CHAPTER 6

SOLUTIONS TO EXERCISES—SET B

EXERCISE 6-1B

Ending inventory—physical count …………………………………………. $255,000

1. Add to inventory: Title passed to Markham when goods

were shipped ……………………………………………………………… 22,000

2. No effect—title does not transfer to Markham until

goods are received ……………………………………………………… 0

EXERCISE 6-2B

Ending inventory—as reported ………………………………………………. $550,000

1. No effect—title does not pass to Hobson until

goods are received (Jan. 3) ………………………………………….. 0

2. Subtract from inventory: The goods belong to

Discland Corporation. Hobson is merely holding

them as a consignee ……………………………………………………. (170,000)

3. Subtract from inventory: Office supplies should

5. Add to inventory: Gavin ordered goods

with a cost of $6,000. Hobson should record the

corresponding sales revenue of $10,000. Hobson’s

decision to ship extra “unordered” goods does not

constitute a sale. The manager’s statement that Gavin

EXERCISE 6-2B (Continued)

6. Subtract from inventory: GAAP require that inventory

be valued at the lower of cost or market. Obsolete parts

EXERCISE 6-3B

(a) FIFO Cost of Goods Sold

(b) It could choose to sell specific units purchased at specific costs if it

wished to impact earnings selectively. If it wished to minimize earnings

it would choose to sell the units purchased at higher costs—in which

(c) I recommend they use the FIFO method because it produces a more

appropriate balance sheet valuation and reduces the opportunity to

manipulate earnings.

EXERCISE 6-4B

FIFO

Beginning inventory (20 X $120) ……………………………….. $ 2,400

Purchases

July 12 (35 X $125) …………………………………………….. $4,375

July 19 (15 X $128) …………………………………………….. 1,920

EXERCISE 6-4B (Continued)

Proof

Date

Units

Unit Cost

Total Cost

7/1

20

$120

$ 2,400

7/12

35

7/19

15

7/26

18

88

LIFO

Cost of goods available for sale ……………………………….. $13,895

Less: Ending inventory (20 X $120) ………………………….. $2,400

Proof

Date

Units

Unit Cost

Total Cost

7/26

40

$130

$ 5,200

7/19

15

7/12

33

4,125

88

$11,245

(b)

Cost of

goods

EXERCISE 6-5B

FIFO

Beginning inventory (40 X $7) ………………………………………. $ 280

Purchases

May 15 (32 X $10) ………………………………………………….. $320

EXERCISE 6-5B (Continued)

Proof

Date

Units

Unit Cost

Total Cost

5/1

40

$ 7

$280

5/15

32

5/24

LIFO

Proof

Date

Units

Unit Cost

Total Cost

5/24

45

$495

5/15

32

5/1

EXERCISE 6-6B

(a) FIFO

Beginning inventory (250 X $7)…………………………. $1,750

Purchases

June 12 (325 X $8) …………………………………….. $2,600

EXERCISE 6-6B (Continued)

(b) The FIFO method will produce the higher ending inventory because

costs have been rising. Under this method, the earliest costs are

(c) The LIFO method will produce the higher cost of goods sold for Tevis

Company. Under LIFO the most recent costs are charged to cost of

EXERCISE 6-7B

(a) 1. FIFO

Beginning inventory …………………………………… $ 8,000

Purchases …………………………………………………. 33,000

Cost of goods available for sale ………………….. 41,000

2. LIFO

Beginning inventory …………………………………… $ 8,000

Purchases …………………………………………………. 33,000

3. AVERAGE

Beginning inventory …………………………………… $ 8,000

Purchases …………………………………………………. 33,000

(b) The use of FIFO would result in the highest net income since the earlier

lower costs are matched with revenues.

EXERCISE 6-8B

(a)

Cost of Goods

Available for Sale

$8,625

÷

Total Units

Available for Sale

1,050

=

Weighted Average

Unit Cost

$8.2143

(b) Ending inventory is lower than FIFO ($990) and higher than LIFO

(c) The average-cost method uses a weighted-average unit cost, not a simple

average of unit costs.

