*PROBLEM 6-8A (Continued)

(b)

Gross profit:

LIFO

FIFO

Moving-

Average

Sales

$15,690

$15,690

$15,690

– Cost of goods sold

8,200

7,825

7,927

*PROBLEM 6-9A

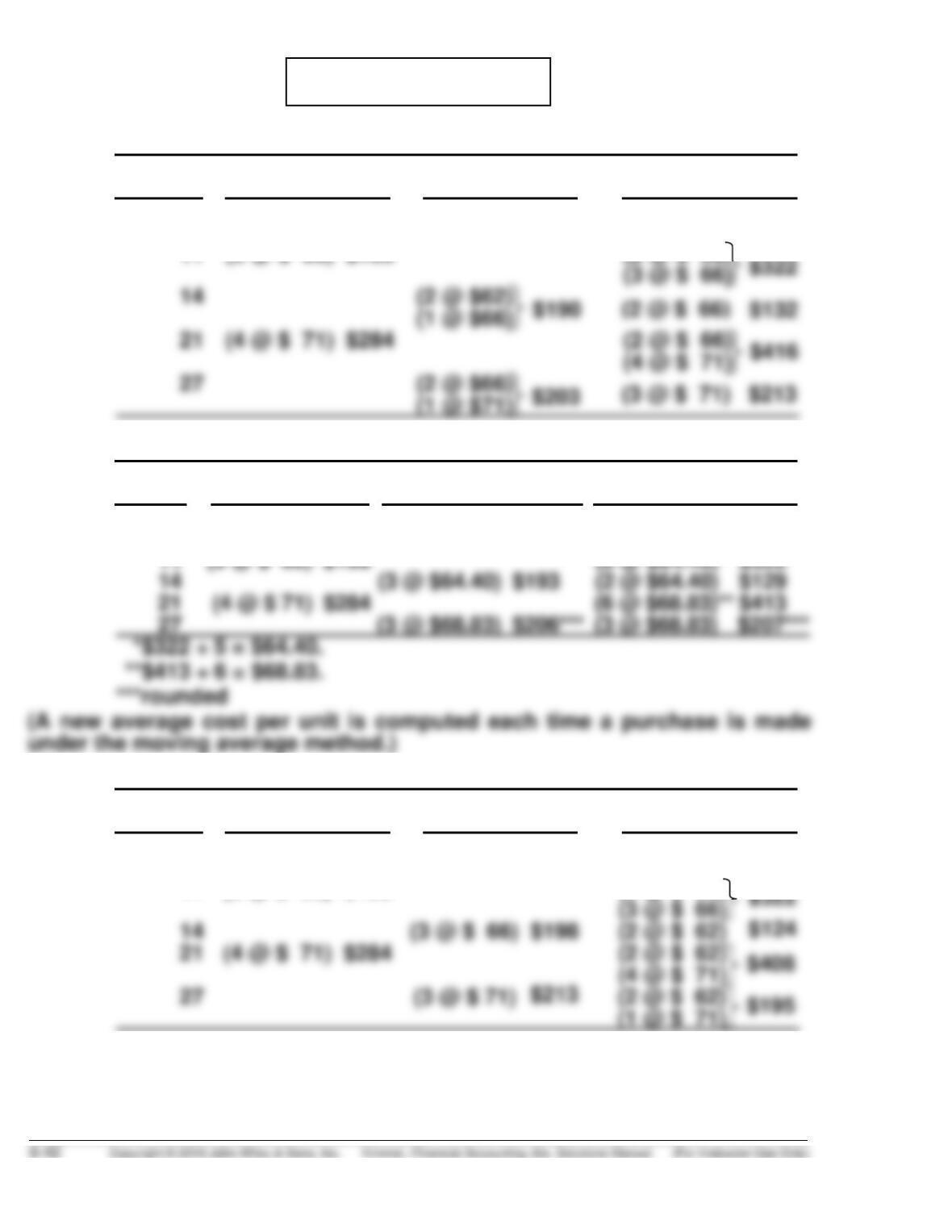

(a) (1) FIFO

Cost of

Date Purchases Goods Sold Balance

July 1 (7 @ $ 62) $434 (7 @ $ 62) $434

6 (5 @ $62) $310 (2 @ $ 62) $124

11 (3 @ $ 66) $198 (2 @ $ 62)

(2) MOVING-AVERAGE

Cost of

Date Purchases Goods Sold Balance

July 1 (7 @ $ 62) $434 (7 @ $62) $434

6 (5 @ $62) $310 (2 @ $62) $124

(3) LIFO

Cost of

Date Purchases Goods Sold Balance

July 1 (7 @ $ 62) $434 (7 @ $ 62) $434

6 (5 @ $ 62) $310 (2 @ $ 62) $124

11 (3 @ $ 66) $198 (2 @ $ 62)

(b) The highest ending inventory is $213 under the FIFO method.

