Exercise 6-4 (continued)

Requirement 2 LIFO

(a)

Date

Transaction

Number

of units

Unit

cost

Ending

Inventory

Apr. 7

Purchase

(b)

Date

Transaction

Number

of units

Unit

cost

Cost of

Goods Sold

Apr. 7

Purchase

120

$54

$ 6,480

Jul. 16

Purchase

210

$25,410

a Last 440 units purchased are assumed sold

6-22 Financial Accounting, 5e

Exercise 6-4 (concluded)

Requirement 3 Weighted average

Date

Transaction

Number

of units

Unit

cost

Total

cost

Jan. 1

Beginning Inventory

60

$52

$ 3,120

Apr. 7

Purchase

140

Jul. 16

Purchase

210

Oct. 6

Purchase

120

Weighted-average cost = $29,610 / 530 units = $55.8679

(a) Ending inventory = 80 units × $55.8679 = $4,469

Requirement 4

FIFO

LIFO

Weighted-

average

Chapter 6 – Inventory and Cost of Goods Sold

Exercise 6-5 (LO 6-3)

Requirement 1 FIFO

(a)

Date

Transaction

Number

of units

Unit

cost

Ending

Inventory

Nov. 11

Purchase

(b)

Date

Transaction

Number

of units

Unit

cost

Cost of

Goods Sold

Jan. 1

Beginning inventory

Mar. 4

Purchase

Nov. 11

Purchase

a First 81 units purchased are assumed sold

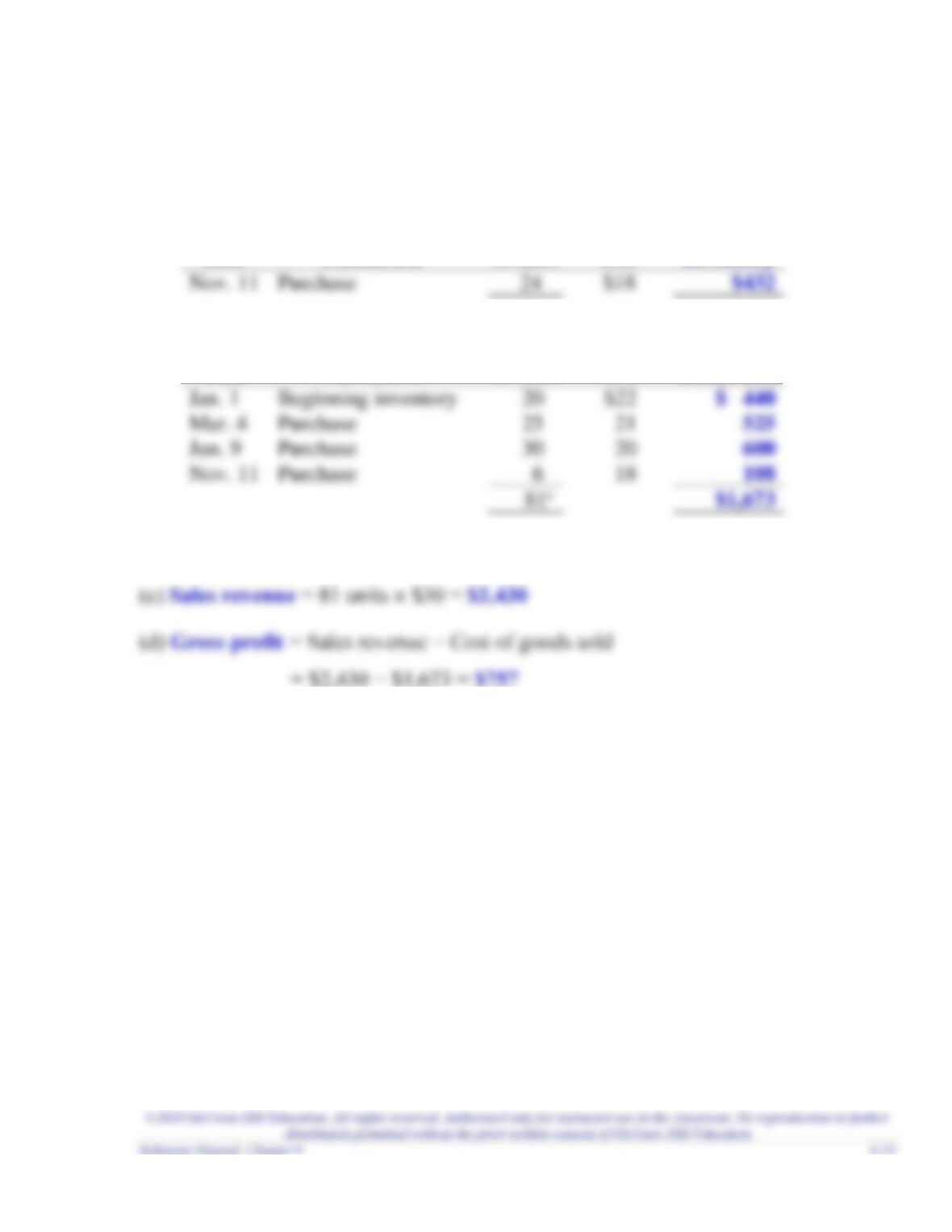

Exercise 6-5 (continued)

Requirement 2 LIFO

(a)

Date

Transaction

Number

of units

Unit

cost

Ending

Inventory

Mar. 4

Purchase

(b)

Date

Transaction

Number

of units

Unit

cost

Cost of

Goods Sold

Mar. 4

Purchase

21

$21

$ 441

Jun. 9

Purchase

* Last 81 units purchased are assumed sold

Exercise 6-5 (concluded)

Requirement 3 Weighted average

Date

Transaction

Number

of units

Unit

cost

Total

Cost

Jan. 1

Beginning Inventory

20

$22

$ 440

Mar. 4

Purchase

Jun. 9

