Chapter 06 – Inventory and Cost of Goods Sold

6-12

P6-9B

LO6-8

FIFO

Record transactions and prepare a partial income

20

Additional

Perspectives

Topic

Time

(Min.)

AP6-1

Continuing Problem: Great Adventures

40

AP6-2

Financial Analysis: American Eagle Outfitters, Inc.

25

AP6-3

Financial Analysis: The Buckle, Inc.

25

Buckle, Inc.

AP6-5

Ethics

20

AP6-6

Internet Research

30

AP6-7

Written Communication

25

AP6-8

Earnings Management

30

Chapter 06 – Inventory and Cost of Goods Sold

6-13

Alternate Let’s Review

Problem #1

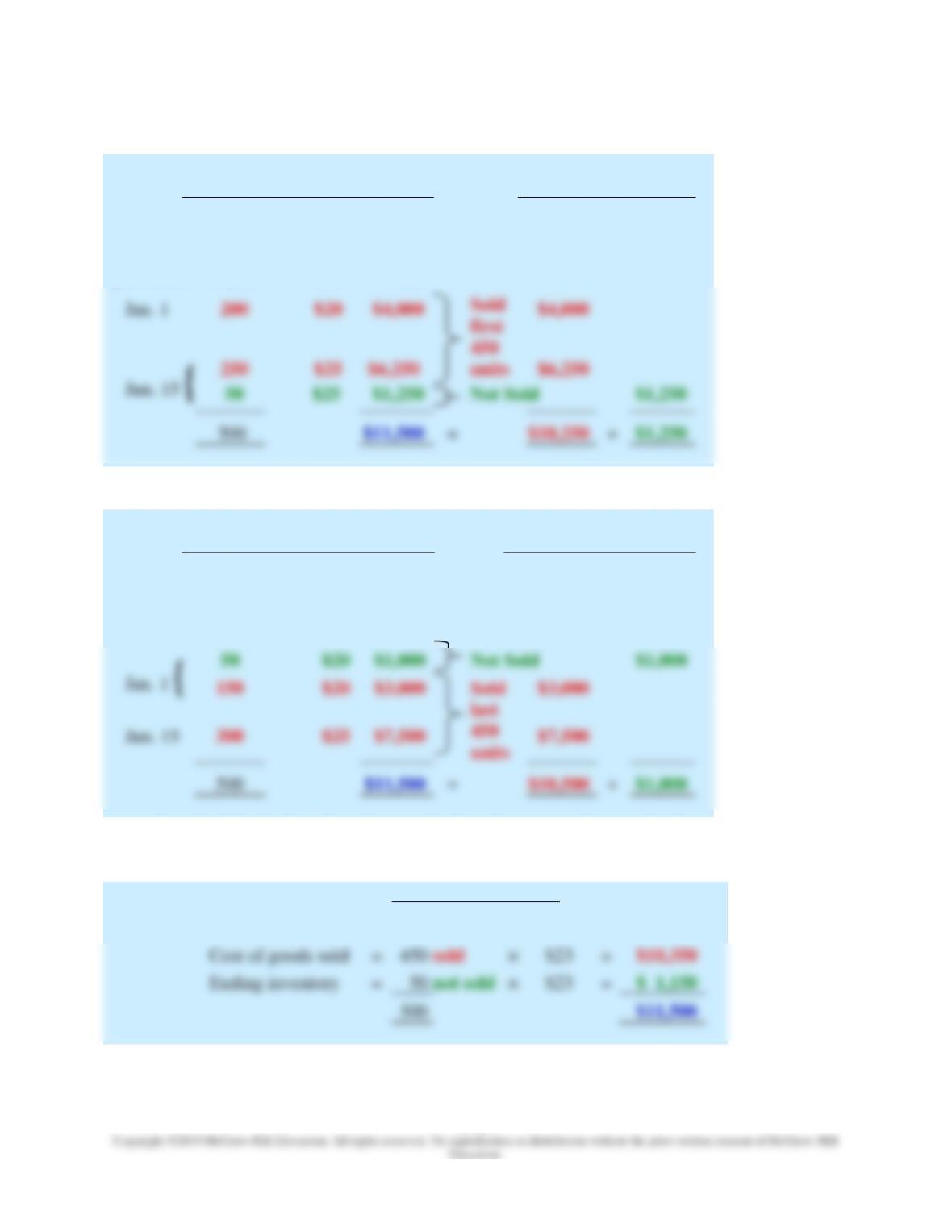

For the current year, a company has the following beginning inventory and purchase.

Date

Transaction

Number

of units

Unit

cost

Total

cost

Jan. 1

Beginning inventory

200

$20

$ 4,000

Jun. 15

Purchase

300

500

$11,500

Required:

1. Calculate cost of goods sold and ending inventory using the FIFO method.

Chapter 06 – Inventory and Cost of Goods Sold

6-14

Solution:

1.

Cost of goods available for sale

=

Cost of

goods sold

+

Ending

inventory

Beginning

inventory

and

purchases

Number

of units

×

Unit

cost

=

Total

Cost

2.

