6-52

PROBLEM 6-46 (CONTINUED)

(c)

Fixed- and variable-cost components:

Monthly fixed cost = $11,796

Variable cost = $677 per hundred flights

Calculation and interpretation of R 2 using manual calculations

(a)

Formula for calculation:

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

6-53

PROBLEM 6-46 (CONTINUED)

(b)

Tabulation of data:*

Month

Y

X

Predicted Cost (in

thousands)

Based on

Regression

Line Y’

[( Y– Y’)2]†

[(Y –

Y

)2]†

January ……….

20

12

19.920

.006

.340

February ……..

19

10

18.566

.188

.174

March ………….

18

17.889

.012

April ……………

19

14

21.274

.174

May …………….

17

17.212

.045

June ……………

20

11

19.243

.573

.340

July …………….

21

15

21.951

August ………..

17

17.889

.790

21

12

19.920

October ……….

19

10

18.566

.188

.174

November ……

24

14

21.274

December ……

18

11

19.243

=

($11,796 + $677X)/$1,000

(c)

Calculation of R2:

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

SOLUTIONS TO CASES

CASE 6-47 (45 MINUTES)

1.

Cairns’ preliminary estimate for overhead of $18.00 per direct-labor hour does not

distinguish between fixed and variable overhead. This preliminary rate is applicable

only to the activity level at which it was computed (72,000 direct-labor hours per year)

and may not be used to predict total overhead at other activity levels.

2.

Direct material ………………………………………………………………………………….

$390.00

Variable overhead (5 DLH $9.25 per DLH) ………………………………………..

Total variable cost per 1,000 square feet ……………………………………………

$491.25

*DLH denotes direct-labor hours.

3.

The minimum bid should include the following incremental costs of the project.:

Direct material ($390.00 50) …………………………………………………………….

$19,500.00

Variable overhead ($9.25 per DLH 5 DLH 50) ………………………………..

412.50

Minimum bid …………………………………………………………………………………….

4.

decreases.

Yes, Cairns can rely on the formula as long as she recognizes that there are some

shortcomings. The fact that least-squares regression estimates cost behavior

6-55

CASE 6-47 (CONTINUED)

5.

a.

Variable OH1 (50 5 $4.15) ……………………………………………………………..

$1,037.50

Variable OH2 (50 $13.60) …………………………………………………………………

Variable OH3 (70 $5.90) …………………………………………………………………..

413.00

Total incremental variable overhead …………………………………………………..

b.

Variable OH1 (50 5 $4.15) ……………………………………………………………..

$1,037.50

Variable OH2 (25 $13.60) …………………………………………………………………

Variable OH3 (230 $5.90) …………………………………………………………………

Total incremental variable overhead …………………………………………………..

c.

The two scenarios in (a) and (b) differ in terms of the activities to be undertaken.

6-56

CASE 6-48 (45 MINUTES)