Purchase

Nov. 11

Purchase

$2,105

Weighted-average cost = $2,105 / 105 units = $20.04762

Requirement 4

FIFO

LIFO

Weighted-

average

Chapter 6 – Inventory and Cost of Goods Sold

6-26 Financial Accounting, 5e

Exercise 6-6 (LO 6-5)

Debit

Credit

Inventory

310,000

Accounts Payable

310,000

(Purchase inventory on account)

Accounts Receivable

Sales Revenue

520,000

Cost of Goods Sold

Inventory

335,000

(Cost of inventory sold)

Chapter 6 – Inventory and Cost of Goods Sold

Exercise 6-7 (LO 6-5)

June 5

Debit

Credit

Inventory

4,000

Accounts Payable

4,000

(Purchase inventory on account)

June 9

Debit

Credit

Accounts Payable

Inventory

($800 = 40 units × $20 unit cost)

June 16

Debit

Credit

Accounts Receivable

5,600

Sales Revenue

5,600

(Sell inventory on account)

($5,600 = 160 units × $35 unit price)

Cost of Goods Sold

3,200

(Record cost of inventory sold)

($3,200 = 160 units × $20 unit cost)

Chapter 6 – Inventory and Cost of Goods Sold

Exercise 6-8 (LO 6-5)

Requirement 1

June 5

Debit

Credit

Inventory

3,800

Accounts Payable

3,800

Requirement 2

June 22

Debit

Credit

Accounts Payable

3,800

Chapter 6 – Inventory and Cost of Goods Sold

Exercise 6-9 (LO 6-5)

Requirement 1

May 2

Debit

Credit

Inventory

3,300

Accounts Payable

3,300

(Purchase inventory on account)

May 3

Inventory

Cash

May 5

Accounts Payable

Inventory

(Return inventory on account)

May 10

Accounts Payable

2,900

Inventory

29

Cash

2,871

(Pay on account with 1% discount)

($29 = $2,900 × 1%)

May 30

Sales Revenue

4,000

(Sell inventory on account)

Cost of Goods Sold

Inventory

(Record cost of inventory sold)

