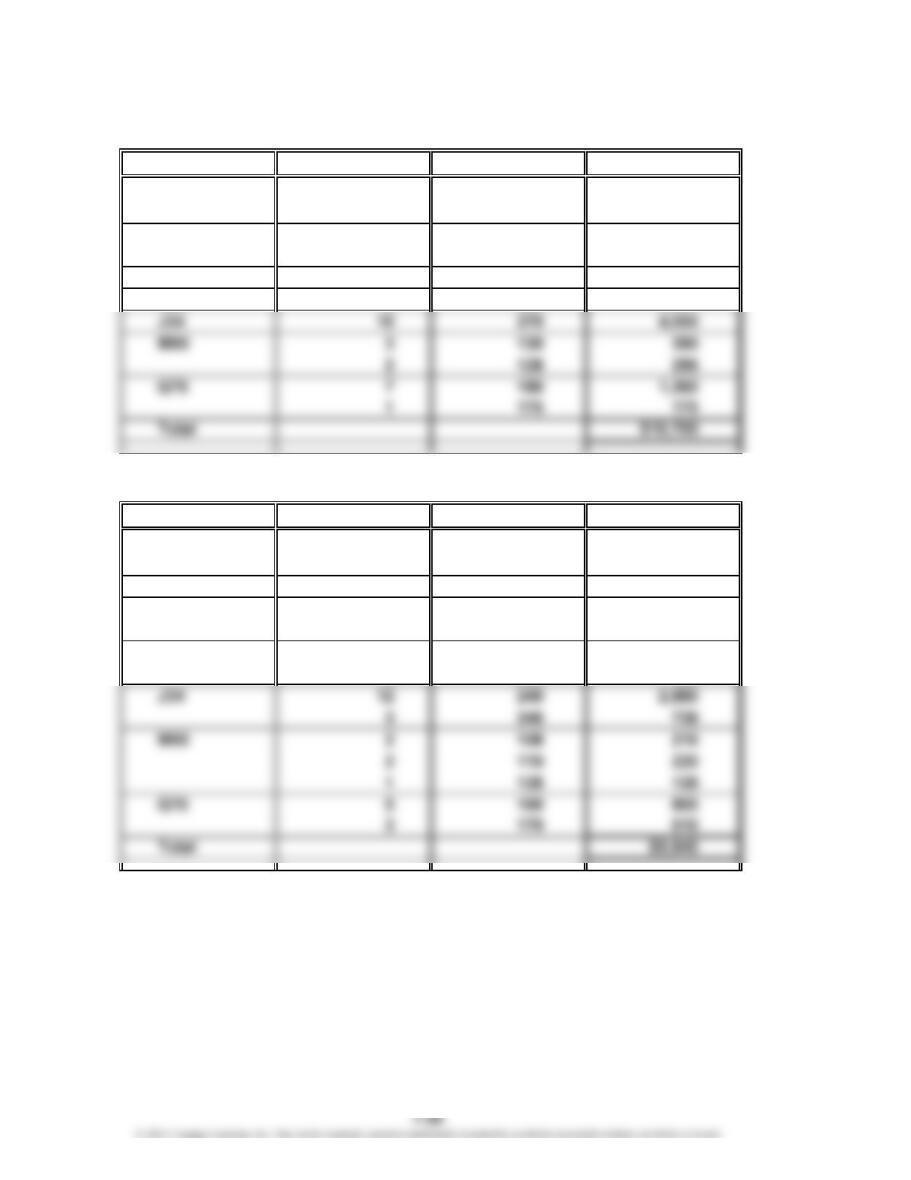

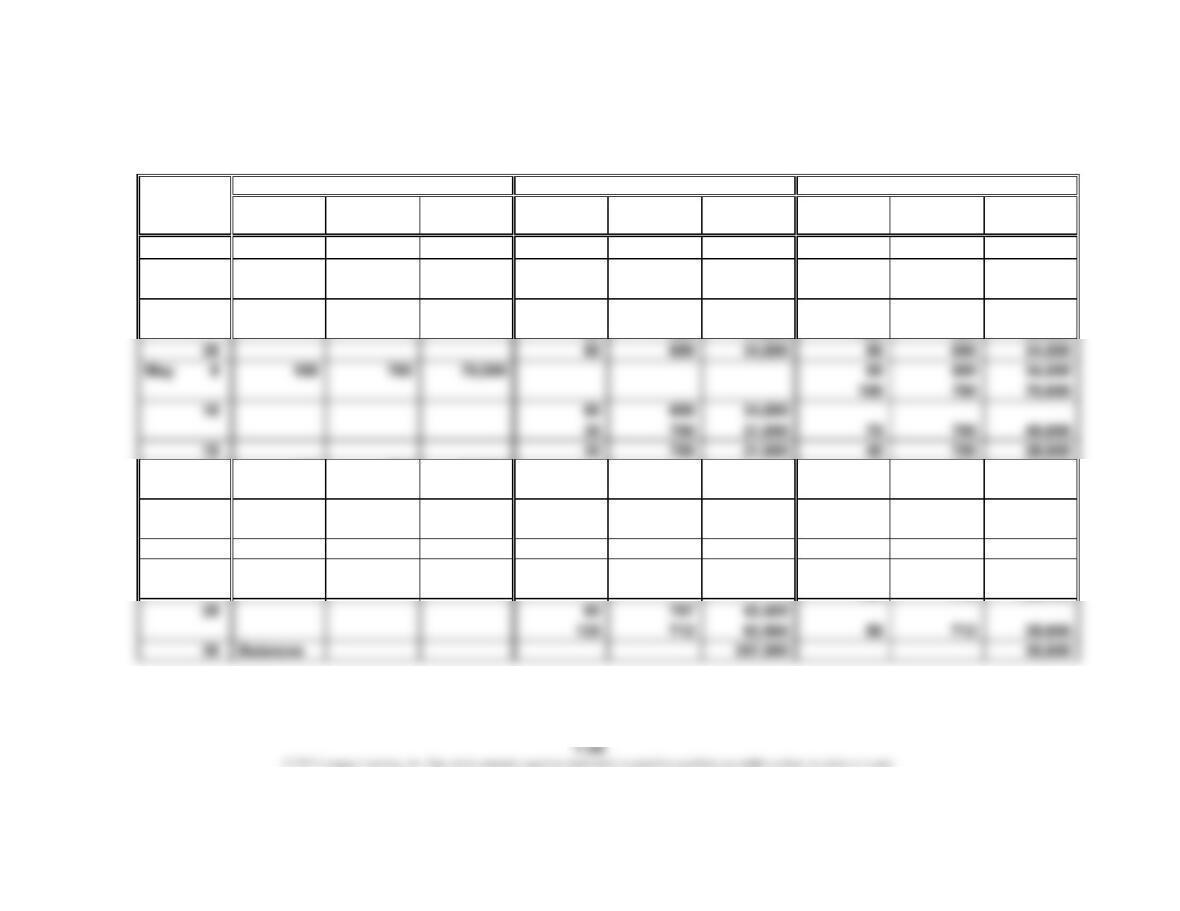

Prob. 7-1A

1.

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

Jan. 1 7,500 75.00 562,500

10 22,500 85.00 1,912,500 7,500 75.00 562,500

22,500 85.00 1,912,500

28 7,500 75.00 562,500

3,750 85.00 318,750 18,750 85.00 1,593,750

30 3,750 85.00 318,750 15,000 85.00 1,275,000

Feb. 5 1,500 85.00 127,500 13,500 85.00 1,147,500

10 54,000 87.50 4,725,000 13,500 85.00 1,147,500

PROBLEMS

Date

Purchases Cost of Merchandise Sold Inventory

CHAPTER 7 Inventories

Prob. 7-1A (Concluded)

2. Accounts Receivable 19,875,000

Sales 19,875,000

Cost of Merchandise Sold 10,891,875

Merchandise Inventory 10,891,875

* $19,875,000 = $1,687,500 + $562,500 + $225,000 + $4,320,000 + $4,080,000 + $4,800,000 + $4,200,000

3. $8,983,125 ($19,875,000 – $10,891,875)

4. $1,010,625 ($335,625 + $675,000)

