7

Job Costing

Solutions to Review Questions

7-1.

Companies using a job order cost system are likely to be performing services or

7-2.

There are two primary reasons that cost allocation bases using direct labor are common.

7-3.

The Manufacturing Overhead account is used to accumulate the actual manufacturing

7-4.

A materials requisition is used to document the authorization for issuances of materials

7-5.

The job costing procedure is basically the same in both types of organizations, except that

7-6

The costs of a product using normal costing are:

7-7.

Mega has choices to make about the allocation base and the cost pools used to

7-8.

Improprieties in job costing are generally caused by one or more of the following: (1)

7-9.

Solutions to Critical Analysis and Discussion Questions

7-10.

Actual costing requires knowing the actual costs of overhead as well as the actual direct

7-11.

If materials costs are not properly assigned to jobs, management may later be misled in

7-12.

The allocation of overhead matters because decisions are made about individual

7-14.

Answers will vary.

7-15.

7-16.

7-17.

7-18.

Answers will vary. The steps might include:

7-19.

Answers will vary. Common responses are (labor) time, materials cost, wall area, and so

on.

7-20.

Answers will vary. In general, the answer is that this is not ethical. Although the “correct”

Solutions to Exercises

7-21. (30 min.) Assigning Costs to Jobs: Steve’s Cabinets.

a.

1.

Materials Inventory ………………………………………………….

80,000

Accounts Payable ………………………………………………..

80,000

Manufacturing Overhead Control ……………………………….

Materials Inventory ………………………………………………….

Accounts Payable ………………………………………………..

4.

Accounts Payable ……………………………………………………

80,000

Cash …………………………………………………………………..

80,000

Wages Payable ……………………………………………………

7.

Manufacturing Overhead Control ……………………………….

Cash …………………………………………………………………..

Manufacturing Overhead Control ……………………………….

Equipment ……………………………………………………….

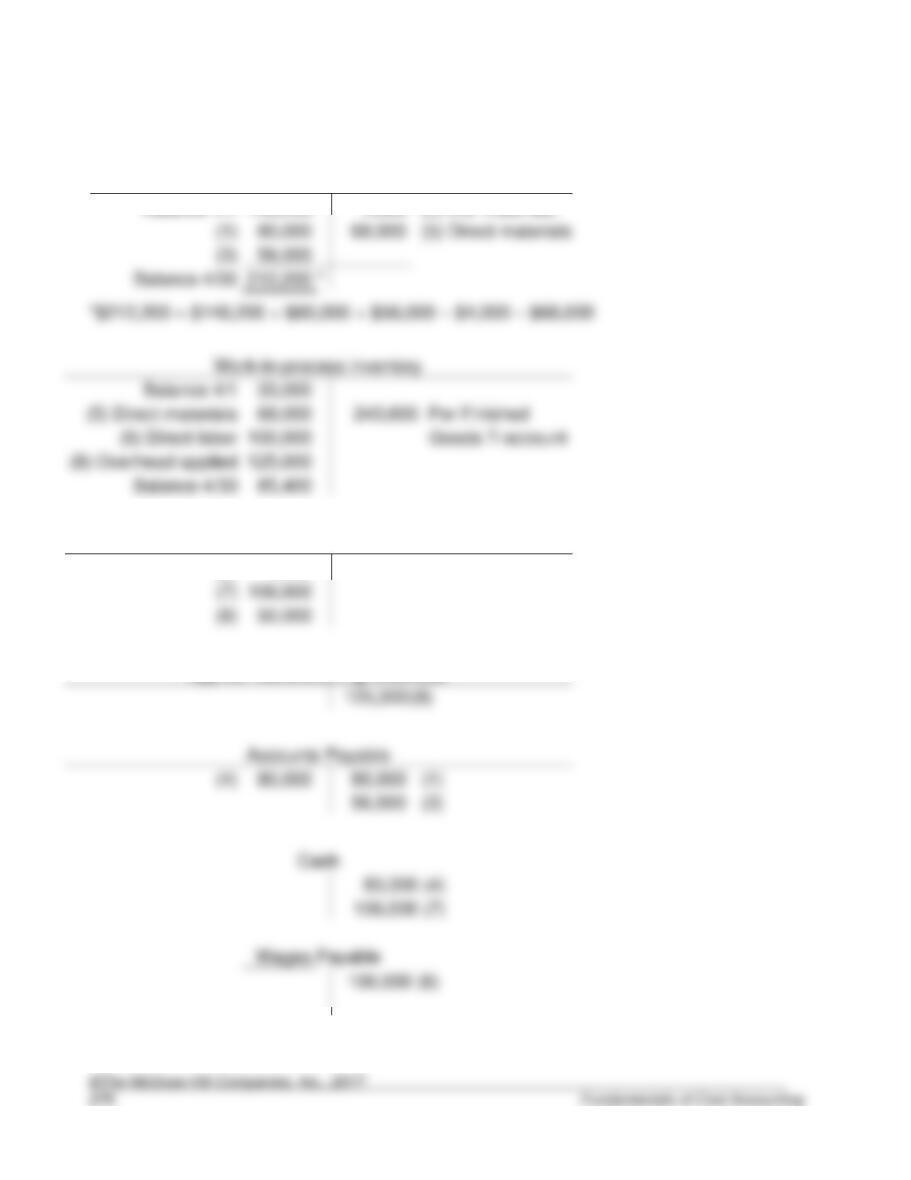

7-21. (continued)

b.

