CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Prob. 20–4B (FIN MAN); Prob. 6–4B (MAN) (Continued)

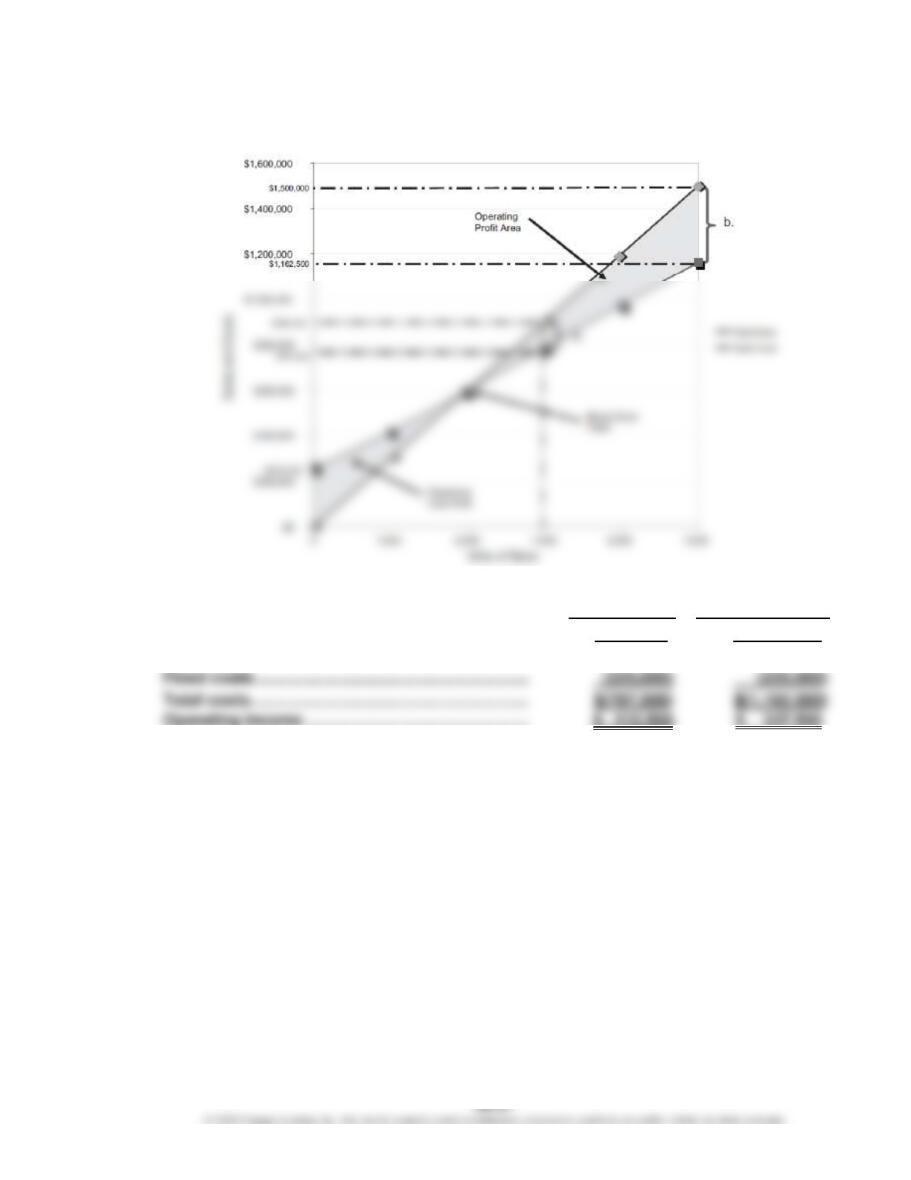

2.

(a)

4,500 units

(b)

7,500 units

Sales ……………………………………………………………

$ 900,000

$ 1,500,000

Variable costs ………………………………………………

$(562,500)

$ (937,500)

Total costs ……………………………………………………

Operating income …………………………………………

$ 112,500

$ 337,500

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Prob. 20–4B (FIN MAN); Prob. 6–4B (MAN) (Continued)

3.