*

CHAPTER 7 Inventories

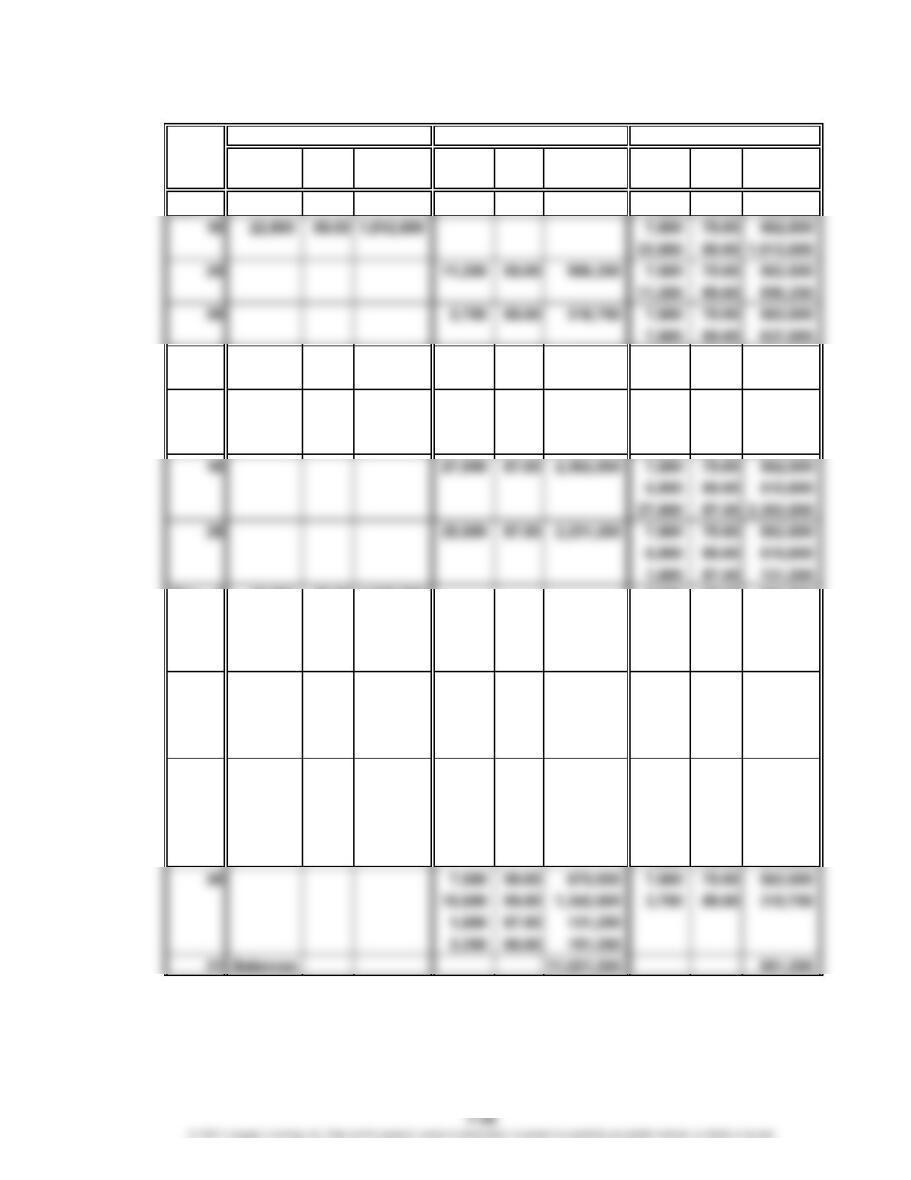

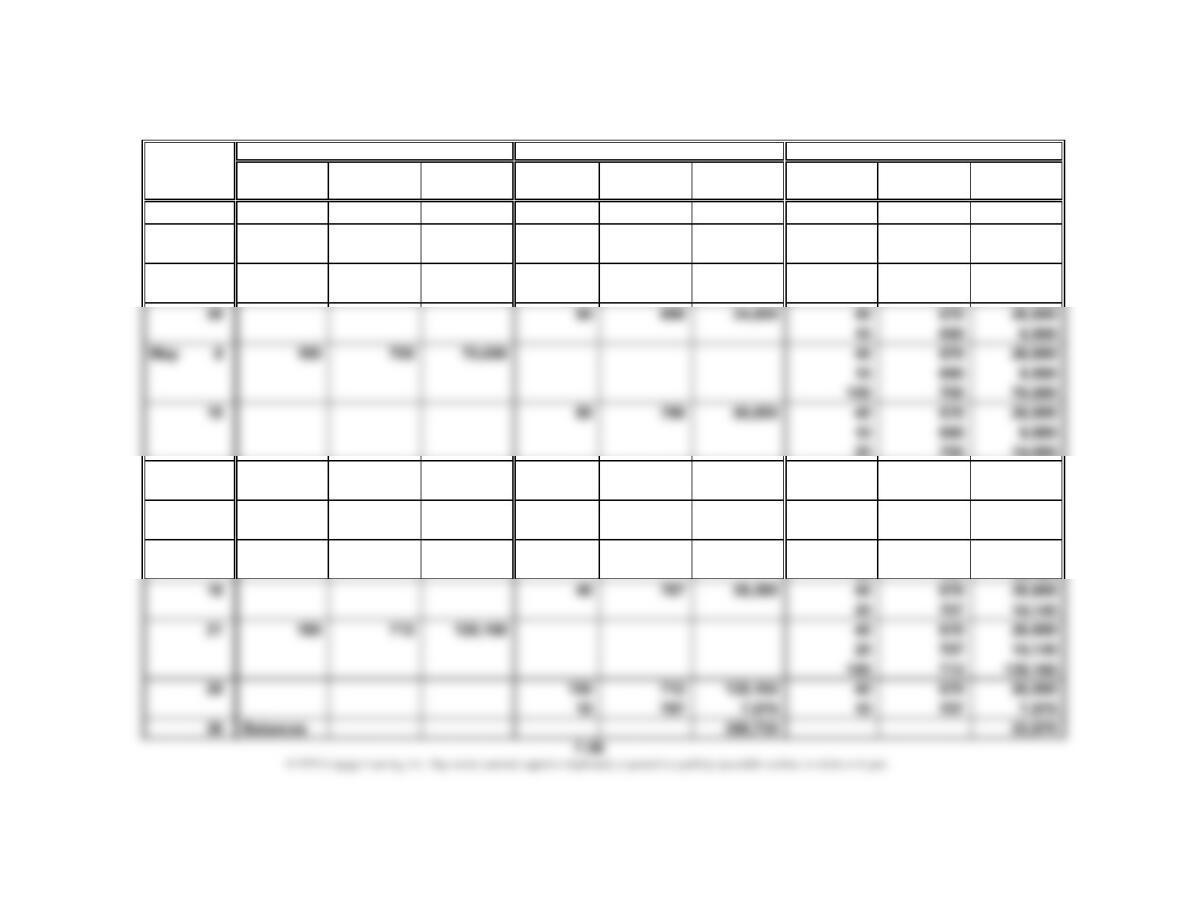

Prob. 7-2A

1.

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

Feb. 5 1,500 85.00 127,500 7,500 75.00 562,500

6,000 85.00 510,000

10 54,000 87.50 4,725,000 7,500 75.00 562,500

6,000 85.00 510,000

54,000 87.50 4,725,000

Mar. 5 45,000 89.50 4,027,500 7,500 75.00 562,500

6,000 85.00 510,000

1,500 87.50 131,250

45,000 89.50 4,027,500

14 30,000 89.50 2,685,000 7,500 75.00 562,500

6,000 85.00 510,000

1,500 87.50 131,250

15,000 89.50 1,342,500

25 7,500 90.00 675,000 7,500 75.00 562,500

6,000 85.00 510,000

1,500 87.50 131,250

15,000 89.50 1,342,500

Cost of Merchandise Sold Inventory

Date

Purchases

CHAPTER 7 Inventories

Prob. 7-2A (Concluded)

2. Total sales………………………………………………………………………

…

$19,875,000

Total cost of merchandise sold………………………………………………

…

11,021,250

Gross profit………………………………………………………………………

…

$ 8,853,750

* Total Sales = $19,875,000 = $1,687,500 + $562,500 + $225,000 + $4,320,000 + $4,080,000 +