Materials Inventory

Balance 4/1

148,200

4,000

(2) Ind. materials

*

Per Finished

(8) Overhead applied

Manufacturing Overhead Control

(2)

4,000

(7)

Applied Manufacturing Overhead

(8)

(4)

(4)

(7)

(6)

7-21. (continued)

Accumulated Depreciation—

Property, Plant, and Equipment

Finished Goods Inventory

Balance 4/1

166,000

of Goods Sold

7-22. (20 min.) Assigning Costs to Jobs: Sunset Products.

a.

1.

Materials Inventory …………………………………………………..

30,000

Accounts Payable …………………………………………………

30,000

2.

Manufacturing Overhead Control ……………………………….

1,500

Materials Inventory ……………………………………………….

1,500

Materials Inventory …………………………………………………..

Accounts Payable …………………………………………………

4.

Accounts Payable …………………………………………………….

30,000

Cash …………………………………………………………………..

30,000

5.

Materials Inventory ……………………………………………….

Wages Payable …………………………………………………….

7.

Manufacturing Overhead Control ……………………………….

Cash …………………………………………………………………..

8.

52,500

Applied Manufacturing Overhead …………………………..

52,500

Manufacturing Overhead Control ……………………………….

Equipment ……………………………………………………….

7-22. (continued)

b.

Materials Inventory

Balance 3/1

13,500

1,500

(2) Ind. materials

45,000

*

Work-in-process inventory

Balance 3/1

24,750

(5) Direct materials

45,000

77,250

Per Finished

82,500

52,500

(8)

(4)

42,250

(7)

(6)

7-22. (continued)

Accumulated Depreciation—

Property, Plant, and Equipment

7,500

(9)

Balance 3/1

of Goods Sold

7-23. (20 min.) Assigning Costs to Jobs: Forest Components.

a.

1.

Materials Inventory ………………………………………………….

119,000

Accounts Payable ………………………………………………..

119,000

2.

Work-in-Process—Direct Materials …………………………….

117,600

Materials Inventory ……………………………………………….

117,600

Manufacturing Overhead Control ……………………………….

Materials Inventory ……………………………………………….

4.

Accounts Payable ……………………………………………………

119,000

Cash …………………………………………………………………..

119,000

5.

Materials Inventory ………………………………………………….

Work-in-Process—Direct Materials ………………………..

Cash …………………………………………………………………..

217,000

7.

Manufacturing Overhead Control ……………………………….

Accounts Payable ………………………………………………..

8.

Manufacturing Overhead Control ……………………………….

245,000

Accumulated Depreciation—Plant …………………………..

245,000

9.

Applied Manufacturing Overhead …………………………..

201,810

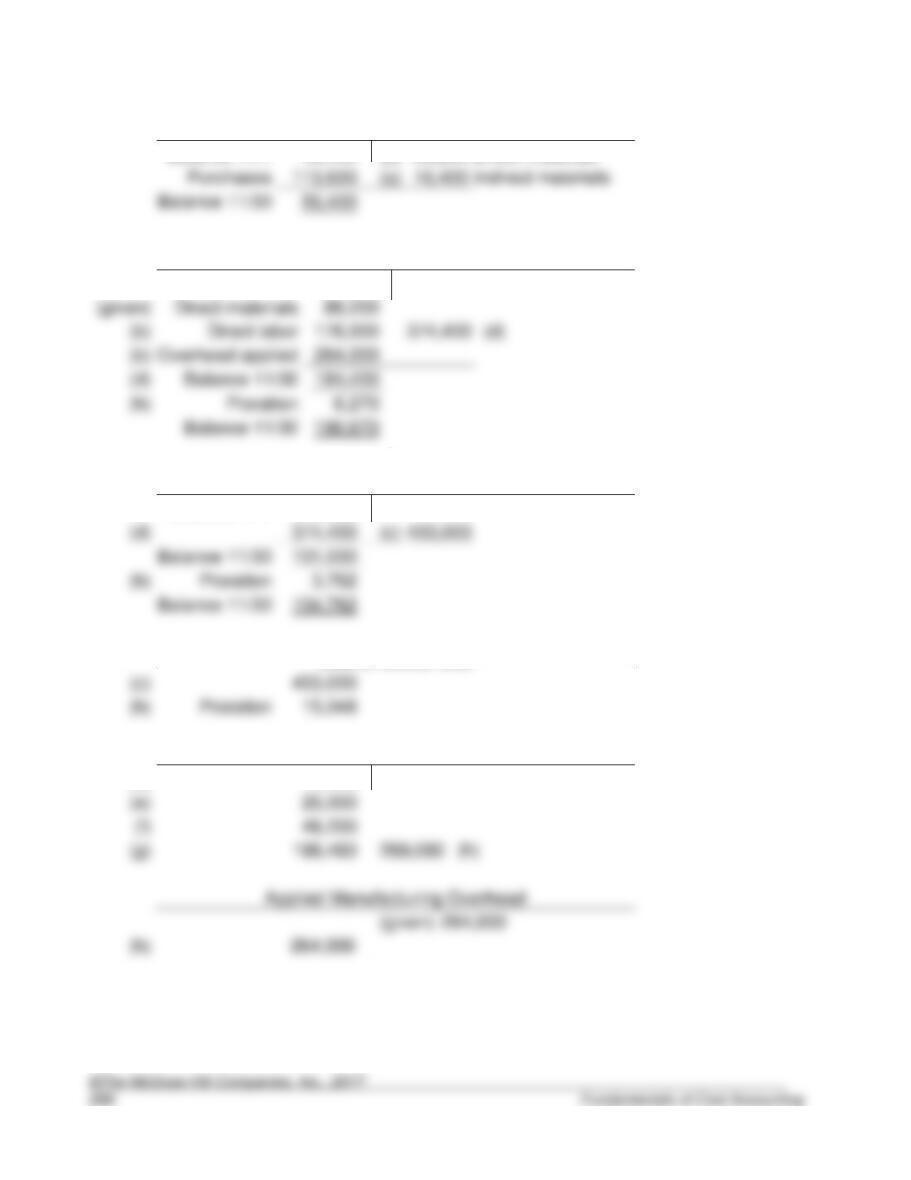

7-23. (continued)

b.