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Prob. 20-4B (FIN MAN); Prob. 6-4B (MAN) (Continued)

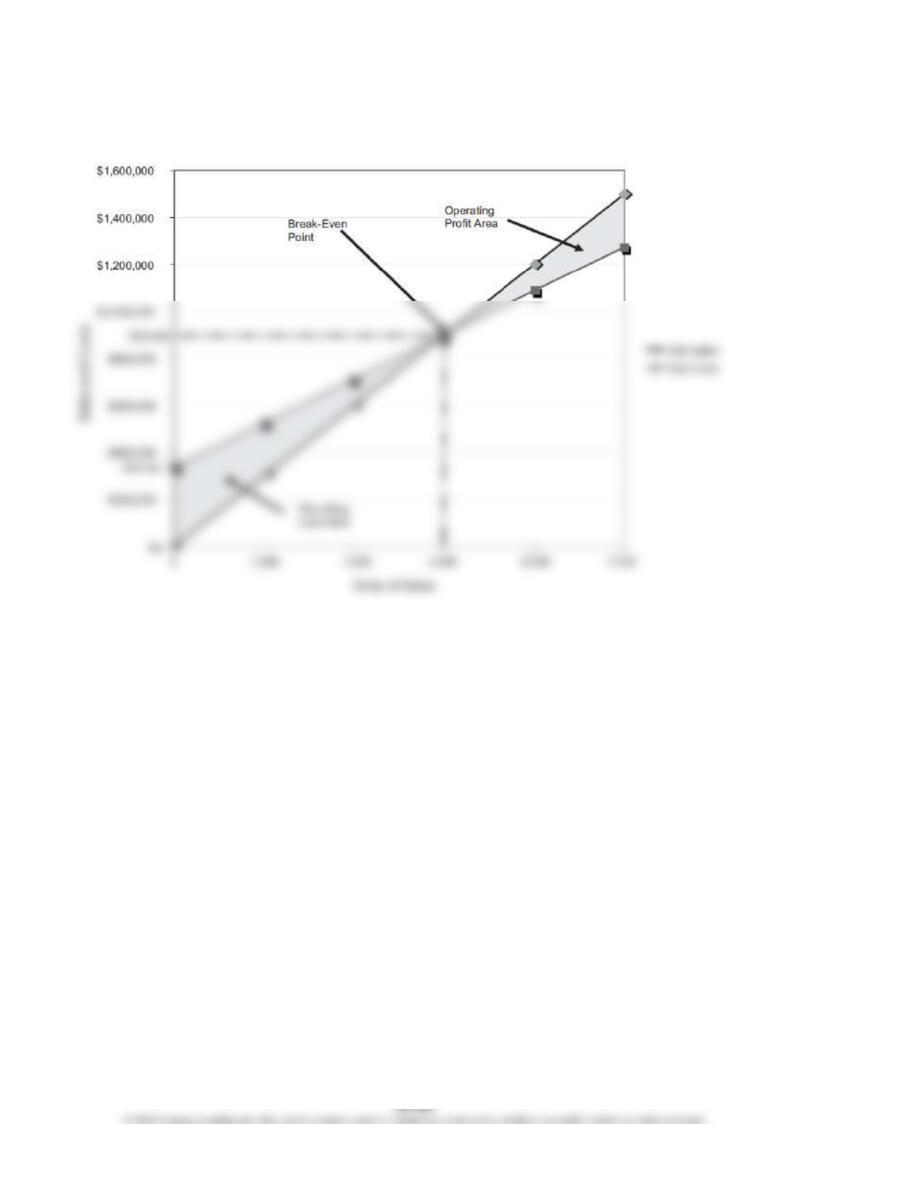

3. Break-Even Units:

–Total Fixed Costs Total Fixed Costs

Break Even Sales (units) = =

Unit Contribution Margin Unit Selling Price – Unit Variable Cost

$225,000 + $112,500

= $2 = 4,500units

00 Unit Selling Price – $125 Unit Variable Cost

Break-Even Dollars:

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Prob. 20–4B (FIN MAN); Prob. 6–4B (MAN) (Concluded)

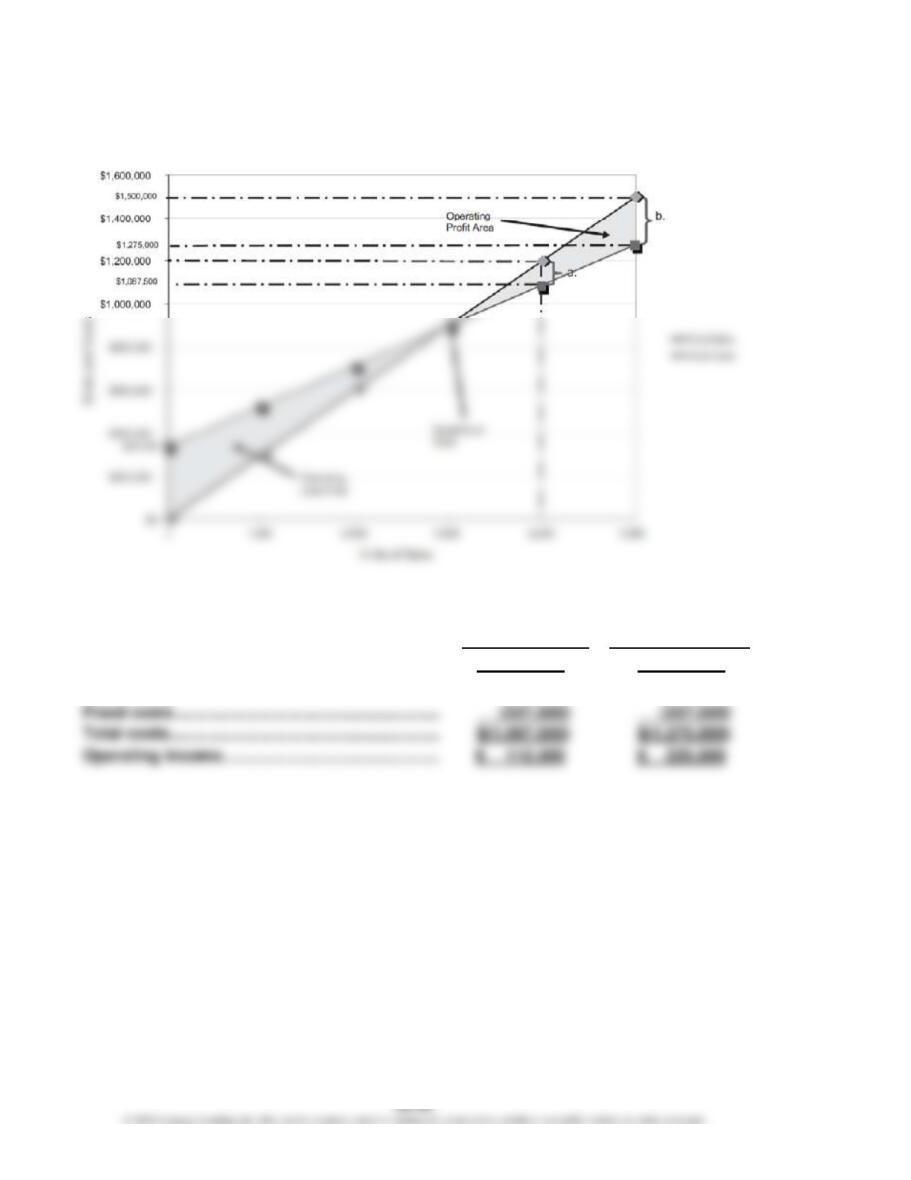

4.