Cost of goods available for sale

=

Cost of

goods sold

+

Ending

inventory

Beginning

inventory

and

purchases

Number

of units

×

Unit

cost

=

Total

Cost

3.

Weighted-average unit cost

=

$11,500

=

$23

500

Cost of goods sold

=

×

=

Ending inventory

=

×

=

500

Chapter 06 – Inventory and Cost of Goods Sold

Problem #2

A company accounts for its inventory using FIFO with a perpetual system. At the beginning of

March, the company has inventory of $40,000.

Required:

Record the following transactions for the company for the month of March:

1. On March 7, the company purchases additional inventory for $65,000 on account, terms 3/10,

n/30.

2. On March 10, inventory that cost $5,000 arrived damaged and was returned for a full refund.

3. On March 16, the company makes full payment for inventory purchased on March 7,

excluding inventory returned and the discount received.

4. During the month of March, revenue from inventory sales totals $85,000. All sales are for

cash. The cost of inventory sold is $35,000.

Solution:

1.

Inventory 65,000

Accounts Payable 65,000

Chapter 06 – Inventory and Cost of Goods Sold

6-16

Problem #3

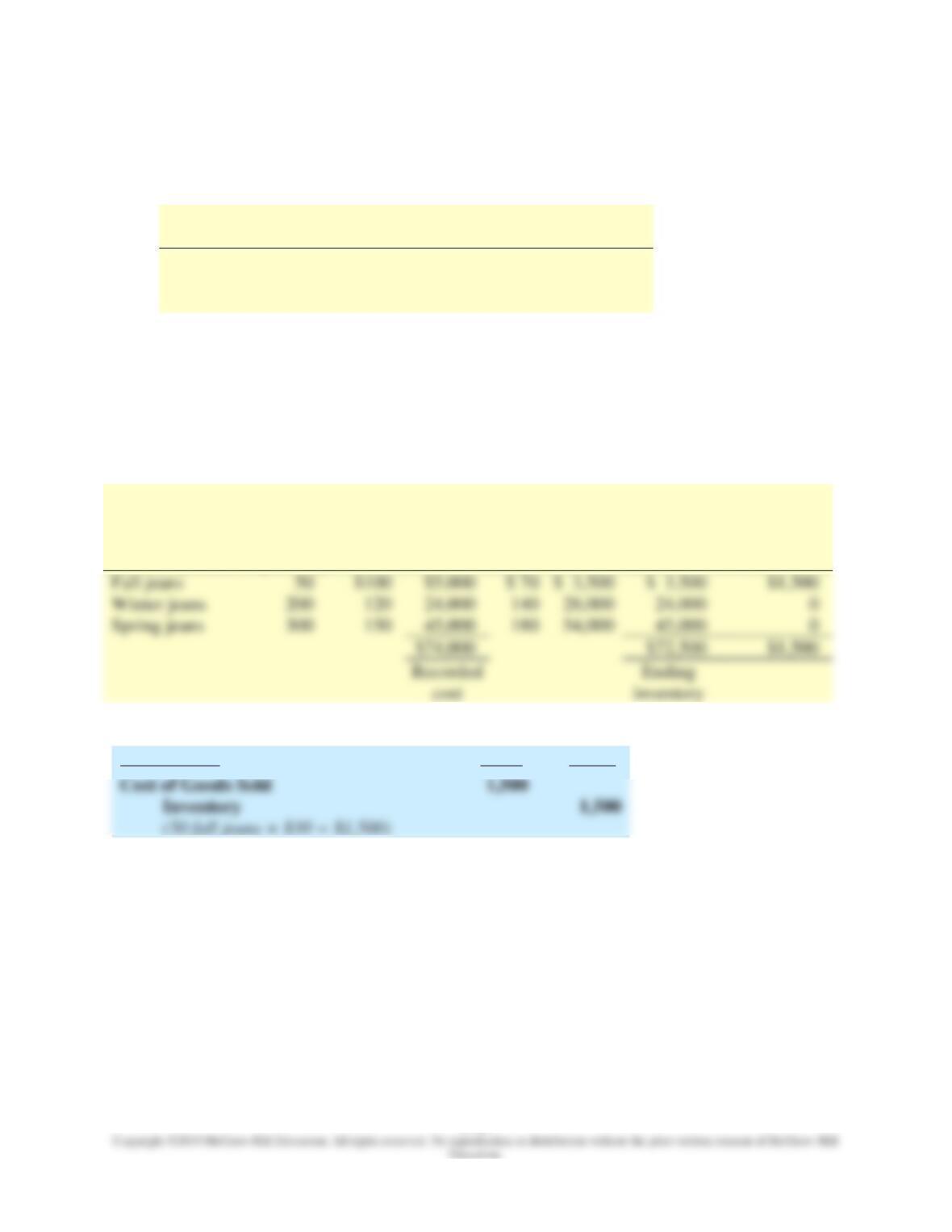

J-Lo Fashions provides year-round specialty jeans. At December 31, the company’s records

show the following amounts in ending inventory for each item.

