EXERCISE 6-13

(a)

Inventory

turnover

$16,255

($3,042 + $2,397) ÷ 2 = $16,255

$2,719.5 = 5.98

(b) Based on data presented:

Current ratio $30,857 ÷ $12,753 = 2.42 : 1

(c) After adjusting for the LIFO reserve, Deere’s current ratio increases

*EXERCISE 6-14

(a)

FIFO

Date

Purchases

Cost of goods sold

Balance

June 1

(120 @ $5)

$ 600

June 12

(370 @ $6) $2,220

(120 @ $5)

(370 @ $6)

June 15

(120 @ $5)

(290 @ $6)

$ 480

June 23

(200 @ $7) $1,400

(200 @ $7)

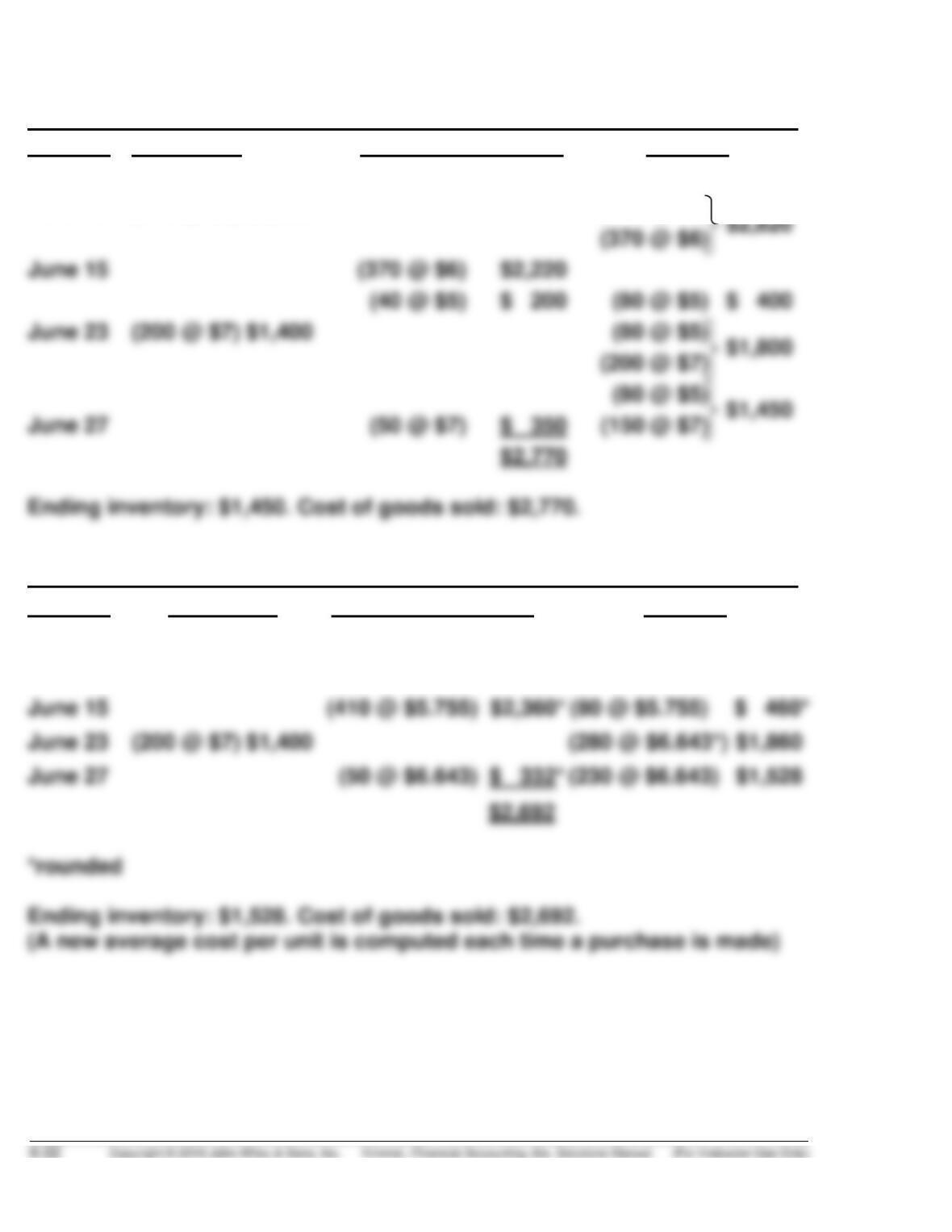

*EXERCISE 6-14 (Continued)

