CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21–17 (FIN MAN); Ex. 7–17 (MAN)

a.

East Coast Railroad Company

Contribution Margin by Route

For the Month Ended April 30

Atlanta/

Baltimore

Baltimore/

Pittsburgh

Pittsburgh/

Atlanta

Total

Revenues

$ 255,000

$ 594,000

$ 542,080

$ 1,391,080

Variable costs:

Labor costs for loading

Fuel costs

Switchyard labor costs

and unloading railcars

$ (19,550)

$ (99,360)

$ (56,672)

$ (175,582)

Revenues: Revenue per railcar × Number of railcars

Labor costs for loading and unloading railcars: $46.00 × Number of railcars

Fuel costs: $12.40 × Number of train-miles

Train crew labor costs: $7.20 × Number of train-miles

Switchyard labor costs: $31.00 × Number of railcars

b. The Atlanta/Baltimore route performs significantly worse than do the other two

Note to Instructors: Part (b) is somewhat subtle but a worthy discussion. The cost

behavior issues discussed in (b) are common in service companies. For example,

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Ex. 21–18 (FIN MAN); Ex. 7–18 (MAN)

Underwater University

Variable Costing Income Statement

For the Fall Term

Revenue

$ 7,254,000

Variable costs:

Registration, records, and marketing costs

$(1,237,500)

Instructional costs

(3,868,800)

Contribution margin

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

PROBLEMS

Prob. 21–1A (FIN MAN); Prob. 7–1A (MAN)

1.

Kodiak Fridgeration Company

Absorption Costing Income Statement

For the Month Ended August 31

Sales

$10,800,000

Cost of goods sold:

Cost of goods manufactured

$9,600,000

Inventory, August 31 (8,000 units × $120.00*)

(960,000)

Gross profit

2.

Kodiak Fridgeration Company

Variable Costing Income Statement

For the Month Ended August 31

Sales

$10,800,000

Variable cost of goods sold:

Variable cost of goods manufactured*

$9,280,000

Inventory, August 31 (8,000 units × $116.00**)

(928,000)

Total variable cost of goods sold

(8,352,000)

Fixed selling and administrative expenses

3. The operating income reported under absorption costing exceeds the operating

income reported under variable costing by $32,000 ($900,000 – $868,000). This

$32,000 is due to including $32,000 of fixed manufacturing cost in inventory under

absorption costing [8,000 units × $4 ($320,000 ÷ 80,000)]. The $32,000 was thus

deferred to a future month under absorption costing, while it was included as an

expense of August (part of fixed costs) under variable costing.

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Prob. 21–2A (FIN MAN); Prob. 7–2A (MAN)

1.

Logan Industries Inc.

Estimated Income Statement—Absorption Costing—Solvent

For the Month Ending October 31

Sales (6,000 units)

$ 480,000

Cost of goods sold:

Direct materials

$210,000

Direct labor

144,000

Variable manufacturing cost

Fixed manufacturing cost

100,000

Operating loss

2.

Logan Industries Inc.

Estimated Income Statement—Variable Costing—Solvent

For the Month Ending October 31

Sales (6,000 units)

$ 480,000

Variable cost of goods sold:

Direct materials

$210,000

Direct labor

144,000

Variable manufacturing cost

48,000

Contribution margin

3. $140,000. The operating loss from temporarily closing the portion of the plant

associated with solvent would be $140,000 (fixed manufacturing cost of $100,000 plus

fixed selling and administrative expenses of $40,000).