EXERCISE 6-9B

Cost

Market

Lower

of Cost

or Market:

Cameras

Minolta

$ 900

$1,000

$ 900

Total

Light meters

Vivitar

1,320

1,440

1,320

Kodak

Total

Total inventory

$4,760

EXERCISE 6-10B

Cost

Market

Lower

of Cost

or Market:

Cameras

$11,000

$10,000

10,000

DVD players

21,000

19,500

19,500

iPods

EXERCISE 6-11B

2016

2017

Beginning inventory ……………………………………. $ 27,000 $ 36,000

Cost of goods purchased …………………………….. 200,000 235,000

EXERCISE 6-12B

(a)

2016

2017

Sales revenue ………………………………………….. $300,000 $350,000

Cost of goods sold

Beginning inventory ………………………….. 40,000 48,000

Cost of goods purchased …………………… 186,000 217,000

(b) The cumulative effect on total gross profit for the two years is zero as

shown below:

Incorrect gross profits: $129,000 + $131,000 = $260,000

(c) Dear Mr./Ms. President:

Because your ending inventory of December 31, 2016 was overstated

by $7,000, your net income for 2016 was overstated by $7,000. For 2017

net income was understated by $7,000.

In a periodic system, the cost of goods sold is calculated by deducting

EXERCISE 6-12B (Continued)

The error also affects the balance sheet at the end of 2016. The inven-

tory reported in the balance sheet is overstated; therefore, total assets

are overstated. The overstatement of the 2016 net income results in the

EXERCISE 6-13B

2015

2016

2017

Inventory

turnover

$1,400,000

$1,440,000

$1,740,000

($120,000 + $280,000) ÷ 2

($280,000 + $200,000) ÷ 2

($200,000 + $400,000) ÷ 2

$1,400,000

= 7.0 times

$1,440,000

= 6.0 times

$1,740,000

= 5.8 times

$200,000

$240,000

$300,000

Days in

inventory

= 52.1 days

= 60.8 days

= 62.9 days

The inventory turnover ratio decreased by approximately 17% from 2015 to

2017 while the days in inventory increased by almost 21% over the same

EXERCISE 6-14B

(a)

Brady Company

Perez Company

Inventory Turnover

$280,000

$394,000

(b) Perez Company is moving its inventory more quickly, since its inventory

*EXERCISE 6-15B

(1)

FIFO

Date

Purchases

Cost of Goods Sold

Balance

Jan. 1

(3 @ $500) $1,500

8

(2 @ $500) $1,000

(1 @ $500) 500

(6 @ $640) $3,840

(1 @ $500)

(6 @ $640) 4,340

(1 @ $500)

(2)

LIFO

Date

Purchases

Cost of Goods Sold

Balance

Jan. 1

(3 @ $500) $1,500

8

(2 @ $500) $1,000

(1 @ $500) 500

(6 @ $640) $3,840

(1 @ $500)

(6 @ $640) 4,340

(4 @ $640) $2,560

(1 @ $500)

(2 @ $640) 1,780

*EXERCISE 6-15B (Continued)

(3)