LIFO

Date

Purchases

Cost of Goods Sold

Balance

June 1

(120 @ $5)

$ 600

June 12

(370 @ $6) $2,220

(120 @ $5)

June 15

(370 @ $6)

$ 400

June 23

(200 @ $7) $1,400

(200 @ $7)

June 27

Moving-Average

Date

Purchases

Cost of Goods Sold

Balance

June 1

(120 @ $5)

$ 600

June 12

(370 @ $6) $2,220

(490 @ $5.755)

$2,820

June 15

(410 @ $5.755)

(80 @ $5.755)

$ 460*

*EXERCISE 6-14 (Continued)

(b) FIFO gives the same ending inventory and cost of goods sold values

(c) The simple average would be [($5 + $6 + $7) ÷ 3] or $6. However, the

LO 4 BT: AP Difficulty: Hard TOT: 20 min. AACSB: Analytic AICPA FC: Measurement and Reporting

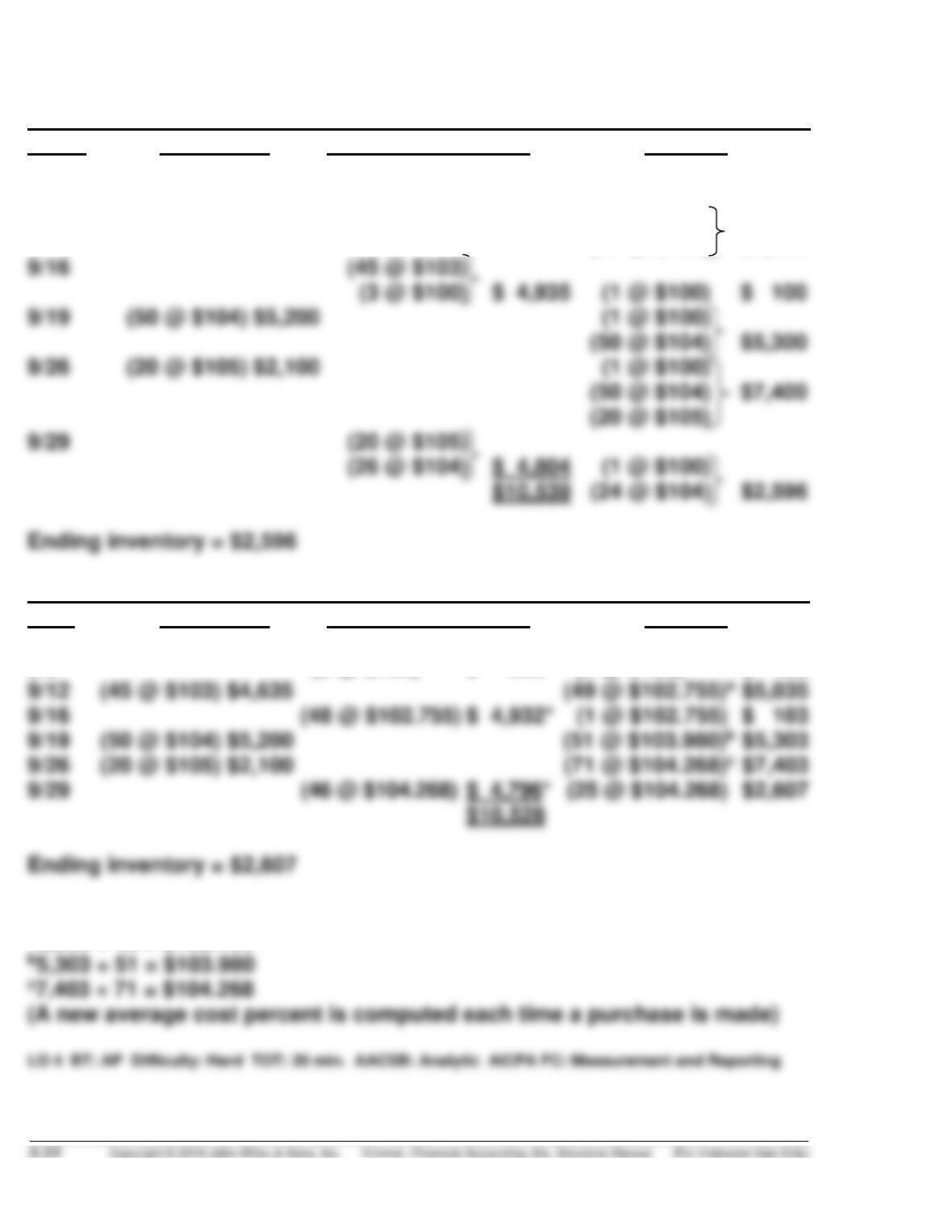

*EXERCISE 6-15

FIFO

Date Purchases Cost of Goods Sold Balance

9/1 (12 @ $100) $1,200

9/5 (8 @ $100) $ 800 (4 @ $100) $ 400

9/12 (45 @ $103) $4,635 (4 @ $100)

(45 @ $103) $5,035

*EXERCISE 6-15 (Continued)

LIFO

Date Purchases Cost of Goods Sold Balance

9/1 (12 @ $100) $1,200

9/5 (8 @ $100) $ 800 (4 @ $100) $ 400

9/12 (45 @ $103) $4,635 (4 @ $100)

(45 @ $103) $5,035

MOVING-AVERAGE

Date Purchases Cost of Goods Sold Balance

9/1 (12 @ $100) $1,200

9/5 (8 @ $100) $ 800 (4 @ $100) $ 400

*Rounded

a5,035 ÷ 49 = $102.755

*EXERCISE 6-16

2016 2017

Beginning inventory ……………………………………………. $ 20,000 $ 28,000

*EXERCISE 6-17

(a)

2016 2017

Sales ……………………………………………………………. $210,000 $250,000

Cost of goods sold

(b) The cumulative effect on total gross profit for the two years is zero as

shown below:

*EXERCISE 6-17 (Continued)

(c) Dear Mr./Ms. President:

Because your ending inventory of December 31, 2016 was overstated

by $8,000, your net income for 2016 was overstated and net income for

2017 was understated by $8,000.

SOLUTIONS TO PROBLEMS

PROBLEM 6-1A

(a) The goods should not be included in inventory as they were shipped

FOB shipping point and shipped February 26. Title to the goods trans-

(b) The amount should not be included in inventory as they were shipped

(c) Include $500 in inventory.

(Legal title determines if an item should be included in inventory)

(d) Include $400 in inventory.

(Legal title determines if an item should be included in inventory)