4. Production of solvent should be continued. Temporary suspension of production

would result in an operating loss of $140,000 [from (3) above], compared with an

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

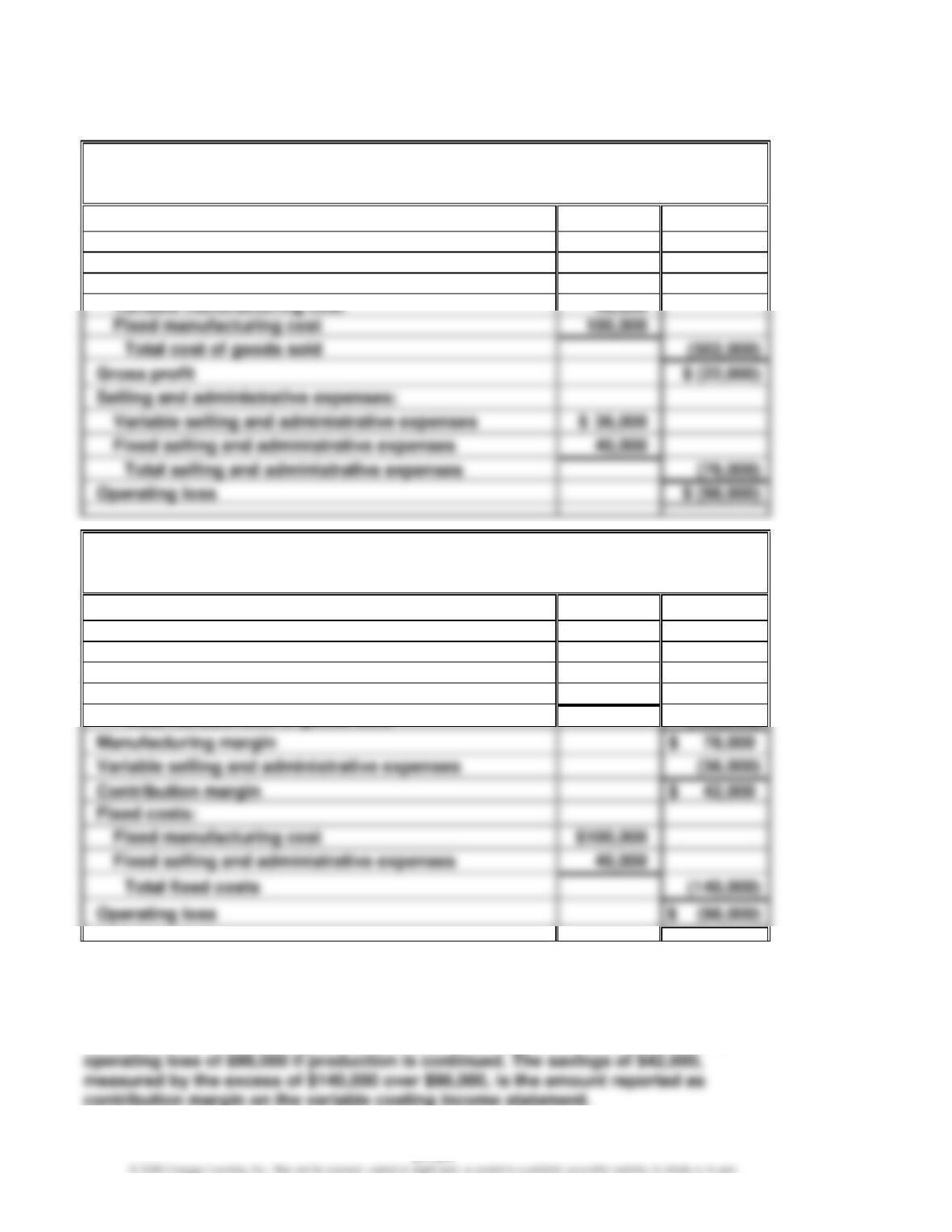

Prob. 21–3A (FIN MAN); Prob. 7–3A (MAN)

1.

a.

Big Sky Creations Company

Absorption Costing Income Statement

For the Month Ended May 31

Sales

$ 4,500,000

Cost of goods sold:

$ 1,260,000

Selling and administrative expenses

*

$3,600,000 ÷ 40,000 units = $90.00

b.

Big Sky Creations Company

Absorption Costing Income Statement

For the Month Ended June 30

Sales

$ 4,500,000

Cost of goods sold:

Gross profit

2.

a.

Big Sky Creations Company

Variable Costing Income Statement

For the Month Ended May 31

Sales

$ 4,500,000

Variable cost of goods sold:

Variable cost of goods manufactured

$3,480,000

Inventory, May 31 (4,000 units × $87*)

(348,000)