(a)

6,000 units

(b)

7,500 units

Sales ………………………………………………………….

$ 1,200,000

$ 1,500,000

Variable costs ……………………………………………..

$ (750,000)

$ (937,500)

Operating income ………………………………………..

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Prob. 20–5B (FIN MAN); Prob. 6–5B (MAN)

(Overall enterprise product is labeled E.)

2. 4,500 units of E × 30% = 1,350 units of 12-inch pizza

4,500 units of E × 70% = 3,150 units of 16-inch pizza

3.

Unit selling price of E [($12 × 50%) + ($15 × 50%)] ……………………………………..

$13.50

Unit variable cost of E [($3 × 50%) + ($4 × 50%)] ………………………………………..

(3.50)

4,680 units of E × 50% = 2,340 units of 12-inch pizza

4,680 units of E × 50% = 2,340 units of 16-inch pizza

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Prob. 20–6B (FIN MAN); Prob. 6–6B (MAN)

1.

Belmain Co.

Estimated Income Statement

For the Year Ended December 31, 20Y7

Sales (12,000 × $240)

$ 2,880,000

Cost of goods sold:

Factory overhead [$350,000 + (12,000 × $6)]

Expenses:

Selling expenses:

Sales salaries and commissions

[$340,000 + (12,000 × $4)]

$388,000

Advertising

116,000

Travel

4,000

Miscellaneous selling expense

[$2,300 + (12,000 × $1)]

14,300

$325,000

Supplies [$6,000 + (12,000 × $4)]

Miscellaneous administrative expense

[$8,700 + (12,000 × $1)]

20,700

Total expenses

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Prob. 20–6B (FIN MAN); Prob. 6–6B (MAN) (Continued)