PROBLEM 6-2A

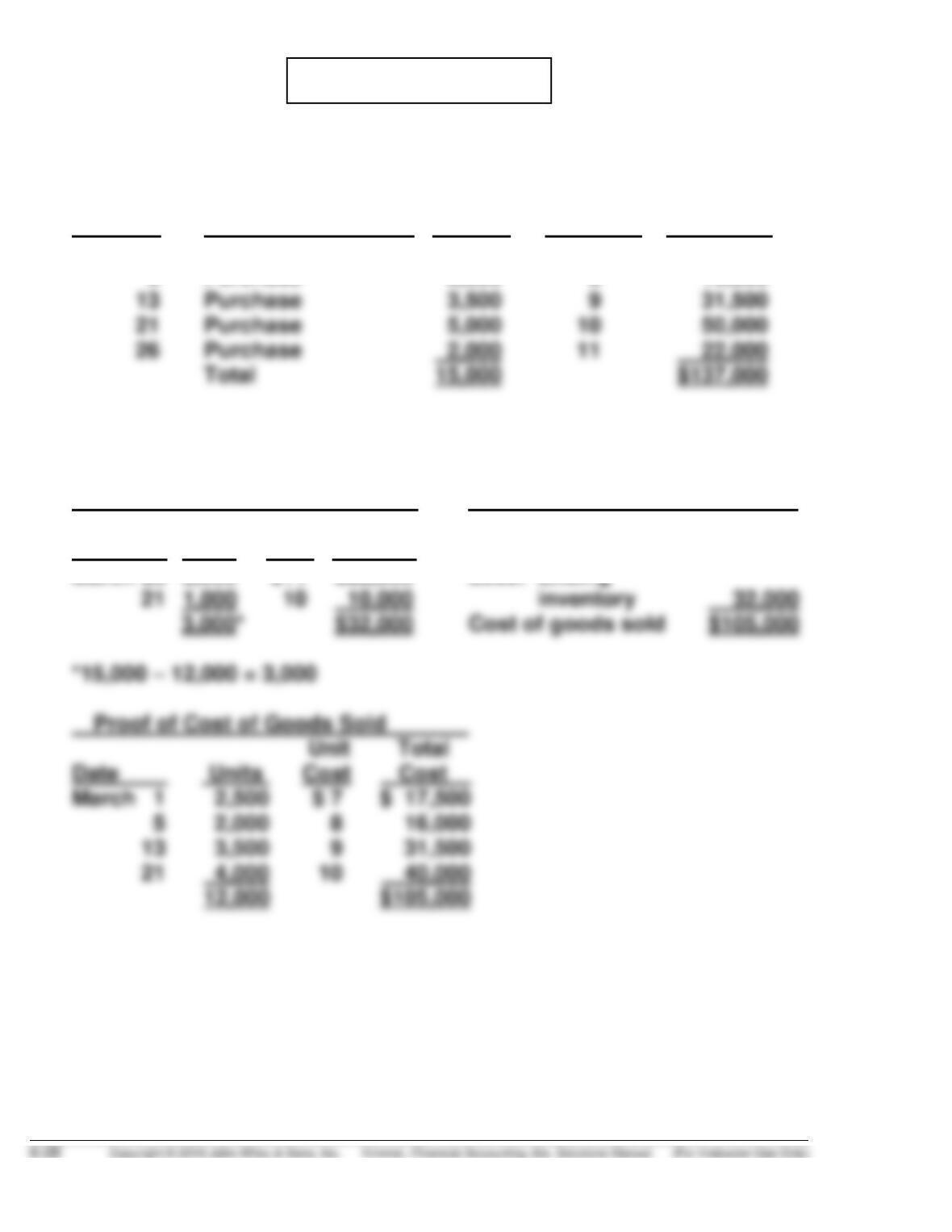

(a)

COST OF GOODS AVAILABLE FOR SALE

Date Explanation Units Unit Cost Total Cost

March 1 Beginning inventory 2,500 $ 7 $ 17,500

5 Purchase 2,000 8 16,000

(b)

FIFO

(1) Ending Inventory (2) Cost of Goods Sold

Unit Total Cost of goods

Date Units Cost Cost available for sale $137,000

March 26 2,000 $11 $22,000 Less: Ending

PROBLEM 6-2A (Continued)

LIFO

(1) Ending Inventory (2) Cost of Goods Sold

Unit Total Cost of goods

Proof of Cost of Goods Sold

Unit Total

Date Units Cost Cost

March 26 2,000 $ 11 $ 22,000

AVERAGE-COST

(1) Ending Inventory (2) Cost of Goods Sold

Cost of goods

$137,000 ÷ 15,000 = $9.133 available for sale $137,000

(c) (1) As shown in (b), FIFO produces the highest inventory amount,

$32,000.

PROBLEM 6-3A

(a) COST OF GOODS AVAILABLE FOR SALE

Date

Explanation

Units

Unit Cost

Total Cost

Jan. 1

Beginning inventory

100

$ 8

$ 800

Feb. 20

Purchase

600

9

5,400

May 5

Purchase

500

5,000

Aug. 12

Purchase

400

4,400

Dec. 8

Purchase

Total

$16,800

(b)

FIFO

(1) Ending Inventory

(2) Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$16,800

Dec. 8

100

$12

$1,200

Less: Ending

Aug. 12

100

inventory

$14,500

Date

Jan. 1

Feb. 20

May 5

Aug. 12

PROBLEM 6-3A (Continued)

LIFO

(1) Ending Inventory

(2) Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$16,800

Jan. 1

100

$8

$ 800

Less: Ending

Feb. 20

100

inventory

Cost of goods sold

$15,100

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Dec. 8

100

$12

$ 1,200

Aug. 12

400

11

May 5

500

10

Feb. 20

$15,100

AVERAGE-COST

(1) Ending Inventory (2) Cost of Goods Sold

Cost of goods

$16,800 ÷ 1,700 = $9.882 available for sale $16,800

Less: Ending

Unit Total inventory 1,976

(c) LIFO results in the lowest inventory amount for the balance sheet,

$1,700.

PROBLEM 6-4A

(a) NATIONAL, INC.