Contribution margin

$ 1,296,000

Fixed manufacturing costs

Fixed selling and administrative expenses

Operating income

*

$3,480,000 ÷ 40,000 units = $87.00

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

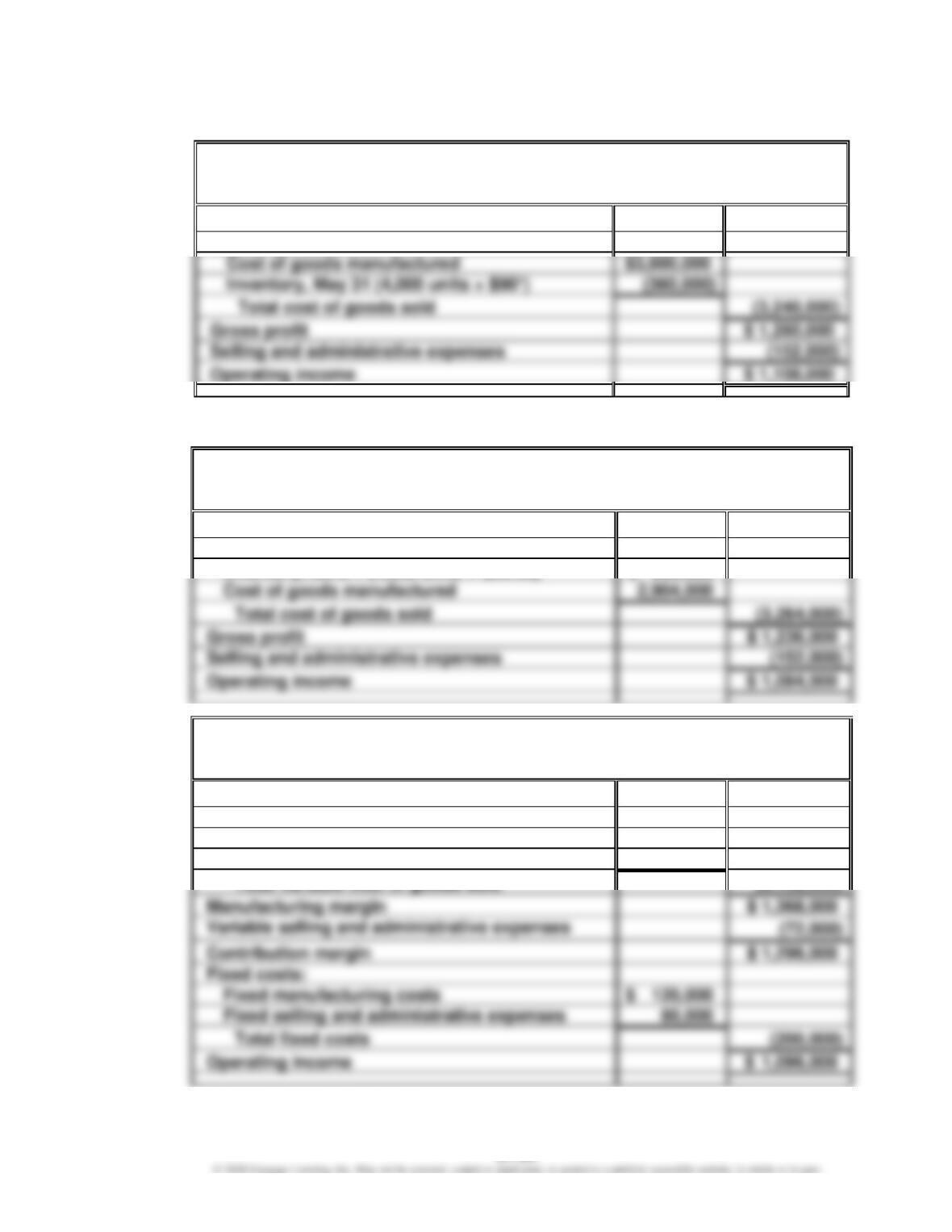

Prob. 21–3A (FIN MAN); Prob. 7–3A (MAN) (Concluded)

2.

b.

Big Sky Creations Company

Variable Costing Income Statement

For the Month Ended June 30

Sales

$ 4,500,000

Variable cost of goods sold:

Inventory, June 1 (4,000 units × $87.00)

$ 348,000

Variable cost of goods manufactured

2,784,000

Manufacturing margin

$ 1,368,000

Contribution margin

$ 1,296,000

Fixed manufacturing costs

Fixed selling and administrative expenses

3. a. For May, the operating income reported under absorption costing exceeds the

operating income reported under variable costing by $12,000 ($1,108,000 –

$1,096,000). This difference is due to including $12,000 of fixed manufacturing

cost in inventory under absorption costing [4,000 units × $3.00 ($120,000 ÷

40,000)]. The $12,000 was thus deferred to June under absorption costing, while

it was included as an expense of May (part of fixed costs) under variable

costing.

