CHAPTER 6

Full and Fair Reporting

THINKING BEYOND THE QUESTION

How do we ensure that reports to external users fairly present business activities?

Full and fair reporting should help external users understand the deci-

sions made by managers. It is not intended to protect those users from

QUESTIONS

Q6-1 A variety of individuals rely on financial statements to make decisions.

For example, stockholders and creditors make stock purchasing and

Q6-2 Investors need assurance that the shares they are evaluating are reason-

Q6-3 Sarbanes-Oxley is intended to restore investor confidence in the financial

markets by making management more accountable for the accounting re-

170 Chapter 6

Q6-4 The audit committee is responsible for selecting, compensating, and

overseeing the corporation’s auditor. The auditor reports directly to the

Q6-5 Accounting standards are issued through a political process. Groups that

use and prepare financial information must agree that a proposed stand-

Q6-6 The SEC has delegated standard-setting to private organizations such as

Q6-7 Elements include assets, liabilities, equity, investments by owners, distri-

Q6-8 The primary objective of financial reporting is to provide information use-

ful to current and potential investors, creditors, and other users in mak-

Q6-9 The term “unqualified opinion” in no way implies anything about the qual-

ifications of the auditors. In fact, an unqualified opinion is good news, not

Q6–10 There are two primary reasons for notes to financial statements. First, to

keep the financial statements to a reasonable size—say, one page each—

a great deal of combining and aggregation of accounts must occur. One

Full and Fair Reporting 171

Q6–11 An audit is a detailed and systematic investigation of a company’s ac-

counting records. Auditors select a representative sample of transactions

to form an opinion as to whether the company’s controls and systems are

Q6-12 Managers and other decision makers need information upon which to

base decisions. Part of that information is provided by the accounting

system. At the same time, a company’s activities are generally too com-

Q6-13 The two primary purposes of internal controls are (1) to safeguard the or-

Q6-14 Internal controls are used in a computerized accounting system to pro-

tect its data from unauthorized access, improper use, and destruction.

Unauthorized access is prevented by using a system of identification and

Q6-15 A strong system of internal controls begins with a management philoso-

phy that encourages appropriate security and behavior in a company. If

Q6-16 Human resource controls include good hiring practices that involve hir-

ing qualified employees. Background checks help ensure employee in-

Q6-17 Safeguarding assets often involves controlling physical access. Mer-

chandise and materials can be secured in warehouses and display cases.

EXERCISES

E6-2 Development of the New York Stock Exchange (NYSE)—Founded in 1792,

the NYSE facilitated the growing trade in corporate stocks. In later years,

the NYSE required listed companies to provide accounting information to

E6-3 a. Securities Act of 1933—The act required most corporations to file

registration statements before selling stock to investors. Reports

must include a balance sheet and income statement.

Full and Fair Reporting 173

E6-4 a. FASB

E6-5 This is a true statement. Complying with regulations is costly because fi-

nancial information must be collected, summarized, and reported. In addi-

E6-6 Generally accepted accounting principles are financial reporting rules es-

tablished by a political process. The standard-setting process involves a

E6-7 Qualitative characteristics are attributes that make accounting infor-

mation useful. The primary qualitative characteristics are understandabil-

ity and usefulness. Relevance and reliability are considered to be the two

E6-8 The conceptual framework was developed in the 1970s and 1980s. The

E6-9 The first paragraph of an auditors’ report identifies the statements and

174 Chapter 6

E6–10 Management’s discussion and analysis (MD&A) is intended to explain

important events and changes in performance among the years present-

E6–11 a. It’s a little difficult to believe that such a giant company has only nine

b. A judgment has been made by management that a greater level of

c. It is very unlikely that this high level of aggregation would be helpful

to the manager of any General Mills division. First, a manager would

E6–12 Quick is a going concern because it has an indefinite life. This life is suf-

ficiently long that it can engage in long-term transactions, such as issu-

ing long-term debt and purchasing long-term assets. It expects to contin-

Full and Fair Reporting 175

E6–13 Bill, I think you misunderstand some of the basic issues regarding audits

and auditors’ reports. First, an auditor does not prepare the company’s fi-

nancial statements. The audit expresses only an opinion regarding them.