Materials Inventory

Balance 7/1

79,800

*

15,400

(3) Indirect materials

Work-in-process inventory

Balance 7/1

105,490*

(2) Direct materials

117,600

15,400

(5)

Finished Goods

120,400

Applied Manufacturing Overhead

Accounts Payable

120,400

(4)

(6)

7-23. (continued)

Accumulated Depreciation—

Property, Plant, and Equipment

Finished Goods Inventory

7-24. (25 min.) Assigning Costs to Jobs: Cardinals, Inc.

7-25. (25 min.) Assigning Costs to Jobs: Blake Corporation.

e.

7-26. (25 min.) Assigning Costs to Jobs: Pine Ridge Corporation.

7-27. (10 min.) Predetermined Overhead Rates: Dixboro Company.

Direct material used …………………………………….

$5,500,000c

Manufacturing overhead applied …………………..

7-28. (15 min.) Predetermined Overhead Rates: Southern Rim Parts.

a.

Job 301:

Job 303:

7-29. (10 Min.) Prorate Under- or Overapplied Overhead: Southern Rim Parts.

First, determine the percentage of overhead applied is in each account:

Applied

Overhead

% of Total

Applied

Finished goods ……………………..

(= $102,850 ÷ $467,500)

Cost of goods sold…………………

(= $327,250 ÷ $467,500)

7-30. (15 min.) Predetermined Overhead Rates: Aspen Company.

a.

$812,500

7-31. (10 Min.) Prorate Over- or Underapplied Overhead: Aspen Company.

First, determine the percentage of overhead applied in each account:

Applied

Overhead

% of

Total

Applied

Work in process inventory (Job 2–3) ..

$162,500

20%

(= $162,500 ÷ $812,500)

Finished goods (Job 2-2) ……………….

50

(= $406,250 ÷ $812,500)

7-32. (20 min.) Applying Overhead Using a Predetermined Rate: Mary’s

Landscaping.

Since Job No. 3318 is the only job in the account, the ending balance of the account must

equal the total cost of the job. We can find the account’s ending balance using the basic

cost equation:

BB + TI – TO = EB

=

=

Total cost

=

direct materials + direct labor + factory overhead

Direct materials

=

$28,700 – $3,375 – $2,700

7-33. (10 min.) Applying Overhead Using a Predetermined Rate: Turco Products.

The ending balance in Work in Process can be determined from the following T-acocunt:

Work-in-process inventory

Balance 9/1

70,200

Direct materials

421,200

832,000

To Finished Goods Inventory

*

7-34. (10 min.) Calculating Over- or Underapplied Overhead: Tom’s Tool & Die.

Application rate:

$714,000

= $10.50 per machine hour

68,000 hours

7-35. (20 min.) Predetermined Overhead Rates: Ethical Issues: Marine

Components.

a.

c. Using direct-labor cost as the base for applying overhead will lead to higher income for

7-36. (20 min.) Predetermined Overhead Rates: Ethical Issues: Marine

Components.

a.

c. Using machine hours as the base for applying overhead will lead to higher income for

7-37. (20 min.) Job Costing in a Service Organization: Arthur’s Olde Consulting

Corporation.

a. Beginning of month

Direct

Labor

Applied

Overhead

(@60%)

Total

b.

Direct

Labor

Applied

Overhead

Total

c. Overhead applied during month:

SY–400 ………………………………………………………

$ 15,120

SY–403 ………………………………………………………

7-38. (30 min.) Job Costing In A Service Organization: RCMP.

a.

Wages Payable

Work in Process

Cost of

Services Billed

Service Overhead Control

Applied Service O.H.

60,000

60,000d

72,000d

72,000b

b.

Royal Consulting and Mediation Practice

Income Statement

For the Month Ended August 31

Sales revenue …………………………………………….

$1,200,000

a

Cost of services billed ………………………………….

Subtract: Overapplied service overhead …………

Gross margin ……………………………………………..

Marketing and administration ………………………..

7-39. (30 min.) Job Costing In A Service Organization: Allocation Busters.

a.

Wages Payable

Work in Process

Cost of

Services Billed

Service Overhead Control

Applied Service O.H.

b.

Allocation Busters

Income Statement

For the Month Ended March 31

Sales revenue …………………………………………….

$550,000

a

Cost of services billed ………………………………….

Gross margin ………………………………………………

Marketing and administration ………………………..

7-40. (30 min.) Job Costing In A Service Organization: TechMaster.

a.

Wages Payable

Work in Process

Cost of

Services Billed

b.

TechMaster

Income Statement

For the Month Ended August 31

Sales revenue …………………………………………….

$175,000

a

Gross margin ……………………………………………..

Solutions to Problems

7-41. (15 min.) Estimate Machine-Hours Worked From Overhead Data: Melbourne

Company.

With $320,000 in fixed costs expected and 40,000 machine hours expected, the

application rate for the fixed costs was $8.00 per machine hour (= $320,000 ÷ 40,000

hours).

7-42. (25 min.) Estimate Hours Worked From Overhead Data: Capitol, Inc.

115,050 direct labor-hours were worked. With $702,000 in fixed costs expected and

117,000 direct-labor-hours expected, the application rate for the fixed costs was $6.00 per

7-43. (40 min.) Assigning Costs—Missing Data.

