EXERCISE 6-10 (Continued)

(b) The cumulative effect on total gross profit for the two years is zero as

shown below:

(c) Dear Mr./Ms. President:

Because your ending inventory of December 31, 2016 was overstated

by $6,000, your net income for 2016 was overstated by $6,000. For 2017

net income was understated by $6,000.

In a periodic system, the cost of goods sold is calculated by deducting

the cost of ending inventory from the total cost of goods you have

The error also affects the balance sheet at the end of 2016. The inven–

tory reported in the balance sheet is overstated; therefore, total assets

are overstated. The overstatement of the 2016 net income results in the

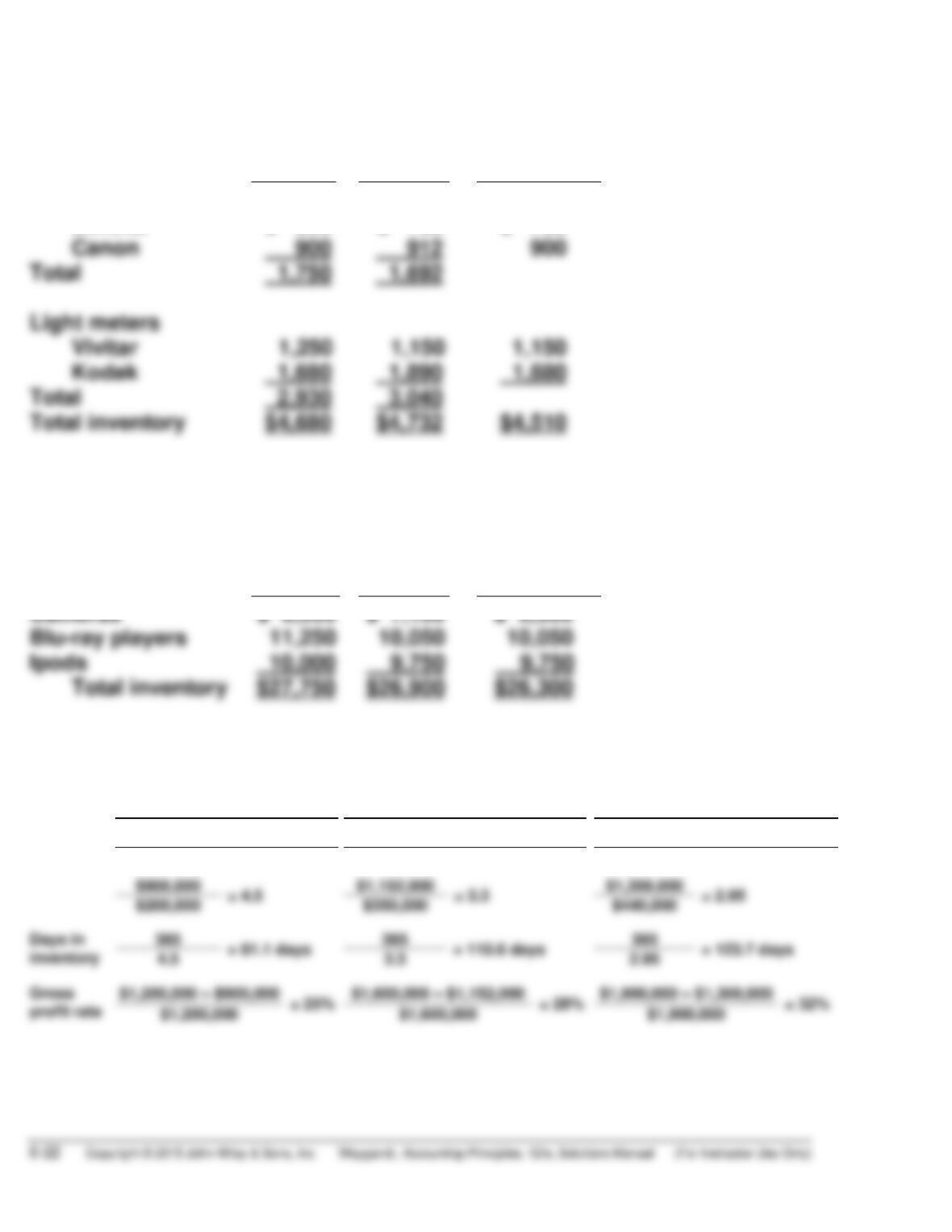

EXERCISE 6-11

Cost

Market

Lower

–of-Cost

–or-Market:

Cameras

Minolta

$ 850

$ 780

$ 780

Canon

900

912

Total

Light meters

Vivitar

1,250

1,150

1,150

Kodak

1,680

1,890

1,680

Total

Total inventory

EXERCISE 6-12

Cost

Market

Lower

–of-Cost-

or-Market:

Cameras

$ 6,500

$ 7,100

$ 6,500

Blu-ray players

11,250

10,050

10,050

Ipods

9,750

Total inventory

EXERCISE 6-13

2015

2016

2017

Inventory

turnover

$900,000

$1,152,000

$1,300,000

($100,000 + $300,000) ÷ 2

($300,000 + $400,000) ÷ 2

($400,000 + $480,000) ÷ 2

$900,000

$200,000

Days in

inventory

EXERCISE 6-13 (Continued)

The inventory turnover decreased by approximately 34% from 2015 to 2017

while the days in inventory increased by almost 53% over the same time

period. Both of these changes would be considered negative since it’s

EXERCISE 6-14

(a)

Sooner Company

Later Company

Inventory Turnover

$190,000

$292,000

($45,000 + $55,000)/2

($71,000 + $69,000)/2

*EXERCISE 6-15

(1)

FIFO

Date

Purchases

Cost of Goods Sold

Balance

Jan. 1

(3 @ $600)

$1,800

8

(2 @ $600) $1,200

(1 @ $600)

600

(6 @ $660) $3,960

(1 @ $600)

(6 @ $660)

(1 @ $600)

(2)

LIFO

Date

Purchases

Cost of Goods Sold

Balance

Jan. 1

(3 @ $600)

$1,800

8

(2 @ $600) $1,200

(1 @ $600)

600

(6 @ $660) $3,960

(1 @ $600)

(6 @ $660)

(1 @ $600)

*EXERCISE 6-15 (Continued)

(3)

MOVING-AVERAGE COST

Date

Purchases

Cost of Goods Sold

Balance

Jan. 1

(3 @ $600) $1,800

8

(2 @ $600) $1,200

(1 @ $600) 600

*EXERCISE 6-16

(a) The cost of goods available for sale is:

June 1 Inventory

200 @ $5

$1,000

June 12 Purchase

June 23 Purchase

300 @ $7

Total cost of goods available for sale

FIFO

Date

Purchases

Cost of Goods Sold

Balance

June 1

(200 @ $5)

$1,000

June 12

(400 @ $6) $2,400

(200 @ $5)

June 15

(200 @ $5)

$ 960

June 23

(300 @ $7) $2,100

(300 @ $7)

June 27

$ 700

*EXERCISE 6-16 (Continued)

LIFO

Date

Purchases

Cost of Goods Sold

Balance

June 1

(200 @ $5)

$1,000

June 12

(400 @ $6) $2,400

(200 @ $5)

}

$3,400

(400 @ $6)

June 15

$ 200

(160 @ $5)

(160 @ $5)

}

$2,900

June 23

June 27

(300 @ $7)