The company’s accounting staff prepares the financial statements and

then asks an independent, outside auditor to express an opinion on them.

E6–14 Accountants work in business organizations to prepare the financial in-

formation contained in companies’ annual reports. They manage the in-

E6–15 Pencils Pens Markers

Division revenues $200,000 $300,000 $100,000

Division expenses 140,000 160,000 60,000

Division profit $ 60,000 $140,000 $ 40,000

E6–16 Internal auditors work for businesses and are responsible for developing

and monitoring internal control systems and for auditing a company’s di-

E6–17 Computer system controls are designed to protect a company’s infor-

mation resources from unauthorized access, improper use, and destruc-

tion. Controls include the following:

• Appropriate identification and passwords—to prevent unauthorized

persons from gaining access to the system

Human resources controls include the following:

• Hiring qualified employees and conducting background checks

Physical controls include the following:

• Securely storing merchandise and materials in warehouses and display

cases

E6–18 Independent CPAs audit business financial reports to ensure that they

fairly present a company’s business activities. The audit is an important

tool in maintaining strong capital markets. If managers fail in their re-

Full and Fair Reporting 177

E6–19 a. The purpose of internal control is to protect the organization’s re-

of the company’s assets or the misstatement of its accounts.

b. Example: If the same person both handles the cash and accounts for

cash, that individual could cover up the theft of cash by charging it

E6–20 Internal control problems include the following: Ima has control of both

assets (cash) and accounting for the assets (sales slips) and there is no

mechanism to prevent her from falsifying information or from stealing

Solving the problems requires that Ima have less discretion over the

sales slips. If possible, the cash register should automatically record the

amount of a sale and produce a prenumbered sales slip. Ima should be

178 Chapter 6

PROBLEMS

P6-1 A. Managers use financial information to evaluate performance of a di-

vision, product line, or geographical area.

B. Stockholders rely on financial information to help them make deci-

P6-2 Accounting regulation is vital to the capital markets because investors

must have confidence in published financial information. If investors are

P6-3 The common theme is that all services are directly related to producing a

company’s financial statements.

Management is responsible for producing the financial statements and an

independent public accounting firm is responsible for expressing an

P6-4 The CEO and CFO are certifying that the financial condition and results of

operations are presented fairly. They use the term “in all material re-

spects.” This means the financial statements are free from mistakes and

P6-5 SOX demands more accountability of corporate executives. Those who

falsely certify the financial statements are subject to a fine of up to $5 mil-

Full and Fair Reporting 179

P6-6 1. The main theme of the certifications is that the annual report does

2. SOX requires these certifications as a result of several high-profile

frauds and bankruptcies that had a negative effect on investor confi-

P6-7 1. Accounting issues are identified and evaluated for consideration.

Primary documents

Discussion memorandum—identifies accounting issues and alternative

P6-8 Students’ responses will vary because the FASB’s website is dynamic.

However, students should find items as follows:

180 Chapter 6

P6-9 Students’ responses will vary because the IASB’s website is dynamic.

However, students should find items as follows:

• Principal news items

P6–10 Conceptual framework components and purpose

1. Objectives of financial reporting provide an overall purpose for fi-

nancial reports.

P6–11

Useful

Reliability

Relevance

Full and Fair Reporting 181

Qualitative characteristics are attributes that make accounting infor-

mation useful. Understandability and usefulness for decision making are

P6–12 Jenny is facing pressure from a client who is attempting to persuade her

to compromise her professional judgment. If she yields to pressure, the

P6–13 A. The report was issued on October 1, 2008. The report was not issued

in a timely manner. It was released nine months after the year-end.

As a result the information in the financial statements may not be

relevant.