7-44. (50 min.) Assigning Costs—Missing Data.

Materials Inventory

Balance 11/1

45,400

(a)

86,200

Direct materials

(a)

16,400

Indirect materials

56,400

Work-in-Process Inventory

Balance 11/1

32,600

(given)

(b)

(b)

Overhead applied

(h)

Finished Goods Inventory

Balance 11/1

129,600

(c)

Balance 11/30

(h)

Cost of Goods Sold

(h)

15,048

Manufacturing Overhead Control

(a)

16,400

(e)

26,000

48,200

(g)

(h)

(given)

(h)

7-44. (continued)

Wages Payable

(b)

(e)

Sales Revenue

(given)

(a) From the work in process account, we obtain the $86,200 in direct materials issued.

The beginning balance equals the ending balance of $56,400 minus the increase of

$11,000 equals $45,400. The unaccounted balance represents indirect materials and is

determined as:

(b) Let X = Direct labor costs

150% X

150% X

=

180% X

=

180% X

=

101,000 + 28,600

Finished Goods BB

=

$101,000 + $403,000 – $129,600

Work in process EB

=

$32,600 + $86,200 + $176,000 + $264,000 – $374,400

(e)

Indirect labor

=

=

$202,000 – $176,000

7-44. (continued)

7-45. (40 min.) Analysis Of Overhead Using A Predetermined Rate: Kansas

Company.

Direct materials …………………………………………..

Direct labor …………………………………………………

*

$220,500.

Supplies …………………………………………………….

Indirect labor wages ……………………………………

Factory facilities ………………………………………….

f. Credit it to cost of goods sold. The amount is clearly not material (0.1% of cost of

goods sold), so it is not worth the effort involved in prorating.

Overapplied Overhead …………….

$0

Cost of Goods Sold…………………

*$2,940,000 – $3,000

7-46. (40 min.) Analysis Of Overhead Using A Predetermined Rate: Script

Company.

b.

$890,300.

Beginning balance ………………………………………

Overhead applied ………………………………………..

*The wage rate for direct labor is $48.00 per hour. $48.00 x 8,400 hours = $403,200.

**$100.00 x 8,400 direct labor-hours.

e.

$826,800.

Supplies …………………………………………………….

$ 184,080

Factory facilities ………………………………………….

Underapplied Overhead ………….

f. In this case, the underapplied overhead is relatively large (it is greater than 10% of

cost of goods sold, so the company might consider it material and decide to prorate

Direct Labor ……………………………………………….

($36 per hour x 300 hours)

Manufacturing Overhead ……………………………..

($18 per hour x 300 hours)

Total Cost of Ending Work in

7-47. (30 min.) Finding Missing Date: BackupsRntUs

a. March 31: Ending Work-in-process inventory:

—only one job is remaining in ending Work-in-process inventory.

b. Direct materials purchased during March:

Since the accounts payable account is used only for direct material purchases, the

month’s purchases can be determined from analyzing the accounts payable account:

d. Cost of goods sold during March:

Beginning Finished

Goods Inventory

+

Cost of Goods

Manufactured

–

Cost of

Goods Sold

=

Ending Finished

Goods Inventory

+

–

=

Cost of Goods Sold

Cost of

7-48. (30 min.) Cost Accumulation—Service: Youth Athletic Services.

T-accounts (Not required—see next page for income statement)

Wages, Salaries,

and Accounts

Payable

Managing Direct

Labor Cost

Officiating

Direct Labor Cost

Training Direct

Labor Cost

Dispute

Resolution

Direct Labor Cost

Unassigned

Labor Cost

4,800

1,200

1,875

1,350

375

Cost

7-48. (continued)

Income Statement

Youth Athletic Services

Income Statement

For Month Ending July 31

Managing

Officiating

Training

Dispute

Resolution

Total

Revenue …………………………………………………….

$6,950

$7,900

$3,000

$1,000

$18,850

Cost of Services:

$4,800

$1,200

$1,875

$1,350

1,525

2,175

$6,709

$3,471

$3,125

$1,718

Department margin ……………………………………..

$ 241

$4,429

$(125)

Less other costs:

Operating profit …………………………………………..

Total hours

640 hours worked

(including idle time)

7-48. (continued)

7-49. (25 min.) Job Costs—Service Company: UP Payroll Services.

a.

Dune Motors

Jake’s Charters

Mission Hospital

Unassigned

Costs (not

required)

Total

Revenue ……………………………………………………….……….

$384,000

$115,200

$192,000

$691,200

(= 3,000 x $128)

(= 900 x $128)

(= 1,500 x $128)

(= 3,000 x $48)

(= 900 x $48)

(= 1,500 x $48)

(= 600 x $48)

7-49. (continued)

b.

UP Payroll Services

Income Statement

For Month Ending July 31

Revenue from clients …………………………………….

$691,200

Less cost of services to clients:

Less other costs:

7-50. (50 min.) Job Costs In A Service Company: Pete’s Patios.

Materials Inventory

Balance 9/1 (given)

11,040

192

Indirect Materials

Requisition

Job PP–24

(c)

Job PP–30

(e)

10,872

Finished Goods Inventory

19,616

26,886

=

$2,038 + $1,280 + $768 + $3,360 + [50% ($768 + $3,360)]

$2,720 Direct Labor + ($2,720 x 50%) Applied Overhead

=

$4,080.

=

$3,190 + $2,720 + 50%($2,720)

=

$1,296 + $8,000 + $4,000

Transfer of Job PP-30: Beginning Inventory Cost + Current Cost

=

Balance 1/1 ($4,704 +

6,600

7-50. (continued)

f.