$2,100

Moving-Average Cost

Date

Purchases

Cost of Goods Sold

Balance

June 1

(200 @ $5) $1,000

June 12

(400 @ $6) $2,400

(600 @ $5.666) $3,400

June 15

June 23

(300 @ $7) $2,100

(460 @ $6.537) $3,007

June 27

(b) FIFO gives the same ending inventory and cost of goods sold values

under both the periodic and perpetual inventory system. LIFO and

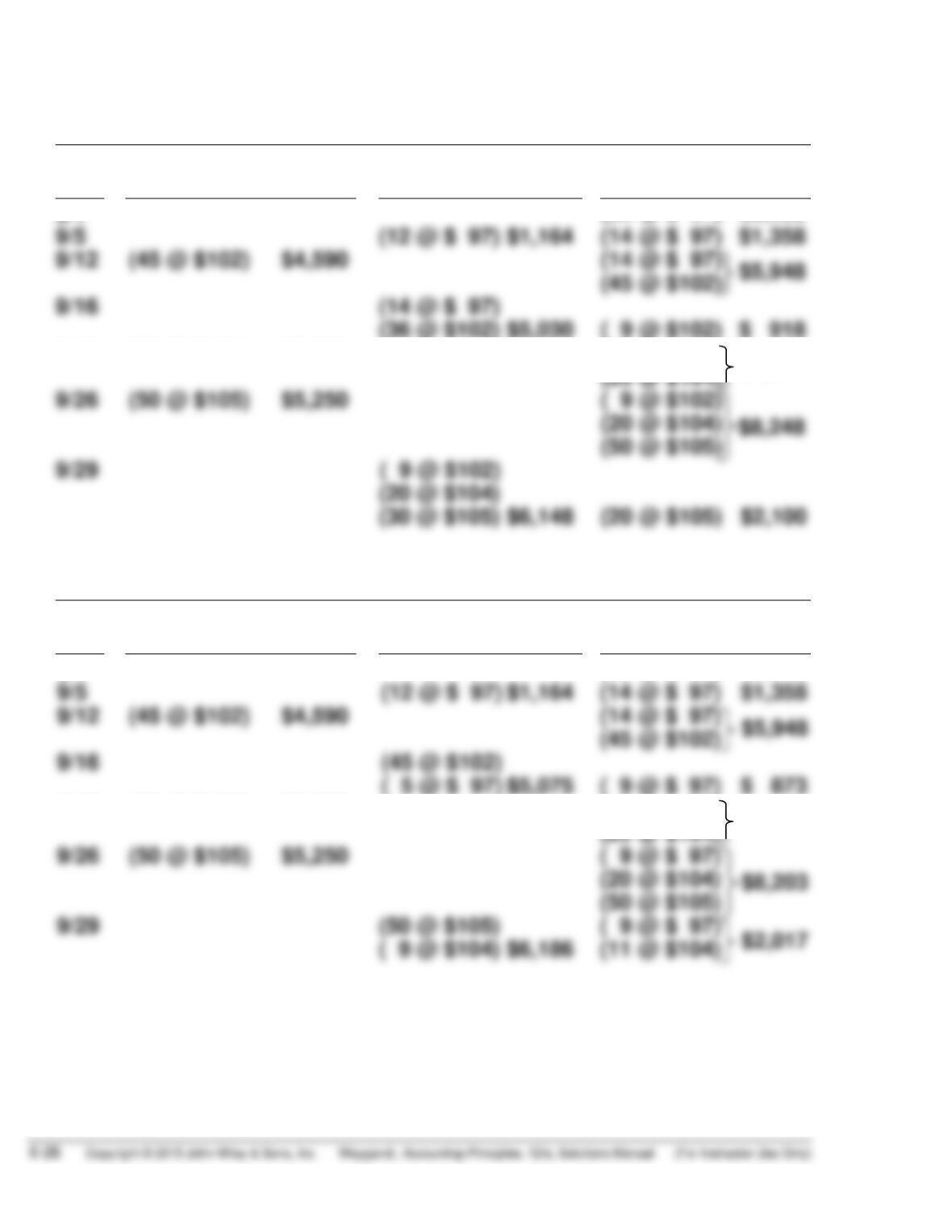

*EXERCISE 6-17

(a)

FIFO

Date

Purchases

Cost of

Goods Sold

Balance

9/1

(26 @ $ 97)

$2,522

9/5

(12 @ $ 97) $1,164

(14 @ $ 97)

$1,358

9/12

(45 @ $102) $4,590

(14 @ $ 97)

(45 @ $102)

9/16

(14 @ $ 97)

(36 @ $102) $5,030

( 9 @ $102)

$ 918

9/19

(20 @ $104) $2,080

( 9 @ $102)

$2,998

(20 @ $104)

9/26

(50 @ $105) $5,250

( 9 @ $102)

(20 @ $104)

(50 @ $105)

9/29

( 9 @ $102)

(20 @ $104)

(30 @ $105) $6,148

(20 @ $105) $2,100

LIFO

Date

Purchases

Cost of

Goods Sold

Balance

9/1

(26 @ $ 97)

$2,522

9/5

(12 @ $ 97) $1,164

(14 @ $ 97)

$1,358

9/12

(45 @ $102) $4,590

(14 @ $ 97)

(45 @ $102)

9/16

(45 @ $102)

( 5 @ $ 97) $5,075

( 9 @ $ 97)

$ 873

9/19

(20 @ $104) $2,080

( 9 @ $ 97)

$2,953

(20 @ $104)

9/26

(50 @ $105) $5,250

( 9 @ $ 97)

$8,203

(20 @ $104)

(50 @ $105)

9/29

(50 @ $105)

( 9 @ $ 97)

( 9 @ $104) $6,186

(11 @ $104)

*EXERCISE 6-17 (Continued)

Moving-Average Cost

Date

Purchases

Cost of

Goods Sold

Balance

9/1

(26 @ $97) $2,522

9/5

(12 @ $97) $1,164

(14 @ $97) $1,358

9/12

(45 @ $102) $4,590

9/16

(50 @ $100.81) $5,041*

( 9 @ $100.81) $ 907

9/19

(20 @ $104) $2,080

9/26

(50 @ $105) $5,250

9/29

(59 @ $104.27) $6,152*

(20 @ $104.27) $2,085

*Rounded

a $5,948 ÷ 59 = $100.81

(b)

Periodic

Perpetual

Ending Inventory FIFO

$2,100

$2,100

Ending Inventory LIFO

$1,940

$2,017

*EXERCISE 6-18

(a) Sales …………………………………………………………… $840,000

Cost of goods sold

Inventory, November 1 …………………………. $130,000

*EXERCISE 6-18 (Continued)