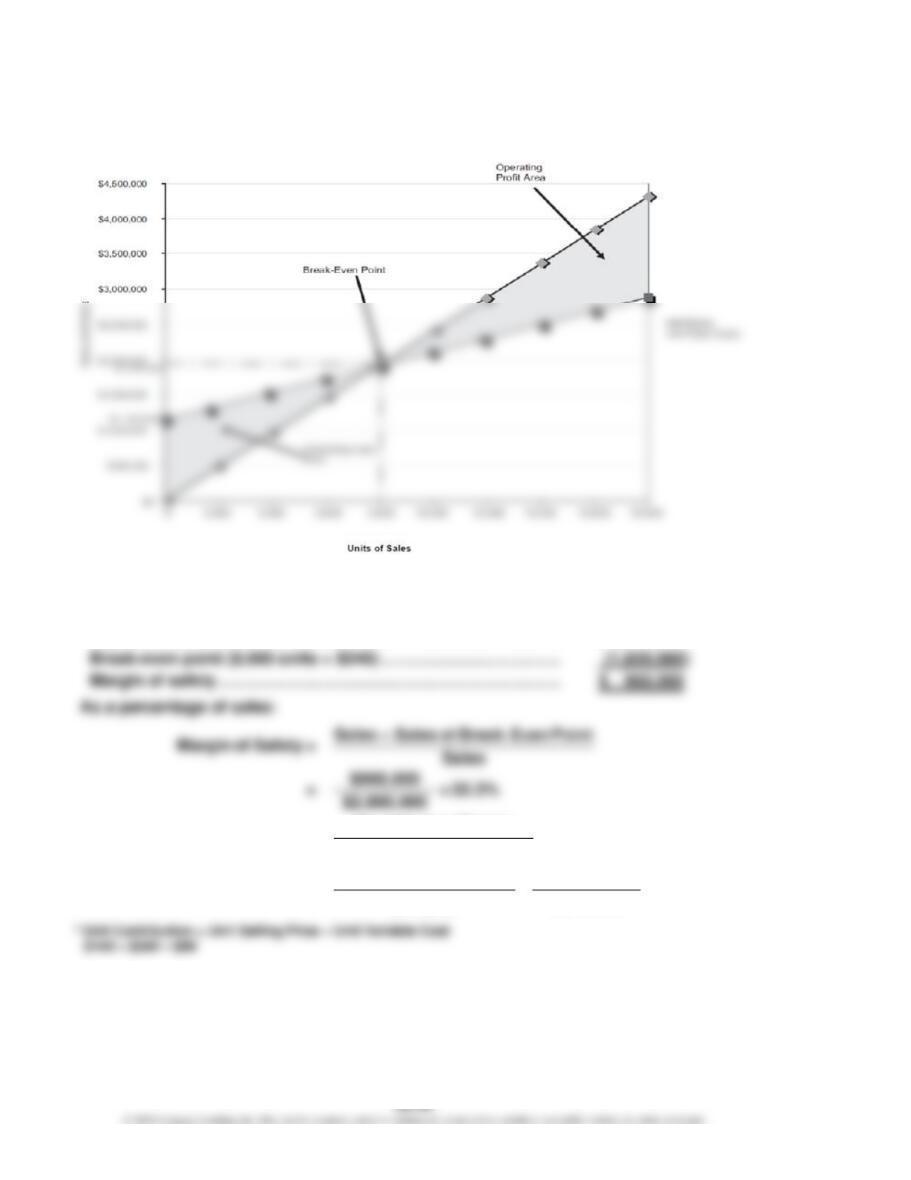

2.

Contribution Margin Ratio

=

Sales – Variable Costs

3.

Break-Even Sales (units)

=

Fixed Costs

Unit Contribution Margin

=

$1,152,000 = 8,000units

=

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Prob. 20–6B (FIN MAN); Prob. 6–6B (MAN) (Concluded)

4.

5.

Margin of safety:

In dollars:

Expected sales (12,000 units × $240) ………………………………….

$ 2,880,000

*

Contribution Margin

6. Operating Leverage = Operating Income

12,000 units × $144 $1,728,000

= =

$576,000 $576,000 =3

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

MAKE A DECISION

MAD 20–1 (FIN MAN); MAD 6–1 (MAN)

a.

–

–

Fixed Costs

Break Even Sales (units) = Unit Contribution Margin

$80,000

Break Even Sales (units) = = 125 passengers

$760 – $120

d. First, the airline should consider the impact of the new flight on other flights to Los

Angeles. That is, the airline should determine whether the seats sold on the new

flight are truly incremental seats for the airline, or whether passengers are shifting

MAD 20–2 (FIN MAN); MAD 6–2 (MAN)

a.

Total fixed costs per cruise:

Crew ……………………………………………………………………………………….

$ 240,000

Fuel ………………………………………………………………………………………..

60,000

Fixed operating costs ………………………………………………………………

800,000

Total fixed costs per cruise …………………………………………………

$ 1,100,000

MAD 20–2 (FIN MAN); MAD 6–2 (MAN) (Concluded)

b. The break-even point is 1,000 passengers [from (a)]. If 900 passengers book the

cruise, that will be 100 passengers under the break-even point. The loss can be

calculated as:

(900 passengers – 1,000 passengers) × ($2,400 – $1,300) = $(110,000)

d. If the cruise is operating under break-even, the cruise line can take a number

of actions to improve the financial performance of the cruise:

1. The cruise line could cancel the cruise. This is an extreme response and

would require finding an alternative use for the boat, which is a significant

investment that cannot remain idle.