AVERAGE-COST

Date

Purchases

Cost of Goods Sold

Balance

Jan. 1

(3 @ $500) $1,500

8

(2 @ $500) $1,000

(1 @ $500) 500

(6 @ $640) $3,840

(7 @ $620)* 4,340

(4 @ $620) $2,480

(3 @ $620) 1,860

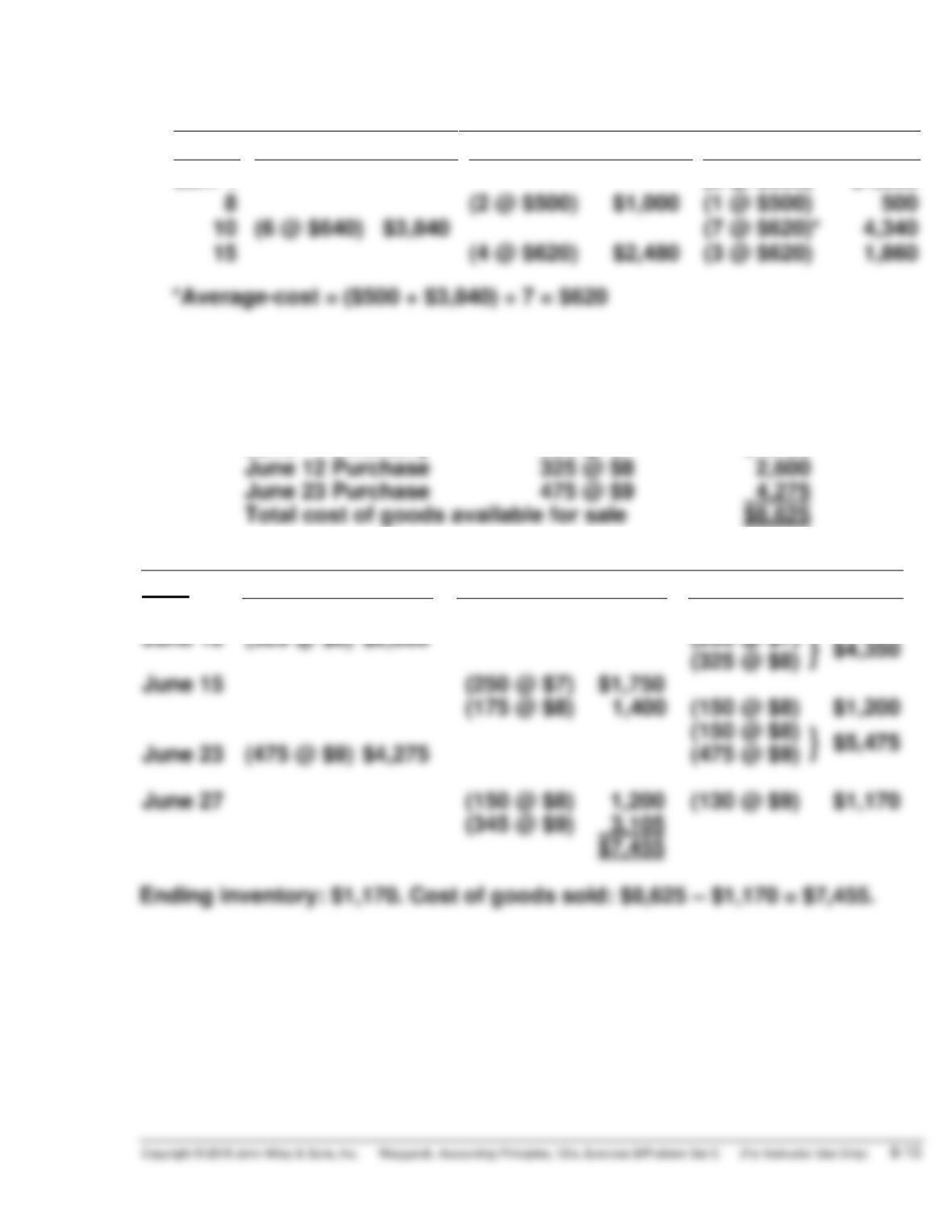

*EXERCISE 6-16B

(a) The cost of goods available for sale is:

June 1 Inventory

250 @ $7

$1,750

June 12 Purchase

325 @ $8

June 23 Purchase

475 @ $9

Total cost of goods available for sale

$8,625

FIFO

Date

Purchases

Cost of Goods Sold

Balance

June 1

(250 @ $7)

$1,750

June 12

(325 @ $8) $2,600

(250 @ $7)

(325 @ $8)

June 15

(250 @ $7)

(175 @ $8)

(150 @ $8)

$1,200

(150 @ $8)

June 23

(475 @ $9) $4,275

(475 @ $9)

June 27

(150 @ $8)

(130 @ $9)

$1,170

(345 @ $9)

*EXERCISE 6-16B (Continued)

LIFO

Date

Purchases

Cost of Goods Sold

Balance

June 1

(250 @ $7)

$1,750

June 12

(325 @ $8) $2,600

(250 @ $7)

}

$4,350

(325 @ $8)