4. Big Sky Creations Company was equally profitable in May and June under the

variable costing concept. Sales and the variable cost per unit were the same for

both May and June. The difference in operating income reported under the

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

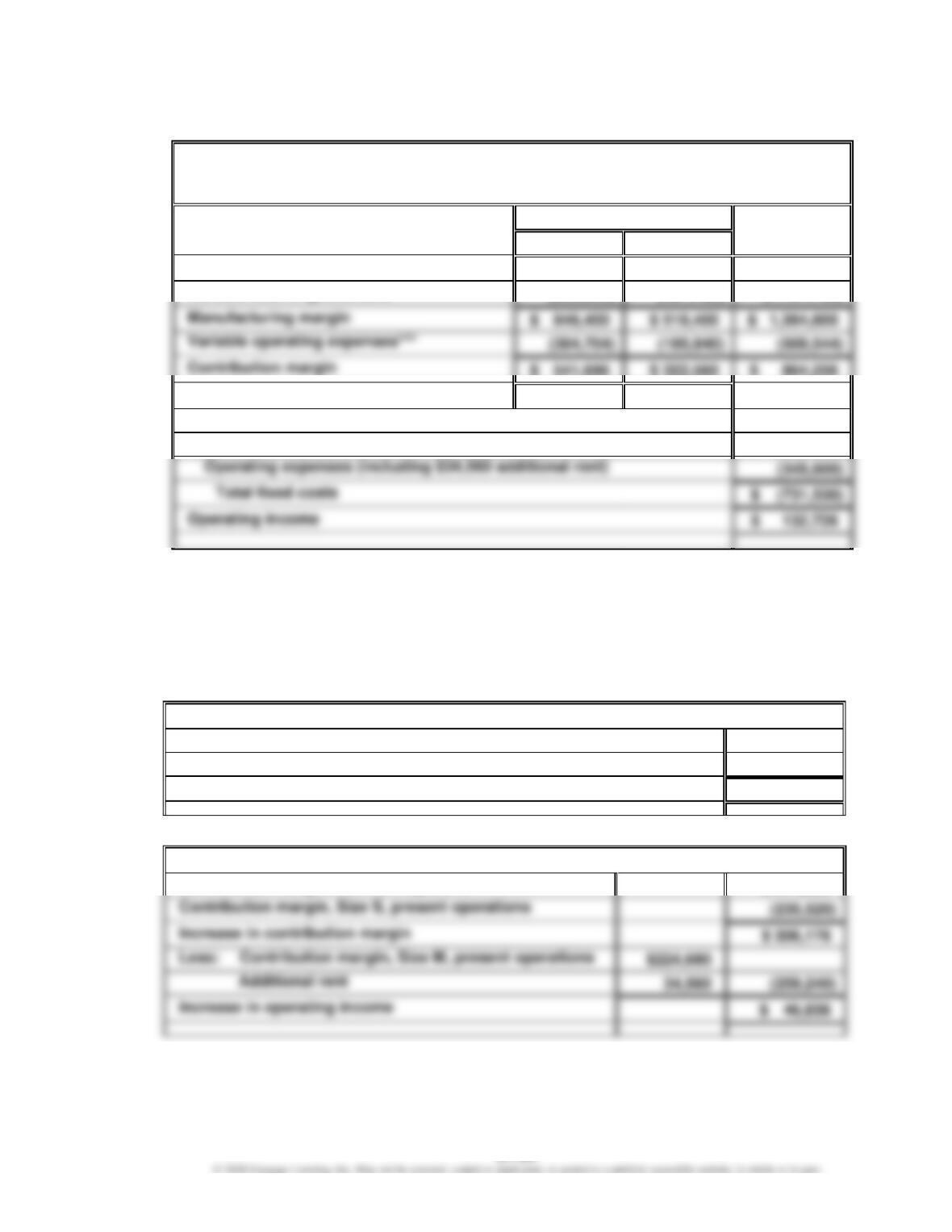

Prob. 21–4A (FIN MAN); Prob. 7–4A (MAN)

1.

Waltham Industries Inc.

Salespersons’ Analysis

For the Year Ended December 31

Variable

Variable Cost

Selling

of Goods Sold

Expenses

Contribution

Contribution

as a Percent

as a Percent

Margin

Salesperson

Margin

of Sales

of Sales

Ratio

Case

$231,800

44%

18%

38%

Dix

265,320

40%

16%

44%

181,660

48%

21%

31%

Orcas

308,000

36%

14%

50%

2. Orcas has the highest contribution margin and contribution margin ratio for the

year. This is because of two factors. First, Orcas has the smallest variable cost