New Job Cost = Current Charges to WIP less Current Charges for Jobs PP-24 and

PP–30:

=

Current Materials + Direct Labor + Overhead – Job PP-24 Current Cost

7-51. (55 min.) Tracing Costs In A Job Company: Apex Manufacturing.

a.

(1)

Materials Inventory ……………………………………………….

75,180

Accounts Payable ……………………………………………..

75,180

(2)

Manufacturing Overhead ……………………………………….

Materials Inventory …………………………………………….

(3)

Accounts Payable …………………………………………………

75,180

Cash …………………………..…………………………………..

75,180

(4)

Work in Process—Direct Materials ………………………….

Materials Inventory …………………………………………….

(5)

Payroll ……………………………………………………….……….

Payroll Taxes Payable ……………………………………….

18,900

Cash …………………………..…………………………………..

39,900

(6)

Payroll ……………………………………………………….……….

Fringe Benefits Payable ……………………………………..

29,400

(7)

Work in Process (60% x $88,200) …………………………..

52,920

Manufacturing Overhead (30% x $88,200) ……………….

26,460

Administrative and Marketing Costs (10% x $88,200) ..

Payroll ($29,400 + $58,800) ………………………………..

(8)

Manufacturing Overhead ……………………………………….

45,360

Cash …………………………..…………………………………..

(9)

Work in Process—Overhead ($52,920 x 175%) ………..

92,610

Applied Manufacturing Overhead………………………..

92,610

(10)

Manufacturing Overhead Control…………………………….

24,150

24,150

7-51. (continued)

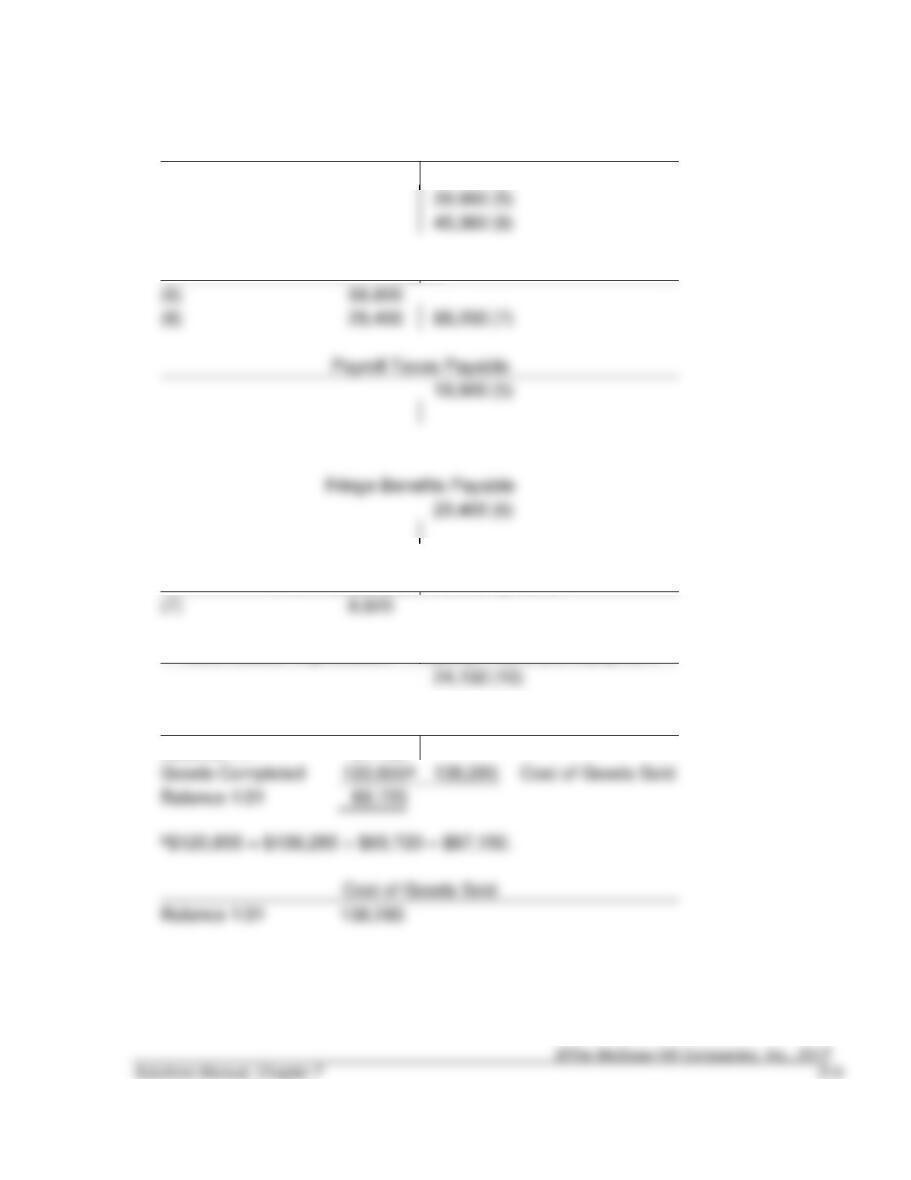

b.

Materials Inventory

Balance 1/1

77,805

2,100

(2)

(1)

75,180

(4)

Balance 1/31

a

Goods

(4) Direct Materials

(9) Overhead Applied

Manufacturing Overhead Control

(2)

2,100

(7)

26,460

24,150

92,610

(9)

75,180

75,180

(1)

7-51. (continued)

Cash

75,180

(3)

39,900

(5)

45,360

(8)

Payroll

(5)

58,800

(6)

(7)

(5)

(6)

Administrative and Marketing Costs

(7)

8,820

Accumulated Depreciation—Property, Plant, and Equipment

24,150

(10)

Finished Goods

Balance 1/1

87,150

Goods Completed

a

Balance 1/31

Balance 1/31

7-52. (50 min.) Cost Flows Through Accounts: Brighton Services

a. T accounts.