Requirement 2

May 24

Debit

Credit

Accounts Payable

2,900

Cash

2,900

Chapter 6 – Inventory and Cost of Goods Sold

6-30 Financial Accounting, 5e

Chapter 6 – Inventory and Cost of Goods Sold

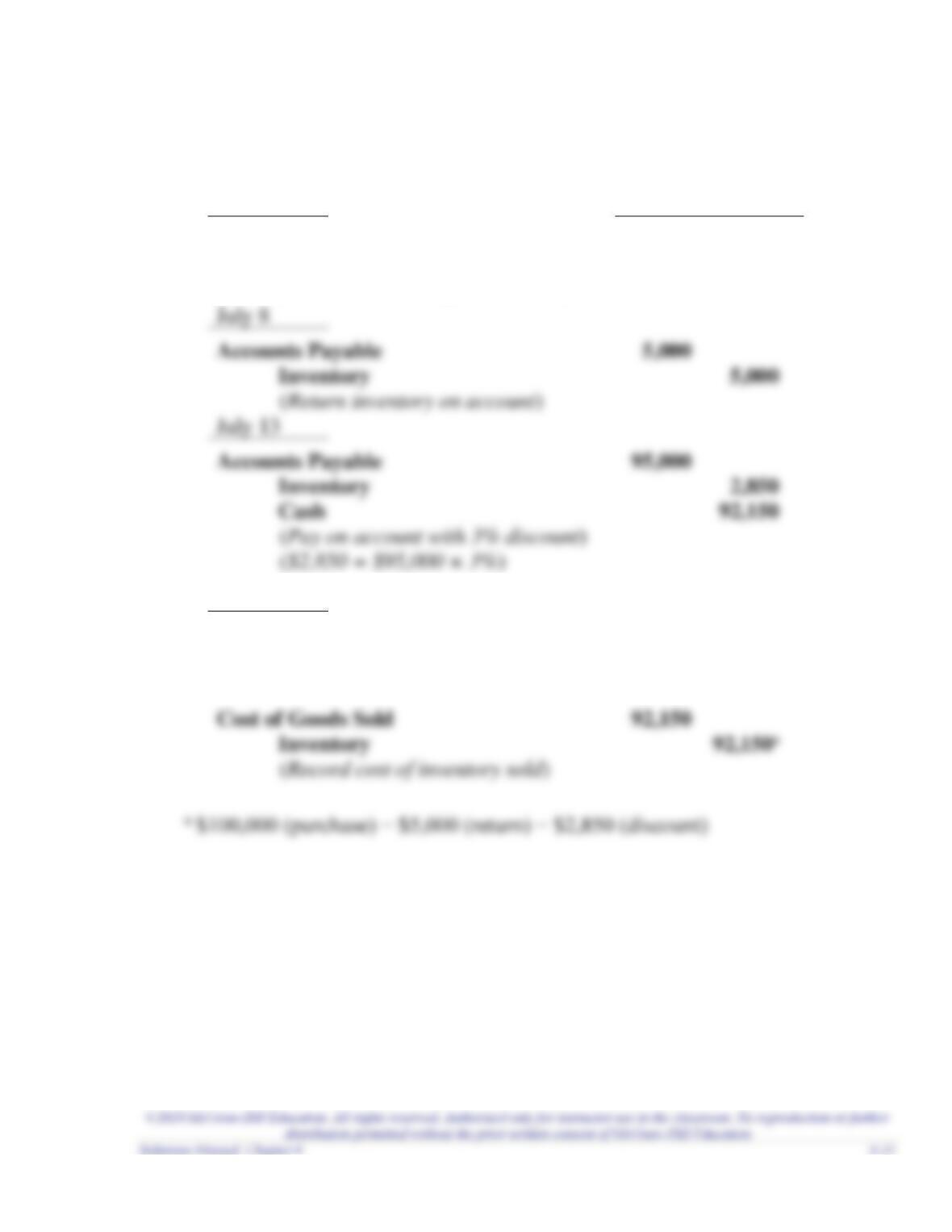

Exercise 6-10 (LO 6-5)

July 5

Debit

Credit

Inventory

100,000

Accounts Payable

100,000

(Purchase inventory on account)

July 8

Accounts Payable

Inventory

(Return inventory on account)

July 13

Accounts Payable

Inventory

Cash

July 28

Accounts Receivable

114,000

Sales Revenue

114,000

(Sell inventory on account)

Inventory

(Record cost of inventory sold)

Exercise 6-11 (LO 6-5)

August 6

Debit

Credit

Inventory

14,000

Accounts Payable

14,000

(Purchase inventory on account)

August 7

Inventory

Cash

(Pay freight-in cost)

August 10

Accounts Payable

Inventory

August 14

Accounts Payable

12,800

Inventory

128

Cash

12,672

(Pay cash on account with 1% discount)

($128 = $12,800 × 1%)

August 23

Sales Revenue

(Sell inventory on account)

Cost of Goods Sold

Inventory

(Record cost of inventory sold)