*

CHAPTER 7 Inventories

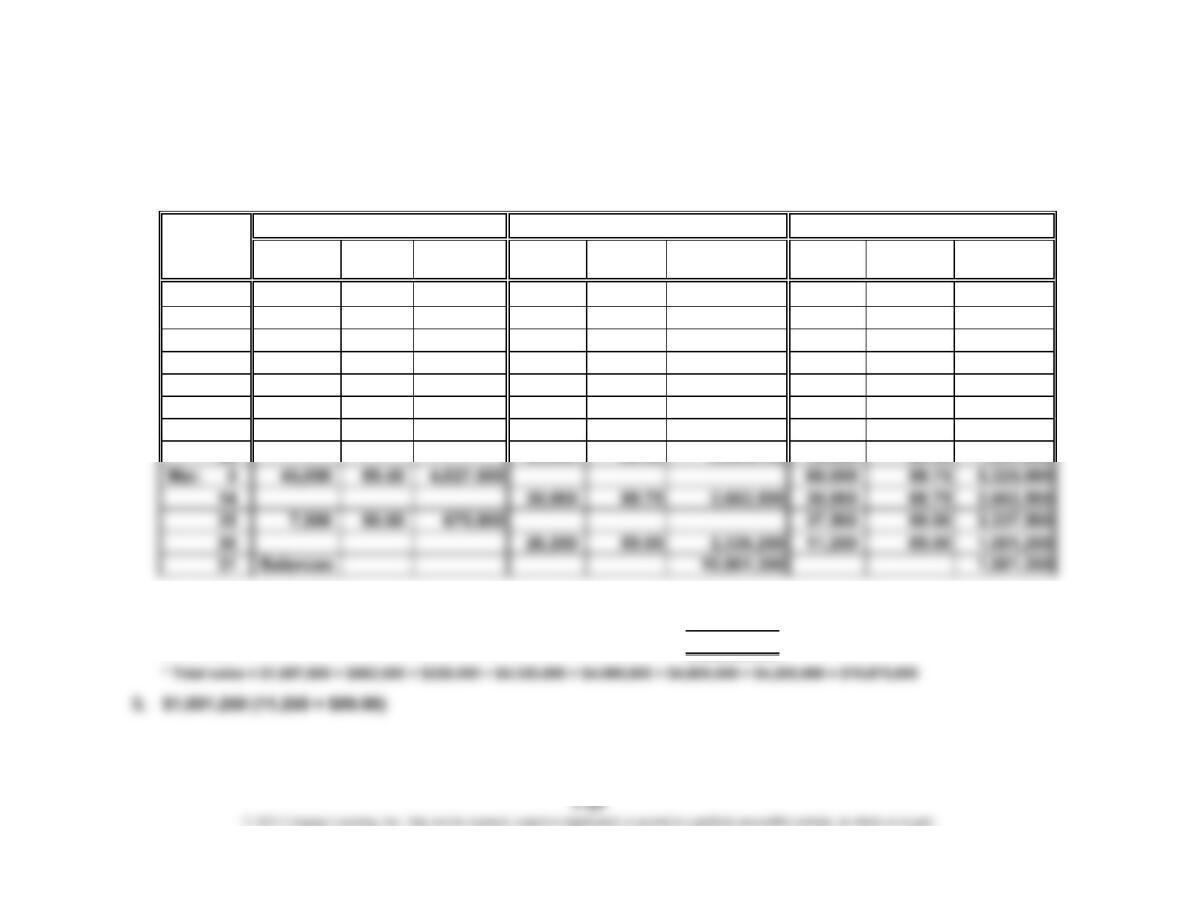

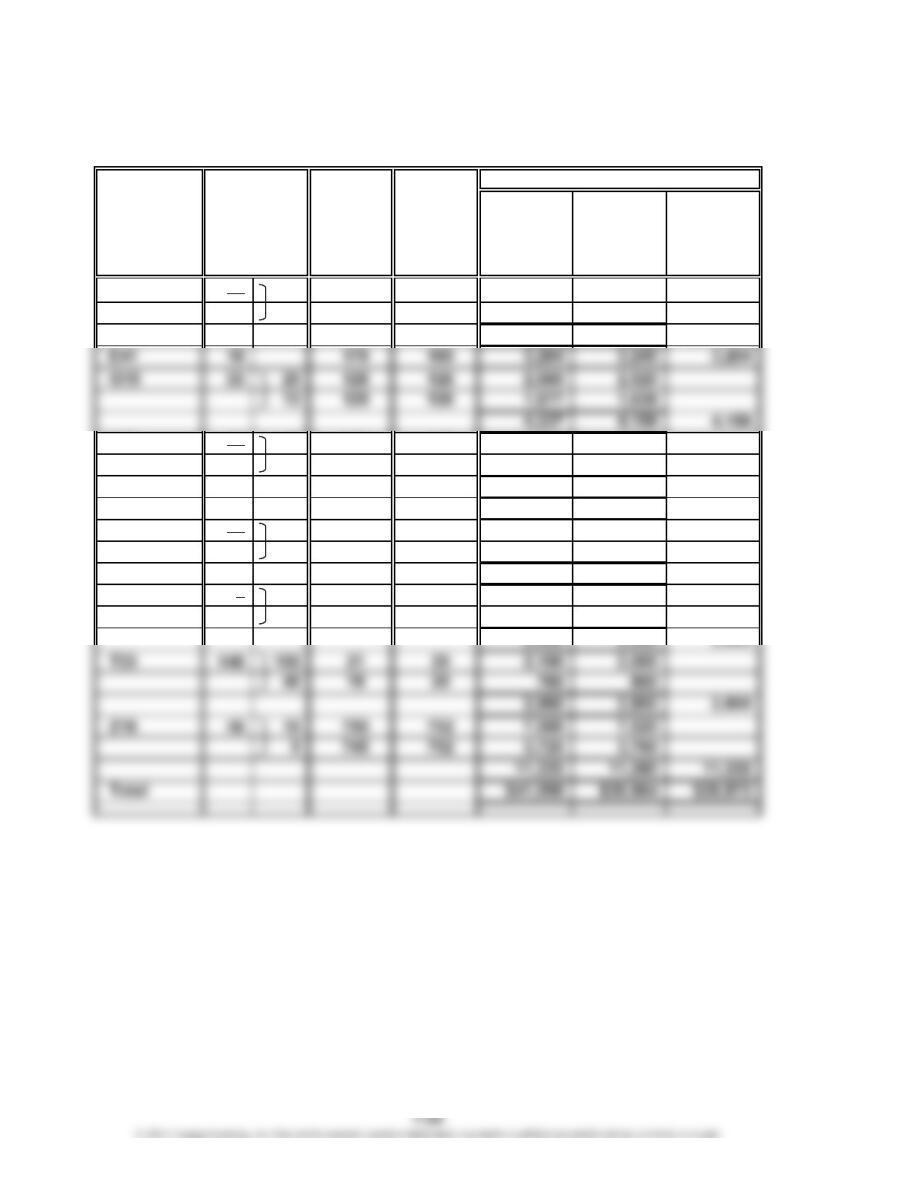

Prob. 7-3A

1.

Unit Total Total Total

Quantity Cost Cost Quantity Unit Cost Cost Quantity Unit Cost Cost

Jan. 1 7,500 75.00 562,500

10 22,500 85.00 1,912,500 30,000 82.50 2,475,000

28 11,250 82.50 928,125 18,750 82.50 1,546,875

30 3,750 82.50 309,375 15,000 82.50 1,237,500

Feb. 5 1,500 82.50 123,750 13,500 82.50 1,113,750

10 54,000 87.50 4,725,000 67,500 86.50 5,838,750

16 27,000 86.50 2,335,500 40,500 86.50 3,503,250

2. Total sales………………………………………………………………

…

$19,875,000

Total cost of merchandise sold………………………………………

…

10,901,250

Gross profit………………………………………………………………

…

$ 8,973,750

Cost of Merchandise Sold Inventory

Date

Purchases

*

CHAPTER 7 Inventories

Prob. 7-4A

1. First-In, First-Out Method

Merchandise inventory, March 31………………………………………

…

$ 1,010,625

Cost of merchandise sold………………………………………..………

…

10,891,875

Supporting computations

Cost of merchandise sold:

Beginning inventory, January 1…………………………………………

…

$ 562,500

Purchases……………………………………………………………………

…

11,340,000

Merchandise available

f

or sale……………………………………………

$11

,

902

,5

00

Ending inventory, March 31………………………………………………

…

1,010,625

Cost of merchandise sold……………………………………………..…

…

$10,891,875

* $1,912,500 + $4,725,000 + $4,027,500 + $675,000

2. Last-In, First-Out Method

…

Supporting computations

Inventory:

7,500 units @ $75.00…………………………………………………

…

$562,500

3,750 units @ $85.00…………………………………………………

…

318,750

11,250 units…………………………………………………….………

…

$881,250

Cost of merchandise sold:

…

…

f

$11

902

00

…

*

…

…

…

CHAPTER 7 Inventories

Prob. 7-4A (Concluded)

3. Weighted Average Cost Method

Inventory, March 31………………………………………………………… $ 981,000

Cost of merchandise sold…………………………………………………

…

10,921,500

Supporting computations

Inventory:

11,250 units × $87.20 = $981,000

Cost of merchandise sold:

Beginning inventory, January 1…………………………………………………..

.

$ 562,500

Purchases………………………………………………………………………………….

.