Materials Inventory

137,200

(1a)

(1b)

(1c)

Wages Payable

490,000

(2a)

312,400

(2b)

197,600

(2c)

(Actual)

62,000

(3a)

(3b)

(3c)

(Actual)

104,000

(4a)

(4b)

(4c)

7-52. (continued)

Finished Goods Inventory

b. Total Direct Labor Costs = $4,000,000.

7-52. (continued)

c. T accounts

Materials Inventory

137,200

(1a)

(1b)

(1c)

Wages Payable

490,000

(2a)

312,400

(2b)

197,600

(2c)

Variable Manufacturing Overhead*

(Actual)

(Applied)

62,000

38,220

(3a)**

(3b)

(3c)

(Applied)

89,180

(4a)***

(4c)

27,200

(5) Underapplied

7-52. (continued)

Work-in-Process Inventory

(1)

324,200

754,600

(a)

(b)

(3)

(4)

182,000

(1) = the sum of the amounts (1a) + (1b) + (1c)

Finished Goods Inventory

(a)

(b)

(5)

d.

Actual

Normal

Sales Revenue ……………………………………………

$1,400,000

$1,400,000

Less Cost of Goods Sold ………………………………

Gross Margin ………………………………………………

Less:

(Under-) Overapplied Overhead ……………………

Marketing and Administrative Costs ………………

7-53. (60 min.) Show Flow Of Costs To Jobs: Kim’s Asphalt.

a.

1.

Payment received on account

Cash …………………………………………………………………………….

12,500

Accounts receivable ……………………………………………………

12,500

2.

Inventory purchase

Materials and equipment inventory …………………………………..

Accounts payable ……………………………………………………….

3.

Billing

Accounts receivable ……………………………………………………….

Sales revenue ……………………………………………………………

Cash …………………………………………………………………………….

Accounts receivable ……………………………………………………

75,000

4.

Indirect labor

Manufacturing overhead—Indirect labor …………………………...

650

Wages payable …………………………………………………………..

650

5.

Indirect materials issued

Manufacturing Overhead …………………………………………………

155

Materials and equipment inventory ………………………………..

155

6.

Overhead and advertising

Selling costs—Advertising ……………………………………………….

600

Cash ………………………….. …………………………..………………..

Accumulated Depreciation ……………………………………………

450

7.

Charges to Work in Process

[$3,000 + $4,800 + $4,600 + $2,900] …………………………….

[$4,500 + $6,750 + $5,900 + $1,600] …………………………….

Work in process—overhead applied [30% x $18,750] …………

Materials inventory ……………………………………………………..

Wages payable …………………………………………………………..

18,750

Cost of installations completed and sold …………………………...

Note: No finished goods inventory account is required.

7-53. (continued)

b.

Overhead analysis:

Applied (Entry 7) ………………………………………

$5,625

Incurred

Entry 4 …………………………………………………

Entry 5 …………………………………………………

Entry 6 …………………………………………………

c. Inventory balances

Materials and Equipment Inventory

Balance 5/1

36,000

15,300

(7)

(2)

(5)

Balance 5/31

Work-in-process inventory

Balance 5/1

119,550

*

Current charges (7)

(8) Job 33

Balance 5/31

(8)

overhead

Balance 5/31

7-54. (70 min.) Reconstruct Missing Data: Toledo Farm Implements.

This is a challenging problem. We put the work in process account for May on the

board for the “big picture,” then solve for each item in the account as follows:

Work-in-Process

(a)

Balance, beginning

172,400

(b)

Direct materials

140,628

107,000

Transferred to

finished goods

(d)

(c)

Direct labor

135,400

408,028

Disaster loss

(f)

(e)

Overhead applied

66,600

Balance, ending

–0–

The calculations are shown below. We usually present these using both T-accounts

and the following formulas.

(a) Given

(b)

Direct materials

=

Beginning inventory + Purchases – Ending inventory – Indirect

materials

=

=

$140,628

*Purchases

=

Accounts payable, ending + Cash payments – Accounts

payable, beginning

=

=

$132,800

( c)

Direct labor

=

Payroll – Indirect labor

=

=

$135,400

=

=

$107,000

7-54. (continued)

(e)

Overhead applied

=

Ending manufacturing overhead – beginning

7-55. (70 min.) Find Missing Data: IYF Corporation.

The calculations are shown below. We usually present these using both T-accounts

and the following formulas.

(a)

Beginning inventory + Transfers in = Ending inventory + Transfers Out

=

=

$8,400

(e) $3,000.

and,

7-56. (70 min.) Find Missing Data: NIC Enterprises.

The calculations are shown below. We usually present these using both T-accounts

and the following formulas.

(a)

Beginning inventory + Transfers in = Ending inventory + Transfers Out

Ending inventory

=

Beginning inventory + Transfers in – Transfers Out

=

$148,000 + $1,520,000 – $1,460,000

=

$208,000

(c)

Overhead rate

=

(d)

Overhead incurred

=

Overhead applied – Underapplied overhead

=

=

$490,000

Work in process beginning + Manufacturing costs

= Work in process ending + Transfers to Finished Goods Inventory.

7-57. (45 min.) Incomplete Data—Job Costing: Chelsea Household

Renovations.

The following information should be included (in summary) in a report to management.