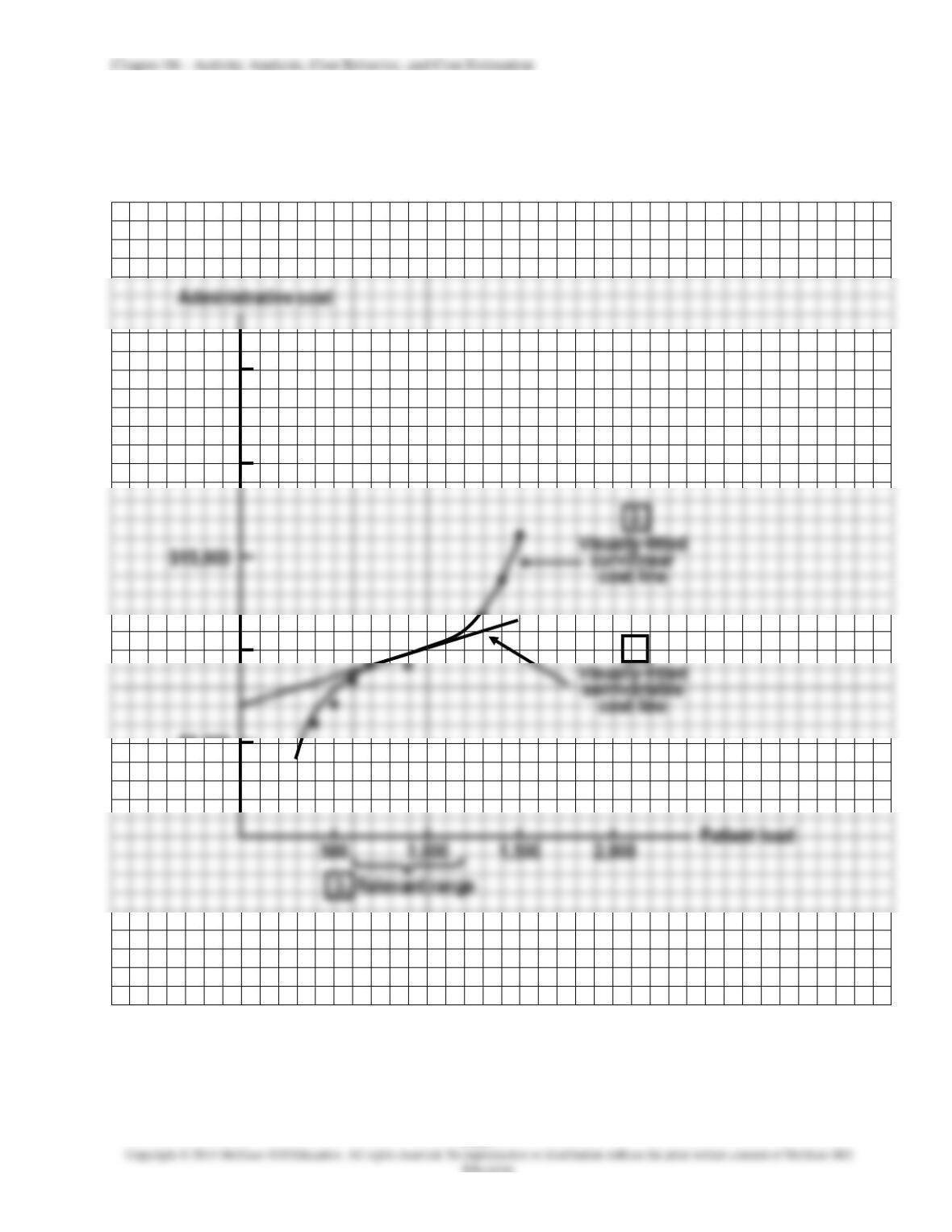

1.

Scatter diagram:

2. through 4.

See scatter diagram for requirement (1).

$25,000

$20,000

$15,000

2.

•

$10,000

$5,000

500

3.

•

•

•

•

•

4.

•

•

•

•

•

CASE 6-48 (CONTINUED)

5.

Fixed cost = $7,000

6.

Administrative cost = $7,000 + $3.00X, where X denotes the number of patients.

7.

Cost predictions using visually-fit cost lines:

Patient

Load

Cost

Prediction

750 …………………

$9,300

350…….

5,500

which is near the middle of the relevant range. However, for a patient load of 350

CASE 6-49 (50 MINUTES)

1.

High-low method:

Total cost at 1,500 patients…………………………………………………………………

Variable cost at 1,500 patients ……………………………………………………………

Fixed cost per month …………………………………………………………………………

$4,100 $16,100 =

−

Cost formula:

Total monthly administrative cost = $1,100 + $10X, where X denotes the number of

The variable cost per patient is $10.

6-58

CASE 6-49 (CONTINUED)

3.

Memorandum

Date:

Today

To:

Jeffrey Mahoney, Administrator

From:

I.M. Student

Subject:

Comparison of cost estimates for clinic administrative costs

Three alternative cost-estimation methods were used to estimate the pediatric clinic’s

administrative cost behavior. The results of these three approaches (in formula form)

are shown below. In each formula, X denotes the number of patients in a month.

(a)

Least-squares regression method:

Total monthly administrative cost = $2,671 + $7.81X

(b)

High-low method:

Total monthly administrative cost = $1,100 + $10X

(c)

Visual-fit method:

Total monthly administrative cost = $7,000 + $3.00X

These cost estimates differ very significantly. The activity level in the clinic

during its first year of operation fluctuated greatly. This fluctuation is not expected in

the future; patient loads in the range of 600 to 1,200 patients per month are

anticipated.

relevant range. Since the regression and high-low estimates are so heavily influenced

6-59

CASE 6-49 (CONTINUED)

Another possible approach would be to use least-squares regression, but

4.

It is very inappropriate for the hospital administrator to manipulate the cost

information supplied by the director of cost management in order to push his own

agenda before the board of trustees. It is the board’s legitimate role to decide whether

or not to establish and continue operations in the clinic. In making decisions about

the clinic, the board should have the best information possible, including the

controller’s best estimate as to how administrative costs will behave.

Megan McDonough, the hospital’s director of cost management, has a

professional obligation to provide her best professional judgment to the board of

trustees. The standards of ethical conduct for management accountants include the

following requirements concerning credibility:

(a)

Communicate information fairly and objectively.

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

6-60

CASE 6-49 (CONTINUED)

The following alternative approach to calculating the regression parameters is not a

requirement in the problem.

Least-squares regression using manual calculations

(a)

Tabulation of data:

Month

Dependent

Variable

(cost in

hundreds)

Y

Independent

Variable

(patients in

hundreds)

X

X2

XY

January …………………..

60

4

16

240

February …………………

70

5

25

350

March ……………………..

139

14

196

1,946

April ……………………….

92

9

81

828

May ………………………..

119

13

169

1,547

June ……………………….

100

10

100

1,000

July ………………………..

94

7

49

658

August ……………………

41

3

9

123

September ………………

102

11

121

1,122

October …………………..

November ……………….

83

6

36

498

December ……………….

(b)

Calculation of parameters:

a

=

))(( )(

))(( ))((

2

2

XXXn

XYXXY

−

−

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

6-61

CASE 6-49 (CONTINUED)

(c)

Cost behavior in formula form (with rounded parameters):*

$7.81 per patient.

(d)

The variable cost per patient is $7.81, as explained above.

FOCUS ON ETHICS (See page 245 in the text.)

Is direct labor a variable cost? Is it ethical to “tap and zap” employees?

Direct labor is a variable cost if management is both able and willing to continually

adjust the workforce to meet short-term needs. Many observers would argue that it is