11,340,000

Merchandise available for sale……………………………………………………. $11,902,500

Ending inventory, March 31……………………………….……………………….. 981,000

Cost of merchandise sold…………………………………………………………… $10,921,500

4. Weighted

CHAPTER 7 Inventories

Prob. 7-5A

1. First-In, First-Out Method

Model Quantity Unit Cost Total Cost

A10 4 $ 76 $ 304

2 70 140

B15 6 184 1,104

2 170 340

E60 5 70 350

G83 9 259 2,331

2. Last-In, First-Out Method

Model Quantity Unit Cost Total Cost

A10 4 $ 64 $ 256

2 70 140

B15 8 176 1,408

E60 3 75 225

2 65 130

G83 7 242 1,694

2 250 500

CHAPTER 7 Inventories

Prob. 7-5A (Concluded)

3. Weighted Average Cost Method

Quantity Unit Cost*Total Cost

6 $ 70 $ 420

8 174 1,392

5 69 345

*Computations of unit costs:

A10: $70 = [(4 × $64) + (4 × $70) + (4 × $76)] ÷ (4 + 4 + 4)

B15: $174 = [(8 × $176) + (4 × $158) + (3 × $170) + (6 × $184)] ÷ (8 + 4 + 3 + 6)

E60: $69 = [(3 × $75) + (3 × $65) + (15 × $68) + (9 × $70)] ÷ (3 + 3 + 15 + 9)

G83: $253 = [(7 × $242) + (6 × $250) + (5 × $260) + (10 × $259)] ÷ (7 + 6 + 5 + 10)

J34: $258 = [(12 × $240) + (10 × $246) + (16 × $267) + (16 × $270)] ÷ (12 + 10 + 16 + 16)

M90: $121 = [(2 × $108) + (2 × $110) + (3 × $128) + (3 × $130)] ÷ (2 + 2 + 3 + 3)

Q70: $172 = [(5 × $160) + (4 × $170) + (4 × $175) + (7 × $180)] ÷ (5 + 4 + 4 + 7)

4. a. During periods of rising prices, the LIFO method will result in a lower cost