LO 4 BT: AP Difficulty: Hard TOT: 30 min. AACSB: Analytic AICPA FC: Measurement and Reporting

ACCOUNTING CYCLE REVIEW SOLUTION

(a)

Dec. 3

Inventory (4,000 X $0.72) ……………………….

Accounts Payable ………………………….

2,880

2,880

5

Accounts Receivable (4,400 X $0.90) ……..

Sales Revenue ……………………………….

3,960

3,960

Inventory ………………………………………………

Cost of Goods Sold ………………………..

144

144

17

Inventory (2,200 X $0.80) ……………………….

Cash ……………………………………………..

1,760

1,760

Inventory ……………………………………….

1,440

Income Tax Expense …………………………….

Income Taxes Payable ……………………

215

215

ACCOUNTING CYCLE REVIEW SOLUTION (Continued)

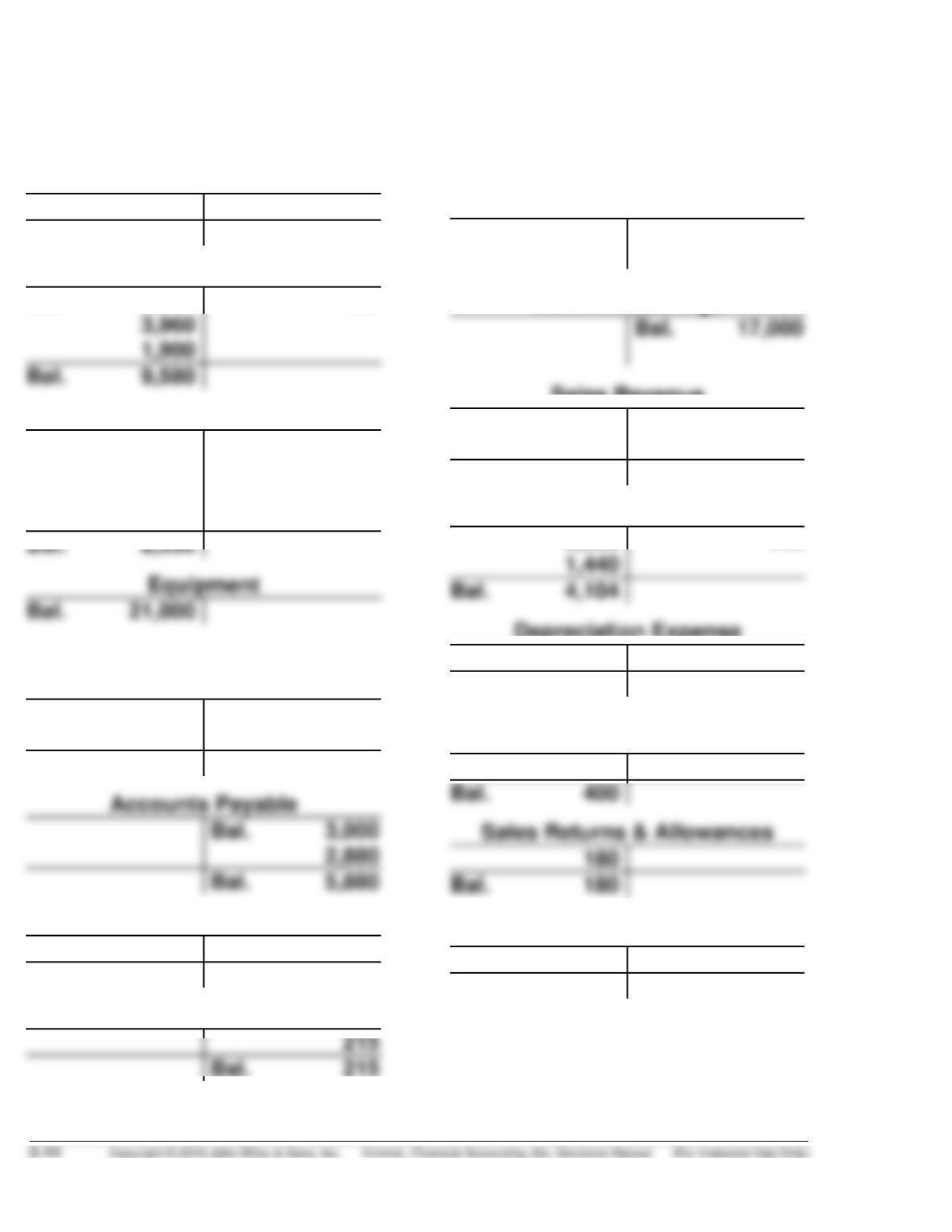

(b) General Ledger

Cash

Bal. 4,800

1,760

Bal. 3,040

Accounts Receivable

Bal. 9,580

Bal. 17,000

Bal. 3,900

180

Inventory

Bal. 1,800

2,880

144

1,760

2,808

1,440

Bal. 2,336

Bal. 21,000

Bal. 4,104

Accumulated

Depreciation—Equipment

Bal. 1,500

200

Bal. 1,700

Bal. 3,000

Bal. 5,880

Bal. 400

Sales Returns & Allowances

180

Bal. 180

Salaries and Wages Payable

400

Bal. 400

Income Taxes Payable

215

Common Stock

Bal. 10,000

Retained Earnings

Sales Revenue

3,960

1,900

Bal. 5,860

Cost of Goods Sold

2,808

144

Depreciation Expense

200

Bal. 200

Salaries and Wages Expense

400

Income Tax Expense

215

Bal. 215

ACCOUNTING CYCLE REVIEW SOLUTION (Continued)

(c) WAYLON COMPANY

Adjusted Trial Balance

December 31, 2017

DR.