Condensed Income Statements

For the Year Ended December 31, 2017

FIFO LIFO

Sales …………………………………………………………… $750,000 $750,000

Cost of goods sold

Beginning inventory ……………………………… 35,000 35,000

Cost of goods purchased ………………………. 468,500 468,500

Cost of goods available for sale …………….. 503,500 503,500

(b) Answers to questions:

(1) The FIFO method produces the inventory amount that most closely

(2) The LIFO method produces the net income amount that is a more

(3) The FIFO method is most likely to approximate actual physical flow

PROBLEM 6-4A (Continued)

(4) There will be $4,452 additional cash available under LIFO because

income taxes are $66,892 under LIFO and $71,344 under FIFO.

(5) The illusionary gross profit is $15,900 ($378,800 – $362,900) under

FIFO. Under LIFO, National Inc. has recovered the current

replacement cost of the units ($387,100), whereas under FIFO, it

has only recovered the earlier costs ($371,200). This means that

under FIFO, the company must reinvest $15,900 of the gross profit

to replace the units used.

Answer in business-letter form:

Dear National Inc.

After preparing the comparative condensed income statements for

2017 under the FIFO and LIFO methods, we have found the following:

PROBLEM 6-5A

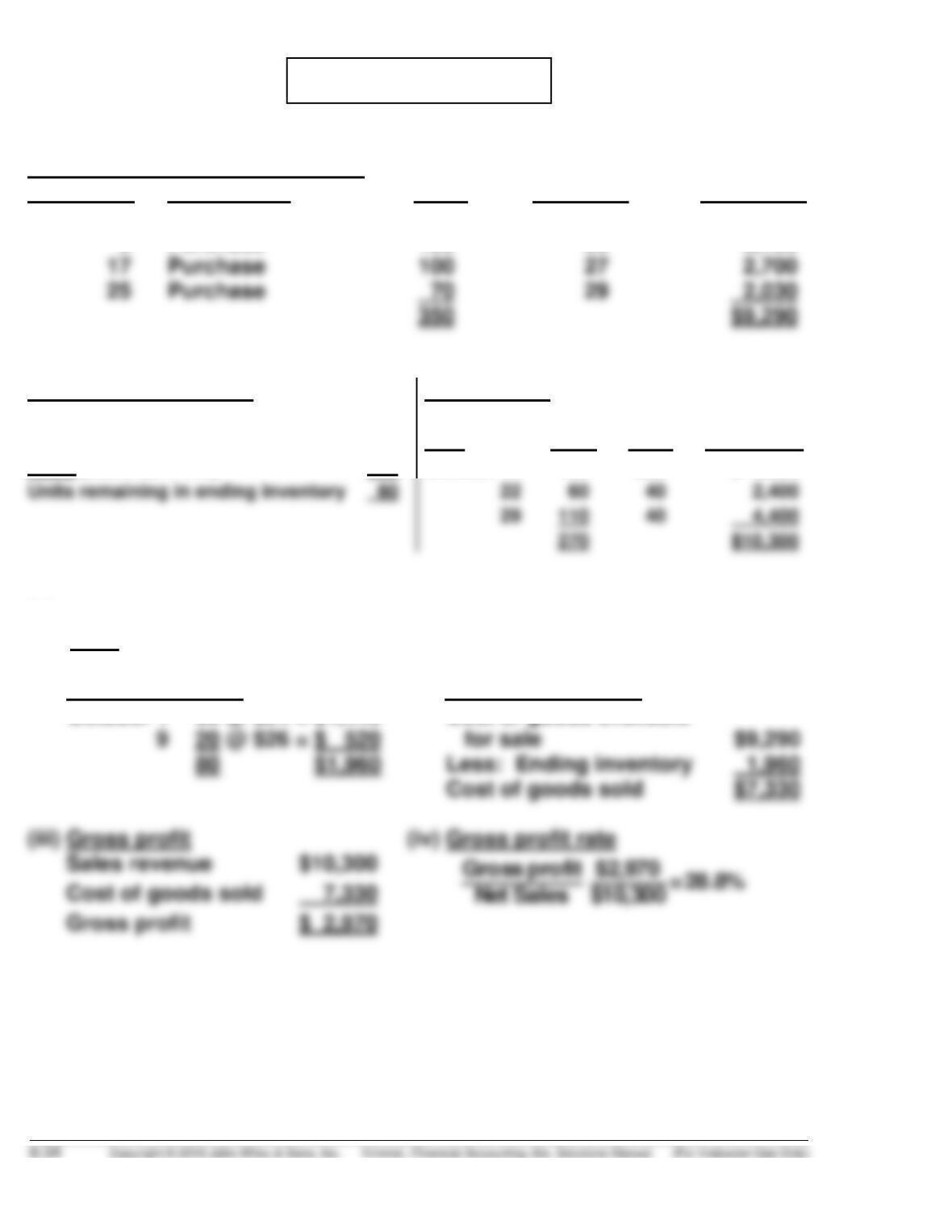

Cost of Goods Available for Sale

Date Explanation Units Unit Cost Total Cost

October 1 Beginning inventory 60 $24 $1,440

9 Purchase 120 26 3,120

Ending Inventory in Units

Sales revenue

Units available for sale

350

Date

Units

Unit

Price

Total Sales

Sales (100 + 60 + 110)

270

October 11

100

$35

$ 3,500

Units remaining in ending inventory

110

4,400

270

$10,300

(a)

(1) LIFO

(i) Ending inventory

(ii) Cost of goods sold

80 $1,960

Less: Ending inventory

Cost of goods sold

(iii) Gross profit

(iv) Gross profit rate

October 1 60 @ $24 = $1,440

Cost of goods available

PROBLEM 6-5A (Continued)

(2) FIFO

(i) Ending inventory

(ii) Cost of goods sold

October 25 70 @ $29 = $2,030

Cost of goods available

for sale

$9,290

October 17 10 @ $27 = $ 270

Less: Ending inventory

Cost of goods sold

(iii) Gross profit