B. The balance sheet included management’s estimates of the in-

C. Procedures used to calculate revenues and expenses were different

for 2007 than for 2006 and earlier years. Information about an organi-

zation is more valuable when it can be compared with information

182 Chapter 6

P6-14 A. Responsibility: Users of financial information must understand that

management is responsible for preparing the statements, while audi-

C. Material misstatement and material respects: Materiality is a criterion

for establishing the importance of a potential misstatement in audit-

D. A test basis: Auditors do not examine all transactions. They use sta-

E. Present fairly . . . in conformity with generally accepted accounting

Full and Fair Reporting 183

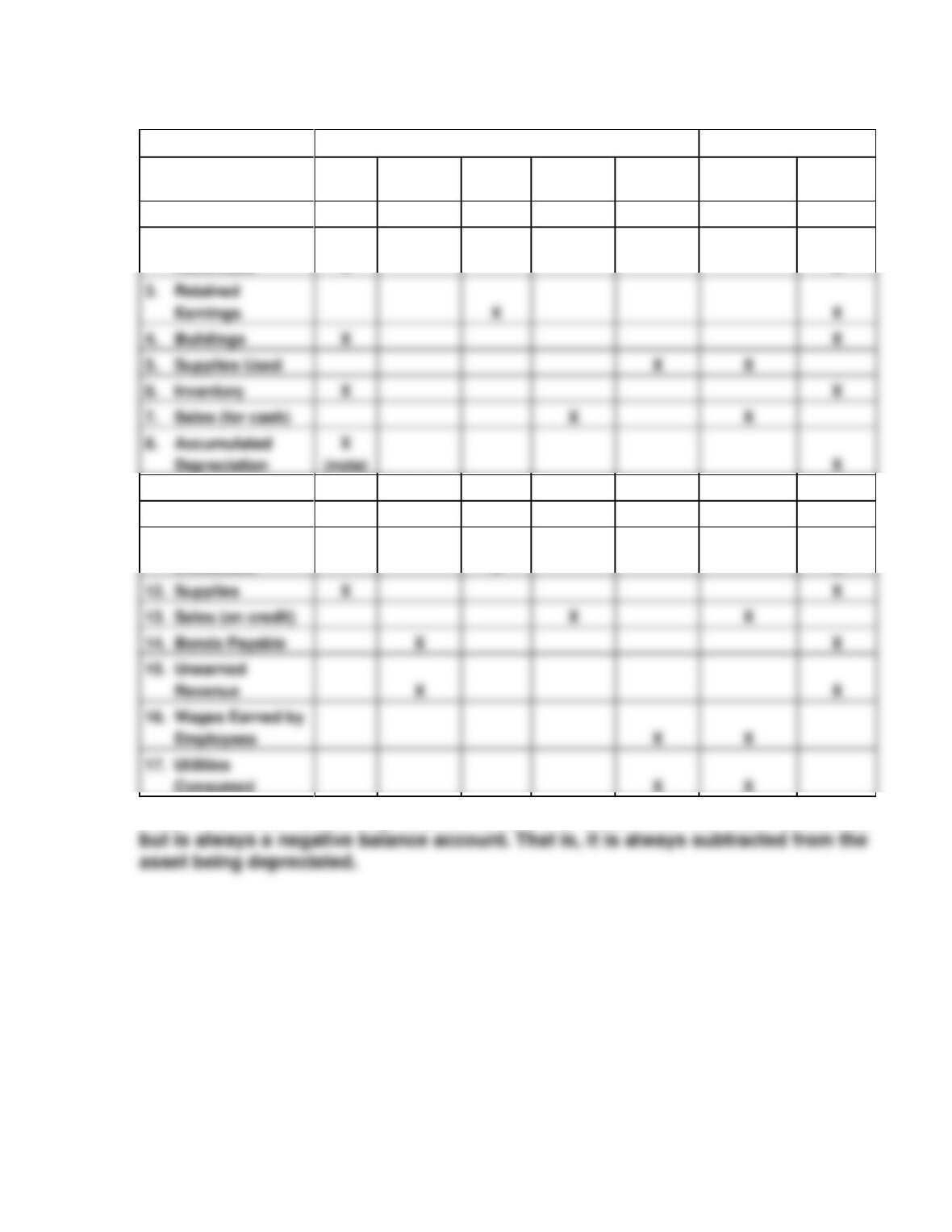

P6-15 A. and B.