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

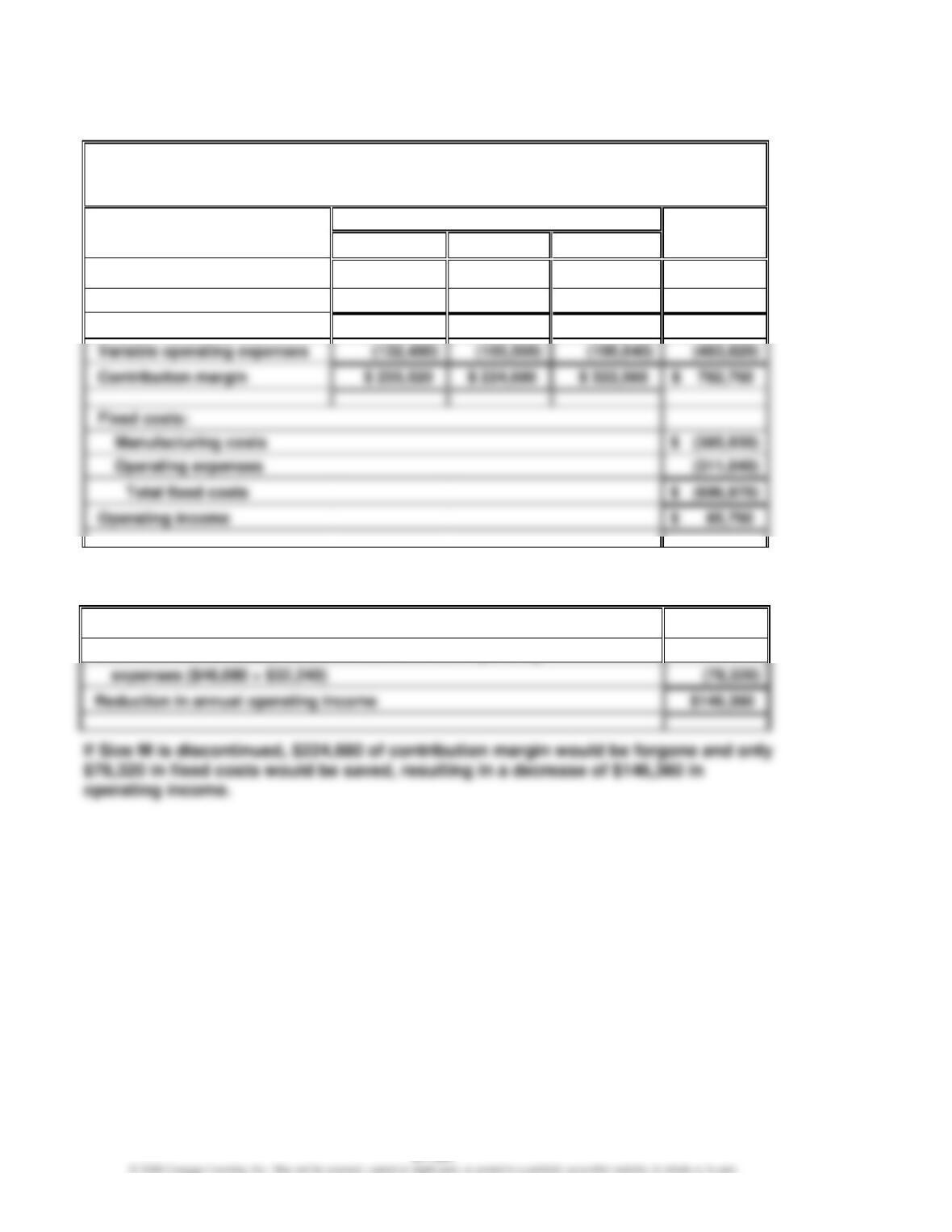

Prob. 21–5A (FIN MAN); Prob. 7–5A (MAN)

1.

Valdespin Company

Variable Costing Income Statement

For the Year Ended June 30, 20Y9

Size

Total

S

M

L

Sales

$ 668,000

$ 737,300

$ 956,160

$ 2,361,460

Variable cost of goods sold

(300,000)

(357,120)

(437,760)

(1,094,880)

Manufacturing margin

$ 368,000

$ 380,180

$ 518,400

$ 1,266,580

Variable operating expenses

(132,480)

(155,500)

(195,840)

Fixed costs:

2. Annual operating income would be reduced below its present level by $146,360

if Size M were to be discontinued (Proposal 2), as indicated below.

Contribution margin for Size M

$224,680

Less reduction in fixed production costs and fixed operating

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Prob. 21–5A (FIN MAN); Prob. 7–5A (MAN) (Concluded)

3.

Valdespin Company

Variable Costing Income Statement

For the Year Ended June 30, 20Y9

Size

Total

S

L

Sales*

$1,536,400

$ 956,160

$ 2,492,560

Manufacturing margin

$ 518,400

$ 1,364,800

Variable operating expenses***

Variable cost of goods sold**

$ 541,696

$ 322,560

$ 864,256

Fixed costs:

Manufacturing costs

$ (385,930)

*

$668,000 + ($668,000 × 130%)

**

$300,000 + ($300,000 × 130%)

***

$132,480 + ($132,480 × 130%)

4. $46,936. A comparison of the amount of operating income under present

conditions, as indicated in (1), and under Proposal 3, as indicated in (3), suggests

an increase of $46,936 if Proposal 3 is accepted, as illustrated below.

Operating income, Proposal 3

$ 132,726

Operating income, present conditions

(85,790)

Increase in operating income

$ 46,936

Alternatively, the $46,936 increase can be determined as follows:

Contribution margin, Size S, Proposal 3

Contribution margin, Size S, present operations

Increase in contribution margin

$ 306,176

$ 541,696

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

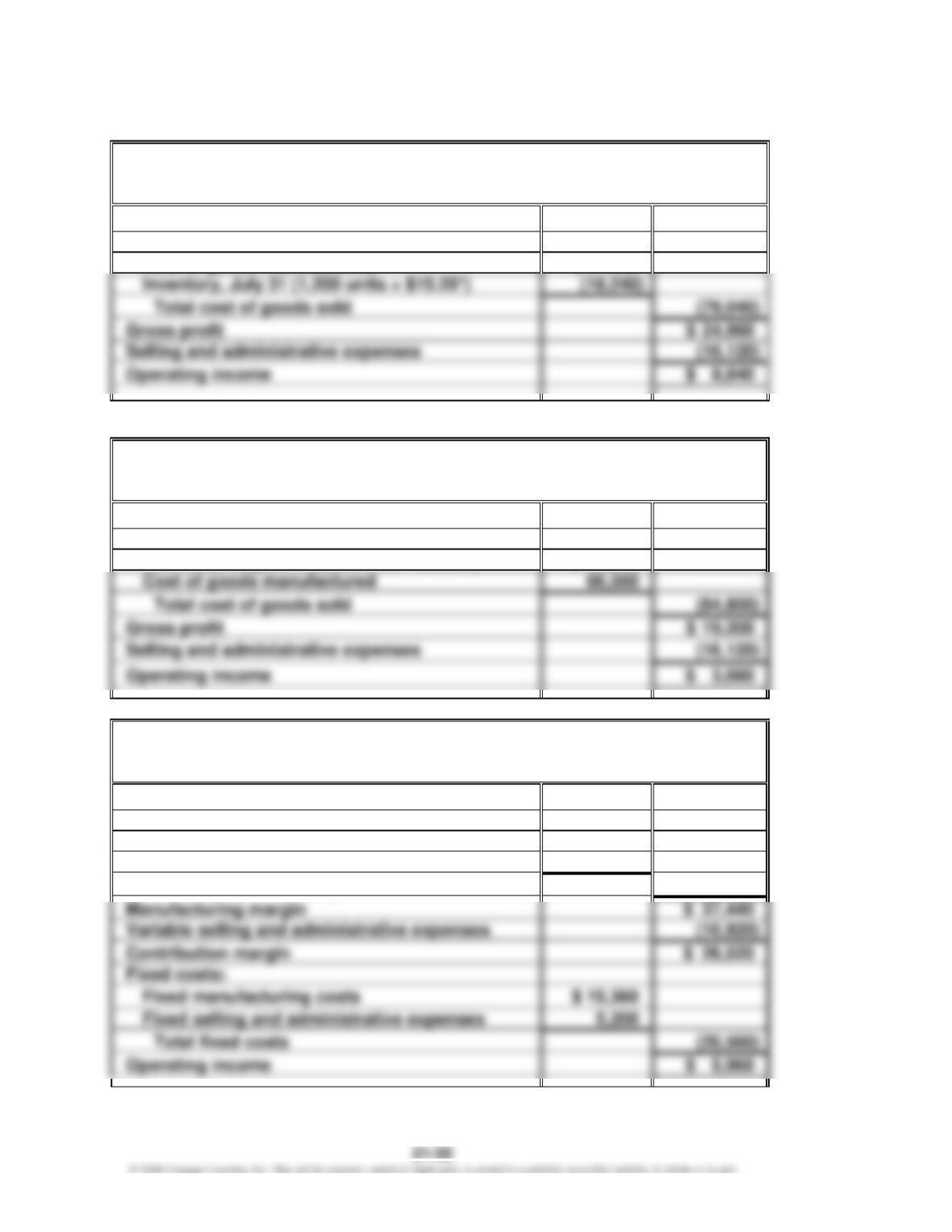

Prob. 21–1B (FIN MAN); Prob. 7–1B (MAN)

1.

YoSan Inc.

Absorption Costing Income Statement

For the Month Ended July 31

Sales

$ 2,150,000

Cost of goods sold:

Cost of goods manufactured

$1,824,000

Gross profit

Selling and administrative expenses

*

$1,824,000 ÷ 2,400 units = $760

2.

YoSan Inc.

Variable Costing Income Statement

For the Month Ended July 31

Sales

$ 2,150,000

Variable cost of goods sold:

Variable cost of goods manufactured

$1,536,000

Inventory, July 31 (400 units × $640*)

(256,000)

Manufacturing margin

Variable selling and administrative expenses

Contribution margin

Fixed costs:

Fixed manufacturing costs

Fixed selling and administrative expenses

*

$1,536,000 ÷ 2,400 units = $640

3. The operating income reported under absorption costing exceeds the operating

income reported under variable costing by $48,000 ($330,000 – $282,000). This

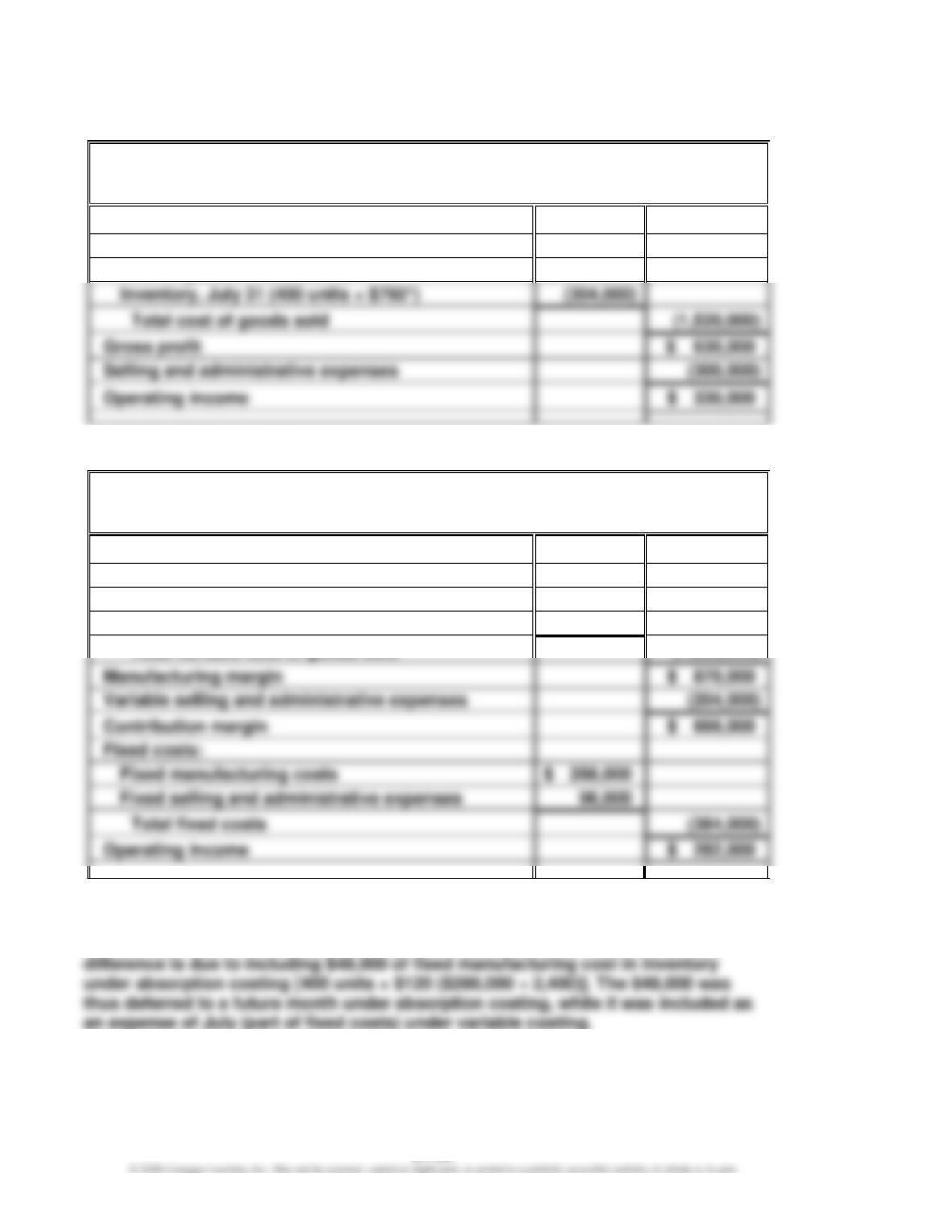

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

Prob. 21–2B (FIN MAN); Prob. 7–2B (MAN)

1.

Smooth Skin Care Products Inc.

Estimated Income Statement—Absorption Costing—Aloe Vera Hand Lotion

For the Month Ending November 30

Sales (320,000 units)

$ 25,600,000

Cost of goods sold:

Direct materials

$ 4,800,000

Direct labor

5,440,000

Variable manufacturing cost

11,200,000

Fixed manufacturing cost

(22,970,000)

Gross profit

Selling and administrative expenses:

Variable selling and administrative expenses

$ 3,200,000

Fixed selling and administrative expenses

Operating loss

2.

Smooth Skin Care Products Inc.

Estimated Income Statement—Variable Costing—Aloe Vera Hand Lotion

For the Month Ending November 30

Sales (320,000 units)

$ 25,600,000

Variable cost of goods sold:

Direct materials

$ 4,800,000

Direct labor

5,440,000

Variable manufacturing cost

11,200,000

Manufacturing margin

Variable selling and administrative expenses

Contribution margin

Fixed costs:

Fixed manufacturing cost

$ 1,530,000

Fixed selling and administrative expenses

Operating loss

3. $1,800,000. The operating loss from temporarily closing the portion of the plant

associated with A.V. lotion would be $1,800,000 (fixed manufacturing cost of

$1,530,000 plus fixed selling and administrative expenses of $270,000). This

assumes that the variable costs would be eliminated with the shutdown.