(iv) Gross profit rate

Sales revenue

Gross profit

(3) Average-Cost

Weighted-average cost per unit:

Cost of goods available for sale

Units available for sale

(i) Ending inventory

(ii) Cost of goods sold

*rounded to nearest dollar

Less: Ending inventory

Cost of goods sold

Cost of goods available

(iii) Gross profit

(iv) Gross profit rate

Sales revenue

Gross profit

(b) LIFO produces the lowest ending inventory value, gross profit, and

PROBLEM 6-6A

(a) (1) To maximize gross profit, Jewels’ Gems should sell the diamonds

with the lowest cost.

Sale Date

Cost of goods sold

Sales Revenue

March 5

150 @ $310

$ 46,500

180 @ $600

$108,000

30 @ $350

10,500

March 25

170 @ $350

59,500

390 @ 650

253,500

220 @ $375

$361,500

570

$199,000

(2) To minimize gross profit, Jewels’ Gems should sell the diamonds

with the highest cost.

Sale Date

Cost of goods sold

Sales Revenue

March 5

180 @ $350

$ 63,000

180 @ $600

$108,000

March 25

330 @ $375

123,750

390 @ 650

253,500

40 @ $310

570

$206,150

(b) FIFO

Cost of goods available for sale

March 1

Beginning inventory

150 @ $310

$ 46,500

3

Purchase

200 @ $350

70,000

Purchase

$240,250

Goods available for sale

Units sold

Ending inventory

PROBLEM 6-6A (Continued)

Cost of goods available for sale $240,250

– Ending inventory 41,250

(c) LIFO

Cost of goods available for sale $240,250

(from part b)

(d) The choice of inventory method depends on the company’s objectives.

Since the diamonds are marked and coded, the company could use

specific identification. This could, however, result in “earnings manage–

PROBLEM 6-7A

(a) Inventory

turnover

$166,259

($13,921+ $14,939)÷2

(b) Current

ratio

$60,135

$70,308 =.86:1

*PROBLEM 6-8A

(a)

Sales:

Date

January 6

180 @ $40

$ 7,200

January 10

January 30

130 @ $48

(1) LIFO

Date

Purchases

Cost of goods sold

Balance

January 1

(160 @ $20)

$3,200

January 2

(100 @ $22) $2,200

(160 @ $20)

(100 @ $22)

$5,400

*PROBLEM 6-8A (Continued)

(2) FIFO

Date

Purchases

Cost of goods sold

Balance

January 1

(160 @ $20)

$3,200

January 2

(100 @ $22) $2,200

(160 @ $20)