Type of Account

Financial Statement

Asset

Liability

Equity

Revenue

Expense

Income

Statement

Balance

Sheet

1. Wages Payable

X

X

2. Accounts

Receivable

X

X

9. Loan from Bank

X

X

10. Land

X

X

11. Owners’

Investment

X

X

12. Supplies

X

X

13. Sales (on credit)

X

14. Bonds Payable

X

X

15. Unearned

X

X

16. Wages Earned by

Employees

X

17. Utilities

X

Note: The accumulated depreciation account is listed with the asset accounts,

3. Retained

Earnings

X

X

4. Buildings

X

X

5. Supplies Used

X

6. Inventory

X

X

7. Sales (for cash)

X

8. Accumulated

Depreciation

X

184 Chapter 6

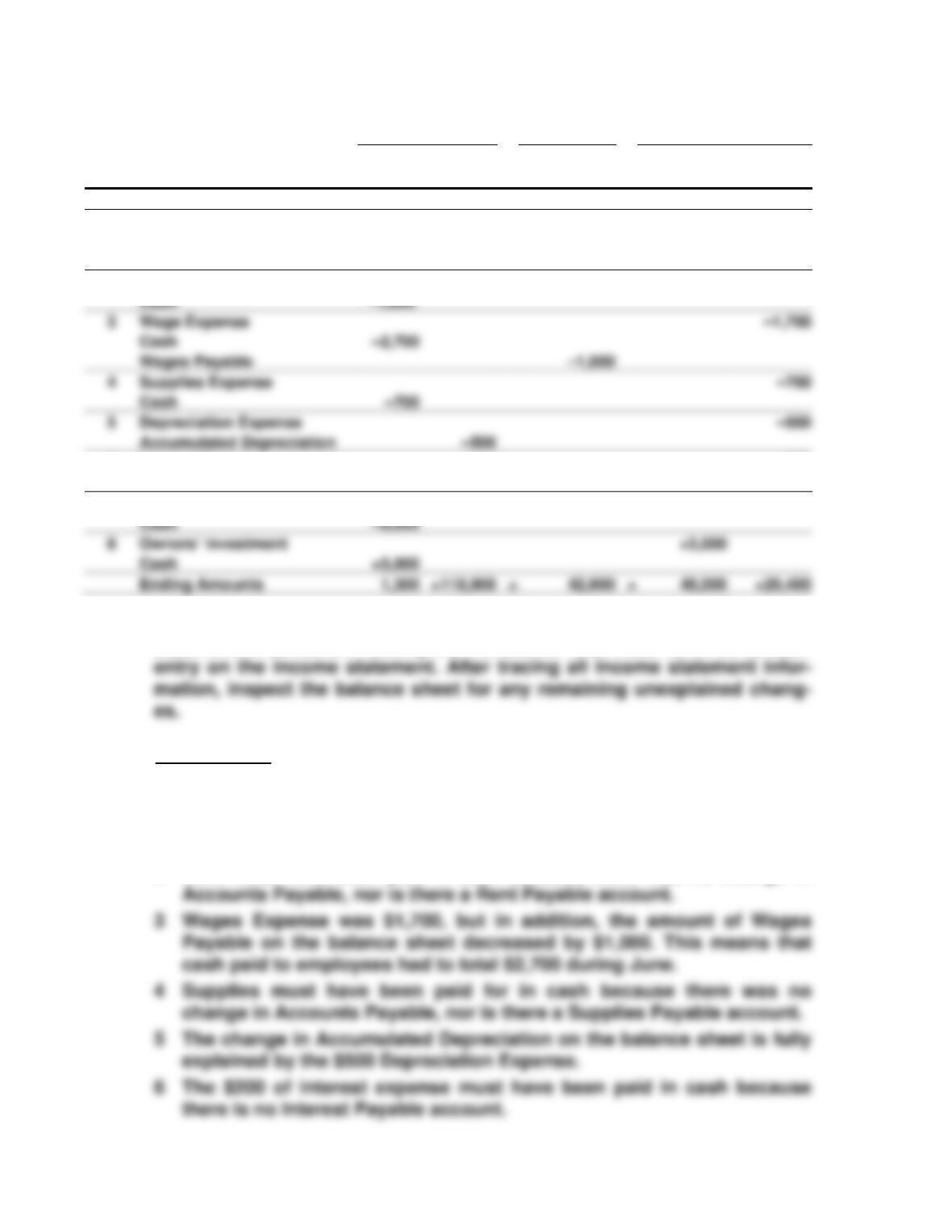

P6-16

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Beginning Amounts

3,200

+119,000

=

52,800

+

43,000

+26,400

1

Cash

+7,500

Accounts Receivable

+400

Service Revenues

+7,900

2

Rent Expense

–1,800

6

Interest Expense

–200

Cash

–200

7

Notes Payable

–9,000

Cash

8

Cash

+5,000

Ending Amounts

=

42,800

+

48,000

Explanations: To solve this problem, it is easiest to start with the income

statement information. Identify the transaction that must have led to each

Transactions

1 Service Revenue during June totaled $7,900 but Accounts Receivable

increased by $400. This means that only $7,500 of the revenue was

collected. The other $400 explains the change in Accounts Receivable

on the balance sheet.

2 Rent must have been paid in cash because there was no change in

Cash

3

Wage Expense

–1,700

Cash

Wages Payable

–1,000

4

Supplies Expense

–700

Cash

–700

5

Depreciation Expense

–500

Accumulated Depreciation

Full and Fair Reporting 185

7 There was a $9,000 decrease in Notes Payable. It was paid off in cash

P6-17 A. The letter was prepared by:

Stephen W. Sanger, Chairman of the Board and Chief Executive Of-

ficer

Stephen R. Demeritt, Vice Chairman

Raymond G. Viault, Vice Chairman

B. The overall tone of the letter is positive.

P6-18 A. General Mills has three business segments.

1. The Retail segment markets ready–to-eat cereals, meals, refrig-

erated and frozen dough products, baking products, snacks,

2. The Bakeries and Foodservice segment markets to retail and