CR.

Cash ………………………………………………………

$ 3,040

Accounts Receivable ………………………………

9,580

Inventory ………………………………………………..

2,336

Equipment ……………………………………………..

21,000

Accumulated Depreciation—Equipment …..

$ 1,700

Accounts Payable …………………………………..

5,880

Salaries and Wages Payable ……………………

Income Taxes Payable …………………………….

Common Stock ……………………………………….

10,000

Retained Earnings ………………………………….

17,000

Sales Revenue ………………………………………..

5,860

Sales Returns & Allowances ……………………

180

Cost of Goods Sold ………………………………..

4,104

Salaries and Wages Expense ………………….

Depreciation Expense …………………………….

Income Tax Expense ………………………………

215

$41,055

$41,055

(d) WAYLON COMPANY

Income Statement

For the Month Ending December 31, 2017

Sales revenue ………………………………………

$5,860

Less: Sales returns and allowances …….

180

Net sales ……………………………………………..

$5,680

Cost of goods sold ………………………………

4,104

Gross profit …………………………………………

Operating expenses

Salaries and wages expense ………….

Depreciation expense ……………………

600

Income before income tax …………………….

Income tax expense ……………………………..

215

Net income …………………………………………..

$ 761

ACCOUNTING CYCLE REVIEW SOLUTION (Continued)

WAYLON COMPANY

Balance Sheet

December 31, 2017

Assets

Current assets

Cash ………………………………………………..

$ 3,040

Accounts receivable …………………………

Inventory ………………………………………….

2,336

Total current assets …………………….

Property, plant, and equipment

Equipment ……………………………………….

21,000

Total assets …………………………………………….

Less: Accumulated depreciation—

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable …………………………….

$ 5,880

Salaries and wages payable ……………..

400

Income taxes payable ……………………….

Total current liabilities …………………

$ 6,495

Common stock …………………………………

10,000

Retained earnings ($17,000 + $761) …..

17,761

Total stockholders’ equity ……………

27,761

ACCOUNTING CYCLE REVIEW SOLUTION (Continued)

(e) FIFO Method

Units

Unit Cost

Cost of Goods

Available for Sales

Beg. Inventory

3,000

$0.60

$1,800

Dec. 3 purchase

4,000

$0.72

2,880

Dec. 17 purchase

2,200

$0.80

9,200

$6,440

Dec. 17

2,200 X $0.80 = $1,760

Cost of goods available for sale

$6,440

Dec. 3

Less: Ending inventory

Cost of goods sold

$4,104

(f) LIFO Method

Ending Inventory

Cost of Goods Sold

Dec. 1

3,000 X $0.60 = $1,800

Cost of goods available for sale

$6,440

Less: Ending inventory

Cost of goods sold

$4,640

CT 6-1 FINANCIAL REPORTING PROBLEM

(Note: All dollar amounts are in millions)

(a) Inventories were $2,111 at September 27, 2014 and $1,764 at September

28, 2013.

CT 6-2 COMPARATIVE ANALYSIS PROBLEM

(a) Columbia Sportswear VF Corporation

1. Inventory turnover

$1, 145,639

($384,650 + $329,228) ÷ 2

$6,288,190

($1,482,804 + $1,399,062) ÷ 2

(b) Generally, companies that are able to keep their inventory at lower

levels and higher turnovers and still satisfy customer needs are the

most successful. Both companies have low inventory turnovers. As a

CT 6-3 COMPARATIVE ANALYSIS PROBLEM

(a) Amazon.com Wal-Mart

1. Inventory turnover

$62,752

($7,411 + $8,299) ÷ 2

$365,086__ __

($45,141 + $44,858)/2

CT 6-4 INTERPRETING FINANCIAL STATEMENTS

(a) Finished goods are manufactured inventory items that are ready for

resale. Work in process is inventory that has been put into production

but is not complete. Raw materials are the basic materials that will be

used in production.

(c)

2017

2016

Inventory turnover:

$809,956

($216,671 + $203,873)/2

$780,771

($182,618 + $216,671)/2

(d) The LIFO reserve, $86,025, represents 42% of total inventory

($86,025/$203,873 = .42).

Ending inventory using LIFO ………………… $203,873

CT 6-4 (Continued)

(e) Current ratio:

$561,395 = 1.63 : 1

$343,405

Current assets using LIFO $561,395

$343,405