June 15

(150 @ $7)

$1,050

(150 @ $7)

}

$5,325

June 23

(475 @ $9) $4,275

(475 @ $9)

}

$ 910

June 27

Moving-Average

Date

Purchases

Cost of Goods Sold

Balance

June 1

(250 @ $7) $1,750

June 12

(325 @ $8) $2,600

(575 @ $7.57) $4,350

June 15

(425 @ $7.57)

$3,217

(150 @ $7.55) $1,133

June 23

(475 @ $9) $4,275

(625 @ $8.65) $5,408

June 27

(495 @ $8.65)

$4,282

(130 @ $8.66) $1,126

(b) FIFO gives the same ending inventory and cost of goods sold values

under both the periodic and perpetual inventory system. LIFO and

(c) The simple average would be [($7 + $8 + $9) ÷ 3)] or $8. However, the

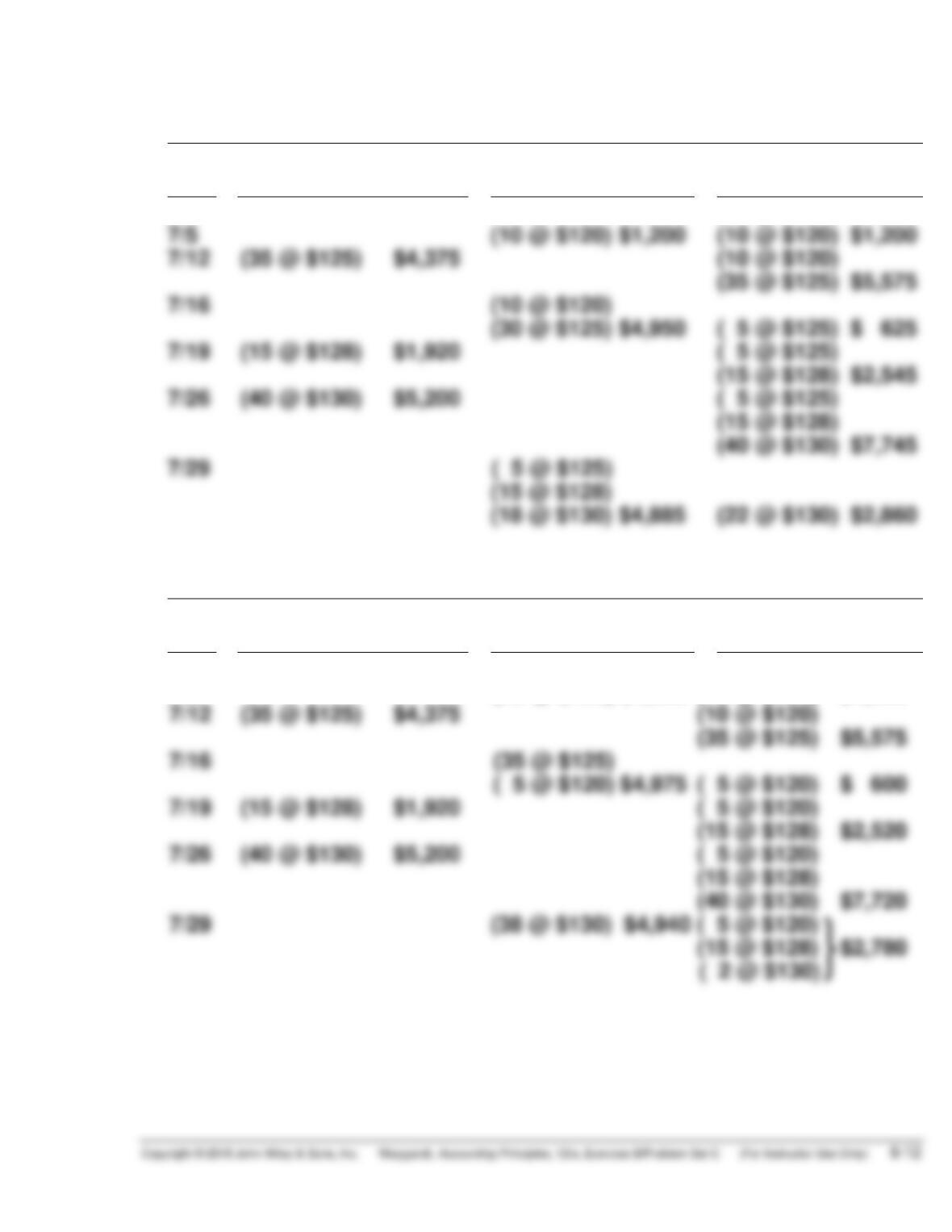

*EXERCISE 6-17B

(a)