Chapter 6 – Inventory and Cost of Goods Sold

Exercise 6-12 (LO 6-5)

August 6

Accounts Receivable

14,000

Sales Revenue

14,000

Cost of Goods Sold

12,600

August 10

Sales Returns

Accounts Receivable

August 14

Cash

12,672

Sales Discounts

Accounts Receivable

12,800

Chapter 6 – Inventory and Cost of Goods Sold

6-34 Financial Accounting, 5e

Exercise 6-13 (LO 6-6)

Requirement 1

Inventory

Quantity

Unit

Cost

Total

Recorded

Cost

Furniture

Electronics

Requirement 2

Inventory

Quantity

Lower of Cost

and NRV

per unit

Ending

Inventory

Furniture

Electronics

Requirement 3

Debit

Credit

Cost of Goods Sold

5,000

Inventory

5,000

(Adjust inventory down to net realizable value)

(50 units of electronics × $100)

Requirement 4

Chapter 6 – Inventory and Cost of Goods Sold

Exercise 6-14 (LO 6-6)

Requirement 1

Inventory

Quantity

Unit

Cost

Total

Recorded

Cost

Shirts

35

$ 60

$ 2,100

MegaDriver

Requirement 2

Inventory

Quantity

Lower of Cost

and NRV

per unit

Ending

Inventory

Shirts

35

$ 60

$ 2,100

MegaDriver

Requirement 3

Debit

Credit

Cost of Goods Sold

1,650

Requirement 4

The write-down of inventory has the effect of reducing total assets (inventory),

Exercise 6-15 (LO 6-2, 6-7)

Requirement 1

Lewis

Clark

Beginning inventory

$ 24,000

$ 50,000

Cost of goods sold

$252,000

$165,000

Requirement 2

Lewis

Clark

Cost of goods sold

Inventory

Requirement 3

Lewis

Clark

Average

365

365

365

Requirement 4

Lewis seems to be managing its inventory more efficiently. For Lewis, inventory turns

Chapter 6 – Inventory and Cost of Goods Sold

Exercise 6-16 (LO 6-2, 6-7)

Requirement 1

Gross

Profita

Operating

Incomeb

Income Before

Income Taxesc

Net

Incomed

a Gross profit = Sales revenue − Cost of goods sold

Requirement 2

Henry

Grace

James

Gross

Gross profit

$27,200

$10,500

$15,200

Purchases

3,300

6-38 Financial Accounting, 5e

Exercise 6-17 (LO 6-8)

Requirement 1

May 2

Debit

Credit

Purchases

3,300

Accounts Payable

3,300

(Purchase inventory on account)

May 3

200

Cash

(Pay freight-in cost)

May 5

Purchase Returns

(Return inventory on account)

May 10

Accounts Payable

2,900

Purchase Discounts

29

Cash

2,871

May 30

Accounts Receivable

4,000

4,000

(Sell inventory on account)

Requirement 2

May 31

Debit

Credit

Cost of Goods Sold

3,071

Purchase Returns

400

Chapter 6 – Inventory and Cost of Goods Sold

Exercise 6-18 (LO 6-8)

Requirement 1

July 5

Debit

Credit

Purchases

100,000

Accounts Payable

100,000

(Purchase inventory on account)

July 8

Accounts Payable

Purchase Returns

(Return inventory on account)

July 13

Accounts Payable

Purchase Discounts

Cash

July 28

Accounts Receivable

Sales Revenue

114,000

(Sell inventory on account)

Requirement 2

July 31

Debit

Credit

Cost of Goods Sold

92,150

Purchase Returns

5,000

Purchase Discounts

Purchases

100,000

Exercise 6-19 (LO 6-9)

August 6

Debit

Credit

Purchases

14,000

Accounts Payable

14,000

(Purchase inventory on account)

August 7

Cash

August 10

Accounts Payable

Purchase Returns

(Return inventory on account)

August 14

Accounts Payable

12,800

Purchase Discounts

128

Cash

12,672

(Pay cash on account with 1% discount)

($128 = $12,800 × 1%)

August 23

Accounts Receivable

11,000

Sales Revenue

11,000

(Sell inventory on account)

Requirement 2

August 31

Debit

Credit

Inventory (ending)

2,859.50

Purchase Returns

Purchase Discounts

Purchases

14,000