3. The International businesses fundamentally market the same

B. The earnings shortfall was caused primarily by the following:

1. Higher commodity costs

186 Chapter 6

C. Management plans to increase list prices in certain lines, capture

P6–19 A. The company did not fully and accurately disclose the results of its

operations. When investors learned that the reliability of the financial

information was in doubt (as evidenced by an earnings restatement),

P6–20 A. • Specific cash register—Each sales clerk is responsible for one

cash register. If clerks used a variety of cash registers during a

shift, errors and omissions could not be traced to one individual.

• Copy of cash register slip is given to customer. Customers who

receive cash register slips provide another form of internal control

because they help verify that the sale was recorded for the correct

amount.

B. • The movie example illustrates segregation of duties as an internal

control. The ticket seller must produce cash for each ticket that he

Full and Fair Reporting 187

P6–21 The church has no system of internal control. The church did not conduct

an adequate background check before allowing Jay to serve as treasurer.

They have no segregation of duties. Jay has access to resources and in-

P6–22 Yes, such a policy is an example of an internal control to prevent cashiers

from pocketing cash from unrecorded sales. Giving customers receipts is

one way of ensuring that all sales are rung into the cash register. Cus-

tomers will also usually notice if the amounts are incorrect. Therefore, of-

P6–23

1

2

3

4

5

6

7

8

9

10

188 Chapter 6

CASES

C6-1 A. General Mills’ auditor is KPMG LLP. The audit was completed on

June 29, 2004.

B. The auditors’ responsibility is to express an opinion on the financial

statements. Management is responsible for the financial statements.

C6-2 A. Management is responsible for the accounting numbers in the annu-

al report.

B. Companies use a system of internal controls to help safeguard as-

C. The auditor does not state that the amounts are correct. Rather, the

independent public accountant states whether the financial state-