4. Production of A.V. lotion should be continued. Temporary suspension of

production would result in an operating loss of $1,800,000 [from (3) above],

CHAPTER 21 (FIN MAN); CHAPTER 7 (MAN) Variable Costing for Management Analysis

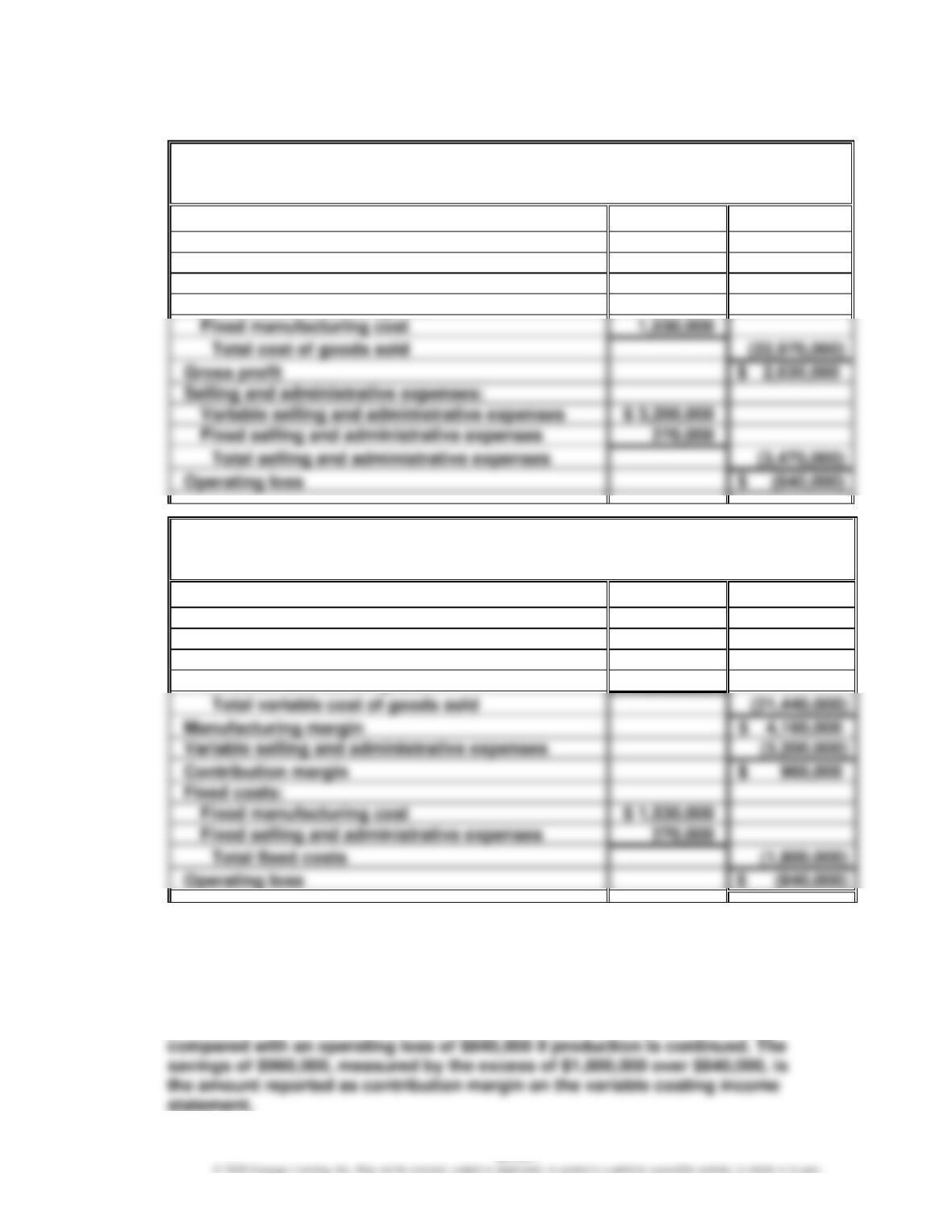

Prob. 21–3B (FIN MAN); Prob. 7–3B (MAN)

1.

a.

Head Gear Inc.

Absorption Costing Income Statement

For the Month Ended July 31

Sales

$104,000

Cost of goods sold:

Cost of goods manufactured

$ 97,280

Inventory, July 31 (1,200 units × $15.20*)

Total cost of goods sold

Selling and administrative expenses

*

$97,280 ÷ 6,400 units = $15.20

b.

Head Gear Inc.

Absorption Costing Income Statement

For the Month Ended August 31

Sales

$104,000

Cost of goods sold:

Inventory, August 1 (1,200 units × $15.20)

$ 18,240

Cost of goods manufactured

Total cost of goods sold

(84,800)

2.

a.

Head Gear Inc.

Variable Costing Income Statement

For the Month Ended July 31

Sales

$104,000

Variable cost of goods sold:

Variable cost of goods manufactured

$ 81,920

Inventory, July 31 (1,200 units × $12.80*)

(15,360)

Total variable cost of goods sold

(66,560)

Variable selling and administrative expenses

Fixed costs:

Fixed selling and administrative expenses

*

$81,920 ÷ 6,400 units = $12.80