(b) Sales …………………………………………………………………………… $1,000,000

Less: Estimated gross profit (35% X $1,000,000) …………… 350,000

*EXERCISE 6-19

(a) Net sales ($51,000 – $1,000) ………………………………………….. $50,000

Less: Estimated gross profit (30% X $50,000) ……………….. 15,000

Estimated cost of goods sold ……………………………………….. $35,000

(b) Net sales ……………………………………………………………………… $50,000

Less: Estimated gross profit (40% X $50,000) ……………….. 20,000

Estimated cost of goods sold ……………………………………….. $30,000

*EXERCISE 6-20

Women’s Shoes

Men’s Shoes

Cost

Retail

Cost

Retail

Beginning inventory

$ 25,000

$ 46,000

$ 45,000

$ 60,000

Goods purchased

110,000

179,000

136,300

185,000

Less: Net sales

178,000

185,000

Ending inventory at retail

$ 47,000

$ 60,000

PROBLEM 6-1A

(a) The sale will be recorded on February 26. The goods (cost, $800) should

be excluded from Houghton’s February 28 inventory.

(b) Houghton owns the goods once they are shipped on February 26.

Include inventory of $480.

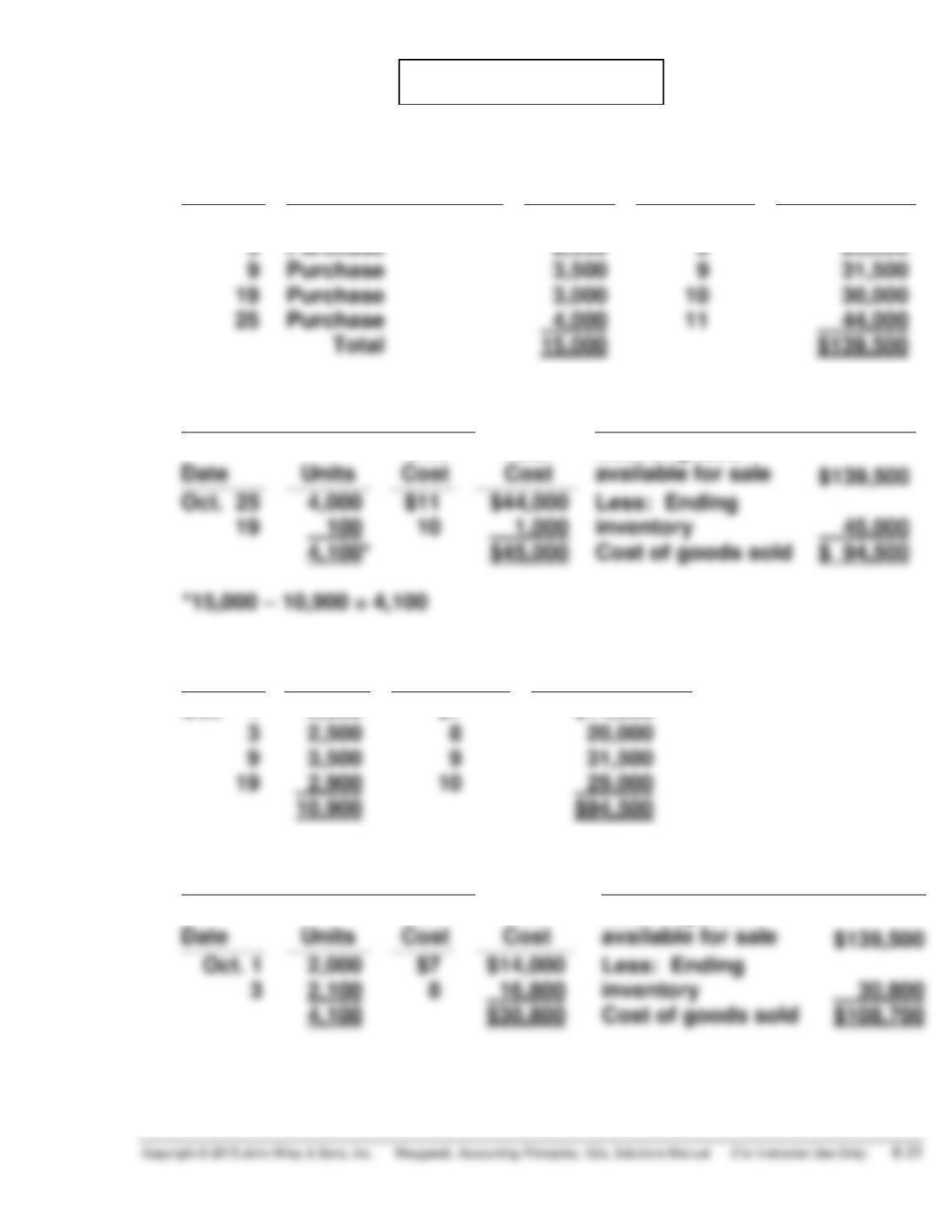

PROBLEM 6-2A

(a)