Work-in-Process

Cost of Goods Sold

Cash or Accounts Payable

Job No. 61

Job No. 61

18,400

*

M*

8,000

8,000

M*

8,000

L

6/1

*

6/30

Wages Payable

Job No. 62

Job No. 62

128,000

*

M5

12,000

12,000

M

12,000

L

24,000

24,000

O

24,000

6/30

84,000

Overhead

Job No. 63

Underapplied Overhead

Actual

Applied

M*

6,400

16,00010

80,000

*

6/30

7-57. (continued)

M refers to direct materials

1Labor to complete job is $76,800 since the beginning inventory was 50% complete

2Applied overhead

=

$123,200 – $8,000 – $76,800

=

=

of direct labor dollars

3Overhead in beginning inventory

=

0.50 x $38,400

=

4Overhead applied in June

=

0.50 x $38,400

=

$19,200

5Materials for Job No. 62

=

Purchases – materials for Job No. 63

=

$18,400 – $6,400

=

$12,000

for Job No. 63

=

$128,000 – $38,400 – $41,600

=

=

0.50 x $48,000

=

8Overhead for Job No. 63

=

0.50 x $41,600

=

7-57. (continued)

7-58. (25 min.) Job Costing and Ethics: Old Port Shipyards.

(This problem is based on actual experience.)

a.

Olde Town

Newton

Overhead cost ……………..

$20,000,000

$80,000,000

Direct labor-hours …………

200,000

200,000

Predetermined rate……….

7-59. (25 min.) Job Costing and Ethics: Price and Waters.

7-60. (25 min.) Job Costing and Ethics: Global Partners.

a. Because the choice is between direct labor hours and direct labor cost, the

Solutions to Integrative Case

7-61. (75 min.) Cost Estimation, Estimating Overhead Rates, Job Costing, and

Decision-Making: O’Leary Corporation.

This problem relates overhead allocation to cost estimation and decision making. It

uses some of the methods of Chapters 4 and 5.

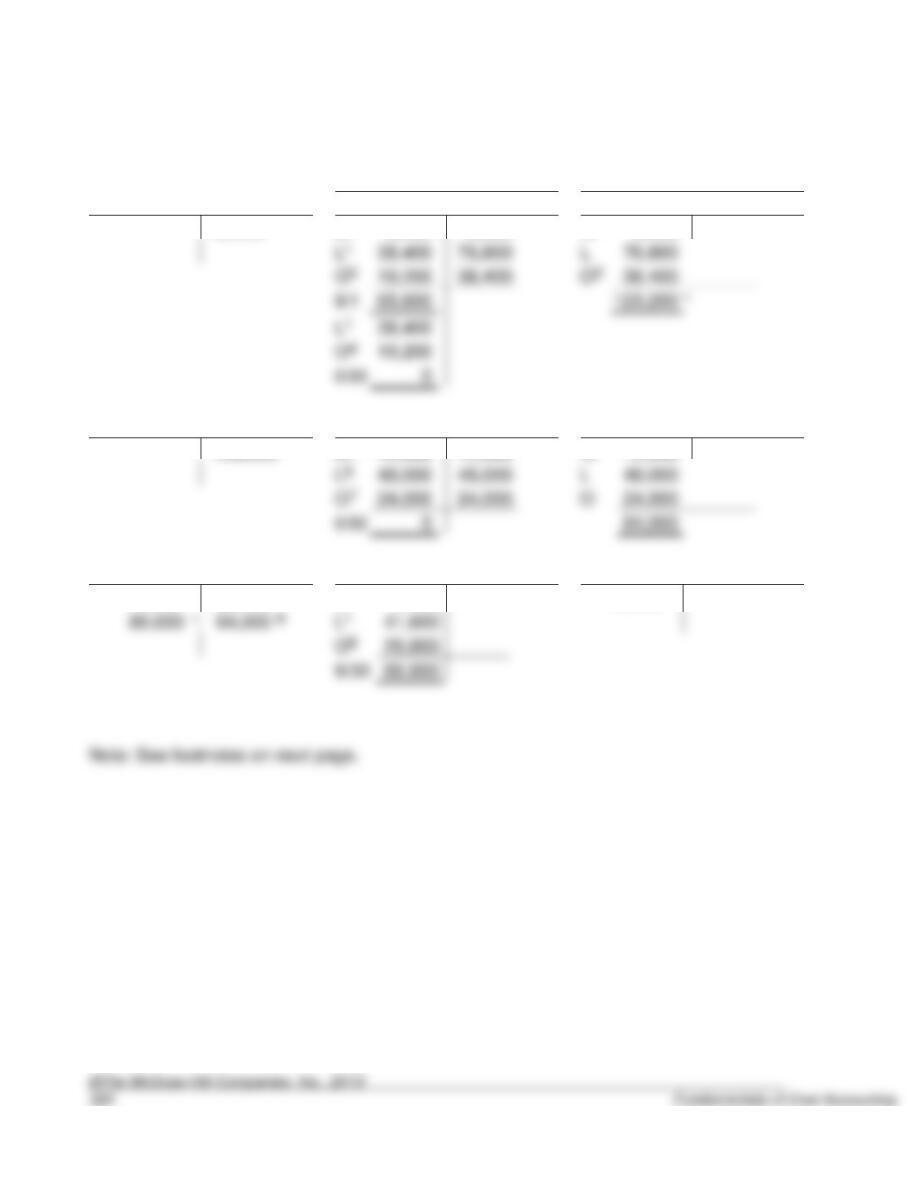

a. $965,400 (Work-in-Process Inventory) and $637,500 (Finished Goods Inventory).

Job MC-275 is the only job in process. It has accumulated the following costs:

Direct materials ……………..