$5,400

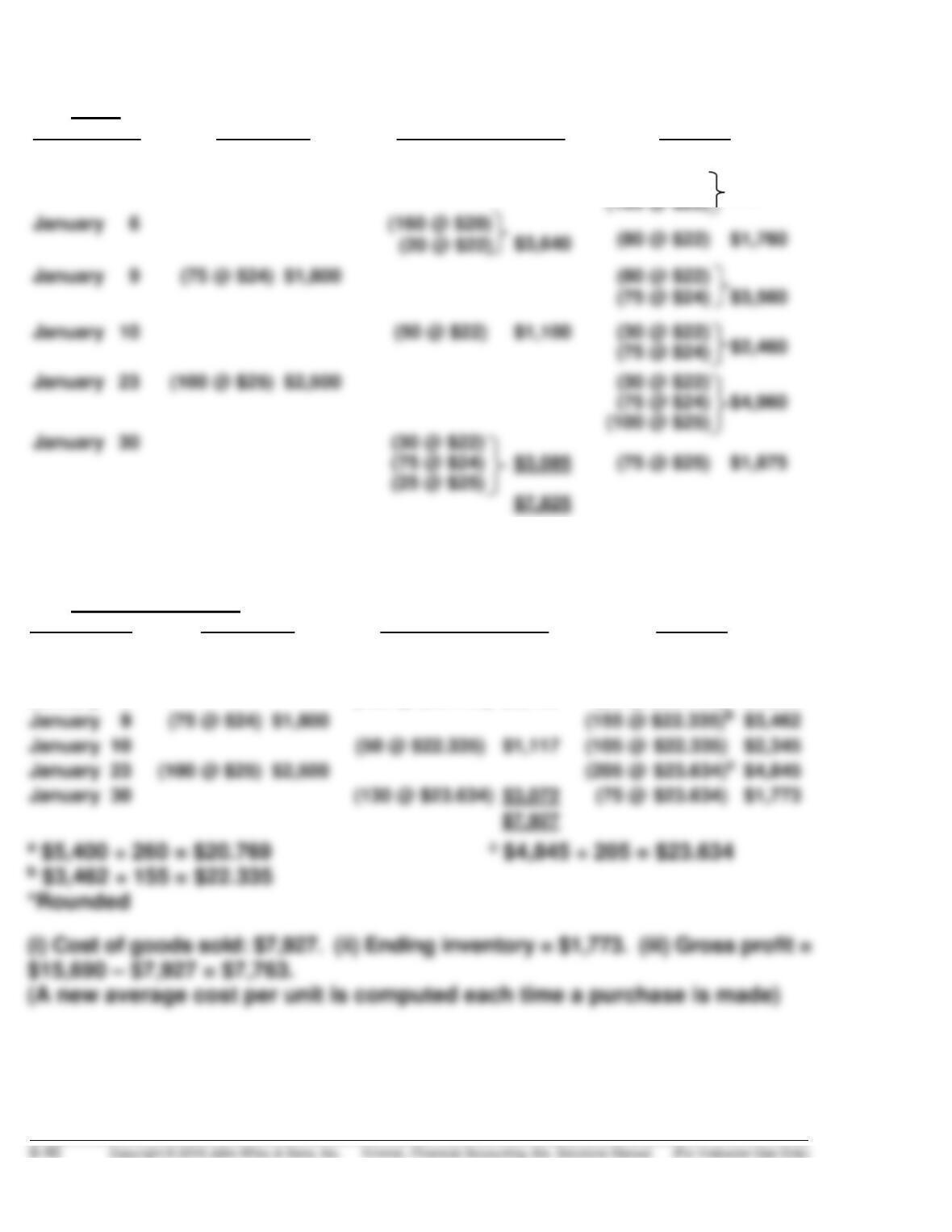

(i) Cost of goods sold: $7,825. (ii) Ending inventory = $1,875. (iii) Gross profit =

$15,690 – $7,825 = $7,865.

(3) Moving-Average:

Date

Purchases

Cost of goods sold

Balance

January 1

(160 @ $20)

$3,200

January 2

(100 @ $22) $2,200

(260 @ $20.769)a

$5,400

January 6

(180 @ $20.769) $3,738*

(80 @ $20.769)

$1,662

January 10

(105 @ $22.335)

January 23

(100 @ $25) $2,500

January 30

(130 @ $23.634) $3,072