COST OF GOODS AVAILABLE FOR SALE

Date

Explanation

Units

Unit Cost

Total Cost

Oct. 1

Beginning Inventory

2,000

$7

$ 14,000

3

Purchase

2,500

8

20,000

Purchase

3,500

Purchase

Purchase

(b)

FIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$139,500

$11

Cost of goods sold

Proof of Cost of Goods Sold

Date

Units

Unit Cost

Total Cost

Oct. 1

2,000

$7

$14,000

3

2,500

8

20,000

9

3,500

9

10

LIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$139,500

8

Cost of goods sold

PROBLEM 6-2A (Continued)

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Oct. 25

4,000

$11

$ 44,000

9

9

AVERAGE COST

(1)

Ending Inventory

(2)

Cost of Goods Sold

$139,500 ÷ 15,000 = $9.30

Cost of goods available

for sale

Total Cost

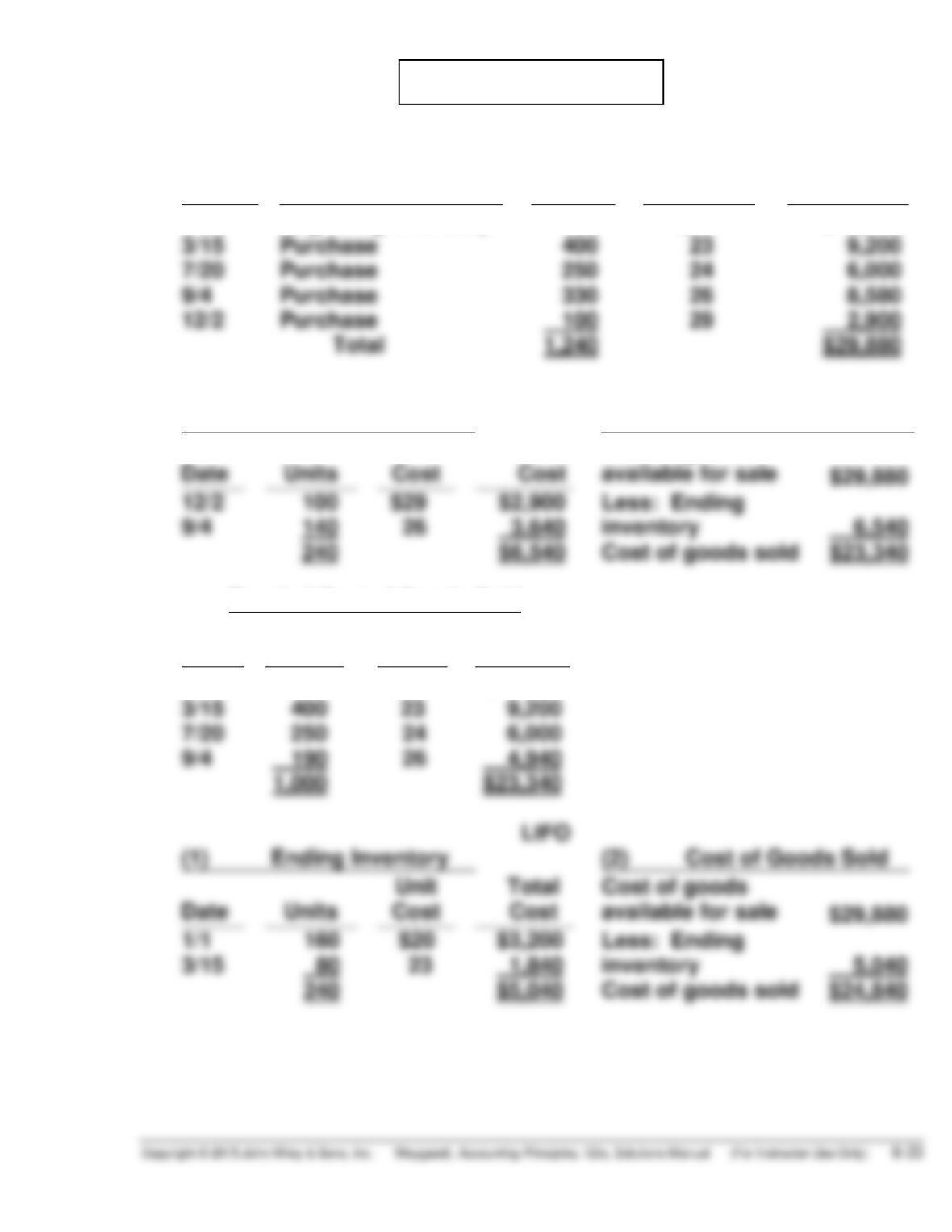

PROBLEM 6-3A

(a)