$495,000

(Given)

Direct labor ……………………

(= $17 x 3,200 hours)

Manufacturing overhead ….

(= $130 x 3,200 hours)

Job MC-270 is the only job in finished goods. It has accumulated the following

costs:

Direct materials ……………..

$270,000

(Given)

Direct labor ……………………

(= $17 x 2,500 hours)

Manufacturing overhead ….

(= $130 x 2,500 hours)

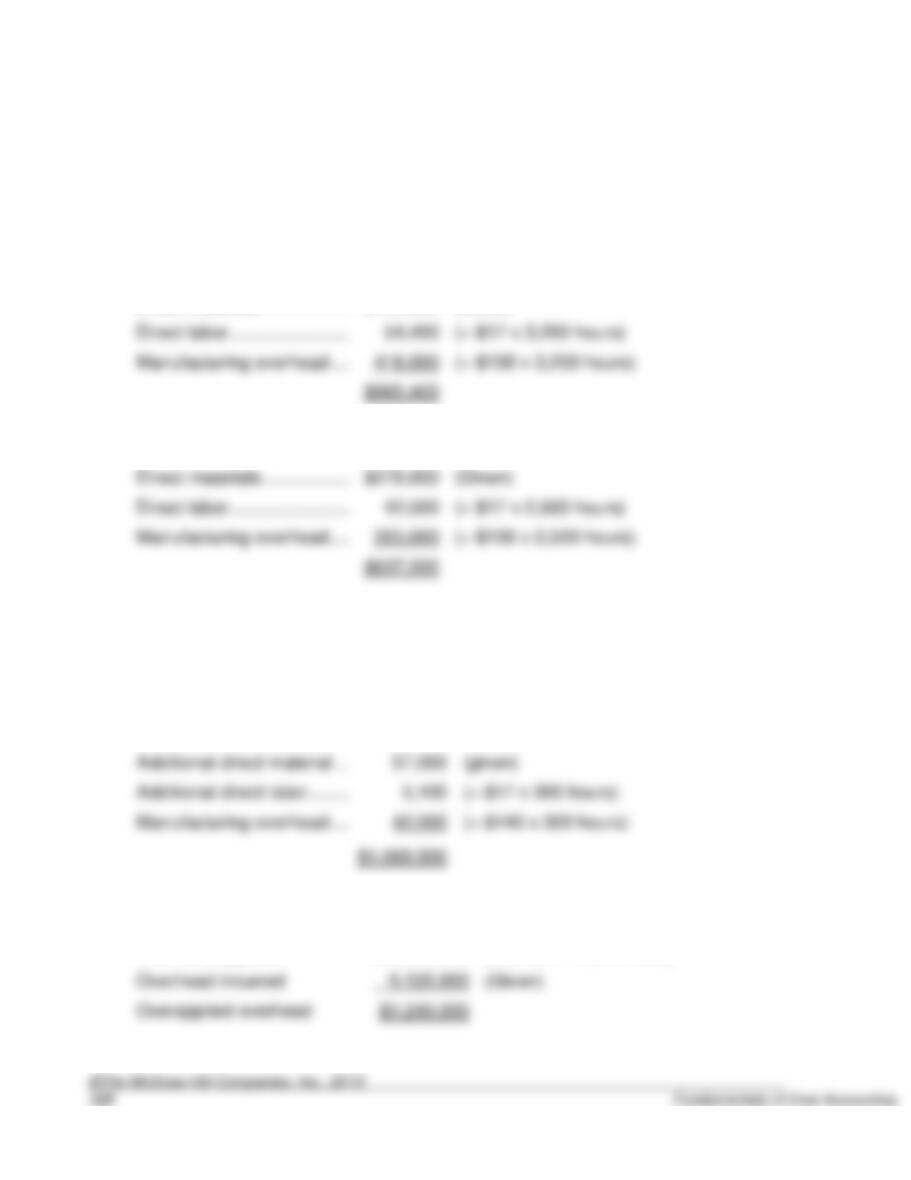

b. $1,069,500.

The predetermined overhead rate in year 3 is $140 per direct labor-hour. O’Leary

uses the actual rate from the previous year and $140 = $7,560,000 ÷ 54,000

hours).

Beginning costs …………….

$965,400

(From requirement (a))

Additional direct material …

(given)

Additional direct labor ……..

(= $17 x 300 hours)

c. $1,240,000 overapplied.

Overhead applied

$10,360,000

(= $140 x 74,000 hours)

Overhead incurred

(Given)

7-61. (continued)

d. A variety of allocations can be used. Because we know how many direct labor hours

are in each account from year 3, we will use this basis. Direct labor hours are the

basis for applying overhead. If this were unknown, we could use total account

balances. First, determine the number of direct labor-hours used in year 3 in each

account.

Direct labor hours, year 3

(Given)

In cost of goods, year 3

(74,000 – 11,840)

The allocation is then based on the relative amounts in each account:

Account

Percentage

Allocation

Work in process

10% (= 7,400 ÷ 74,000)

$124,000

(= .10 x $1,240,000)

Finished goods

6 (= 4,440 ÷ 74,000)

(= .06 x $1,240,000)

Cost of sales

84 (= 62,160 ÷ 74,000)

(= .84 x $1,240,000)

7-61. (continued)

e. $567,500.

This is a special order problem similar to those discussed in Chapter 4. The

minimum bid would be the variable cost of the job, ignoring strategic or other

considerations. The variable cost of the job (ignoring sales and administrative costs

as instructed in the problem) consists of direct material, direct labor, and variable

manufacturing overhead.

Applying the high-low method:

$9,120,000 – $7,560,000

=

$1,560,000

74,000 – 54,000

20,000

=

(5,772,000)