MAD 20–3 (FIN MAN); MAD 6–3 (MAN)

–

–

Fixed Costs

a. Break Even Sales (units) = Unit Contribution Margin

$3,000,000,000

Break Even Sales (units) = = 37,500,000 subscribers

$120 – $40

Fixed costs: $100,000,000 + $2,000,000,000 + $900,000,000 = $3,000,000,000

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

MAD 20–3 (FIN MAN); MAD 6–3 (MAN) (Concluded)

–$3,600,000,000

c. Break Even Sales (units) = = 37,500,000 subscribers

X – $40

MAD 20–4 (FIN MAN); MAD 6–4 (MAN)

–Fixed Costs

a. Break Even Sales (units) = Unit Contribution Margin

The unit contribution margin consists of both the per-guest contribution margin from

$50

b. The daily weekday profit can be determined by multiplying the number of units over

break-even by the contribution margin per guest per day, as follows:

(24,000 guests – 15,000 guests) × $50 per guest* = $450,000

* See the calculation in (a).

e. The average daily admissions are 24,000 for the average weekday. Thus, the park

still operates above break-even and is therefore profitable with the increased

fixed costs. The daily profit would be $200,000 (4,000 guests above break-even

per day × $50 contribution margin per guest per day).

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

TAKE IT FURTHER

TIF 20–1 (FIN MAN); TIF 6–1 (MAN)

In an absolute sense, Edward’s actions are devious. He is clearly attempting to use the

first four years, which are favorable, as a way to market the partnerships. However, in

substance, these are longer-term investments. After the first four years, the risk

TIF 20–2 (FIN MAN); TIF 6–2 (MAN)