FIFO

Date

Purchases

Cost of

Goods Sold

Balance

7/1

(20 @ $120) $2,400

7/5

(10 @ $120) $1,200

(10 @ $120) $1,200

7/12

(35 @ $125) $4,375

(10 @ $120)

(35 @ $125) $5,575

7/16

(10 @ $120)

(30 @ $125) $4,950

( 5 @ $125) $ 625

7/19

(15 @ $128) $1,920

( 5 @ $125)

(15 @ $128) $2,545

7/26

(40 @ $130) $5,200

( 5 @ $125)

(15 @ $128)

(40 @ $130) $7,745

7/29

(15 @ $128)

LIFO

Date

Purchases

Cost of

Goods Sold

Balance

7/1

(20 @ $120) $2,400

7/5

(10 @ $120) $1,200

(10 @ $120) $1,200

7/12

(35 @ $125) $4,375

(10 @ $120)

(35 @ $125) $5,575

7/16

(35 @ $125)

( 5 @ $120) $4,975

( 5 @ $120) $ 600

7/19

(15 @ $128) $1,920

( 5 @ $120)

(15 @ $128) $2,520

7/26

(40 @ $130) $5,200

( 5 @ $120)

(15 @ $128)

(40 @ $130) $7,720

7/29

(38 @ $130)

( 5 @ $120)

(15 @ $128) $2,780

*EXERCISE 6-17B (Continued)

Average-Cost

Date

Purchases

Cost of

Goods Sold

Balance

7/1

(20 @ $120) $2,400

7/5

(10 @ $120) $1,200

(10 @ $120) $1,200

7/12

(35 @ $125) $4,375

(45 @ $123.889*) $5,575

7/16

(40 @ $123.889) $4,956*

( 5 @ $123.889*) $ 619

7/19

(15 @ $128) $1,920

(20 @ $126.95) $2,539

7/26

(40 @ $130) $5,200

(60 @ $128.983*) $7,739

7/29

*Rounded

(b)

Periodic

Perpetual

Ending Inventory FIFO

$2,860

$2,860

Ending Inventory LIFO

$2,650

$2,780

*EXERCISE 6-18B

(a) Sales revenue ………………………………………………. $1,000,000

Cost of goods sold

Inventory, November 1 …………………………. $140,000

*EXERCISE 6-18B (Continued)

(b) Sales revenue ……………………………………………………………… $1,200,000

Less: Estimated gross profit (38% X $1,200,000) …………… 456,000

Estimated cost of goods sold ……………………………………….. $ 744,000

*EXERCISE 6-19B

(a) Net sales ($105,000 – $5,000) ………………………………………… $100,000

Less: Estimated gross profit (40% X $100,000) ……………… 40,000

Estimated cost of goods sold ……………………………………….. $ 60,000

(b) Net sales ……………………………………………………………………… $100,000

Less: Estimated gross profit (30% X $100,000) ……………… 30,000

Estimated cost of goods sold ……………………………………….. $ 70,000

*EXERCISE 6-20B

Adult’s

Department

Kid’s

Department

Cost

Retail

Cost

Retail

Beginning inventory

$ 40,000

$ 57,000

$ 50,000

$ 77,000

Goods purchased

Net sales

Ending inventory at retail

$ 70,000

$140,000

$195,000

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 6-1C

(a) Title to the goods does not transfer to the customer until March 2.

Include the $800 in ending inventory.

(b) Mareska owns the goods once they are shipped on February 26.

Include inventory of $375.