Inventory items

Quantity

Cost

Per unit

Market

per unit

Fall jeans

50

$100

$ 70

Winter jeans

200

120

140

Spring jeans

300

150

180

Required:

1. Determine ending inventory using the lower of cost and net realizable value.

2. Record any necessary year-end adjustment associated with the lower of cost and net realizable

value.

Solution:

1.

Cost

NRV

Inventory items

Quantity

Per

unit

Total

Per

unit

Total

Lower

of cost

and NRV

Year-end

adjustment

needed

Fall jeans

Winter jeans

28,000

24,000

Spring jeans

54,000

45,000

$74,000

inventory

2.

December 31

Debit

Credit

Cost of Goods Sold

Chapter 06 – Inventory and Cost of Goods Sold

6-17

Common Mistakes

Common Mistakes made by students are highlighted in each of the chapters. With greater

awareness of the potential pitfalls, student can avoid making the same mistakes and gain a deeper

understanding of the chapter material.

Common Mistake

When calculating cost of goods sold using FIFO, students sometimes forget to count beginning

inventory as the first purchase. These units were purchased last period, which was before any

purchases this period, so they are assumed to be the first units sold.

Common Mistake

Many students find it surprising that companies are allowed to report inventory costs using

assumed amounts rather than actual amounts. Nearly all companies sell their actual inventory in

a FIFO manner, but they are allowed to report it as if they sold it in a LIFO manner. Later, we’ll

Common Mistake

In calculating the weighted-average unit cost, be sure to use a weighted average of the unit cost

instead of the simple average. In the example above, there are three unit costs: $7, $9, and $11. A

Common Mistake

FIFO and LIFO describe more directly the calculation of cost of goods sold, rather than ending

inventory. For example, FIFO (first-in, first-out) directly suggests which inventory units are

assumed sold (the first ones in) and therefore used to calculate cost of goods sold. It is implicit

under FIFO that the inventory units not sold are the last ones in and are used to calculate ending

inventory.

Common Mistake

Many students use ending inventory rather than average inventory in calculating the inventory

Chapter 06 – Inventory and Cost of Goods Sold

6-18

Decision Points and Decision Maker’s Perspective

Decision Points and Decision Maker’s Perspectives are provided throughout each chapter to give

insight into how measurement and communication of financial accounting information help

decision makers.

Decision Points

Question

Accounting Information

Analysis

When comparing

The LIFO difference

When inventory costs are rising, FIFO

Question

Accounting Information

Analysis

Is the company

effectively managing

its inventory?

Inventory turnover ratio

and average days in inventory

A high inventory turnover ratio (or

low average days in inventory)

generally indicates that the company’s

inventory policies are effective.

Question

Accounting Information

Analysis

For how much is a

Gross profit and net sales

The ratio of gross profit to net sales

Decision Maker’s Perspective

Investors Understand One-Time Gains

Investors typically take a close look at the components of a company’s profits. For example,

Ford Motor Company announced that it had earned a net income for the fourth quarter (the

Chapter 06 – Inventory and Cost of Goods Sold

6-19

FIFO or LIFO?

Management must weigh the benefits of FIFO and LIFO when deciding which inventory cost

flow assumption will produce a better outcome for the company. Here we review the logic

behind that decision.

Why Choose FIFO?

Most companies’ actual physical flow follows FIFO. Think about a supermarket, sporting

goods store, clothing shop, electronics store, or just about any company you’re familiar with.

Why Choose LIFO?

If FIFO results in higher total assets and higher net income and produces amounts that most

closely follow the actual flow of inventory, why would any company choose LIFO? The

Conservatism and the Lower of Cost and Net Realizable Value Method

Firms are required to report the falling value of inventory, but they are not allowed to report any

increasing value of inventory. Why is this? The answer lies in the conservative nature of some

Chapter 06 – Inventory and Cost of Goods Sold

6-20

Ethical Dilemma

Diamond Computers, which is owned and operated by Dale Diamond, manufactures and sells

different types of computers. The company has reported profits every year since its inception in

2002 and has applied for a bank loan near the end of 2021 to upgrade manufacturing facilities.

These upgrades should significantly boost future productivity and profitability.

In preparing the financial statements for the year, the chief accountant, Sandy Walters,

mentions to Dale that approximately $80,000 of computer inventory has become obsolete and a

write-down of inventory should be recorded in 2021.

Key Issues

• Writing off inventory reduces net income and total assets in the year of the write-off. By

delaying the write-off, the company shifts profits from the following year to the current

year, overstating current performance.

• Proper reporting vs. the long-term care of the company and its employees

Option 1: Wait to book the write-off

• Booking the write-off could be very damaging to the long-term health of the company

Chapter 06 – Inventory and Cost of Goods Sold

6-21

Option 2: Book the write-off now

• The company is in the situation they are in concerning the obsolete inventory because of

business decisions and circumstances over the past few years. Bad decision-making

should not be corrected via creative accounting.

• Despite the possible increased productivity that would be generated from the loan that

saving the job of many others.