COST OF GOODS AVAILABLE FOR SALE

Date

Explanation

Units

Unit Cost

Total Cost

1/1

Beginning Inventory

160

$20

$ 3,200

3/15

Purchase

400

23

9,200

7/20

Purchase

250

9/4

Purchase

330

26

12/2

Purchase

100

29

(b)

FIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

12/2

$29

9/4

Cost of goods sold

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

1/1

160

$20

$ 3,200

3/15

400

23

9,200

7/20

9/4

190

4,940

1,000

Ending Inventory

(2)

1/1

3/15

Cost of goods sold

PROBLEM 6-3A (Continued)

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total Cost

12/2

100

$29

$ 2,900

9/4

330

26

8,580

7/20

250

3/15

23

AVERAGE COST

(1)

Ending Inventory

(2)

Cost of Goods Sold

$29,880 ÷ 1,240 = $24.097

Cost of goods available

for sale

Cost of goods sold

(c) (1) FIFO results in the highest inventory amount, $6,540, as shown in

(b) above.

PROBLEM 6-4A

(a) GRESA INC.

Condensed Income Statements

For the Year Ended December 31, 2017

FIFO

LIFO

Sales revenue ………………………………….. $747,000 $747,000

Cost of goods sold

Beginning inventory …………………… 14,000 14,000

Cost of goods purchased ……………. 466,000 466,000

Cost of goods available for sale ….. 480,000 480,000

(b) (1) The FIFO method produces the most meaningful inventory amount

for the balance sheet because the units are costed at the most

recent purchase prices.

(4) There will be $3,960 additional cash available under LIFO because

income taxes are $69,200 under LIFO and $73,160 under FIFO.