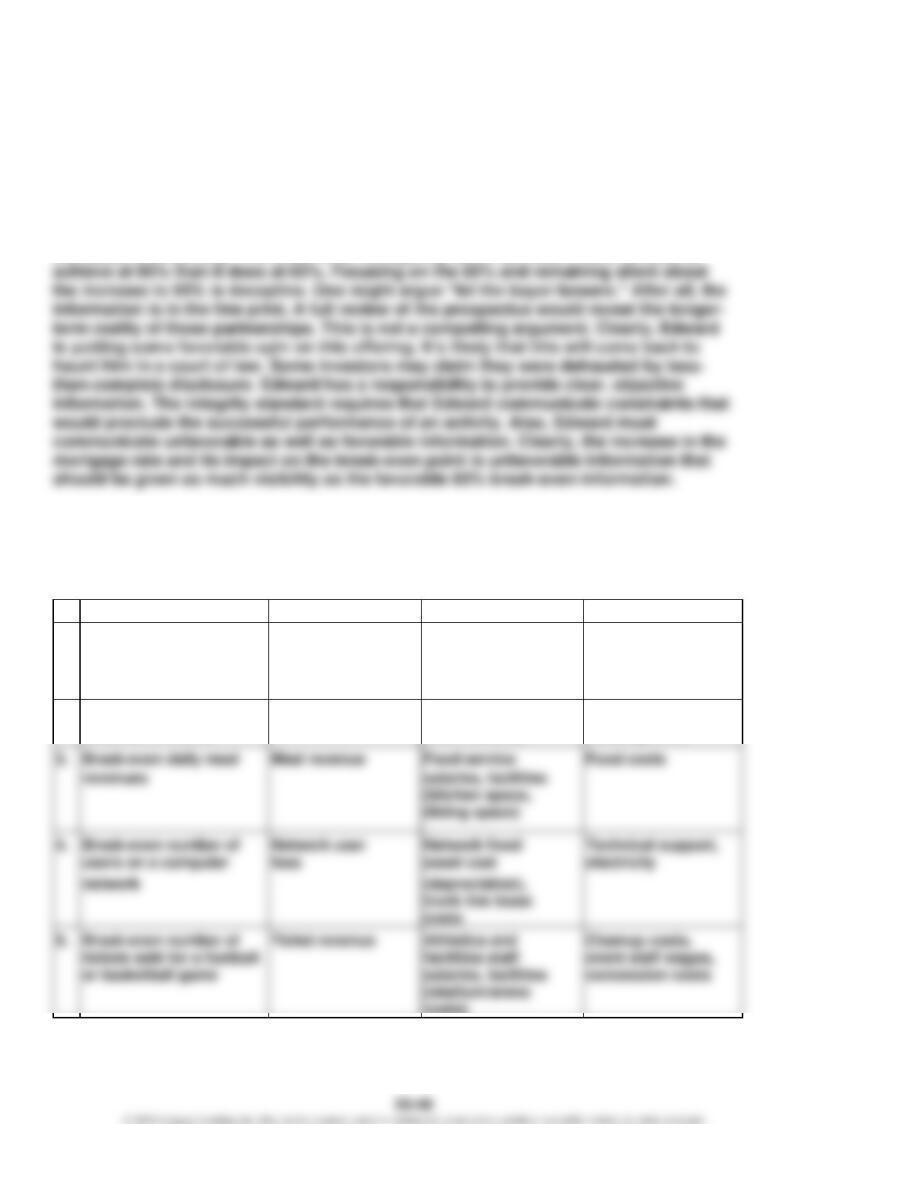

There are many possible applications of break-even analysis in a university environment.

Below are just a few possible ideas.

Break-Even Analysis

Revenues

Fixed Costs

Variable Costs

1.

Break-even number of

Student tuition for

Faculty salary,

Classroom supplies,

students in a class

a class

facilities (space,

classroom cleaning

classroom

costs

technology) costs

2.

Break-even number of

Room revenue

Facilities (space,

Operating supplies,

students in a dorm

room fixtures)

cleaning costs

revenues

salaries, facilities

(kitchen space,

4.

Break-even number of

Network user

Network fixed

Technical support,

network

(depreciation),

trunk line lease

costs

5.

Break-even number of

Ticket revenue

Athletics and

Cleanup costs,

tickets sold for a football

facilities staff

event staff wages,

or basketball game

salaries, facilities

concession costs

(stadium/arena

costs)

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

TIF 20–3 (FIN MAN); TIF 6–3 (MAN)

Memo

To: Neil Armstrong, CEO Sun Airlines

From: Ima Student

Re: Increasing Ticket Prices

In recent months, Sun Airlines has struggled to stay above break-even sales volume,

which has led to a string of monthly losses. Sun’s break-even volume is 75% of

capacity, which is significantly higher than the industry average of 65% of capacity.

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

TIF 20–4 (FIN MAN); TIF 6–4 (MAN)

Do-Nothing Strategy:

Revenue – Variable Costs – Fixed Costs

=

Profit

($80 × 1,000,000) – ($35 × 1,000,000) – $35,000,000

=

Profit

$120,000,000 – $70,000,000 – $35,000,000

=

$15,000,000

TIF 20–5 (FIN MAN); TIF 6–5 (MAN)

The direct labor costs are not variable to the increase in unit volume. The unit

volume is the wrong activity base for direct labor costs. The “number of

impressions” is a more accurate reflection of the direct labor cost. An impression

is a separate printing color application on the banners. Thus, the analysis should

be done as follows:

One

Two

Three

Four

Color

Color

Color

Color

Total

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

TIF 20–6 (FIN MAN); TIF 6–6 (MAN)

The Shipping Department manager should respond by pointing out that the

activities performed by his department are not related to sales volume but to

sales orders. The orders require inventory pulling and sorting activities as well

as paperwork activities. Thus, even though the sales volume is decreasing, the

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

CERTIFIED MANAGEMENT ACCOUNTANT (CMA®)

EXAMINATION QUESTIONS (ADAPTED)

1. a. A costs are semivariable or mixed, because they vary between quantities but do

2. c. Kimber’s total manufacturing cost is expected to be $615,000, computed as

follows:

3. c. Bolger’s break-even point would increase by 375 units, computed as follows:

Revised break-even point [$350,000 ÷ ($300 – $220)]

4,375

units

Current break-even point [$360,000 ÷ ($300 – $210)]

(4,000)

units

Increase in break-even point

375

units

4. b. To maximize contribution margin, Eagle Brand should produce 250 units of

Product X at $20 contribution margin per unit for a total of $5,000. The total

contribution margin for each of the alternatives is as follows:

Alternative A:

100 units × ($130 – $100) = $3,000