of inventory, a greater amount of cost of merchandise sold, and less net

income than the other two methods. For Dymac Appliances, the LIFO method

Model

A10

B15

E60

CHAPTER 7 Inventories

Prob. 7-6A

Market

Value per

Cost Unit (Net

Inventory per Realizable

Item Unit Value) Cost Market LCM

B12 38 30 $ 60 $ 57 $ 1,800 $ 1,710

8 59 57 472 456

2,272 2,166 $ 2,166

L88 18 10 563 550 5,630 5,500

8 560 550 4,480 4,400

10,110 9,900 9,900

N94 400 8 7 3,200 2,800 2,800

P24 90 80 22 18 1,760 1,440

10 21 18 210 180

1,970 1,620 1,620

R66 8 5 248 250 1,240 1,250

3 260 250 780 750

Quantity

Inventory Sheet

December 31

Inventory

Total

CHAPTER 7 Inventories

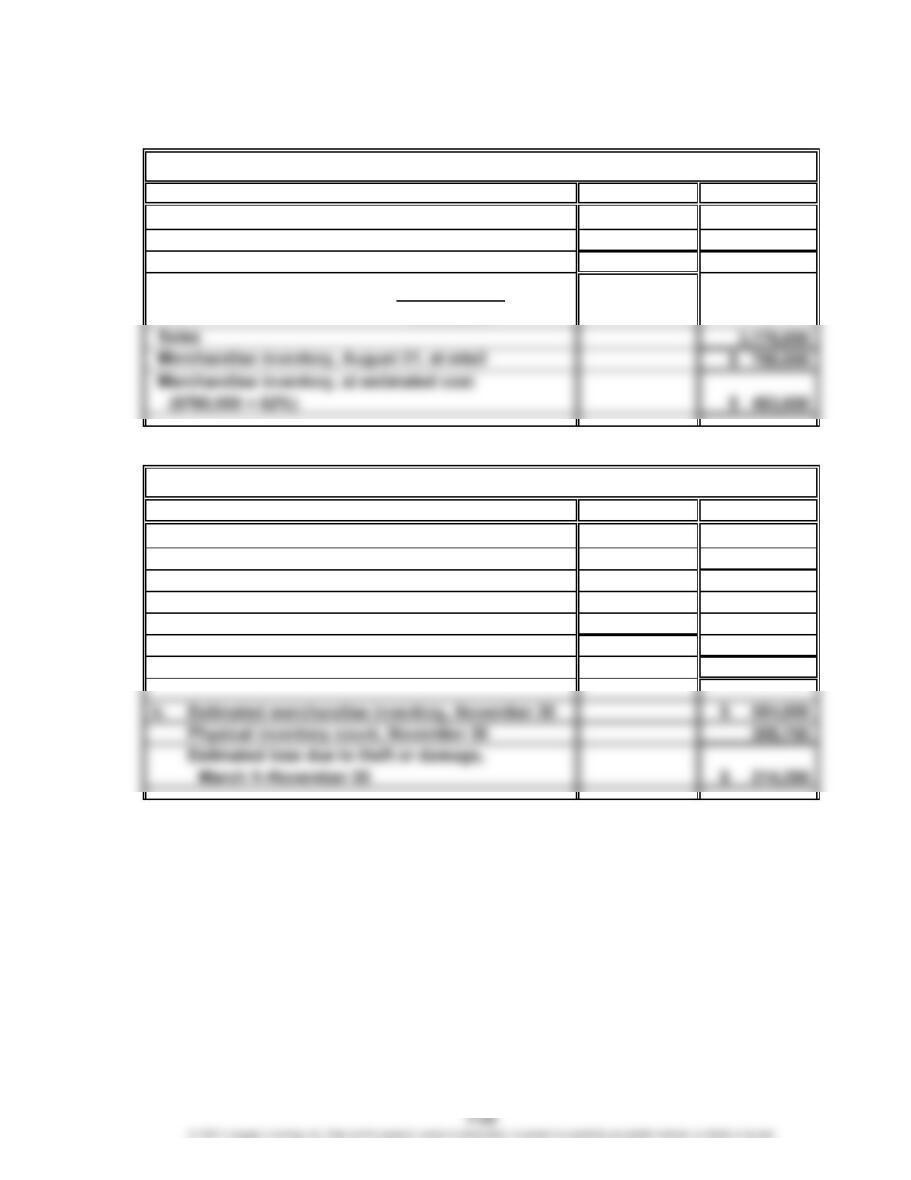

Appendix Prob. 7-7A

1.

Cost Retail

Merchandise inventory, August 1 $ 300,000 $ 575,000

Net purchases 2,149,000 3,375,000

Merchandise available for sale $2,449,000 $3,950,000

$2,449,000

$3,950,000

2.

Cost

a. Merchandise inventory, March 1 $ 880,000

Net purchases 9,500,000

Merchandise available for sale $10,380,000

Sales $15,800,000

Less estimated gross profit ($15,800,000 × 38%) 6,004,000

Estimated cost of merchandise sold 9,796,000

Estimated merchandise inventory, November 30 $ 584,000

Celebrity Tan Co.

Ranchworks Co.

Ratio of cost to retail price: = 62%

CHAPTER 7 Inventories

Prob. 7-1B

1.

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

Apr. 3 40 670 26,800

8 120 690 82,800 40 670 26,800

120 690 82,800

11 40 670 26,800

28 120 707 84,840 40 700 28,000

120 707 84,840

June 5 40 700 28,000

20 707 14,140 100 707 70,700

16 40 707 28,280 60 707 42,420

21 180 712 128,160 60 707 42,420

180 712 128,160

Date

Purchases Cost of Merchandise Sold Inventory

CHAPTER 7 Inventories

Prob. 7-1B (Concluded)

2. Accounts Receivable 611,800

Sales 611,800

Cost of Merchandise Sold 357,000

Merchandise Inventory 357,000

* $611,800 = $67,200 + $56,000 + $89,600 + $33,600 + $75,600 + $50,400 + $239,400

3. $254,800 ($611,800 – $357,000)

4. $35,600 (50 units × $712)

*

CHAPTER 7 Inventories

Prob. 7-2B

1.

Unit Total Unit Total Unit Total

Quantity Cost Cost Quantity Cost Cost Quantity Cost Cost

Apr. 3 40 670 26,800

8 120 690 82,800 40 670 26,800

120 690 82,800

11 60 690 41,400 40 670 26,800

60 690 41,400

20 700 14,000

19 20 700 14,000

10 690 6,900 40 670 26,800

28 120 707 84,840 40 670 26,800

120 707 84,840

June 5 60 707 42,420 40 670 26,800

Date

Purchases Cost of Merchandise Sold Inventory