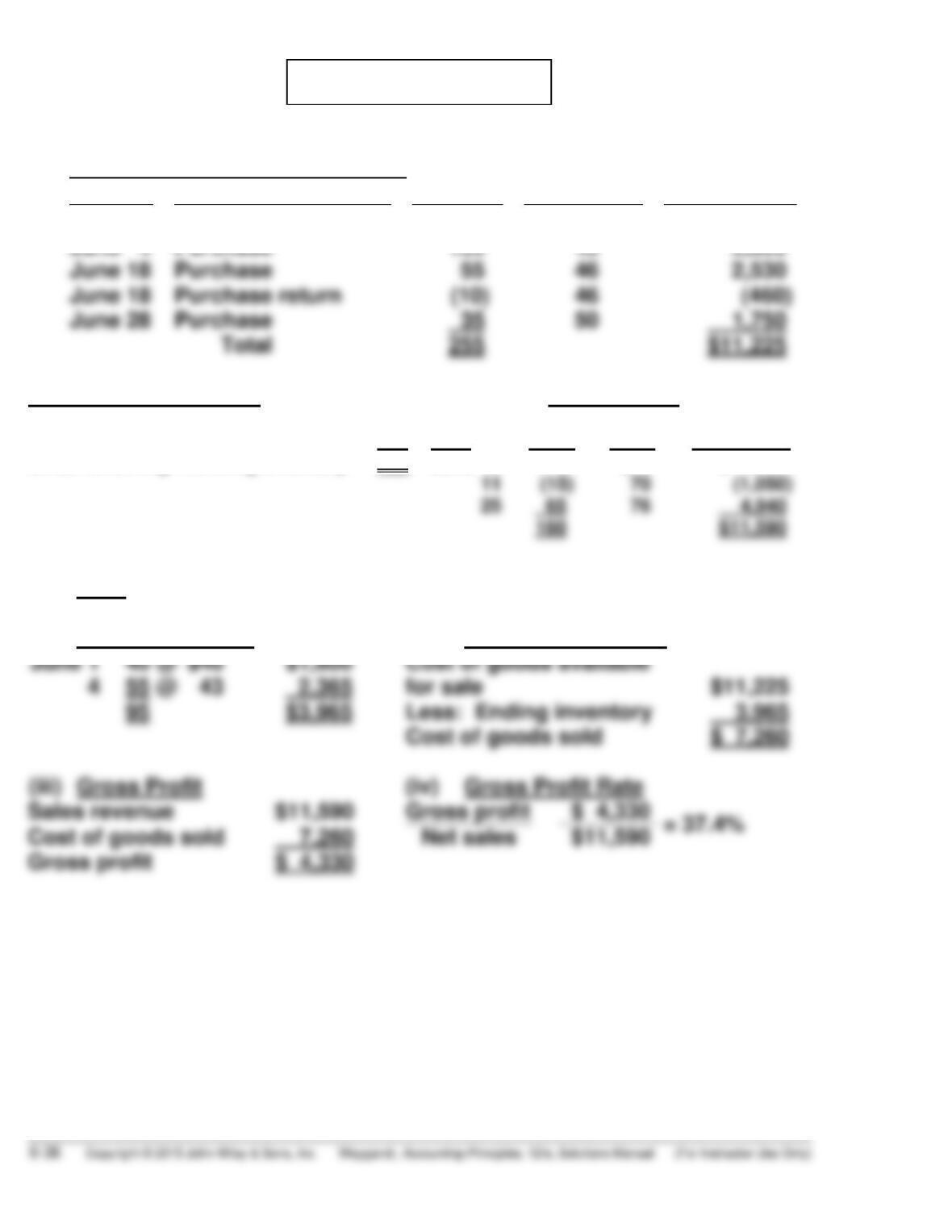

PROBLEM 6-5A

(a)

Cost of Goods Available for Sale

Date

Explanation

Units

Unit Cost

Total Cost

June 1

Beginning Inventory

40

$40

$ 1,600

June 4

Purchase

135

43

5,805

June 18

Purchase

55

2,530

June 18

Purchase return

46

(460)

June 28

Purchase

50

1,750

Ending Inventory in Units:

Sales Revenue

Units available for sale

255

Unit

Sales (110 – 15 + 65)

160

Date

Units

Price

Total Sales

Units remaining in ending inventory

95

June 10

110

$70

$ 7,700

(15)

65

4,940

(1)

LIFO

(i)

Ending Inventory

(ii)

Cost of Goods Sold

June 1

4

40 @ $40

55 @ 43

$1,600

2,365

Cost of goods available

for sale

$11,225

Less: Ending inventory

Cost of goods sold

(iii)

Gross Profit

(iv)

Gross Profit Rate

Sales revenue

Gross profit

Cost of goods sold

Gross profit

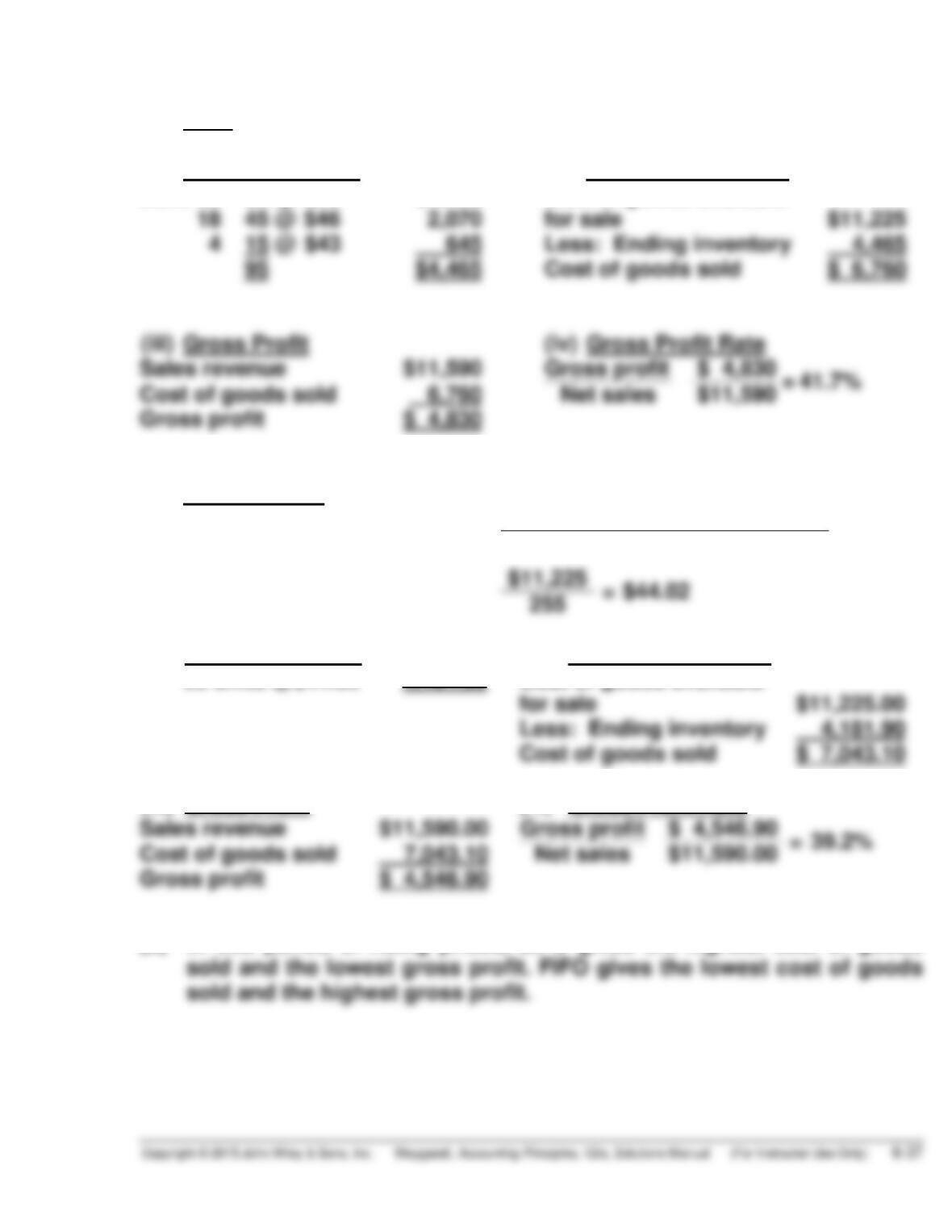

PROBLEM 6-5A (Continued)

(2)

FIFO

(i)

Ending Inventory

(ii)

Cost of Goods Sold

June 28

18

35 @ $50

45 @ $46

$1,750

2,070

Cost of goods available

for sale

$11,225

Less: Ending inventory

Cost of goods sold

(iii)

Gross Profit

(iv)

Gross Profit Rate

Sales revenue

Gross profit

$ 4,830

Cost of goods sold

$11,590

Gross profit

(3)

Average-Cost

Weighted-average cost per unit:

Cost of goods available for sale

Units available for sale

(i)

Ending Inventory

(ii)

Cost of Goods Sold

95 units @$44.02

4,181.90

Cost of goods available

for sale

$11,225.00

Less: Ending inventory

4,181.90

Cost of goods sold

$ 7,043.10

(iii)

Gross Profit

(iv)

Gross Profit Rate

Sales revenue

$11,590.00

Gross profit

$ 4,546.90

Cost of goods sold

Gross profit

$ 4,546.90

PROBLEM 6-6A

(a) GOBLER INC.

Income Statement (partial)

For the Year Ended December 31, 2017

Specific Identification

FIFO

LIFO

Sales revenuea

$8,915

$8,915

$8,915

Beginning inventory

1,200

1,200

1,200

Cost of goods sold

Gross profit

$3,715

$3,930

$3,385

(a)(2,300 @ $1.05) + (5,200 @ $1.25)

(c)Specific identification ending inventory consists of:

Beginning inventory (2,000 liters – 1,000 – 450)

550 @ $.60

$ 330.00

March 3 purchase (2,500 liters – 1,300 – 550)

650 @ $.65

March 10 purchase (4,000 liters – 2,900)

March 20 purchase (2,500 liters – 1,300)

FIFO ending inventory consists of:

March 20 purchase

2,500 @ $.80

$2,000

March 10 purchase

720

LIFO ending inventory consists of:

Beginning inventory

2,000 @ $.60

$1,200

March 3 purchase

(b) Companies can choose a cost flow method that produces the highest

PROBLEM 6-7A

(a) DANICA CO.

Condensed Income Statement

For the Year Ended December 31, 2017

FIFO

LIFO

Sales revenue …………………………………….. $735,000 $735,000

Cost of goods sold

Beginning inventory …………………….. 47,000 47,000

Cost of goods purchased ……………… 532,000 532,000

Gross profit ………………………………………… 301,600 284,600

Operating expenses ……………………………. 140,000 140,000

a(26,000 @ $5.60) = $145,600.

(b) Answers to questions:

(1) The FIFO method produces the most meaningful inventory amount

for the balance sheet because the units are costed at the most

recent purchase prices.

(4) There will be $5,100 additional cash available under LIFO because

income taxes are $43,380 under LIFO and $48,480 under FIFO.

*PROBLEM 6-8A

(a)

Sales:

January 8

110 units @ $28

$3,080

January 10 (return)

(10 units @ $28)

January 20

90 units @ $32

190 units

$5,680

(1)

LIFO

Date

Purchases

Cost of Goods Sold

Balance

January 1

(100 @ $15)

$1,500

January 5

(140 @ $18) $2,520

(100 @ $15)

}

$4,020

(140 @ $18)

January 8

(110 @ $18) $1,980

(100 @ $15)

( 30 @ $18)

January 10

(100 @ $15)

( 40 @ $18)

January 15

( 55 @ $20) $1,100

(100 @ $15)

}

$3,320

( 40 @ $18)

( 55 @ $20)

January 16

( –5 @ $20) ($ 100)

(100 @ $15)

}

( 50 @ $20)

( 50 @ $20)

}

$1,720

January 20

( 40 @ $18)

(100 @ $15)

}

(100 @ $15)

$3,520

( 20 @ $22)

$1,500